Key Insights

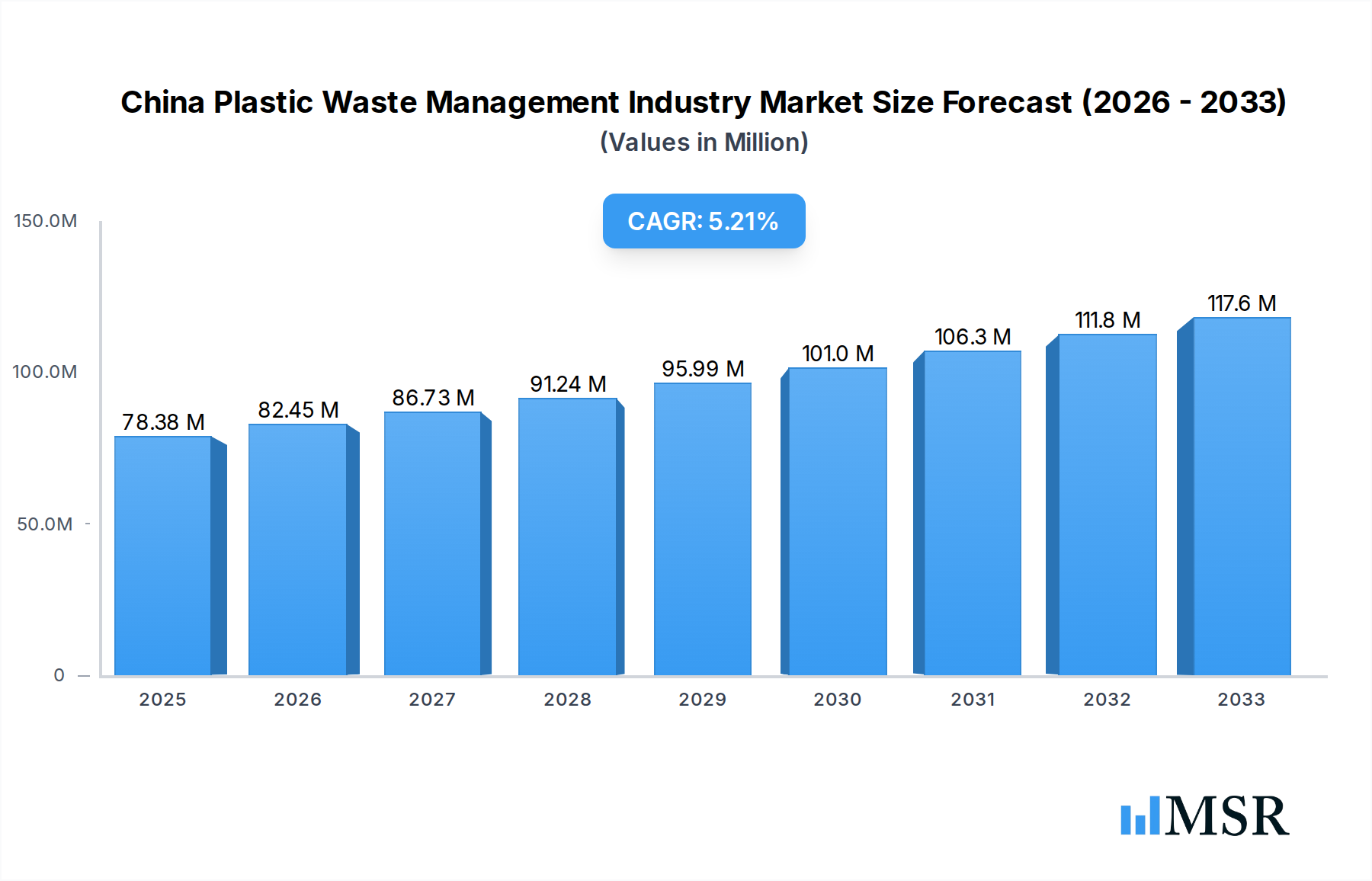

The China Plastic Waste Management Industry is poised for significant growth, driven by increasing plastic consumption and a growing imperative for sustainable waste solutions. With an estimated market size of USD 78.38 million in 2025, the industry is projected to expand at a Compound Annual Growth Rate (CAGR) of 5.25% through 2033. This robust growth is underpinned by the escalating volume of plastic waste generated from various sectors, including municipal solid waste, industrial byproducts, and the burgeoning e-waste stream. Emerging trends like advanced recycling technologies, the circular economy model, and enhanced public-private partnerships are key catalysts, fostering innovation and investment in more efficient waste processing and resource recovery. Government initiatives promoting waste reduction, segregation at source, and the development of infrastructure for plastic waste management are further bolstering market expansion, creating a favorable ecosystem for both domestic and international players.

China Plastic Waste Management Industry Market Size (In Million)

The industry faces several key drivers, including stringent environmental regulations aimed at curbing plastic pollution, growing consumer awareness regarding sustainability, and the economic benefits derived from recycling and resource recovery. The demand for recycled plastics in manufacturing, coupled with the need for safe disposal of hazardous and bio-medical plastic waste, presents substantial opportunities. However, challenges such as the high cost of advanced waste management technologies, the need for widespread public participation in waste segregation, and the logistical complexities of collecting and processing diverse plastic waste streams require strategic solutions. Addressing these restraints through policy support, technological advancements, and awareness campaigns will be crucial for unlocking the full potential of China's plastic waste management market, ensuring a cleaner and more sustainable future.

China Plastic Waste Management Industry Company Market Share

Here is an SEO-optimized, engaging report description for the China Plastic Waste Management Industry, incorporating your specified keywords, structure, and content requirements.

China Plastic Waste Management Industry Report Description

Unlock the vast potential of China's plastic waste management market with this comprehensive, data-driven report. Delve into the intricate dynamics of a sector projected for significant growth, driven by escalating environmental concerns, robust government initiatives, and relentless technological innovation. This indispensable resource provides deep insights into the China plastic waste management market, plastic recycling China, waste to energy China, and circular economy China, essential for stakeholders navigating this complex landscape.

Our analysis spans the historical period of 2019–2024, with a base year of 2025, and offers an in-depth forecast period from 2025–2033. We meticulously examine key segments including industrial waste management China, municipal solid waste China, hazardous waste management China, e-waste recycling China, plastic waste solutions China, and bio-medical waste disposal China. Discover the dominant disposal methods such as landfill China, incineration China, dismantling China, and recycling China, alongside the prevalent ownership types: public, private, and public-private partnerships China.

This report is your definitive guide to understanding the market concentration, industry insights, key market segments, product developments, challenges, growth drivers, emerging opportunities, leading players, and strategic outlook within the China plastic waste management industry. Gain actionable intelligence on companies like China Everbright International Limited, Sembcorp Industries Ltd, Veolia Environnement S A, Capital Environmental Holdings Ltd (CEHL), and HydroThane, and comprehend the critical milestones shaping this vital sector.

Target Audience: Waste Management Companies, Recycling Businesses, Environmental Technology Providers, Government Agencies, Investment Firms, Policy Makers, Researchers, and Industry Consultants.

China Plastic Waste Management Industry Market Concentration & Dynamics

The China plastic waste management industry exhibits a dynamic market concentration, characterized by a growing number of specialized players alongside large, integrated conglomerates. While fragmented in certain niche areas, the overarching trend points towards consolidation driven by economies of scale and advanced technological adoption. The innovation ecosystem is thriving, spurred by government mandates for plastic recycling China and waste to energy China, fostering collaborations between research institutions and private enterprises. Regulatory frameworks are becoming increasingly stringent, with a strong emphasis on reducing virgin plastic production and promoting a circular economy China. Substitute products are emerging, particularly in biodegradable materials, though their widespread adoption is still in its nascent stages. End-user trends are shifting towards greater environmental consciousness, with businesses and consumers demanding more sustainable plastic waste solutions China. Mergers and acquisitions (M&A) activity is on the rise as established players seek to expand their capabilities and market reach, particularly in advanced e-waste recycling China and hazardous waste management China. For instance, M&A deal counts have seen a notable increase in the past two years, indicating active strategic realignment. Market share is increasingly influenced by companies demonstrating superior waste to energy China technologies and comprehensive municipal solid waste China management solutions.

China Plastic Waste Management Industry Industry Insights & Trends

The China plastic waste management industry is poised for substantial growth, projected to reach a market size of approximately 500,000 Million by the end of the forecast period, exhibiting a Compound Annual Growth Rate (CAGR) of over 8%. This expansion is fundamentally driven by a confluence of escalating environmental regulations and a heightened public awareness regarding the detrimental impacts of plastic pollution. The Chinese government's unwavering commitment to sustainability, as evidenced by its ambitious targets for waste reduction and plastic recycling China, acts as a significant market growth driver. Technological disruptions are continuously reshaping the industry, with advancements in waste to energy China technologies, such as pyrolysis and gasification, offering more efficient and environmentally sound methods of waste processing. Furthermore, the development of sophisticated sorting and separation technologies is enhancing the recovery rates of valuable materials, bolstering the circular economy China initiative. Evolving consumer behaviors, particularly a growing preference for eco-friendly products and services, are compelling businesses to adopt more sustainable practices, thereby increasing the demand for effective plastic waste solutions China. The rise of the industrial waste management China sector is also a critical component, driven by the manufacturing boom and the need for responsible disposal of industrial by-products. Similarly, the burgeoning urban populations contribute to the steady increase in municipal solid waste China, necessitating advanced management strategies. The increasing focus on responsible disposal of hazardous waste management China and bio-medical waste disposal China further underscores the industry's growth trajectory. Investments in infrastructure for landfill China (though increasingly being phased out in favor of advanced methods), incineration China, and particularly recycling China facilities are crucial enablers of this growth. The public-private partnership China model is gaining traction, facilitating the deployment of large-scale projects that require substantial capital and operational expertise. The market is moving beyond traditional dismantling China processes towards more automated and efficient recovery methods. The increasing volume of e-waste recycling China presents both a challenge and a significant opportunity, as valuable metals and components can be reclaimed. The overarching trend is a shift towards a more integrated and technologically advanced approach to plastic waste management industry operations in China.

Key Markets & Segments Leading China Plastic Waste Management Industry

The China plastic waste management industry is dominated by the municipal solid waste (MSW) segment, driven by the sheer volume generated from its vast urban populations. This segment is further propelled by increasing government investments in advanced collection and processing infrastructure, including modern incineration China plants equipped with waste-to-energy capabilities and enhanced recycling China facilities. Economic growth and urbanization are key drivers, leading to a continuous rise in the generation of municipal solid waste China.

Waste Type Dominance:

- Municipal Solid Waste: The largest and fastest-growing segment, fueled by urbanization and consumption patterns. Drivers include population growth, rising disposable incomes, and government mandates for cleaner cities.

- Industrial Waste: A significant segment, driven by China's robust manufacturing sector. Growing environmental regulations are pushing industries towards more responsible waste management.

- Plastic Waste: This is a cross-cutting category heavily influencing other segments. The focus on plastic recycling China and the development of plastic waste solutions China are pivotal. Drivers include increasing consumer demand for plastic products and evolving policies for a circular economy China.

- E-waste: Rapid technological advancements and shorter product lifecycles contribute to its growing volume. The recovery of valuable metals and the management of hazardous components are key focal points.

- Hazardous Waste: Strict regulations and the need for specialized treatment and disposal make this a critical but complex segment.

- Bio-medical Waste: Driven by an expanding healthcare sector, requiring stringent containment and disposal protocols.

Disposal Method Dominance:

- Incineration: Increasingly favored for its ability to reduce waste volume and generate energy (Waste-to-Energy). Advanced incineration China technologies are crucial. Drivers include land scarcity for landfills and environmental benefits.

- Recycling: Experiencing significant growth, particularly for plastics and metals. The push for a circular economy China is a major catalyst. Drivers include resource conservation and economic incentives.

- Landfill: While still in use, its dominance is declining as newer, more sustainable methods are adopted. Stricter regulations and environmental concerns are diminishing its role.

- Dismantling: Primarily relevant for e-waste and complex industrial components, focusing on material recovery.

Type of Ownership Dominance:

- Public-Private Partnership (PPP): This model is increasingly dominant for large-scale infrastructure projects, leveraging both public sector oversight and private sector efficiency and capital. This structure is particularly prevalent in developing advanced waste to energy China and comprehensive municipal solid waste China management systems. Drivers include the need for significant investment, risk sharing, and technological expertise.

- Private: Growing rapidly, especially in specialized services like e-waste recycling China and advanced hazardous waste management China. Driven by innovation and market demand for efficient solutions.

- Public: While still significant, especially in basic waste collection, public entities are increasingly collaborating with private firms for specialized management.

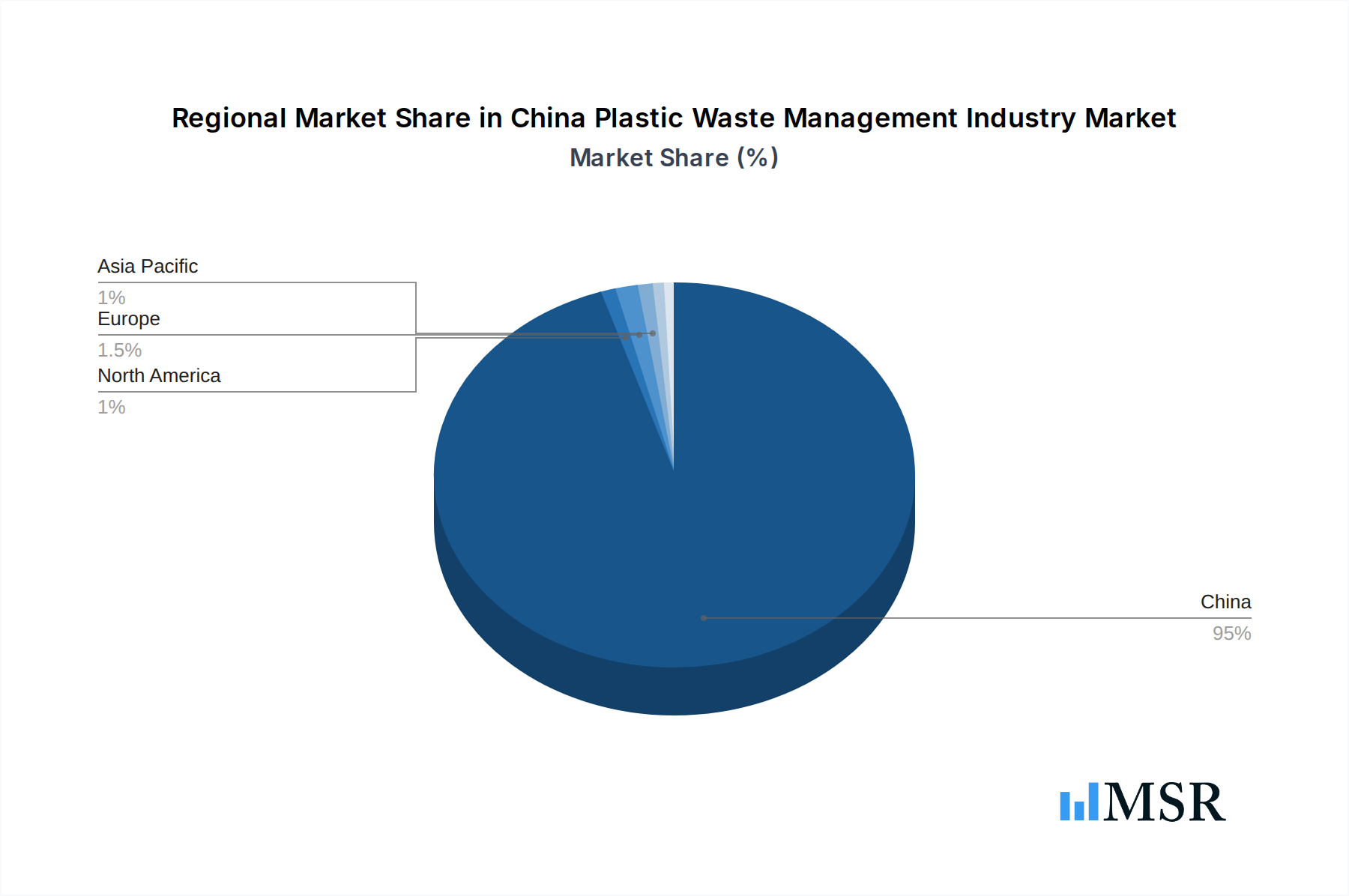

Geographically, the coastal regions and major metropolitan areas are leading the China plastic waste management industry due to higher population density, industrial activity, and greater implementation of advanced waste management policies.

China Plastic Waste Management Industry Product Developments

Recent product developments in the China plastic waste management industry are heavily focused on enhancing the efficiency and sustainability of recycling and waste-to-energy processes. Innovations in automated sorting technologies, utilizing AI and machine learning, are significantly improving the separation of various plastic types and contaminants, thereby increasing the quality and value of recycled materials. Advanced chemical recycling techniques, such as pyrolysis and depolymerization, are gaining traction, enabling the conversion of mixed and contaminated plastic waste into valuable feedstocks for new plastic production. Furthermore, the development of more efficient waste to energy China conversion technologies, including advanced incineration and anaerobic digestion systems, is maximizing energy recovery while minimizing emissions. These product developments are critical for advancing the circular economy China and providing scalable plastic waste solutions China.

Challenges in the China Plastic Waste Management Industry Market

The China plastic waste management industry faces several critical challenges. One significant hurdle is the uneven development of collection and sorting infrastructure across different regions, leading to inefficiencies in waste streams. The presence of mixed waste, particularly in the municipal solid waste China sector, complicates advanced recycling and waste to energy China processes. Furthermore, fluctuations in the global market prices for recycled materials can impact the economic viability of recycling operations. Regulatory enforcement can also be inconsistent, creating an uneven playing field. The sheer scale of plastic waste generation and the need for rapid technological adoption to meet ambitious environmental targets also present substantial operational challenges.

Forces Driving China Plastic Waste Management Industry Growth

Several key forces are propelling the growth of the China plastic waste management industry. Stringent government policies and targets for waste reduction and recycling, coupled with financial incentives for sustainable practices, are primary drivers. Rapid urbanization and industrialization are increasing the volume of waste generated, necessitating more advanced management solutions. Technological advancements in plastic recycling China, waste to energy China, and e-waste recycling China are offering more efficient and environmentally sound processing methods. Growing public awareness and demand for sustainable products and services are also influencing business practices and driving investment in the sector. The active promotion of a circular economy China framework by the government provides a strong impetus for innovation and market expansion.

Challenges in the China Plastic Waste Management Industry Market

Long-term growth catalysts for the China plastic waste management industry lie in continued investment in research and development for next-generation recycling technologies, including advanced chemical recycling and biological methods for degrading plastics. Strategic partnerships between government, industry, and research institutions will be crucial for fostering innovation and scaling up successful solutions. Expansion into emerging regions within China that currently have less developed waste management infrastructure presents significant market opportunities. Furthermore, the development of robust domestic markets for recycled materials, supported by government procurement policies and industry standards, will create sustainable demand and de-risk investments in the plastic waste solutions China sector.

Emerging Opportunities in China Plastic Waste Management Industry

Emerging opportunities in the China plastic waste management industry are abundant and multifaceted. The increasing focus on e-waste recycling China due to the rapid obsolescence of electronics presents a significant growth area for specialized companies. The development of advanced bio-medical waste disposal China solutions, driven by an expanding healthcare sector, is another burgeoning opportunity. Furthermore, the push towards a fully realized circular economy China is creating demand for innovative business models focused on product lifespan extension, repair, and remanufacturing. Opportunities also exist in developing and implementing sophisticated hazardous waste management China solutions for industries facing increasingly stringent regulations. The growing adoption of digital technologies for waste tracking and management, offering greater transparency and efficiency, is also a key emerging trend.

Leading Players in the China Plastic Waste Management Industry Sector

- China Everbright International Limited

- Sembcorp Industries Ltd

- Veolia Environnement S A

- Capital Environmental Holdings Ltd (CEHL)

- HydroThane

Key Milestones in China Plastic Waste Management Industry Industry

- 2019: Increased government focus on reducing single-use plastics, leading to policy shifts and heightened awareness for plastic recycling China.

- 2020: Significant investments in waste to energy China projects to address landfill capacity issues and meet energy demands.

- 2021: Launch of initiatives to bolster the circular economy China, encouraging innovation in plastic waste solutions China.

- 2022: Growing emphasis on e-waste recycling China and the development of specialized facilities.

- 2023: Intensified regulatory efforts for hazardous waste management China and bio-medical waste disposal China.

- 2024: Continued expansion of public-private partnership China models for large-scale waste management infrastructure development.

Strategic Outlook for China Plastic Waste Management Industry Market

The strategic outlook for the China plastic waste management industry is overwhelmingly positive, marked by sustained growth and technological advancement. The ongoing commitment to environmental sustainability and the vigorous promotion of the circular economy China will continue to fuel investments in advanced plastic recycling China and waste to energy China technologies. The industry is expected to witness further consolidation as companies seek to achieve scale and offer integrated plastic waste solutions China. Emerging technologies in chemical recycling and the efficient management of complex waste streams like e-waste recycling China and hazardous waste management China will be key differentiators. Strategic collaborations and the expansion of public-private partnership China models will be crucial for overcoming infrastructure challenges and driving large-scale implementation, ensuring a cleaner and more sustainable future for China.

China Plastic Waste Management Industry Segmentation

-

1. Waste type

- 1.1. Industrial waste

- 1.2. Municipal solid waste

- 1.3. Hazardous waste

- 1.4. E-waste

- 1.5. Plastic waste

- 1.6. Bio-medical waste

-

2. Disposal methods

- 2.1. Landfill

- 2.2. Incineration

- 2.3. Dismantling

- 2.4. Recycling

-

3. Type of ownership

- 3.1. Public

- 3.2. Private

- 3.3. Public - Private Patnership

China Plastic Waste Management Industry Segmentation By Geography

- 1. China

China Plastic Waste Management Industry Regional Market Share

Geographic Coverage of China Plastic Waste Management Industry

China Plastic Waste Management Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Waste type

- 5.1.1. Industrial waste

- 5.1.2. Municipal solid waste

- 5.1.3. Hazardous waste

- 5.1.4. E-waste

- 5.1.5. Plastic waste

- 5.1.6. Bio-medical waste

- 5.2. Market Analysis, Insights and Forecast - by Disposal methods

- 5.2.1. Landfill

- 5.2.2. Incineration

- 5.2.3. Dismantling

- 5.2.4. Recycling

- 5.3. Market Analysis, Insights and Forecast - by Type of ownership

- 5.3.1. Public

- 5.3.2. Private

- 5.3.3. Public - Private Patnership

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Waste type

- 6. China Plastic Waste Management Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Waste type

- 6.1.1. Industrial waste

- 6.1.2. Municipal solid waste

- 6.1.3. Hazardous waste

- 6.1.4. E-waste

- 6.1.5. Plastic waste

- 6.1.6. Bio-medical waste

- 6.2. Market Analysis, Insights and Forecast - by Disposal methods

- 6.2.1. Landfill

- 6.2.2. Incineration

- 6.2.3. Dismantling

- 6.2.4. Recycling

- 6.3. Market Analysis, Insights and Forecast - by Type of ownership

- 6.3.1. Public

- 6.3.2. Private

- 6.3.3. Public - Private Patnership

- 6.1. Market Analysis, Insights and Forecast - by Waste type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China Everbright International Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sembcorp Industries Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Veolia Environnement S A

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Capital Environmental Holdings Ltd (CEHL)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 HydroThane**List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 China Everbright International Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Plastic Waste Management Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Plastic Waste Management Industry Share (%) by Company 2025

List of Tables

- Table 1: China Plastic Waste Management Industry Revenue Million Forecast, by Waste type 2020 & 2033

- Table 2: China Plastic Waste Management Industry Volume Billion Forecast, by Waste type 2020 & 2033

- Table 3: China Plastic Waste Management Industry Revenue Million Forecast, by Disposal methods 2020 & 2033

- Table 4: China Plastic Waste Management Industry Volume Billion Forecast, by Disposal methods 2020 & 2033

- Table 5: China Plastic Waste Management Industry Revenue Million Forecast, by Type of ownership 2020 & 2033

- Table 6: China Plastic Waste Management Industry Volume Billion Forecast, by Type of ownership 2020 & 2033

- Table 7: China Plastic Waste Management Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: China Plastic Waste Management Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 9: China Plastic Waste Management Industry Revenue Million Forecast, by Waste type 2020 & 2033

- Table 10: China Plastic Waste Management Industry Volume Billion Forecast, by Waste type 2020 & 2033

- Table 11: China Plastic Waste Management Industry Revenue Million Forecast, by Disposal methods 2020 & 2033

- Table 12: China Plastic Waste Management Industry Volume Billion Forecast, by Disposal methods 2020 & 2033

- Table 13: China Plastic Waste Management Industry Revenue Million Forecast, by Type of ownership 2020 & 2033

- Table 14: China Plastic Waste Management Industry Volume Billion Forecast, by Type of ownership 2020 & 2033

- Table 15: China Plastic Waste Management Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: China Plastic Waste Management Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Plastic Waste Management Industry?

The projected CAGR is approximately 5.25%.

2. Which companies are prominent players in the China Plastic Waste Management Industry?

Key companies in the market include China Everbright International Limited, Sembcorp Industries Ltd, Veolia Environnement S A, Capital Environmental Holdings Ltd (CEHL), HydroThane**List Not Exhaustive.

3. What are the main segments of the China Plastic Waste Management Industry?

The market segments include Waste type, Disposal methods, Type of ownership.

4. Can you provide details about the market size?

The market size is estimated to be USD 78.38 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Spotlight on the China e-waste generation and its effective management.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Plastic Waste Management Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Plastic Waste Management Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Plastic Waste Management Industry?

To stay informed about further developments, trends, and reports in the China Plastic Waste Management Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence