Key Insights for Medical Device Repair Service Market

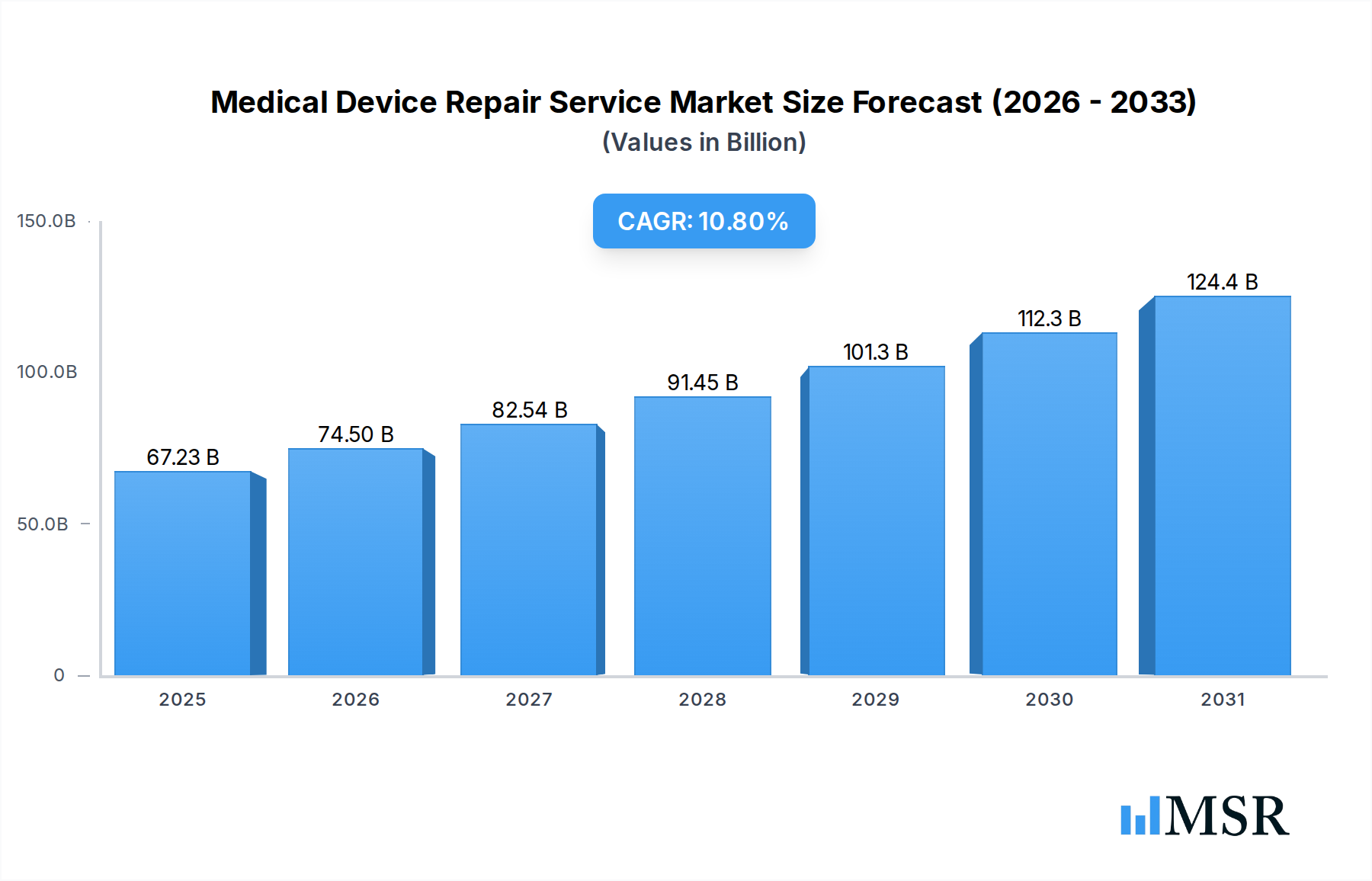

The Global Medical Device Repair Service Market is poised for substantial growth, projected to escalate from an estimated $60.68 billion in 2025 to approximately $139.4 billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 10.8% over the forecast period. This significant expansion is underpinned by a confluence of factors, including the burgeoning global installed base of medical devices, the increasing complexity of modern healthcare technology, and the persistent need for cost containment within healthcare systems. The market's trajectory is primarily driven by the imperative for healthcare providers to maximize asset utilization and extend the operational lifespan of high-value equipment. As healthcare expenditure continues its upward trend globally, there is a heightened focus on optimizing existing investments rather than solely relying on new capital acquisitions. This drives demand for comprehensive repair, maintenance, and calibration services across a diverse range of medical devices.

Medical Device Repair Service Market Size (In Billion)

Macroeconomic tailwinds such as an aging global population and the escalating prevalence of chronic diseases are contributing to a sustained increase in diagnostic and therapeutic procedures, directly correlating with a greater demand for functional and reliable medical equipment. Furthermore, advancements in medical device technology, while enhancing clinical outcomes, often introduce increased complexity in device architecture, necessitating specialized repair and technical expertise. This fosters opportunities for original equipment manufacturers (OEMs) and independent service organizations (ISOs) alike. The market is also experiencing a shift towards proactive service models, with the Preventive Maintenance Market gaining traction as facilities seek to mitigate costly downtime and ensure regulatory compliance. Geographically, while North America and Europe represent mature markets with significant installed bases, the Asia Pacific region is anticipated to exhibit the most accelerated growth, propelled by expanding healthcare infrastructure and rising medical tourism. The strategic outsourcing of device maintenance, evident in the growth of the Medical Device Outsourcing Market, is another critical trend enabling healthcare facilities to focus on core patient care activities while ensuring specialized technical support.

Medical Device Repair Service Company Market Share

The Dominance of Hospitals in the Medical Device Repair Service Market

The end-user segment of Hospitals holds a commanding share of the Medical Device Repair Service Market, attributed to their extensive infrastructure, diverse range of medical specialties, and high patient volumes. Hospitals typically operate a vast inventory of sophisticated medical equipment, ranging from critical care and surgical instruments to advanced diagnostic imaging systems and patient monitoring devices. This substantial asset base necessitates continuous maintenance and frequent repair services to ensure operational reliability and patient safety. The critical nature of hospital operations means that equipment downtime can have severe implications for patient care and financial stability, thus driving a constant demand for prompt and effective repair solutions. The Hospital Services Market encompasses a wide array of service requirements, reflecting the breadth of devices in use.

Within this dominant segment, both OEMs and independent service organizations (ISOs) play crucial roles. OEMs often provide bundled service contracts at the point of sale, leveraging their proprietary knowledge and access to genuine parts for complex devices such as those found in the Diagnostic Imaging Devices Market and Ventilators Market. However, ISOs are increasingly gaining market share by offering competitive pricing, quicker response times, and multi-vendor service capabilities, which is particularly appealing to hospitals seeking cost-efficiency and flexible service agreements. In-house service teams within hospitals also contribute significantly, handling routine maintenance and basic repairs, but often rely on external providers for specialized or complex issues. The increasing burden on hospital budgets is leading many institutions to explore hybrid service models, combining in-house capabilities with outsourced expertise for areas like the Surgical Instruments Market or electrotherapy devices. While Ambulatory Surgical Centers Market and Diagnostic Imaging Centers are growing rapidly, the sheer scale and complexity of equipment within hospitals ensure their continued dominance in the Medical Device Repair Service Market. This dominance is further solidified by the constant technological upgrades in hospital environments, which require ongoing service expertise to integrate and maintain new devices, ensuring seamless workflow and optimal performance. The critical importance of continuous operation in a hospital setting, coupled with regulatory requirements for device uptime and safety, reinforces the sustained high demand for comprehensive repair and maintenance services, underpinning the segment's leading position.

Key Market Drivers in Medical Device Repair Service Market

The Medical Device Repair Service Market is propelled by several potent drivers, each rooted in significant industry trends and quantifiable shifts in healthcare dynamics. A primary driver is the expanding global installed base of medical devices, which naturally escalates the demand for corresponding repair and maintenance services. This expansion is fueled by an aging global population, with the number of individuals aged 65 and over projected to surpass 1.5 billion by 2050, directly correlating with a higher prevalence of chronic diseases requiring ongoing medical intervention and an extensive array of diagnostic and therapeutic equipment. For instance, the demand for devices related to cardiovascular, respiratory, and neurological conditions directly translates into increased service needs.

Another significant catalyst is the increasing technological complexity of medical devices. Modern equipment, such as advanced MRI scanners, robotic surgical systems, and sophisticated patient monitoring equipment, incorporates intricate electronics, software, and precision mechanics. These devices, integral to the Healthcare IT Market, require highly specialized technical expertise and proprietary tools for accurate diagnosis and repair. The average repair cost for a complex diagnostic imaging device can range from $5,000 to over $100,000, underscoring the specialized nature of these services. Furthermore, the rising global healthcare expenditure, which now exceeds $9 trillion annually, places immense pressure on healthcare providers to optimize asset utilization and extend the lifespan of costly capital equipment. Hospitals and clinics are increasingly recognizing that investing in timely repairs and comprehensive Preventive Maintenance Market strategies is more cost-effective than frequent capital outlays for new equipment, thereby supporting the growth of the Medical Device Repair Service Market. This cost-containment imperative is particularly acute in settings like the Ambulatory Surgical Centers Market where efficiency is paramount. Lastly, a growing focus on regulatory compliance and patient safety mandates regular calibration and functional testing of medical devices. Non-compliance can lead to severe penalties, loss of accreditation, and compromised patient outcomes, compelling healthcare facilities to prioritize professional repair and maintenance services.

Competitive Ecosystem of Medical Device Repair Service Market

The Medical Device Repair Service Market is characterized by a mix of established original equipment manufacturers (OEMs), agile independent service organizations (ISOs), and burgeoning in-house service teams, all vying for market share. Competition centers on service quality, response time, technical expertise, and cost-effectiveness.

- Koninklijke Philips: A global leader in health technology, Philips offers comprehensive service contracts and repairs for its extensive portfolio, including diagnostic imaging, patient monitoring, and critical care solutions, leveraging its proprietary technology and global service network.

- GE Healthcare: A major player providing an array of services for its broad medical device range, with significant strength in diagnostic imaging and life sciences, focusing on integrated solutions to maximize equipment uptime and efficiency.

- Abbott Laboratories: Specializes in diagnostics, medical devices, and nutrition, with service offerings primarily concentrated on maintaining its own advanced diagnostic systems and cardiovascular devices, ensuring reliability for critical healthcare applications.

- Siemens Healthineers: A key innovator in medical technology, Siemens provides extensive maintenance and repair services for its sophisticated diagnostic and therapeutic systems globally, emphasizing digitalization and remote service capabilities.

- PrimedeQ: An independent service organization focusing on delivering cost-effective and efficient repair and maintenance solutions for a wide range of medical equipment, serving as an alternative to OEM services.

- Drägerwerk AG & Co. KGaA: Known for medical and safety technology, Drägerwerk provides specialized services for its anesthesia, ventilation, and patient monitoring systems, ensuring high standards of operational safety and performance.

- Nordic Service Group: An independent multi-vendor service provider primarily serving Northern Europe, offering comprehensive repair and maintenance for medical devices with a focus on quick service delivery and customer satisfaction.

- Gumbo Medical: Specializes in the refurbishment and servicing of medical equipment, often providing sustainable and economical alternatives for healthcare facilities looking to extend the life of their devices.

- Medical Equipment Repair Associates: An independent service provider dedicated to offering flexible and cost-effective repair and maintenance solutions across a broad spectrum of medical devices, catering to varied client needs.

- Agiliti Health: Offers comprehensive healthcare technology management and surgical equipment repair services, providing integrated solutions to optimize equipment performance and clinical outcomes for healthcare systems.

- ACF Medical: Provides medical equipment repair, calibration, and maintenance services, often specializing in specific device types and catering to the needs of smaller clinics and ambulatory surgical centers.

- Crothall Healthcare: As part of Compass Group, Crothall offers clinical engineering services, including medical equipment repair, as part of broader facilities management solutions for large healthcare networks.

- Eikon Medical Solutions: Specializes in services for diagnostic imaging equipment, offering repairs, maintenance, and parts supply for high-value modalities such as MRI and CT systems.

- Healthcare 21: A prominent provider of healthcare solutions, including medical equipment service and support, primarily active in the UK and Ireland, focusing on enhancing clinical efficiency and device reliability.

Recent Developments & Milestones in Medical Device Repair Service Market

The Medical Device Repair Service Market is continually evolving, driven by technological advancements, strategic collaborations, and an evolving regulatory landscape. Key developments highlight the industry's response to rising demand and operational complexities.

- January 2024: A leading OEM announced a strategic partnership with a prominent independent service organization (ISO) to expand its reach for basic and moderate repairs of

Diagnostic Imaging Devices Marketin underserved regions, aiming to improve service accessibility and efficiency. - March 2024: Regulatory bodies in Europe updated guidelines concerning cybersecurity in networked medical devices, impacting service protocols for device maintenance and repair to enhance data protection and system integrity.

- June 2024: A significant investment round was secured by a startup specializing in AI-driven predictive maintenance solutions for patient monitoring equipment, aiming to leverage artificial intelligence to reduce device downtime and optimize service schedules.

- September 2024: Several major hospital networks across North America implemented new in-house training programs to enhance their biomedical engineering teams' capabilities for complex repairs of

Surgical Instruments Market, seeking greater operational autonomy and cost savings. - November 2024: A consortium of medical device manufacturers and repair service providers launched a joint initiative to standardize repair part nomenclature and availability, addressing long-standing challenges in the supply chain for generic components within the Medical Device Repair Service Market.

- February 2025: The introduction of new remote diagnostics platforms by several service providers allowed for real-time monitoring and preliminary troubleshooting of

Ventilators Marketand anesthesia equipment, significantly improving response times and reducing on-site visit frequency.

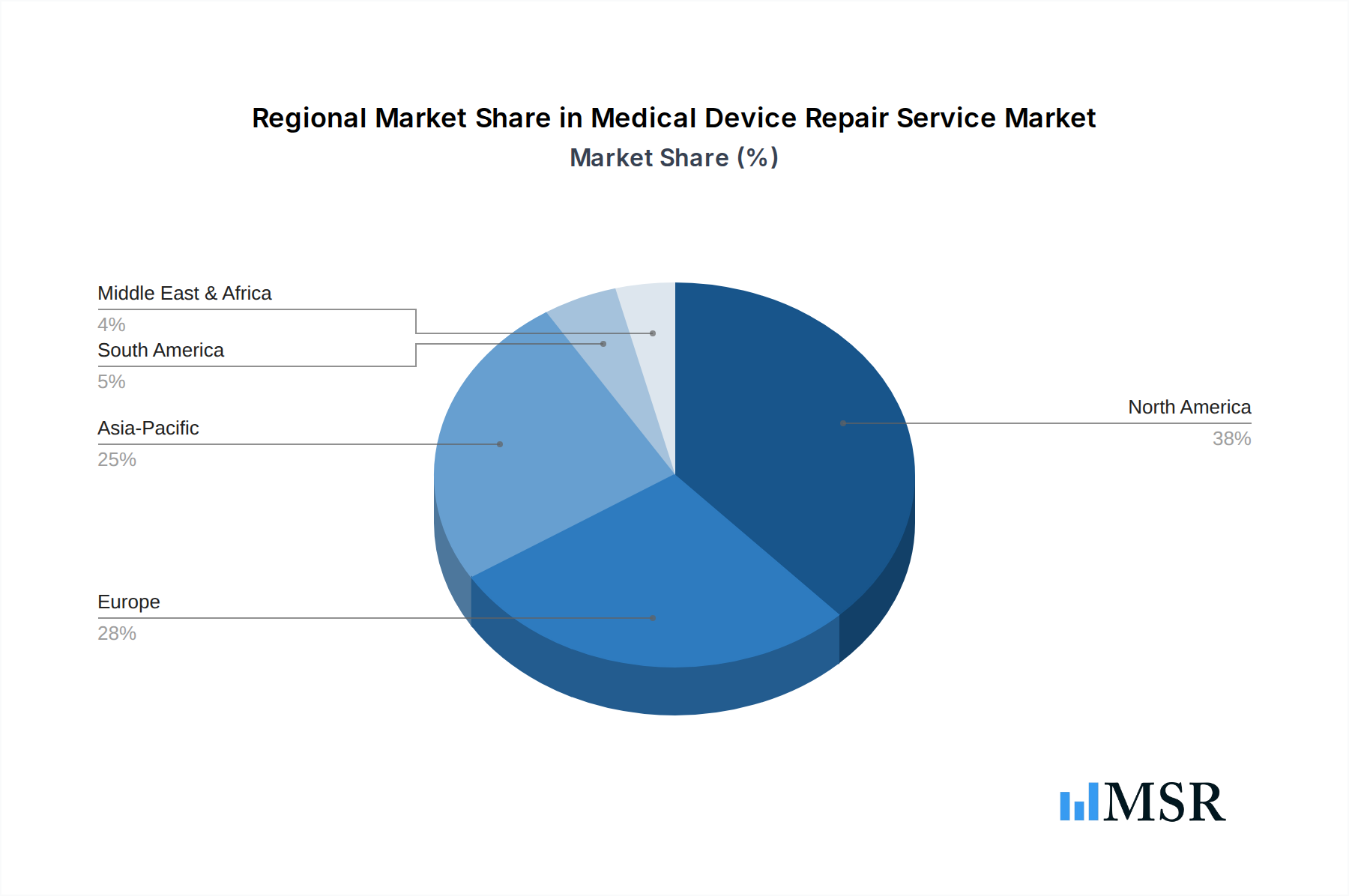

Regional Market Breakdown for Medical Device Repair Service Market

The Medical Device Repair Service Market exhibits distinct characteristics across key global regions, driven by varying healthcare infrastructures, regulatory environments, and expenditure patterns.

North America currently holds the largest revenue share in the Medical Device Repair Service Market, primarily due to its advanced healthcare infrastructure, high adoption rate of sophisticated medical devices, and significant healthcare spending. The United States, in particular, contributes substantially, driven by a large installed base of high-value equipment and stringent regulatory requirements for device maintenance. While a mature market, North America maintains a steady growth trajectory, with a notable emphasis on extending the lifespan of costly equipment through robust repair and Preventive Maintenance Market strategies.

Europe represents another significant market, characterized by well-established healthcare systems and a strong focus on quality and regulatory compliance (e.g., CE Mark certification for devices). Countries like Germany, France, and the UK lead in demand for high-quality repair services, particularly for specialized equipment used in the Hospital Services Market. Europe's growth is stable, driven by an aging population and continued investment in healthcare technology, alongside increasing competition between OEMs and ISOs.

Asia Pacific is projected to be the fastest-growing region in the Medical Device Repair Service Market, poised for exceptional CAGR over the forecast period. This rapid expansion is fueled by the burgeoning healthcare infrastructure in countries like China and India, rising disposable incomes, increasing prevalence of chronic diseases, and expanding medical tourism. The region is witnessing significant investment in new hospitals and diagnostic centers, leading to a surge in the installed base of medical devices. The demand for cost-effective repair solutions is high, fostering opportunities for both local and international service providers. The emerging focus on Healthcare IT Market integration further enhances device complexity and the need for specialized service.

Middle East & Africa and South America are emerging markets experiencing moderate growth. Increased government spending on healthcare infrastructure, particularly in the GCC countries and Brazil, is driving the adoption of modern medical devices. However, challenges such as limited skilled technicians and fragmented supply chains for spare parts can impact service delivery. Nevertheless, the growing awareness of the importance of device uptime and patient safety is gradually boosting demand for professional repair services in these regions.

Medical Device Repair Service Regional Market Share

Supply Chain & Raw Material Dynamics for Medical Device Repair Service Market

The efficacy of the Medical Device Repair Service Market is intimately linked to the robustness and resilience of its upstream supply chain. Dependencies span a complex array of components, from advanced electronics to specialized materials. Key inputs include microprocessors, sensors, circuit boards, display panels, optical components for imaging devices, and various grades of Medical Plastics Market and metals for device casings and internal structures. Sourcing risks are pronounced due to the globalized and often concentrated nature of component manufacturing. Geopolitical tensions, trade disputes, and natural disasters, as evidenced by disruptions during the COVID-19 pandemic, can significantly impact the availability and lead times of critical parts, particularly for highly specialized and proprietary components. This vulnerability affects the Medical Device Outsourcing Market as well.

Price volatility of essential raw materials like rare earth metals (used in magnetic resonance imaging, for instance), specific polymers, and precious metals (found in connectors and circuitry) directly influences repair costs. For example, fluctuations in copper prices can affect wiring and electrical component costs, while changes in the cost of medical-grade polycarbonate or silicone impact device casings and tubing. Historically, unexpected surges in demand or supply chain bottlenecks have led to component shortages, increasing repair turnaround times and, consequently, device downtime for healthcare facilities. This has prompted a strategic shift towards diversifying supplier bases and, in some cases, considering component redesigns to incorporate more readily available materials. Furthermore, the increasing sophistication of medical devices means that a single point of failure for a highly integrated custom component can render an entire system inoperable, highlighting the reliance on precise, often OEM-controlled, supply channels. Efforts to enhance transparency and traceability within the supply chain are ongoing, aiming to mitigate risks and ensure a more stable flow of critical spare parts for the Medical Device Repair Service Market.

Regulatory & Policy Landscape Shaping Medical Device Repair Service Market

The Medical Device Repair Service Market operates within a stringent and evolving global regulatory and policy landscape, primarily driven by concerns for patient safety, device efficacy, and data security. Major regulatory bodies like the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA) via the CE Marking process, Japan's Pharmaceuticals and Medical Devices Agency (PMDA), and the Medicines and Healthcare products Regulatory Agency (MHRA) in the UK, establish comprehensive frameworks. These frameworks govern not only the manufacturing and market authorization of medical devices but also their post-market surveillance, maintenance, and repair.

Key regulations impacting the market include ISO 13485 (Medical devices – Quality management systems – Requirements for regulatory purposes), which sets the international standard for quality management systems specific to the medical device industry, encompassing service and repair. Recent policy changes have heavily emphasized cybersecurity for networked medical devices. The FDA's updated guidance on pre- and post-market cybersecurity management and Europe's NIS2 Directive (Network and Information Security) compel service providers to implement robust security measures during repair and maintenance to protect patient data and device functionality. This significantly impacts how diagnostic imaging devices or patient monitoring equipment in the Healthcare IT Market are serviced. Furthermore, a burgeoning 'Right to Repair' movement is gaining traction, particularly in the United States and parts of Europe. This legislative push seeks to mandate that OEMs provide independent repair shops and consumers with access to necessary parts, tools, and service manuals. If widely adopted, this could profoundly reshape the competitive dynamics, potentially increasing the market share for independent service organizations (ISOs) within the Medical Device Repair Service Market by reducing their dependency on OEM-controlled parts and information. Environmental policies, such as the EU's WEEE (Waste Electrical and Electronic Equipment) Directive, also influence the market by dictating the environmentally sound disposal and recycling of electronic components and end-of-life devices, pushing service providers towards sustainable repair and refurbishment practices.

Medical Device Repair Service Segmentation

-

1. Service Type

- 1.1. Preventive Maintenance

- 1.2. Electrical Safety Test

- 1.3. Operational Test

- 1.4. Repair Services

- 1.5. Others

-

2. Repair Type

- 2.1. Basic Repairs

- 2.2. Moderate Repairs

- 2.3. Complex Repairs

-

3. Device Type

- 3.1. Electrotherapy Devices

- 3.2. Diagnostic Imaging Devices

- 3.3. Monitoring Equipment

- 3.4. Surgical Instruments

- 3.5. Ventilators and Anesthesia Equipment

- 3.6. Others

-

4. Service Provider

- 4.1. OEMs

- 4.2. ISOs

- 4.3. In-House Service Teams

-

5. End User

- 5.1. Hospitals

- 5.2. Diagnostic Imaging Centers

- 5.3. Ambulatory Surgical Centers

- 5.4. Others

Medical Device Repair Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Device Repair Service Regional Market Share

Geographic Coverage of Medical Device Repair Service

Medical Device Repair Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Preventive Maintenance

- 5.1.2. Electrical Safety Test

- 5.1.3. Operational Test

- 5.1.4. Repair Services

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Repair Type

- 5.2.1. Basic Repairs

- 5.2.2. Moderate Repairs

- 5.2.3. Complex Repairs

- 5.3. Market Analysis, Insights and Forecast - by Device Type

- 5.3.1. Electrotherapy Devices

- 5.3.2. Diagnostic Imaging Devices

- 5.3.3. Monitoring Equipment

- 5.3.4. Surgical Instruments

- 5.3.5. Ventilators and Anesthesia Equipment

- 5.3.6. Others

- 5.4. Market Analysis, Insights and Forecast - by Service Provider

- 5.4.1. OEMs

- 5.4.2. ISOs

- 5.4.3. In-House Service Teams

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Hospitals

- 5.5.2. Diagnostic Imaging Centers

- 5.5.3. Ambulatory Surgical Centers

- 5.5.4. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. Global Medical Device Repair Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Preventive Maintenance

- 6.1.2. Electrical Safety Test

- 6.1.3. Operational Test

- 6.1.4. Repair Services

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Repair Type

- 6.2.1. Basic Repairs

- 6.2.2. Moderate Repairs

- 6.2.3. Complex Repairs

- 6.3. Market Analysis, Insights and Forecast - by Device Type

- 6.3.1. Electrotherapy Devices

- 6.3.2. Diagnostic Imaging Devices

- 6.3.3. Monitoring Equipment

- 6.3.4. Surgical Instruments

- 6.3.5. Ventilators and Anesthesia Equipment

- 6.3.6. Others

- 6.4. Market Analysis, Insights and Forecast - by Service Provider

- 6.4.1. OEMs

- 6.4.2. ISOs

- 6.4.3. In-House Service Teams

- 6.5. Market Analysis, Insights and Forecast - by End User

- 6.5.1. Hospitals

- 6.5.2. Diagnostic Imaging Centers

- 6.5.3. Ambulatory Surgical Centers

- 6.5.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. North America Medical Device Repair Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 7.1.1. Preventive Maintenance

- 7.1.2. Electrical Safety Test

- 7.1.3. Operational Test

- 7.1.4. Repair Services

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Repair Type

- 7.2.1. Basic Repairs

- 7.2.2. Moderate Repairs

- 7.2.3. Complex Repairs

- 7.3. Market Analysis, Insights and Forecast - by Device Type

- 7.3.1. Electrotherapy Devices

- 7.3.2. Diagnostic Imaging Devices

- 7.3.3. Monitoring Equipment

- 7.3.4. Surgical Instruments

- 7.3.5. Ventilators and Anesthesia Equipment

- 7.3.6. Others

- 7.4. Market Analysis, Insights and Forecast - by Service Provider

- 7.4.1. OEMs

- 7.4.2. ISOs

- 7.4.3. In-House Service Teams

- 7.5. Market Analysis, Insights and Forecast - by End User

- 7.5.1. Hospitals

- 7.5.2. Diagnostic Imaging Centers

- 7.5.3. Ambulatory Surgical Centers

- 7.5.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Service Type

- 8. South America Medical Device Repair Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 8.1.1. Preventive Maintenance

- 8.1.2. Electrical Safety Test

- 8.1.3. Operational Test

- 8.1.4. Repair Services

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Repair Type

- 8.2.1. Basic Repairs

- 8.2.2. Moderate Repairs

- 8.2.3. Complex Repairs

- 8.3. Market Analysis, Insights and Forecast - by Device Type

- 8.3.1. Electrotherapy Devices

- 8.3.2. Diagnostic Imaging Devices

- 8.3.3. Monitoring Equipment

- 8.3.4. Surgical Instruments

- 8.3.5. Ventilators and Anesthesia Equipment

- 8.3.6. Others

- 8.4. Market Analysis, Insights and Forecast - by Service Provider

- 8.4.1. OEMs

- 8.4.2. ISOs

- 8.4.3. In-House Service Teams

- 8.5. Market Analysis, Insights and Forecast - by End User

- 8.5.1. Hospitals

- 8.5.2. Diagnostic Imaging Centers

- 8.5.3. Ambulatory Surgical Centers

- 8.5.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Service Type

- 9. Europe Medical Device Repair Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 9.1.1. Preventive Maintenance

- 9.1.2. Electrical Safety Test

- 9.1.3. Operational Test

- 9.1.4. Repair Services

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Repair Type

- 9.2.1. Basic Repairs

- 9.2.2. Moderate Repairs

- 9.2.3. Complex Repairs

- 9.3. Market Analysis, Insights and Forecast - by Device Type

- 9.3.1. Electrotherapy Devices

- 9.3.2. Diagnostic Imaging Devices

- 9.3.3. Monitoring Equipment

- 9.3.4. Surgical Instruments

- 9.3.5. Ventilators and Anesthesia Equipment

- 9.3.6. Others

- 9.4. Market Analysis, Insights and Forecast - by Service Provider

- 9.4.1. OEMs

- 9.4.2. ISOs

- 9.4.3. In-House Service Teams

- 9.5. Market Analysis, Insights and Forecast - by End User

- 9.5.1. Hospitals

- 9.5.2. Diagnostic Imaging Centers

- 9.5.3. Ambulatory Surgical Centers

- 9.5.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Service Type

- 10. Middle East & Africa Medical Device Repair Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 10.1.1. Preventive Maintenance

- 10.1.2. Electrical Safety Test

- 10.1.3. Operational Test

- 10.1.4. Repair Services

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Repair Type

- 10.2.1. Basic Repairs

- 10.2.2. Moderate Repairs

- 10.2.3. Complex Repairs

- 10.3. Market Analysis, Insights and Forecast - by Device Type

- 10.3.1. Electrotherapy Devices

- 10.3.2. Diagnostic Imaging Devices

- 10.3.3. Monitoring Equipment

- 10.3.4. Surgical Instruments

- 10.3.5. Ventilators and Anesthesia Equipment

- 10.3.6. Others

- 10.4. Market Analysis, Insights and Forecast - by Service Provider

- 10.4.1. OEMs

- 10.4.2. ISOs

- 10.4.3. In-House Service Teams

- 10.5. Market Analysis, Insights and Forecast - by End User

- 10.5.1. Hospitals

- 10.5.2. Diagnostic Imaging Centers

- 10.5.3. Ambulatory Surgical Centers

- 10.5.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Service Type

- 11. Asia Pacific Medical Device Repair Service Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 11.1.1. Preventive Maintenance

- 11.1.2. Electrical Safety Test

- 11.1.3. Operational Test

- 11.1.4. Repair Services

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Repair Type

- 11.2.1. Basic Repairs

- 11.2.2. Moderate Repairs

- 11.2.3. Complex Repairs

- 11.3. Market Analysis, Insights and Forecast - by Device Type

- 11.3.1. Electrotherapy Devices

- 11.3.2. Diagnostic Imaging Devices

- 11.3.3. Monitoring Equipment

- 11.3.4. Surgical Instruments

- 11.3.5. Ventilators and Anesthesia Equipment

- 11.3.6. Others

- 11.4. Market Analysis, Insights and Forecast - by Service Provider

- 11.4.1. OEMs

- 11.4.2. ISOs

- 11.4.3. In-House Service Teams

- 11.5. Market Analysis, Insights and Forecast - by End User

- 11.5.1. Hospitals

- 11.5.2. Diagnostic Imaging Centers

- 11.5.3. Ambulatory Surgical Centers

- 11.5.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Service Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Koninklijke Philips

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 GE Healthcare

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Abbott Laboratories

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Siemens

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 PrimedeQ

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Drägerwerk

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Nordic Service Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Gumbo Medical

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Medical Equipment Repair Associates

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Agiliti Health

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 ACF Medical

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Crothall Healthcare

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Eikon Medical Solutions

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Healthcare 21

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Others

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Koninklijke Philips

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Medical Device Repair Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Medical Device Repair Service Revenue (billion), by Service Type 2025 & 2033

- Figure 3: North America Medical Device Repair Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 4: North America Medical Device Repair Service Revenue (billion), by Repair Type 2025 & 2033

- Figure 5: North America Medical Device Repair Service Revenue Share (%), by Repair Type 2025 & 2033

- Figure 6: North America Medical Device Repair Service Revenue (billion), by Device Type 2025 & 2033

- Figure 7: North America Medical Device Repair Service Revenue Share (%), by Device Type 2025 & 2033

- Figure 8: North America Medical Device Repair Service Revenue (billion), by Service Provider 2025 & 2033

- Figure 9: North America Medical Device Repair Service Revenue Share (%), by Service Provider 2025 & 2033

- Figure 10: North America Medical Device Repair Service Revenue (billion), by End User 2025 & 2033

- Figure 11: North America Medical Device Repair Service Revenue Share (%), by End User 2025 & 2033

- Figure 12: North America Medical Device Repair Service Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Medical Device Repair Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Medical Device Repair Service Revenue (billion), by Service Type 2025 & 2033

- Figure 15: South America Medical Device Repair Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 16: South America Medical Device Repair Service Revenue (billion), by Repair Type 2025 & 2033

- Figure 17: South America Medical Device Repair Service Revenue Share (%), by Repair Type 2025 & 2033

- Figure 18: South America Medical Device Repair Service Revenue (billion), by Device Type 2025 & 2033

- Figure 19: South America Medical Device Repair Service Revenue Share (%), by Device Type 2025 & 2033

- Figure 20: South America Medical Device Repair Service Revenue (billion), by Service Provider 2025 & 2033

- Figure 21: South America Medical Device Repair Service Revenue Share (%), by Service Provider 2025 & 2033

- Figure 22: South America Medical Device Repair Service Revenue (billion), by End User 2025 & 2033

- Figure 23: South America Medical Device Repair Service Revenue Share (%), by End User 2025 & 2033

- Figure 24: South America Medical Device Repair Service Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Medical Device Repair Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Medical Device Repair Service Revenue (billion), by Service Type 2025 & 2033

- Figure 27: Europe Medical Device Repair Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 28: Europe Medical Device Repair Service Revenue (billion), by Repair Type 2025 & 2033

- Figure 29: Europe Medical Device Repair Service Revenue Share (%), by Repair Type 2025 & 2033

- Figure 30: Europe Medical Device Repair Service Revenue (billion), by Device Type 2025 & 2033

- Figure 31: Europe Medical Device Repair Service Revenue Share (%), by Device Type 2025 & 2033

- Figure 32: Europe Medical Device Repair Service Revenue (billion), by Service Provider 2025 & 2033

- Figure 33: Europe Medical Device Repair Service Revenue Share (%), by Service Provider 2025 & 2033

- Figure 34: Europe Medical Device Repair Service Revenue (billion), by End User 2025 & 2033

- Figure 35: Europe Medical Device Repair Service Revenue Share (%), by End User 2025 & 2033

- Figure 36: Europe Medical Device Repair Service Revenue (billion), by Country 2025 & 2033

- Figure 37: Europe Medical Device Repair Service Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Medical Device Repair Service Revenue (billion), by Service Type 2025 & 2033

- Figure 39: Middle East & Africa Medical Device Repair Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 40: Middle East & Africa Medical Device Repair Service Revenue (billion), by Repair Type 2025 & 2033

- Figure 41: Middle East & Africa Medical Device Repair Service Revenue Share (%), by Repair Type 2025 & 2033

- Figure 42: Middle East & Africa Medical Device Repair Service Revenue (billion), by Device Type 2025 & 2033

- Figure 43: Middle East & Africa Medical Device Repair Service Revenue Share (%), by Device Type 2025 & 2033

- Figure 44: Middle East & Africa Medical Device Repair Service Revenue (billion), by Service Provider 2025 & 2033

- Figure 45: Middle East & Africa Medical Device Repair Service Revenue Share (%), by Service Provider 2025 & 2033

- Figure 46: Middle East & Africa Medical Device Repair Service Revenue (billion), by End User 2025 & 2033

- Figure 47: Middle East & Africa Medical Device Repair Service Revenue Share (%), by End User 2025 & 2033

- Figure 48: Middle East & Africa Medical Device Repair Service Revenue (billion), by Country 2025 & 2033

- Figure 49: Middle East & Africa Medical Device Repair Service Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Medical Device Repair Service Revenue (billion), by Service Type 2025 & 2033

- Figure 51: Asia Pacific Medical Device Repair Service Revenue Share (%), by Service Type 2025 & 2033

- Figure 52: Asia Pacific Medical Device Repair Service Revenue (billion), by Repair Type 2025 & 2033

- Figure 53: Asia Pacific Medical Device Repair Service Revenue Share (%), by Repair Type 2025 & 2033

- Figure 54: Asia Pacific Medical Device Repair Service Revenue (billion), by Device Type 2025 & 2033

- Figure 55: Asia Pacific Medical Device Repair Service Revenue Share (%), by Device Type 2025 & 2033

- Figure 56: Asia Pacific Medical Device Repair Service Revenue (billion), by Service Provider 2025 & 2033

- Figure 57: Asia Pacific Medical Device Repair Service Revenue Share (%), by Service Provider 2025 & 2033

- Figure 58: Asia Pacific Medical Device Repair Service Revenue (billion), by End User 2025 & 2033

- Figure 59: Asia Pacific Medical Device Repair Service Revenue Share (%), by End User 2025 & 2033

- Figure 60: Asia Pacific Medical Device Repair Service Revenue (billion), by Country 2025 & 2033

- Figure 61: Asia Pacific Medical Device Repair Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Device Repair Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: Global Medical Device Repair Service Revenue billion Forecast, by Repair Type 2020 & 2033

- Table 3: Global Medical Device Repair Service Revenue billion Forecast, by Device Type 2020 & 2033

- Table 4: Global Medical Device Repair Service Revenue billion Forecast, by Service Provider 2020 & 2033

- Table 5: Global Medical Device Repair Service Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Medical Device Repair Service Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Global Medical Device Repair Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 8: Global Medical Device Repair Service Revenue billion Forecast, by Repair Type 2020 & 2033

- Table 9: Global Medical Device Repair Service Revenue billion Forecast, by Device Type 2020 & 2033

- Table 10: Global Medical Device Repair Service Revenue billion Forecast, by Service Provider 2020 & 2033

- Table 11: Global Medical Device Repair Service Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Medical Device Repair Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: United States Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Canada Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Mexico Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Device Repair Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 17: Global Medical Device Repair Service Revenue billion Forecast, by Repair Type 2020 & 2033

- Table 18: Global Medical Device Repair Service Revenue billion Forecast, by Device Type 2020 & 2033

- Table 19: Global Medical Device Repair Service Revenue billion Forecast, by Service Provider 2020 & 2033

- Table 20: Global Medical Device Repair Service Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Medical Device Repair Service Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Brazil Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Argentina Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Medical Device Repair Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 26: Global Medical Device Repair Service Revenue billion Forecast, by Repair Type 2020 & 2033

- Table 27: Global Medical Device Repair Service Revenue billion Forecast, by Device Type 2020 & 2033

- Table 28: Global Medical Device Repair Service Revenue billion Forecast, by Service Provider 2020 & 2033

- Table 29: Global Medical Device Repair Service Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Medical Device Repair Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: France Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Italy Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Spain Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Russia Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Benelux Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Nordics Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Global Medical Device Repair Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 41: Global Medical Device Repair Service Revenue billion Forecast, by Repair Type 2020 & 2033

- Table 42: Global Medical Device Repair Service Revenue billion Forecast, by Device Type 2020 & 2033

- Table 43: Global Medical Device Repair Service Revenue billion Forecast, by Service Provider 2020 & 2033

- Table 44: Global Medical Device Repair Service Revenue billion Forecast, by End User 2020 & 2033

- Table 45: Global Medical Device Repair Service Revenue billion Forecast, by Country 2020 & 2033

- Table 46: Turkey Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Israel Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: GCC Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: North Africa Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: South Africa Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Global Medical Device Repair Service Revenue billion Forecast, by Service Type 2020 & 2033

- Table 53: Global Medical Device Repair Service Revenue billion Forecast, by Repair Type 2020 & 2033

- Table 54: Global Medical Device Repair Service Revenue billion Forecast, by Device Type 2020 & 2033

- Table 55: Global Medical Device Repair Service Revenue billion Forecast, by Service Provider 2020 & 2033

- Table 56: Global Medical Device Repair Service Revenue billion Forecast, by End User 2020 & 2033

- Table 57: Global Medical Device Repair Service Revenue billion Forecast, by Country 2020 & 2033

- Table 58: China Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 59: India Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Japan Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 61: South Korea Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 63: Oceania Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Medical Device Repair Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Device Repair Service?

The projected CAGR is approximately 10.8%.

2. Which companies are prominent players in the Medical Device Repair Service?

Key companies in the market include Koninklijke Philips, GE Healthcare, Abbott Laboratories, Siemens, PrimedeQ,, Drägerwerk, Nordic Service Group, Gumbo Medical, Medical Equipment Repair Associates, Agiliti Health, ACF Medical, Crothall Healthcare, Eikon Medical Solutions, Healthcare 21, Others.

3. What are the main segments of the Medical Device Repair Service?

The market segments include Service Type, Repair Type, Device Type, Service Provider, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 60.68 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Device Repair Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Device Repair Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Device Repair Service?

To stay informed about further developments, trends, and reports in the Medical Device Repair Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence