Key Insights

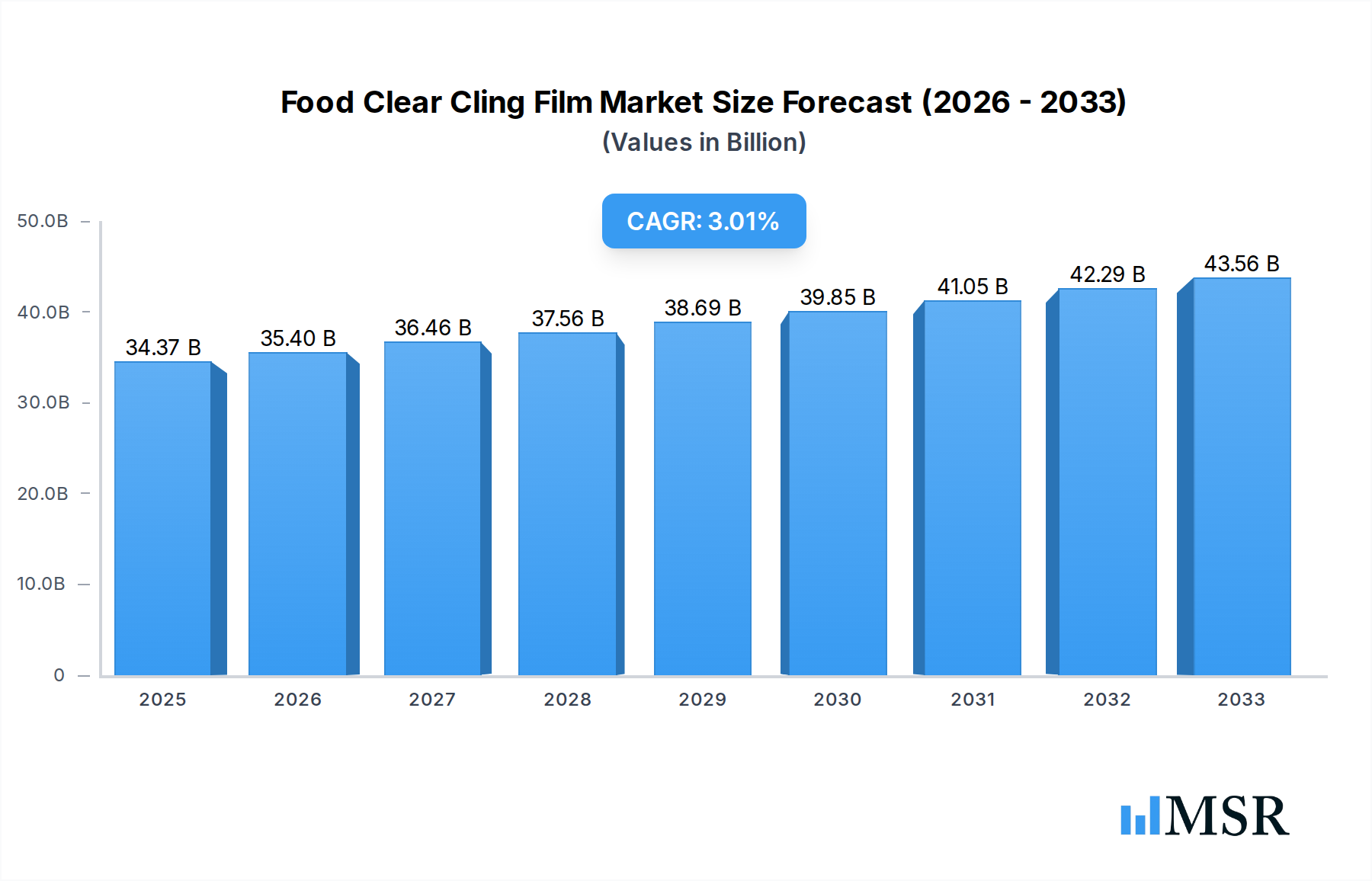

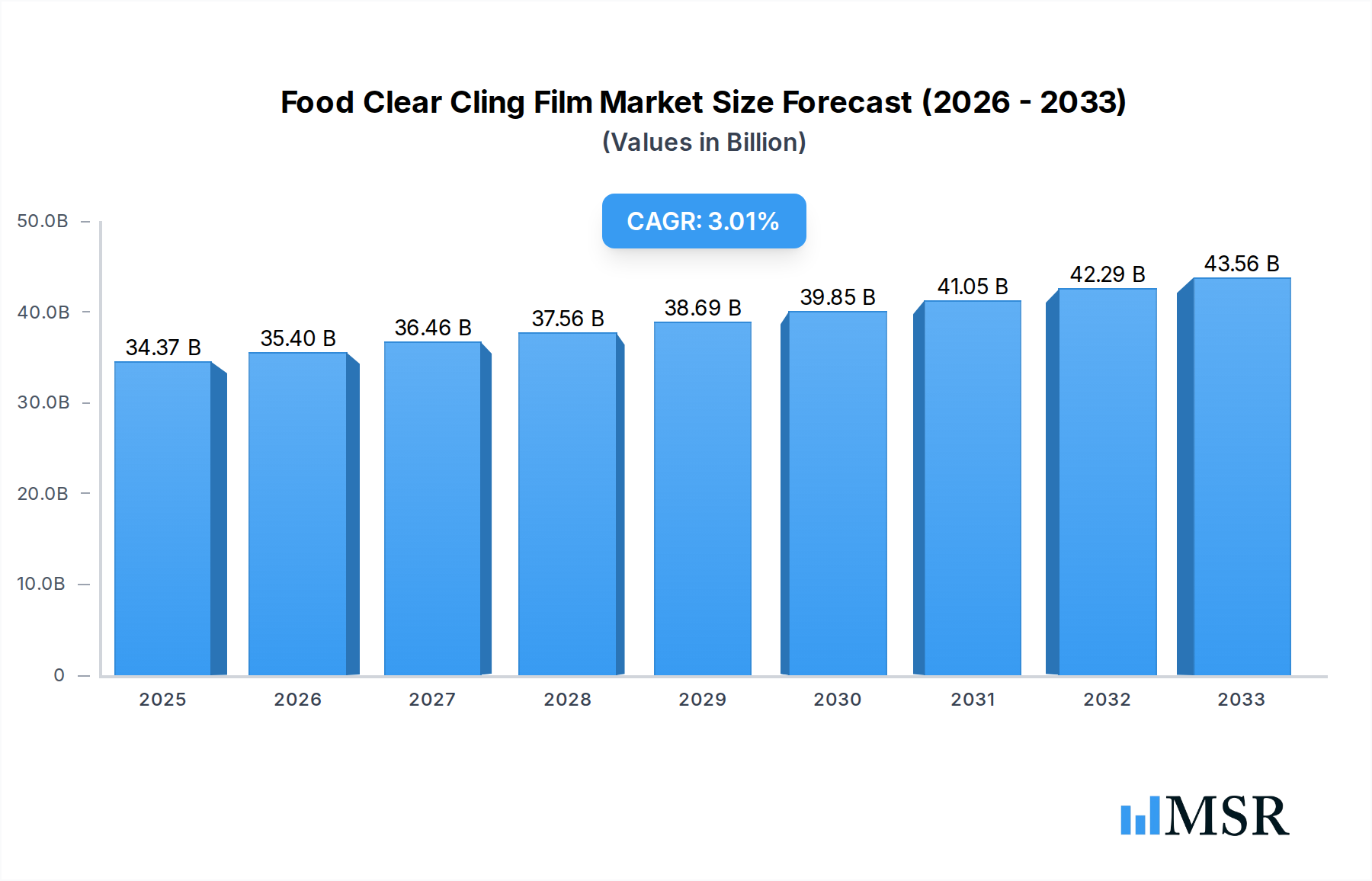

The global market for Food Clear Cling Film is poised for steady expansion, projected to reach an estimated $34.37 billion in 2025. This growth is underpinned by a CAGR of 3%, indicating sustained demand and increasing adoption across various applications. A primary driver for this upward trajectory is the escalating consumer preference for convenient food packaging solutions that offer both freshness preservation and visual appeal. The growing awareness regarding food safety and shelf-life extension further fuels the demand for high-quality cling films that create an effective barrier against external contaminants and moisture. The expanding food service industry, including restaurants and catering services, is a significant contributor, requiring reliable and hygienic packaging for prepared meals and ingredients. Furthermore, the increasing penetration of supermarkets and hypermarkets globally, offering a wider array of pre-packaged food items, directly translates to a higher demand for cling film. Innovations in film technology, focusing on enhanced barrier properties, recyclability, and thinner gauges without compromising performance, are also expected to play a crucial role in market development.

Food Clear Cling Film Market Size (In Billion)

The market is segmented by application into Household, Supermarkets, Restaurants, and Others, with each segment contributing to the overall demand. Household use continues to be a strong segment due to the convenience cling film offers in everyday food storage. Supermarkets and restaurants, however, represent the fastest-growing sectors, driven by bulk purchasing and the need for professional food presentation and preservation. The types of cling films available, including PE, PVC, PVDC, and PMP, cater to diverse performance requirements. Polyethylene (PE) and Polyvinyl Chloride (PVC) remain dominant due to their cost-effectiveness and versatile properties. The market also faces certain restraints, such as increasing environmental concerns regarding plastic waste and the subsequent push for sustainable packaging alternatives. However, manufacturers are actively investing in research and development to create more eco-friendly cling film options, including biodegradable and compostable variants, which are expected to mitigate these challenges and create new avenues for growth. The competitive landscape is characterized by the presence of key global players like Glad, Saran, and AEP Industries, alongside numerous regional manufacturers, all vying for market share through product innovation and strategic expansions.

Food Clear Cling Film Company Market Share

Report Description: Dive deep into the dynamic world of food clear cling film with this in-depth market intelligence report. Covering the period from 2019 to 2033, with a base year of 2025 and a robust forecast period of 2025-2033, this comprehensive analysis is your definitive guide to understanding market concentration, industry insights, key segments, product developments, challenges, growth drivers, emerging opportunities, and leading players. Designed for industry stakeholders, packaging manufacturers, R&D professionals, and strategic decision-makers, this report provides actionable insights and quantitative data to inform your business strategies.

Explore the intricacies of the global food clear cling film market, valued at an estimated $XX billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period. We dissect the market by application (Household, Supermarkets, Restaurants, Others) and type (PE, PVC, PVDC, PMP, Others), offering granular insights into regional dominance and segment-specific growth drivers. Understand the impact of industry developments and technological innovations shaping the future of food preservation and packaging.

This report offers a holistic view, from historical performance (2019-2024) to future projections, providing a billion-dollar market outlook for strategic investment and competitive analysis. Whether you're looking to enhance product offerings, identify new market niches, or navigate regulatory landscapes, this report equips you with the knowledge to succeed in the ever-evolving food clear cling film industry.

Food Clear Cling Film Market Concentration & Dynamics

The global food clear cling film market is characterized by a moderate to high level of concentration, with a few prominent players holding significant market share. In 2025, key companies like Glad and Saran are expected to command substantial portions of the market, estimated at $XX billion. The innovation ecosystem is driven by continuous advancements in material science and processing technologies, aiming for improved barrier properties, sustainability, and user convenience. Regulatory frameworks, particularly concerning food contact safety and environmental impact, play a crucial role in shaping product development and market entry. Substitute products, such as reusable containers and biodegradable films, pose an evolving threat, prompting manufacturers to focus on eco-friendly alternatives. End-user trends lean towards enhanced food safety, extended shelf life, and convenient packaging solutions, influencing product design and marketing strategies. Merger and Acquisition (M&A) activities are moderately prevalent, with an estimated XX M&A deals in the historical period (2019-2024) as companies seek to consolidate market presence and acquire technological capabilities.

- Market Share Snapshot (2025 Estimated):

- Leading Players: XX%

- Key Manufacturers: XX%

- Fragmented Segment: XX%

- M&A Activity (2019-2024):

- Total Deals: XX

- Key Acquisition Targets: Technology Providers, Regional Distributors

- Innovation Focus Areas:

- Biodegradable and compostable cling films

- Enhanced antimicrobial properties

- Improved oxygen and moisture barrier capabilities

Food Clear Cling Film Industry Insights & Trends

The food clear cling film market is poised for substantial growth, projected to reach an estimated $XX billion by 2025, with a remarkable CAGR of XX% anticipated during the forecast period of 2025-2033. This upward trajectory is primarily fueled by increasing global demand for packaged food products, driven by evolving consumer lifestyles, urbanization, and a growing middle class. The rising consciousness around food safety and hygiene standards further bolsters the need for effective food preservation solutions. Technological disruptions are continuously reshaping the industry, with innovations in polymer science leading to the development of advanced cling films offering superior barrier properties, extended shelf life, and improved recyclability. The shift towards sustainable packaging solutions is a significant trend, with a growing emphasis on biodegradable and compostable cling films made from renewable resources. Consumer behaviors are also evolving; consumers are increasingly seeking convenience, portion control, and visually appealing packaging that preserves the freshness and quality of food. This demand translates into a need for versatile cling films that can adapt to various food types and packaging formats. The global food clear cling film market is witnessing a strong impetus from the food service sector, including restaurants and catering businesses, which require reliable and efficient packaging for food storage and transportation. Supermarkets are also a significant driver, utilizing cling films extensively for displaying fresh produce, meats, and ready-to-eat meals, enhancing product appeal and reducing spoilage. The household segment continues to be a steady contributor, with consumers relying on cling films for everyday food storage needs. The market's growth is intricately linked to advancements in extrusion and co-extrusion technologies, enabling the production of multi-layer films with customized functionalities. The increasing adoption of automation in food processing and packaging lines further supports the demand for high-performance cling films. Furthermore, government initiatives promoting food waste reduction and sustainable packaging practices are expected to create a favorable environment for market expansion. The competitive landscape is characterized by ongoing research and development efforts aimed at creating films with improved tear resistance, puncture resistance, and adhesion properties, while simultaneously addressing environmental concerns. The increasing integration of digital technologies in supply chain management is also influencing demand for cling films that can withstand diverse transportation conditions and maintain product integrity. The market's expansion is further supported by investments in R&D for novel materials and manufacturing processes that can reduce production costs and enhance the overall performance of cling films. The growing awareness of foodborne illnesses and the importance of proper food storage are compelling consumers and businesses alike to opt for high-quality cling films that offer reliable protection and preservation of food products.

Key Markets & Segments Leading Food Clear Cling Film

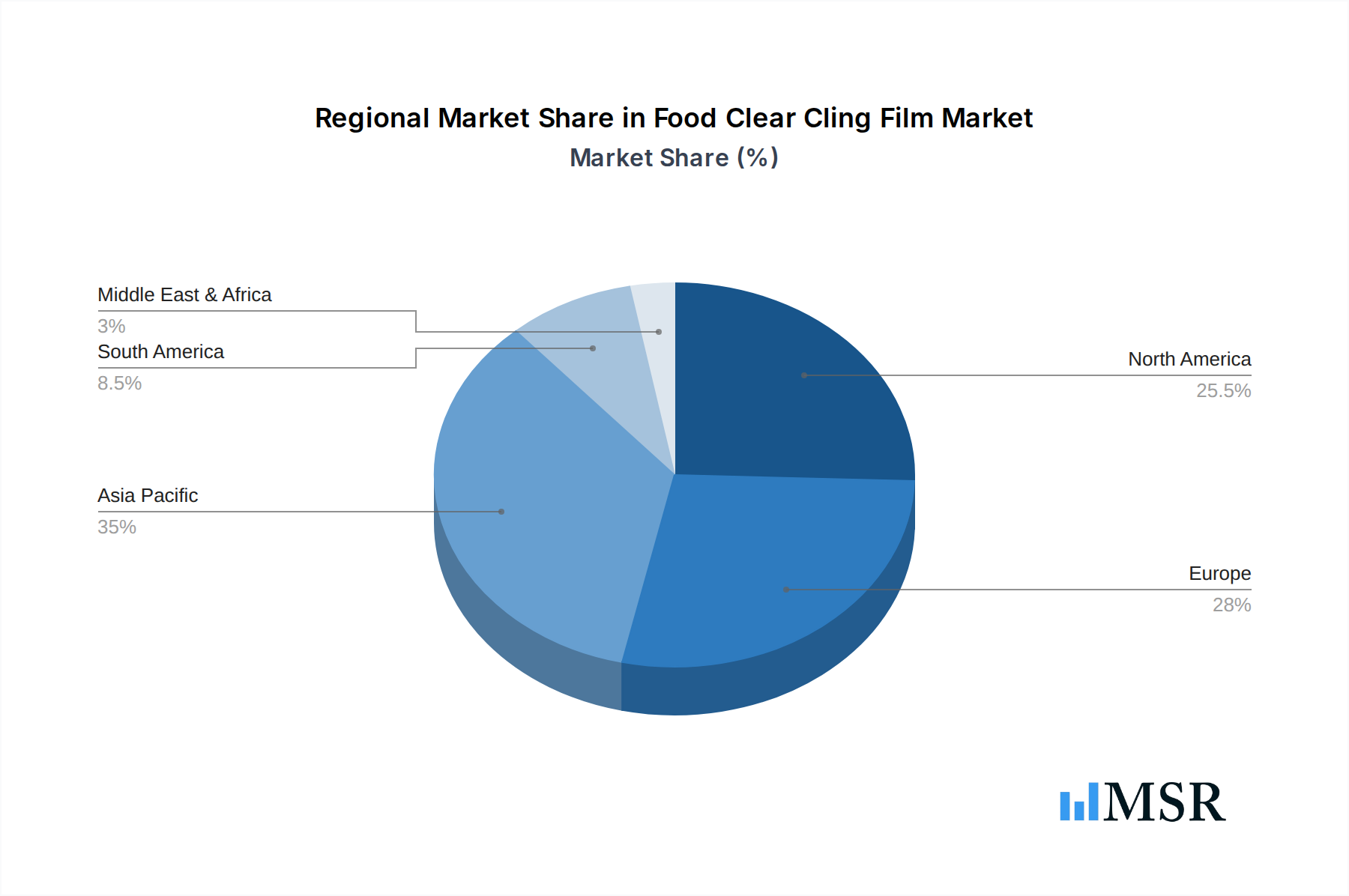

The food clear cling film market demonstrates significant regional and segmental dominance, driven by a confluence of economic, demographic, and infrastructural factors. Asia Pacific, particularly countries like China and India, is emerging as a leading market, fueled by rapid economic growth, a burgeoning population, and a substantial increase in processed and packaged food consumption. Economic growth in this region translates to increased disposable income, enabling consumers to opt for convenience and quality in their food packaging choices. The expanding retail infrastructure, including the proliferation of supermarkets and hypermarkets, directly boosts the demand for cling films used in product display and preservation. North America and Europe remain mature yet robust markets, characterized by high consumer awareness regarding food safety and a strong demand for premium and convenient packaging solutions. Established food processing industries and stringent food safety regulations in these regions necessitate the use of high-performance cling films.

Dominant Regions & Countries:

- Asia Pacific: Driven by China, India, and Southeast Asian nations.

- Drivers: Rapid urbanization, growing middle-class population, expanding food processing industry, increasing adoption of modern retail formats.

- North America: Primarily the United States and Canada.

- Drivers: High consumer spending on convenience foods, strict food safety standards, well-developed retail infrastructure.

- Europe: Key markets include Germany, the UK, and France.

- Drivers: Strong emphasis on food quality and safety, increasing demand for sustainable packaging, well-established food service sector.

- Asia Pacific: Driven by China, India, and Southeast Asian nations.

Segment Dominance by Application:

- Supermarkets: This segment holds the largest market share due to the extensive use of cling film for packaging a wide array of food products, from fresh produce and meats to bakery items and ready-to-eat meals. The need for visually appealing and protective packaging to maintain freshness and extend shelf life is paramount in this segment.

- Drivers: Growing demand for pre-packaged food, aesthetic presentation of products, reduction of food waste.

- Household: While smaller in individual transaction value, the sheer volume of household consumption makes this segment a significant contributor. Consumers rely on cling film for everyday food storage, preserving leftovers, and marinating foods.

- Drivers: Everyday convenience, food preservation at home, cost-effectiveness.

- Restaurants: The food service industry utilizes cling film extensively for food preparation, storage, and takeout orders, emphasizing hygiene and product integrity.

- Drivers: Food safety regulations, portion control, efficient food storage, takeout and delivery services.

- Supermarkets: This segment holds the largest market share due to the extensive use of cling film for packaging a wide array of food products, from fresh produce and meats to bakery items and ready-to-eat meals. The need for visually appealing and protective packaging to maintain freshness and extend shelf life is paramount in this segment.

Segment Dominance by Type:

- PE (Polyethylene): This type of cling film dominates the market due to its excellent balance of properties, including good cling, flexibility, puncture resistance, and cost-effectiveness. It is widely used across various applications, from household use to industrial packaging.

- Drivers: Cost-effectiveness, good cling properties, versatility, recyclability potential.

- PVC (Polyvinyl Chloride): Historically a strong contender, PVC cling films offer superior clarity and excellent cling properties, making them ideal for wrapping fresh produce and meats where visual appeal is critical. However, environmental concerns are leading to a gradual shift towards alternatives.

- Drivers: High transparency, excellent cling, good barrier properties for certain applications.

- PVDC (Polyvinylidene Chloride): Though often used in co-extruded films, PVDC offers exceptional barrier properties against oxygen and moisture, making it crucial for extending the shelf life of sensitive food products.

- Drivers: Superior barrier properties, extended shelf life for specific food products.

- PE (Polyethylene): This type of cling film dominates the market due to its excellent balance of properties, including good cling, flexibility, puncture resistance, and cost-effectiveness. It is widely used across various applications, from household use to industrial packaging.

Food Clear Cling Film Product Developments

Recent product developments in the food clear cling film market are centered on enhancing functionality, sustainability, and consumer convenience. Innovations include the introduction of bio-based and compostable cling films derived from plant starches and polylactic acid (PLA), addressing growing environmental concerns and regulatory pressures. Advanced formulations are yielding cling films with improved puncture and tear resistance, ensuring better product protection during transit and handling. Furthermore, the development of cling films with active packaging properties, such as antimicrobial agents or oxygen scavengers, aims to further extend food shelf life and enhance safety. The market is also witnessing a trend towards thinner, yet stronger, films, optimizing material usage and reducing packaging weight.

- Key Innovations:

- Biodegradable and compostable cling films.

- Cling films with enhanced puncture and tear resistance.

- Active packaging technologies incorporating antimicrobial agents.

- Thinner, high-strength cling films for material reduction.

Challenges in the Food Clear Cling Film Market

The food clear cling film market faces several challenges that can impede its growth and profitability. Increasing regulatory scrutiny regarding the environmental impact of single-use plastics, particularly PVC-based films, poses a significant hurdle, necessitating investment in sustainable alternatives and advanced recycling technologies. Fluctuations in raw material prices, especially petrochemicals, can impact production costs and profit margins, leading to price volatility for end-users. Intense competition from alternative packaging solutions, such as rigid containers, trays, and newer biodegradable materials, also pressures market players to continuously innovate and offer competitive pricing. Furthermore, consumer perception and demand for plastic reduction can lead to boycotts or a preference for alternative packaging, requiring proactive marketing and product development strategies to maintain market share.

- Key Restraints:

- Environmental Regulations: Stringent regulations on single-use plastics impacting PVC-based films.

- Raw Material Price Volatility: Fluctuations in petrochemical prices affecting manufacturing costs.

- Competition from Alternatives: Rise of reusable, biodegradable, and other packaging solutions.

- Consumer Perception: Growing demand for plastic-free alternatives.

Forces Driving Food Clear Cling Film Growth

The food clear cling film market is propelled by several potent growth drivers. The expanding global population and increasing urbanization are leading to a greater demand for packaged and processed foods, directly benefiting cling film manufacturers. Evolving consumer lifestyles, characterized by busy schedules and a preference for convenience, are increasing the consumption of ready-to-eat meals and pre-packaged food items, all of which rely on effective cling film packaging. Heightened consumer awareness regarding food safety, hygiene, and the prevention of foodborne illnesses is a critical driver, as cling films play a vital role in preserving food quality and preventing contamination. Furthermore, the advancements in material science and manufacturing technologies are enabling the development of more efficient, sustainable, and cost-effective cling films, meeting diverse market needs.

- Key Growth Accelerators:

- Population Growth & Urbanization: Increased demand for packaged foods.

- Convenience Food Trend: Growing consumption of ready-to-eat and pre-packaged meals.

- Food Safety Awareness: Enhanced demand for protective and hygienic packaging.

- Technological Advancements: Development of superior and sustainable cling film materials.

Challenges in the Food Clear Cling Film Market

While the market presents numerous opportunities, long-term growth catalysts are essential for sustained expansion in the food clear cling film market. Continued investment in research and development for next-generation cling films with enhanced biodegradability and compostability will be crucial. Strategic partnerships and collaborations between cling film manufacturers, raw material suppliers, and food producers can foster innovation and create integrated solutions. Expanding into emerging economies with growing food processing sectors and developing economies with increasing disposable incomes offers significant untapped market potential. Furthermore, the development of closed-loop recycling systems and the promotion of a circular economy for plastic packaging will address environmental concerns and ensure long-term market viability.

- Long-Term Growth Catalysts:

- Sustainable Material Innovation: Focus on bio-based and truly biodegradable cling films.

- Strategic Alliances: Collaborations for product development and market penetration.

- Emerging Market Penetration: Tapping into high-growth regions with developing food industries.

- Circular Economy Integration: Developing robust recycling and reuse models.

Emerging Opportunities in Food Clear Cling Film

The food clear cling film market is ripe with emerging opportunities, driven by evolving consumer preferences and technological advancements. The increasing demand for personalized and convenient food packaging presents an opportunity for customizable cling films tailored to specific food types and portion sizes. The growing popularity of e-commerce and food delivery services necessitates robust and reliable packaging solutions, including cling films that can withstand the rigors of shipping. Furthermore, the integration of smart packaging technologies, such as temperature indicators or tamper-evident seals embedded in cling films, offers value-added functionalities that can enhance consumer trust and product safety. The push towards reducing food waste globally creates a demand for cling films that can significantly extend the shelf life of perishable goods, offering economic and environmental benefits.

- Key Emerging Trends & Opportunities:

- Smart Packaging Integration: Cling films with embedded sensors or indicators.

- E-commerce Packaging Solutions: Developing films for the online food retail supply chain.

- Food Waste Reduction Initiatives: Cling films that maximize product shelf life.

- Personalized & Portion-Controlled Packaging: Catering to individual consumer needs.

Leading Players in the Food Clear Cling Film Sector

- Glad

- Saran

- AEP Industries

- Polyvinyl Films

- Wrap Film Systems

- Lakeland

- Wrapex

- Linpac Packaging

- Melitta

- Comcoplast

- Fora

- Victor

- Wentus Kunststoff

- Sphere

- Publi Embal

- Koroplast

- Pro-Pack

- Bursa Pazar

- Rotopa

- Parex

- Sedat Tahir

Key Milestones in Food Clear Cling Film Industry

- 2019: Increased focus on developing and marketing compostable cling film alternatives.

- 2020: Significant surge in demand for household cling film due to pandemic-related food storage needs.

- 2021: Growing investment in R&D for advanced barrier properties in cling films.

- 2022: Regulatory discussions intensify around single-use plastic reduction, influencing PVC film market dynamics.

- 2023: Introduction of thinner, yet more durable, cling film grades to optimize material usage.

- 2024: Emerging partnerships between cling film manufacturers and food delivery platforms for specialized packaging.

Strategic Outlook for Food Clear Cling Film Market

The strategic outlook for the food clear cling film market is overwhelmingly positive, driven by continued innovation and growing global demand for effective food preservation. Key growth accelerators include the ongoing development of sustainable cling film solutions, catering to increasing environmental consciousness and regulatory pressures. Strategic opportunities lie in expanding market penetration in emerging economies and leveraging technological advancements to create value-added products, such as smart and active packaging. Manufacturers that can successfully balance cost-effectiveness with superior performance and environmental responsibility will be best positioned to capture market share and achieve sustained growth in the coming years. The future of the market hinges on a proactive approach to sustainability, continuous product innovation, and a keen understanding of evolving consumer needs.

Food Clear Cling Film Segmentation

-

1. Application

- 1.1. Household

- 1.2. Supermarkets

- 1.3. Restaurants

- 1.4. Others

-

2. Types

- 2.1. PE

- 2.2. PVC

- 2.3. PVDC

- 2.4. PMP

- 2.5. Others

Food Clear Cling Film Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Clear Cling Film Regional Market Share

Geographic Coverage of Food Clear Cling Film

Food Clear Cling Film REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Food Clear Cling Film Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Household

- 5.1.2. Supermarkets

- 5.1.3. Restaurants

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PE

- 5.2.2. PVC

- 5.2.3. PVDC

- 5.2.4. PMP

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Food Clear Cling Film Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Household

- 6.1.2. Supermarkets

- 6.1.3. Restaurants

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PE

- 6.2.2. PVC

- 6.2.3. PVDC

- 6.2.4. PMP

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Food Clear Cling Film Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Household

- 7.1.2. Supermarkets

- 7.1.3. Restaurants

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PE

- 7.2.2. PVC

- 7.2.3. PVDC

- 7.2.4. PMP

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Food Clear Cling Film Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Household

- 8.1.2. Supermarkets

- 8.1.3. Restaurants

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PE

- 8.2.2. PVC

- 8.2.3. PVDC

- 8.2.4. PMP

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Food Clear Cling Film Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Household

- 9.1.2. Supermarkets

- 9.1.3. Restaurants

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PE

- 9.2.2. PVC

- 9.2.3. PVDC

- 9.2.4. PMP

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Food Clear Cling Film Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Household

- 10.1.2. Supermarkets

- 10.1.3. Restaurants

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PE

- 10.2.2. PVC

- 10.2.3. PVDC

- 10.2.4. PMP

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Glad

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Saran

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AEP Industries

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Polyvinyl Films

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Wrap Film Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Lakeland

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Wrapex

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Linpac Packaging

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Melitta

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Comcoplast

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Fora

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Victor

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Wentus Kunststoff

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Sphere

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Publi Embal

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Koroplast

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Pro-Pack

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Bursa Pazar

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Rotopa

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Parex

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Sedat Tahir

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 Glad

List of Figures

- Figure 1: Global Food Clear Cling Film Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Food Clear Cling Film Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Food Clear Cling Film Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Food Clear Cling Film Volume (K), by Application 2025 & 2033

- Figure 5: North America Food Clear Cling Film Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Food Clear Cling Film Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Food Clear Cling Film Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Food Clear Cling Film Volume (K), by Types 2025 & 2033

- Figure 9: North America Food Clear Cling Film Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Food Clear Cling Film Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Food Clear Cling Film Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Food Clear Cling Film Volume (K), by Country 2025 & 2033

- Figure 13: North America Food Clear Cling Film Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Food Clear Cling Film Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Food Clear Cling Film Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Food Clear Cling Film Volume (K), by Application 2025 & 2033

- Figure 17: South America Food Clear Cling Film Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Food Clear Cling Film Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Food Clear Cling Film Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Food Clear Cling Film Volume (K), by Types 2025 & 2033

- Figure 21: South America Food Clear Cling Film Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Food Clear Cling Film Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Food Clear Cling Film Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Food Clear Cling Film Volume (K), by Country 2025 & 2033

- Figure 25: South America Food Clear Cling Film Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Food Clear Cling Film Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Food Clear Cling Film Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Food Clear Cling Film Volume (K), by Application 2025 & 2033

- Figure 29: Europe Food Clear Cling Film Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Food Clear Cling Film Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Food Clear Cling Film Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Food Clear Cling Film Volume (K), by Types 2025 & 2033

- Figure 33: Europe Food Clear Cling Film Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Food Clear Cling Film Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Food Clear Cling Film Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Food Clear Cling Film Volume (K), by Country 2025 & 2033

- Figure 37: Europe Food Clear Cling Film Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Food Clear Cling Film Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Food Clear Cling Film Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Food Clear Cling Film Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Food Clear Cling Film Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Food Clear Cling Film Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Food Clear Cling Film Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Food Clear Cling Film Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Food Clear Cling Film Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Food Clear Cling Film Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Food Clear Cling Film Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Food Clear Cling Film Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Food Clear Cling Film Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Food Clear Cling Film Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Food Clear Cling Film Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Food Clear Cling Film Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Food Clear Cling Film Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Food Clear Cling Film Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Food Clear Cling Film Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Food Clear Cling Film Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Food Clear Cling Film Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Food Clear Cling Film Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Food Clear Cling Film Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Food Clear Cling Film Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Food Clear Cling Film Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Food Clear Cling Film Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Clear Cling Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Food Clear Cling Film Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Food Clear Cling Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Food Clear Cling Film Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Food Clear Cling Film Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Food Clear Cling Film Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Food Clear Cling Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Food Clear Cling Film Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Food Clear Cling Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Food Clear Cling Film Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Food Clear Cling Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Food Clear Cling Film Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Food Clear Cling Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Food Clear Cling Film Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Food Clear Cling Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Food Clear Cling Film Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Food Clear Cling Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Food Clear Cling Film Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Food Clear Cling Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Food Clear Cling Film Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Food Clear Cling Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Food Clear Cling Film Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Food Clear Cling Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Food Clear Cling Film Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Food Clear Cling Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Food Clear Cling Film Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Food Clear Cling Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Food Clear Cling Film Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Food Clear Cling Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Food Clear Cling Film Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Food Clear Cling Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Food Clear Cling Film Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Food Clear Cling Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Food Clear Cling Film Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Food Clear Cling Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Food Clear Cling Film Volume K Forecast, by Country 2020 & 2033

- Table 79: China Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Food Clear Cling Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Food Clear Cling Film Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Clear Cling Film?

The projected CAGR is approximately 3%.

2. Which companies are prominent players in the Food Clear Cling Film?

Key companies in the market include Glad, Saran, AEP Industries, Polyvinyl Films, Wrap Film Systems, Lakeland, Wrapex, Linpac Packaging, Melitta, Comcoplast, Fora, Victor, Wentus Kunststoff, Sphere, Publi Embal, Koroplast, Pro-Pack, Bursa Pazar, Rotopa, Parex, Sedat Tahir.

3. What are the main segments of the Food Clear Cling Film?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Clear Cling Film," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Clear Cling Film report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Clear Cling Film?

To stay informed about further developments, trends, and reports in the Food Clear Cling Film, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence