Key Insights for Maritime System Integration Market

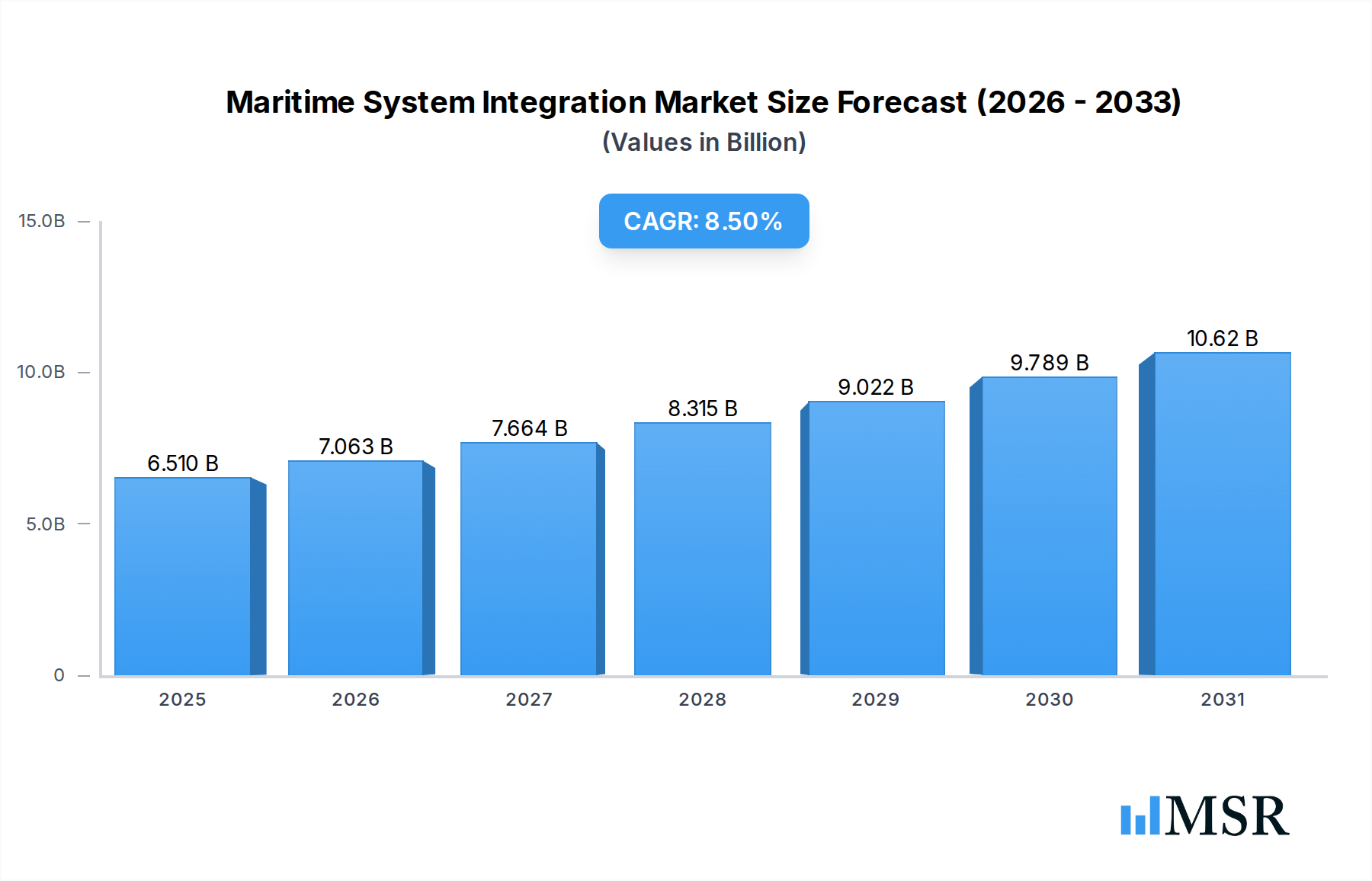

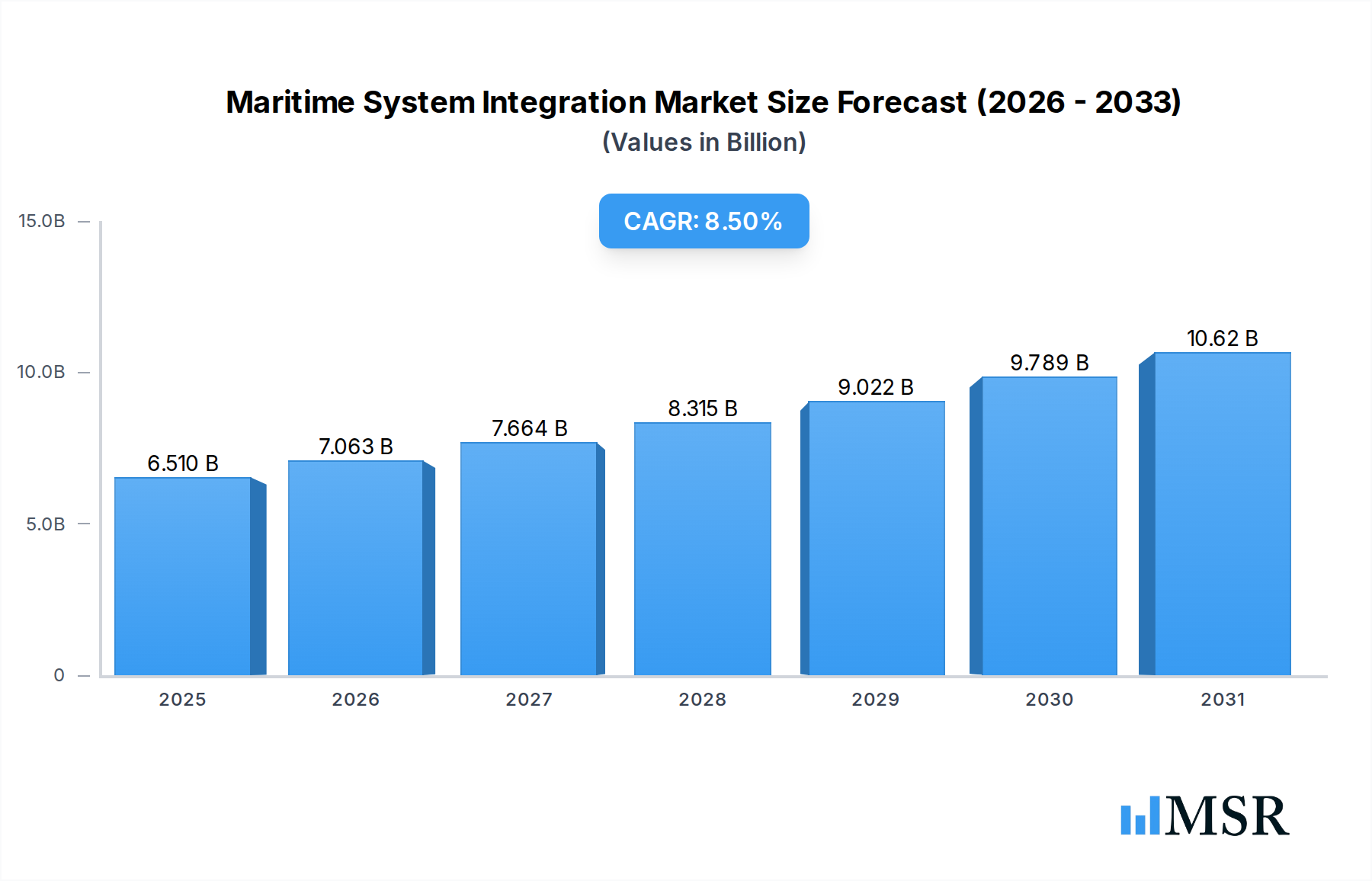

The Global Maritime System Integration Market was valued at $6 billion in 2023, poised for substantial expansion with a projected Compound Annual Growth Rate (CAGR) of 8.9% over the forecast period. This robust growth is primarily driven by the escalating demand for operational efficiency, enhanced safety protocols, and stringent environmental compliance within the maritime industry. The sector is undergoing a profound digital transformation, necessitating sophisticated integrated systems to manage complex vessel operations, navigation, communication, and propulsion. Key demand drivers include the modernization of aging fleets, the proliferation of smart ship initiatives, and the increasing adoption of advanced technologies such as the Internet of Things (IoT) and Artificial Intelligence (AI).

Maritime System Integration Market Size (In Billion)

Macro tailwinds such as global trade growth, increased defense spending on Naval Vessels Market, and the continuous evolution of regulatory frameworks (e.g., IMO 2020 and subsequent environmental mandates) are compelling vessel operators and shipbuilders to invest in integrated solutions. These systems consolidate disparate functionalities into a unified platform, offering benefits ranging from reduced fuel consumption and optimized route planning to improved crew situational awareness and predictive maintenance capabilities. The integration of advanced sensors, data analytics platforms, and automation technologies is becoming critical for competitive advantage. Furthermore, the rising focus on cybersecurity resilience in maritime operations is amplifying the need for securely integrated systems that can protect against sophisticated threats. Companies are increasingly looking towards comprehensive solutions that encompass hardware, software, and critical services, often leveraging the Software as a Service Market model for flexibility and scalability. This shift towards holistic system architecture is not merely about technological adoption but about fundamentally reshaping maritime logistics and operations for a more connected, efficient, and sustainable future. The convergence of operational technology (OT) and information technology (IT) is a cornerstone of this market's evolution, underscoring the vital role of robust maritime system integration.

Maritime System Integration Company Market Share

Dominant Segment Analysis in Maritime System Integration Market

Within the Maritime System Integration Market, the 'Service' offering segment stands out as the single largest contributor to revenue share, and its dominance is projected to strengthen over the forecast period. This segment encompasses a broad spectrum of crucial activities, including system design and engineering, installation and commissioning, software updates and maintenance, training, consulting, and ongoing technical support. The inherent complexity of integrating diverse systems across different vessel types—ranging from Cargo Ships and Tankers to Passenger Ships and Naval Vessels Market—necessitates specialized expertise that often cannot be fully managed in-house by vessel operators or shipyards.

Several factors contribute to the 'Service' segment's leading position. Firstly, the initial integration of hardware components, proprietary software, and communication protocols requires meticulous planning and execution by skilled engineers. This process involves ensuring interoperability between systems such as Marine Navigation Systems Market, Marine Communication Systems Market, and Propulsion & Machinery Management (PMS), which originate from various vendors. Secondly, as maritime technologies rapidly evolve with the penetration of the Internet of Things (IoT) Market and Artificial Intelligence (AI) Market, continuous software updates, cybersecurity patches, and system upgrades become imperative. The lifecycle management of these complex integrated systems demands specialized service providers who can offer proactive maintenance and rapid troubleshooting, minimizing downtime and ensuring regulatory compliance. The sophistication of modern maritime platforms means that the initial sale of hardware and software is often accompanied by multi-year service contracts, providing a stable and recurring revenue stream for integrators.

Key players like L3Harris Technologies, RH Marine, and Vard Electro are prominent in offering comprehensive service portfolios that extend beyond basic installation to encompass advanced data analytics support and remote monitoring capabilities. The increasing adoption of advanced technologies within the Marine Automation Market, coupled with the growing demand for Vessel Management Systems Market, further fuels the need for expert services for customization, optimization, and fault diagnosis. Furthermore, the transition towards more autonomous and remotely operated vessels necessitates robust service frameworks for remote diagnostics, over-the-air updates, and specialized operational support. The service segment's share is consistently growing as it represents the value-added component that ensures the optimal performance, reliability, and longevity of intricate maritime integrated systems, making it a critical driver for the overall market dynamics.

Key Market Drivers & Constraints for Maritime System Integration Market

The Maritime System Integration Market is shaped by a confluence of powerful drivers and notable constraints. A primary driver is the increasing imperative for operational efficiency and cost reduction. Vessel operators are under constant pressure to optimize fuel consumption, reduce port turnaround times, and streamline maintenance schedules. Integrated systems, particularly those incorporating Data Analytics Services Market, offer real-time data insights into vessel performance, enabling predictive maintenance and optimized route planning, which directly translates to significant cost savings. For instance, the adoption of integrated propulsion management systems can lead to fuel efficiency improvements of 5-10% for large commercial vessels.

Another significant driver is the escalation of stringent maritime regulations. International bodies like the IMO and regional authorities continually introduce new mandates related to emissions, ballast water management, and cybersecurity. Compliance often necessitates the upgrade or complete overhaul of onboard systems, driving demand for integrated solutions that meet these new standards. For example, the increasing demand for secure Marine Communication Systems Market is directly linked to new cybersecurity guidelines.

The rise of smart shipping and autonomous vessel initiatives acts as a powerful technological driver. The future of maritime transport envisions vessels equipped with advanced sensors, AI-driven decision-making, and remote operation capabilities. This vision inherently relies on highly sophisticated system integration to ensure seamless data flow and control across various subsystems. The Internet of Things (IoT) Market is fundamental to this trend, enabling interconnectedness and real-time data exchange across the fleet.

However, the market faces notable constraints. The high initial investment costs associated with implementing advanced integrated systems can be a deterrent for smaller operators or those with older vessels. The upgrade cycle for large commercial ships is long, and capital expenditures for new technology can be substantial. For example, a comprehensive system overhaul can run into millions of dollars, creating a significant barrier to entry for some.

Secondly, the complexity of integrating disparate legacy systems presents a major technical challenge. Many existing vessels operate with a patchwork of older, proprietary systems from various manufacturers. Achieving seamless interoperability and data exchange between these legacy components and new digital solutions requires extensive customization and engineering, increasing project timelines and costs. This challenge impacts the broader Marine Automation Market as well.

Finally, cybersecurity concerns are a growing constraint. As maritime systems become more connected, they become more vulnerable to cyber threats. The potential for disruption to navigation, propulsion, or cargo systems due to a cyber-attack is immense, necessitating robust security measures that add to the cost and complexity of integration. The lack of standardized cybersecurity protocols across the industry further complicates this issue, impacting the deployment of new Artificial Intelligence (AI) Market applications.

Competitive Ecosystem of Maritime System Integration Market

The Maritime System Integration Market features a diverse array of companies, from established global technology providers to specialized niche integrators, all vying for market share by offering comprehensive solutions across various vessel types and operational requirements.

- SEAIRTECH: A firm known for its expertise in marine electronics and system integration, focusing on tailored solutions for diverse vessel segments, including leisure and commercial craft, emphasizing reliability and cutting-edge technology.

- Trelleborg Marine and Infrastructure: A global leader providing innovative solutions for marine operations, including advanced docking and mooring systems, as well as critical infrastructure solutions that often require intricate integration with broader vessel management systems.

- Quad Plus: Specializes in industrial automation and drive systems, extending its expertise to marine applications where robust and integrated electrical and control systems are paramount for efficient vessel operation.

- RH Marine: An independent system integrator for complex systems on naval ships and yachts, offering a broad portfolio from bridge systems and electrical installations to automation and energy management solutions.

- European Maritime Safety Agency: Primarily a regulatory and advisory body, its work in maritime safety and security standards heavily influences the types of integrated systems required for compliance across the European fleet.

- L3Harris Technologies: A major global aerospace and defense technology innovator, providing advanced integrated mission systems, communication solutions, and electronic systems for both naval and commercial maritime platforms.

- Norwegian Electric System: Specializes in sustainable and efficient electric propulsion and power management systems, offering integrated solutions that optimize energy consumption and reduce environmental impact for vessels.

- Youredi: A company focused on data integration and connectivity solutions for global supply chains, extending its services to the maritime sector by facilitating seamless data exchange between vessel systems and shore-based logistics platforms.

- Drumgrange: A UK-based company delivering electronic and software engineering solutions, with significant expertise in defense systems integration, particularly for complex naval command and control applications.

- Britton Marine Systems: A specialist in marine electrical systems and electronics, providing integration services for navigation, communication, and entertainment systems on various types of vessels.

- Gebhard Electro: Offers complete electrical systems, automation, and control solutions for the maritime industry, focusing on robust and reliable integration for propulsion, power generation, and distribution systems.

- HEITEC: An engineering solutions provider with experience in automation, software, and electronics, applying its industrial expertise to develop integrated control and monitoring systems for maritime applications.

- Karl Senner: A leading supplier of marine propulsion systems, offering integrated solutions that combine engines, gears, and control systems for optimal vessel performance and efficiency.

- Vard Electro: A global provider of marine electrical systems, automation, and communication solutions, specializing in sophisticated integrated bridge and control systems for offshore vessels and specialized ships.

Recent Developments & Milestones in Maritime System Integration Market

Q1 2023: Several leading integrators announced new partnerships with software providers to enhance their Vessel Management Systems Market offerings, focusing on cloud-based platforms to improve remote monitoring and predictive maintenance capabilities. This move aimed to reduce operational expenditure for fleet owners. Q3 2023: Regulatory bodies initiated discussions on updated cybersecurity frameworks for maritime operational technology, prompting integrators to invest further in secure-by-design principles for Marine Communication Systems Market and control platforms. This development highlighted the growing importance of cyber resilience in the Maritime System Integration Market. Q1 2024: A major trend emerged with the increasing integration of Artificial Intelligence (AI) Market modules into existing navigation and collision avoidance systems, offering enhanced decision support for crew members and paving the way for semi-autonomous operations. Q3 2024: The demand for more efficient and sustainable shipping practices led to significant investments in integrated energy management systems, optimizing power generation and consumption on board, particularly for hybrid and electric propulsion systems within the broader Marine Automation Market. Q1 2025: The market saw the launch of several new comprehensive Software as a Service Market platforms designed for fleet-wide maritime data management, providing consolidated views of vessel performance, regulatory compliance, and cargo logistics, further solidifying the trend towards digital transformation.

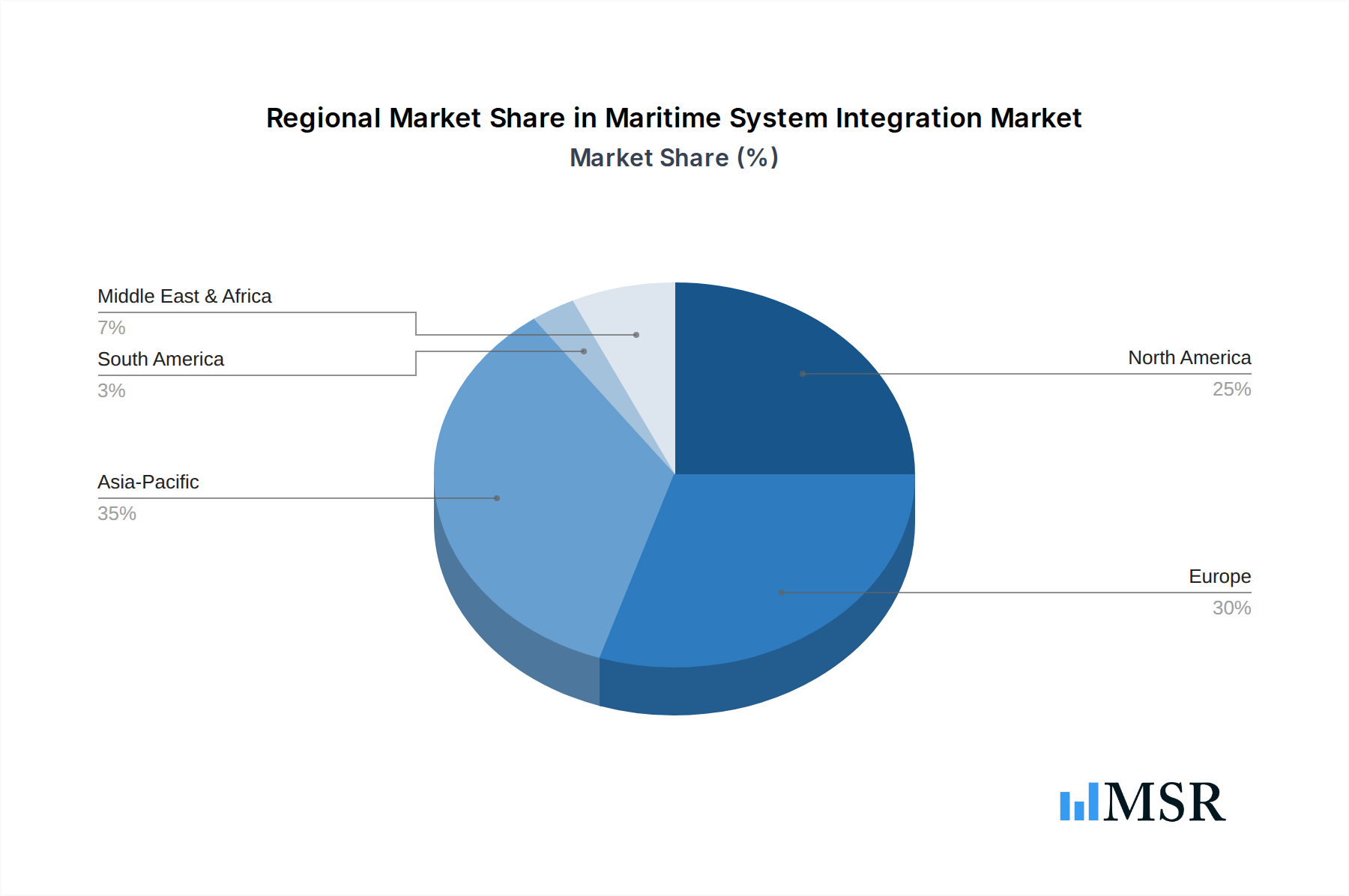

Regional Market Breakdown for Maritime System Integration Market

The Global Maritime System Integration Market exhibits varied growth dynamics across different regions, driven by distinct geopolitical, economic, and technological factors. Asia Pacific emerges as a dominant force and is anticipated to be the fastest-growing region during the forecast period. This growth is primarily fueled by extensive shipbuilding activities, particularly in China, South Korea, and Japan, coupled with significant investments in port infrastructure modernization. The rapid expansion of commercial shipping fleets and the increasing adoption of advanced digital solutions across these nations are key demand drivers. Countries like India and ASEAN nations are also contributing to this growth through their expanding maritime trade and naval modernization programs, generating substantial demand for integrated systems like Marine Navigation Systems Market.

Europe represents a mature yet robust market, holding a significant revenue share in the Maritime System Integration Market. The region benefits from a strong base of established maritime technology providers, a high focus on environmental regulations, and continuous investment in fleet modernization. Countries like Norway, Germany, and the UK are at the forefront of developing sophisticated Marine Automation Market solutions, including autonomous shipping technologies. Demand is largely driven by upgrades to existing fleets, stringent safety standards, and the adoption of energy-efficient integrated systems.

North America also constitutes a substantial market, driven by significant defense spending on Naval Vessels Market and the technological advancements in its commercial shipping and offshore sectors. The United States and Canada are investing heavily in modernizing their naval fleets and enhancing maritime security capabilities, requiring cutting-edge integrated combat and communication systems. The region's focus on technological innovation and high cybersecurity standards also drives the adoption of advanced, secure integration solutions, including those leveraging the Internet of Things (IoT) Market for enhanced monitoring and control.

The Middle East & Africa (MEA) and South America are emerging markets, currently holding smaller shares but demonstrating considerable growth potential. In MEA, investments in oil & gas infrastructure, port development, and naval defense initiatives are key drivers. South America's market growth is propelled by resource extraction industries, increased trade volumes, and the need to upgrade existing commercial and fishing fleets. While these regions may experience higher CAGRs from a lower base, their market size and technological maturity lag behind Asia Pacific, Europe, and North America. Across all regions, the emphasis on data-driven decision-making and the deployment of Data Analytics Services Market is a universal trend influencing system integration requirements.

Maritime System Integration Regional Market Share

Export, Trade Flow & Tariff Impact on Maritime System Integration Market

The Maritime System Integration Market is intricately linked to global trade flows, export dynamics of specialized components, and the impact of various tariff and non-tariff barriers. Major trade corridors for maritime integrated systems components and finished products typically follow global shipping lanes, connecting manufacturing hubs in Asia and Europe with shipbuilding and vessel operation centers worldwide. Leading exporting nations for high-tech maritime electronics and software often include Germany, Norway, the Netherlands, South Korea, and Japan, while major importing nations span across all maritime-intensive regions, especially those with active shipbuilding industries or large commercial and naval fleets.

Recent global trade tensions and protectionist policies have introduced complexities. For instance, tariffs imposed on electronic components or advanced sensors from specific regions can directly increase the cost of integrated systems, potentially slowing adoption or shifting supply chain strategies. Non-tariff barriers, such as stringent local content requirements or complex certification processes, can also hinder market entry for foreign integrators, favoring domestic suppliers. Conversely, free trade agreements can stimulate cross-border collaboration and reduce costs, facilitating the wider deployment of sophisticated solutions like the Vessel Management Systems Market. The COVID-19 pandemic also highlighted vulnerabilities in global supply chains, pushing some companies to diversify sourcing and explore regional manufacturing capabilities for critical hardware components. The export of specialized services, including system design, engineering, and remote support, is less affected by direct tariffs but can be influenced by visa policies and restrictions on cross-border data flow, impacting the global reach of the Software as a Service Market offerings. Overall, geopolitical stability and predictable trade policies are crucial for the sustained growth and efficient operation of the Maritime System Integration Market, influencing both component costs and market accessibility for integrators.

Customer Segmentation & Buying Behavior in Maritime System Integration Market

Customer segmentation in the Maritime System Integration Market primarily revolves around vessel types and operational profiles, leading to distinct purchasing criteria and buying behaviors. The key end-user segments include Commercial Shipping (Cargo Ships, Tankers, Passenger Ships), Naval Vessels Market, Fishing Vessels, and Offshore Support Vessels.

For Commercial Shipping operators, the primary purchasing criteria are often operational efficiency, cost-effectiveness, and regulatory compliance. They seek integrated systems that can reduce fuel consumption, optimize route planning, enhance safety features, and comply with environmental mandates (e.g., emissions monitoring). Price sensitivity is moderate to high, as the return on investment (ROI) over the vessel's lifecycle is a critical factor. Procurement channels typically involve direct engagement with system integrators, often in conjunction with shipyards during new builds or major refits. The demand for scalable and modular solutions, often leveraging the Software as a Service Market model, is growing to allow for future upgrades and customization.

Naval operators prioritize mission-critical reliability, survivability, security, and interoperability with existing defense infrastructures. Their buying behavior is less price-sensitive and more focused on performance, advanced capabilities (e.g., integrated Combat Systems, secure Marine Communication Systems Market), and long-term support from trusted defense contractors. Procurement usually follows rigorous tender processes, with extensive testing and validation. Naval acquisitions often involve multi-year contracts with robust service agreements, reflecting the complex lifecycle management of defense platforms. The need for advanced Artificial Intelligence (AI) Market and Data Analytics Services Market for tactical advantage is a key driver.

Fishing Vessels and Offshore Support Vessels segments share some characteristics with commercial shipping but also have specific needs. Fishing vessels require robust, easy-to-use Marine Navigation Systems Market and communication systems adapted to harsh conditions, with a strong emphasis on reliability and often lower price sensitivity for essential tools that directly impact catch rates. Offshore vessels, meanwhile, demand highly integrated Vessel Management Systems Market, dynamic positioning, and specialized communication for remote operations, where uptime and safety are paramount, making them less price-sensitive for critical systems. Recent shifts indicate a growing preference across all segments for solutions that offer predictive maintenance capabilities and remote diagnostics, highlighting the increasing value placed on uptime and operational continuity, driven by advancements in the Internet of Things (IoT) Market and Marine Automation Market.

Maritime System Integration Segmentation

-

1. Offering

- 1.1. Hardware

- 1.2. Software

- 1.3. Service

-

2. System Type

- 2.1. Combat Systems

- 2.2. Navigation Systems

- 2.3. Communication Systems

- 2.4. Propulsion & Machinery Management (PMS)

- 2.5. Others

-

3. Technology

- 3.1. internet of Things (IoT)

- 3.2. Artificial Intelligence (AI)

- 3.3. Automation and Control Systems

- 3.4. Data Analytics

-

4. Vessel Type

- 4.1. Cargo Ships

- 4.2. Tankers

- 4.3. Passenger Ships

- 4.4. Fishing Vessels

- 4.5. Naval Vessels

- 4.6. Offshore Support Vessels

- 4.7. Others

Maritime System Integration Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Maritime System Integration Regional Market Share

Geographic Coverage of Maritime System Integration

Maritime System Integration REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Service

- 5.2. Market Analysis, Insights and Forecast - by System Type

- 5.2.1. Combat Systems

- 5.2.2. Navigation Systems

- 5.2.3. Communication Systems

- 5.2.4. Propulsion & Machinery Management (PMS)

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. internet of Things (IoT)

- 5.3.2. Artificial Intelligence (AI)

- 5.3.3. Automation and Control Systems

- 5.3.4. Data Analytics

- 5.4. Market Analysis, Insights and Forecast - by Vessel Type

- 5.4.1. Cargo Ships

- 5.4.2. Tankers

- 5.4.3. Passenger Ships

- 5.4.4. Fishing Vessels

- 5.4.5. Naval Vessels

- 5.4.6. Offshore Support Vessels

- 5.4.7. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Global Maritime System Integration Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Service

- 6.2. Market Analysis, Insights and Forecast - by System Type

- 6.2.1. Combat Systems

- 6.2.2. Navigation Systems

- 6.2.3. Communication Systems

- 6.2.4. Propulsion & Machinery Management (PMS)

- 6.2.5. Others

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. internet of Things (IoT)

- 6.3.2. Artificial Intelligence (AI)

- 6.3.3. Automation and Control Systems

- 6.3.4. Data Analytics

- 6.4. Market Analysis, Insights and Forecast - by Vessel Type

- 6.4.1. Cargo Ships

- 6.4.2. Tankers

- 6.4.3. Passenger Ships

- 6.4.4. Fishing Vessels

- 6.4.5. Naval Vessels

- 6.4.6. Offshore Support Vessels

- 6.4.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Offering

- 7. North America Maritime System Integration Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 7.1.1. Hardware

- 7.1.2. Software

- 7.1.3. Service

- 7.2. Market Analysis, Insights and Forecast - by System Type

- 7.2.1. Combat Systems

- 7.2.2. Navigation Systems

- 7.2.3. Communication Systems

- 7.2.4. Propulsion & Machinery Management (PMS)

- 7.2.5. Others

- 7.3. Market Analysis, Insights and Forecast - by Technology

- 7.3.1. internet of Things (IoT)

- 7.3.2. Artificial Intelligence (AI)

- 7.3.3. Automation and Control Systems

- 7.3.4. Data Analytics

- 7.4. Market Analysis, Insights and Forecast - by Vessel Type

- 7.4.1. Cargo Ships

- 7.4.2. Tankers

- 7.4.3. Passenger Ships

- 7.4.4. Fishing Vessels

- 7.4.5. Naval Vessels

- 7.4.6. Offshore Support Vessels

- 7.4.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Offering

- 8. South America Maritime System Integration Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 8.1.1. Hardware

- 8.1.2. Software

- 8.1.3. Service

- 8.2. Market Analysis, Insights and Forecast - by System Type

- 8.2.1. Combat Systems

- 8.2.2. Navigation Systems

- 8.2.3. Communication Systems

- 8.2.4. Propulsion & Machinery Management (PMS)

- 8.2.5. Others

- 8.3. Market Analysis, Insights and Forecast - by Technology

- 8.3.1. internet of Things (IoT)

- 8.3.2. Artificial Intelligence (AI)

- 8.3.3. Automation and Control Systems

- 8.3.4. Data Analytics

- 8.4. Market Analysis, Insights and Forecast - by Vessel Type

- 8.4.1. Cargo Ships

- 8.4.2. Tankers

- 8.4.3. Passenger Ships

- 8.4.4. Fishing Vessels

- 8.4.5. Naval Vessels

- 8.4.6. Offshore Support Vessels

- 8.4.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Offering

- 9. Europe Maritime System Integration Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 9.1.1. Hardware

- 9.1.2. Software

- 9.1.3. Service

- 9.2. Market Analysis, Insights and Forecast - by System Type

- 9.2.1. Combat Systems

- 9.2.2. Navigation Systems

- 9.2.3. Communication Systems

- 9.2.4. Propulsion & Machinery Management (PMS)

- 9.2.5. Others

- 9.3. Market Analysis, Insights and Forecast - by Technology

- 9.3.1. internet of Things (IoT)

- 9.3.2. Artificial Intelligence (AI)

- 9.3.3. Automation and Control Systems

- 9.3.4. Data Analytics

- 9.4. Market Analysis, Insights and Forecast - by Vessel Type

- 9.4.1. Cargo Ships

- 9.4.2. Tankers

- 9.4.3. Passenger Ships

- 9.4.4. Fishing Vessels

- 9.4.5. Naval Vessels

- 9.4.6. Offshore Support Vessels

- 9.4.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Offering

- 10. Middle East & Africa Maritime System Integration Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 10.1.1. Hardware

- 10.1.2. Software

- 10.1.3. Service

- 10.2. Market Analysis, Insights and Forecast - by System Type

- 10.2.1. Combat Systems

- 10.2.2. Navigation Systems

- 10.2.3. Communication Systems

- 10.2.4. Propulsion & Machinery Management (PMS)

- 10.2.5. Others

- 10.3. Market Analysis, Insights and Forecast - by Technology

- 10.3.1. internet of Things (IoT)

- 10.3.2. Artificial Intelligence (AI)

- 10.3.3. Automation and Control Systems

- 10.3.4. Data Analytics

- 10.4. Market Analysis, Insights and Forecast - by Vessel Type

- 10.4.1. Cargo Ships

- 10.4.2. Tankers

- 10.4.3. Passenger Ships

- 10.4.4. Fishing Vessels

- 10.4.5. Naval Vessels

- 10.4.6. Offshore Support Vessels

- 10.4.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Offering

- 11. Asia Pacific Maritime System Integration Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 11.1.1. Hardware

- 11.1.2. Software

- 11.1.3. Service

- 11.2. Market Analysis, Insights and Forecast - by System Type

- 11.2.1. Combat Systems

- 11.2.2. Navigation Systems

- 11.2.3. Communication Systems

- 11.2.4. Propulsion & Machinery Management (PMS)

- 11.2.5. Others

- 11.3. Market Analysis, Insights and Forecast - by Technology

- 11.3.1. internet of Things (IoT)

- 11.3.2. Artificial Intelligence (AI)

- 11.3.3. Automation and Control Systems

- 11.3.4. Data Analytics

- 11.4. Market Analysis, Insights and Forecast - by Vessel Type

- 11.4.1. Cargo Ships

- 11.4.2. Tankers

- 11.4.3. Passenger Ships

- 11.4.4. Fishing Vessels

- 11.4.5. Naval Vessels

- 11.4.6. Offshore Support Vessels

- 11.4.7. Others

- 11.1. Market Analysis, Insights and Forecast - by Offering

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SEAIRTECH

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Trelleborg Marine and Infrastructure

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Quad Plus

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 RH Marine

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 European Maritime Safety Agency

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 L3Harris Technologies

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Norwegian Electric System

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Youredi

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Drumgrange

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Britton Marine Systems

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Gebhard Electro

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 HEITEC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Karl Senner

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Vard Electro

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 SEAIRTECH

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Maritime System Integration Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Maritime System Integration Revenue (billion), by Offering 2025 & 2033

- Figure 3: North America Maritime System Integration Revenue Share (%), by Offering 2025 & 2033

- Figure 4: North America Maritime System Integration Revenue (billion), by System Type 2025 & 2033

- Figure 5: North America Maritime System Integration Revenue Share (%), by System Type 2025 & 2033

- Figure 6: North America Maritime System Integration Revenue (billion), by Technology 2025 & 2033

- Figure 7: North America Maritime System Integration Revenue Share (%), by Technology 2025 & 2033

- Figure 8: North America Maritime System Integration Revenue (billion), by Vessel Type 2025 & 2033

- Figure 9: North America Maritime System Integration Revenue Share (%), by Vessel Type 2025 & 2033

- Figure 10: North America Maritime System Integration Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Maritime System Integration Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Maritime System Integration Revenue (billion), by Offering 2025 & 2033

- Figure 13: South America Maritime System Integration Revenue Share (%), by Offering 2025 & 2033

- Figure 14: South America Maritime System Integration Revenue (billion), by System Type 2025 & 2033

- Figure 15: South America Maritime System Integration Revenue Share (%), by System Type 2025 & 2033

- Figure 16: South America Maritime System Integration Revenue (billion), by Technology 2025 & 2033

- Figure 17: South America Maritime System Integration Revenue Share (%), by Technology 2025 & 2033

- Figure 18: South America Maritime System Integration Revenue (billion), by Vessel Type 2025 & 2033

- Figure 19: South America Maritime System Integration Revenue Share (%), by Vessel Type 2025 & 2033

- Figure 20: South America Maritime System Integration Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Maritime System Integration Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Maritime System Integration Revenue (billion), by Offering 2025 & 2033

- Figure 23: Europe Maritime System Integration Revenue Share (%), by Offering 2025 & 2033

- Figure 24: Europe Maritime System Integration Revenue (billion), by System Type 2025 & 2033

- Figure 25: Europe Maritime System Integration Revenue Share (%), by System Type 2025 & 2033

- Figure 26: Europe Maritime System Integration Revenue (billion), by Technology 2025 & 2033

- Figure 27: Europe Maritime System Integration Revenue Share (%), by Technology 2025 & 2033

- Figure 28: Europe Maritime System Integration Revenue (billion), by Vessel Type 2025 & 2033

- Figure 29: Europe Maritime System Integration Revenue Share (%), by Vessel Type 2025 & 2033

- Figure 30: Europe Maritime System Integration Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Maritime System Integration Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Maritime System Integration Revenue (billion), by Offering 2025 & 2033

- Figure 33: Middle East & Africa Maritime System Integration Revenue Share (%), by Offering 2025 & 2033

- Figure 34: Middle East & Africa Maritime System Integration Revenue (billion), by System Type 2025 & 2033

- Figure 35: Middle East & Africa Maritime System Integration Revenue Share (%), by System Type 2025 & 2033

- Figure 36: Middle East & Africa Maritime System Integration Revenue (billion), by Technology 2025 & 2033

- Figure 37: Middle East & Africa Maritime System Integration Revenue Share (%), by Technology 2025 & 2033

- Figure 38: Middle East & Africa Maritime System Integration Revenue (billion), by Vessel Type 2025 & 2033

- Figure 39: Middle East & Africa Maritime System Integration Revenue Share (%), by Vessel Type 2025 & 2033

- Figure 40: Middle East & Africa Maritime System Integration Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Maritime System Integration Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Maritime System Integration Revenue (billion), by Offering 2025 & 2033

- Figure 43: Asia Pacific Maritime System Integration Revenue Share (%), by Offering 2025 & 2033

- Figure 44: Asia Pacific Maritime System Integration Revenue (billion), by System Type 2025 & 2033

- Figure 45: Asia Pacific Maritime System Integration Revenue Share (%), by System Type 2025 & 2033

- Figure 46: Asia Pacific Maritime System Integration Revenue (billion), by Technology 2025 & 2033

- Figure 47: Asia Pacific Maritime System Integration Revenue Share (%), by Technology 2025 & 2033

- Figure 48: Asia Pacific Maritime System Integration Revenue (billion), by Vessel Type 2025 & 2033

- Figure 49: Asia Pacific Maritime System Integration Revenue Share (%), by Vessel Type 2025 & 2033

- Figure 50: Asia Pacific Maritime System Integration Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Maritime System Integration Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Maritime System Integration Revenue billion Forecast, by Offering 2020 & 2033

- Table 2: Global Maritime System Integration Revenue billion Forecast, by System Type 2020 & 2033

- Table 3: Global Maritime System Integration Revenue billion Forecast, by Technology 2020 & 2033

- Table 4: Global Maritime System Integration Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 5: Global Maritime System Integration Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Maritime System Integration Revenue billion Forecast, by Offering 2020 & 2033

- Table 7: Global Maritime System Integration Revenue billion Forecast, by System Type 2020 & 2033

- Table 8: Global Maritime System Integration Revenue billion Forecast, by Technology 2020 & 2033

- Table 9: Global Maritime System Integration Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 10: Global Maritime System Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Maritime System Integration Revenue billion Forecast, by Offering 2020 & 2033

- Table 15: Global Maritime System Integration Revenue billion Forecast, by System Type 2020 & 2033

- Table 16: Global Maritime System Integration Revenue billion Forecast, by Technology 2020 & 2033

- Table 17: Global Maritime System Integration Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 18: Global Maritime System Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Maritime System Integration Revenue billion Forecast, by Offering 2020 & 2033

- Table 23: Global Maritime System Integration Revenue billion Forecast, by System Type 2020 & 2033

- Table 24: Global Maritime System Integration Revenue billion Forecast, by Technology 2020 & 2033

- Table 25: Global Maritime System Integration Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 26: Global Maritime System Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Maritime System Integration Revenue billion Forecast, by Offering 2020 & 2033

- Table 37: Global Maritime System Integration Revenue billion Forecast, by System Type 2020 & 2033

- Table 38: Global Maritime System Integration Revenue billion Forecast, by Technology 2020 & 2033

- Table 39: Global Maritime System Integration Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 40: Global Maritime System Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Maritime System Integration Revenue billion Forecast, by Offering 2020 & 2033

- Table 48: Global Maritime System Integration Revenue billion Forecast, by System Type 2020 & 2033

- Table 49: Global Maritime System Integration Revenue billion Forecast, by Technology 2020 & 2033

- Table 50: Global Maritime System Integration Revenue billion Forecast, by Vessel Type 2020 & 2033

- Table 51: Global Maritime System Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Maritime System Integration Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Maritime System Integration?

The projected CAGR is approximately 8.9%.

2. Which companies are prominent players in the Maritime System Integration?

Key companies in the market include SEAIRTECH, Trelleborg Marine and Infrastructure, Quad Plus, RH Marine, European Maritime Safety Agency, L3Harris Technologies, Norwegian Electric System, Youredi, Drumgrange, Britton Marine Systems, Gebhard Electro, HEITEC, Karl Senner, Vard Electro.

3. What are the main segments of the Maritime System Integration?

The market segments include Offering, System Type, Technology, Vessel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 6 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Maritime System Integration," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Maritime System Integration report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Maritime System Integration?

To stay informed about further developments, trends, and reports in the Maritime System Integration, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence