Key Insights

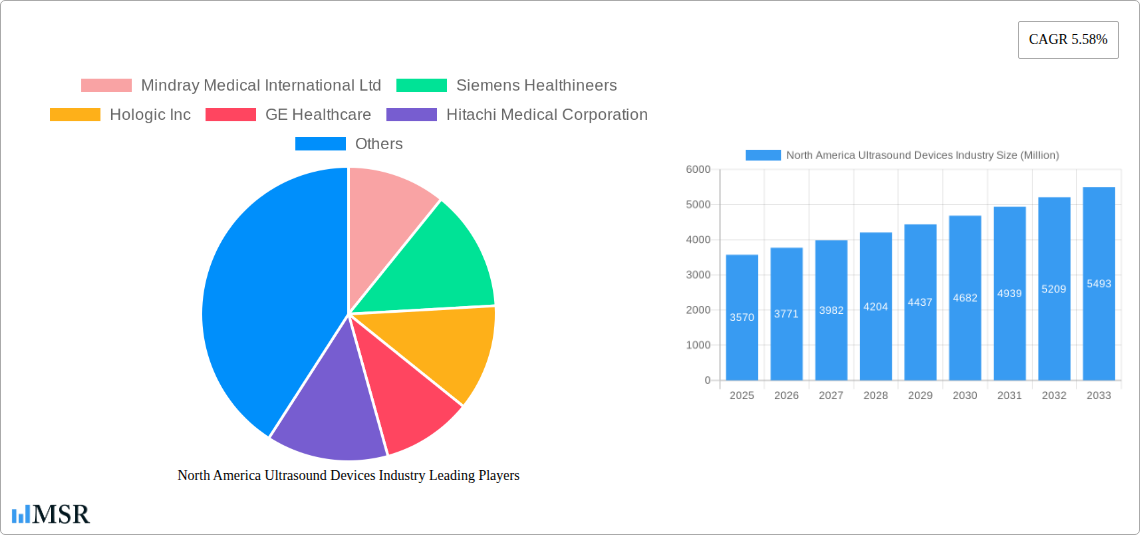

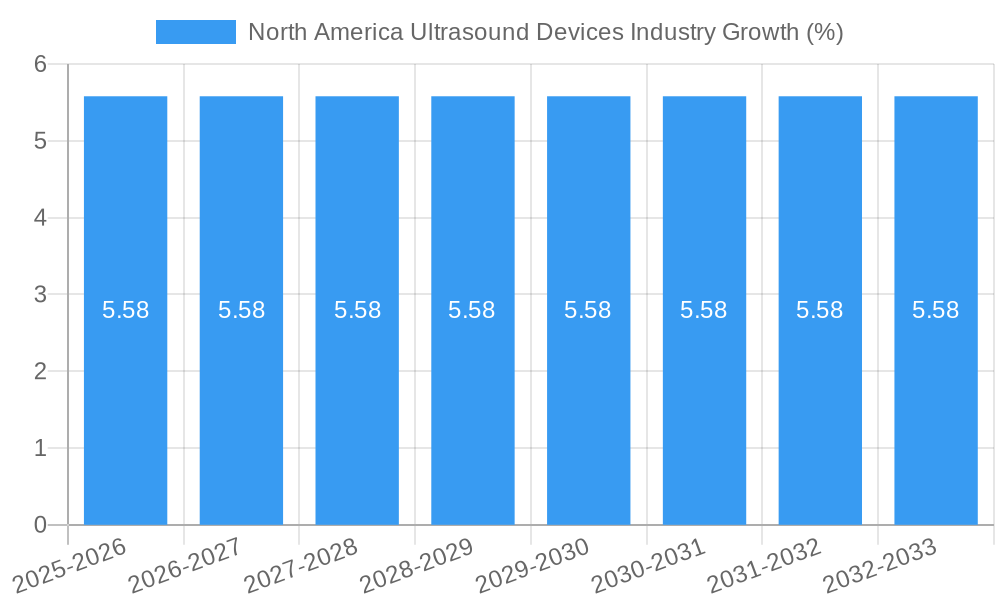

The North America Ultrasound Devices Industry is poised for significant expansion, projected to reach approximately USD 3.57 billion with a robust Compound Annual Growth Rate (CAGR) of 5.58% from 2025 to 2033. This growth trajectory is primarily propelled by advancements in imaging technologies, such as the increasing adoption of 3D and 4D ultrasound imaging, which offer enhanced diagnostic capabilities and patient comfort. The surge in demand for portable ultrasound devices, driven by their flexibility and accessibility in diverse clinical settings like critical care and remote patient monitoring, is another key accelerator. Furthermore, the expanding applications of ultrasound in specialties like cardiology, gynecology/obstetrics, and musculoskeletal imaging, coupled with an aging population and a rising prevalence of chronic diseases, are contributing to sustained market expansion. Key players like GE Healthcare, Siemens Healthineers, and Philips are actively investing in research and development to introduce innovative solutions, further stimulating market growth.

Despite the optimistic outlook, the market faces certain restraints that could temper its growth. Stringent regulatory approval processes for new ultrasound devices can lead to longer market entry times and increased development costs. Additionally, the high initial investment required for advanced ultrasound systems and the need for specialized training for healthcare professionals can pose barriers to adoption, particularly for smaller healthcare facilities. However, the ongoing digital transformation in healthcare, including the integration of AI and cloud-based solutions, is expected to mitigate some of these challenges by improving workflow efficiency and data accessibility. The North American market, encompassing the United States, Canada, and Mexico, is expected to witness steady growth, with the United States leading in terms of market share due to its advanced healthcare infrastructure and high per capita healthcare spending.

This comprehensive report delves into the dynamic North America Ultrasound Devices Industry, providing in-depth analysis, market projections, and strategic insights for stakeholders. Covering the period from 2019 to 2033, with a base year of 2025, this report leverages historical data and future forecasts to illuminate market concentration, innovation, and growth drivers. Discover the leading players, key market segments, technological advancements, and emerging opportunities shaping the future of ultrasound in North America.

North America Ultrasound Devices Industry Market Concentration & Dynamics

The North America Ultrasound Devices Industry is characterized by a moderate to high degree of market concentration, driven by the presence of established global players and significant R&D investments. The innovation ecosystem is robust, with companies continuously investing in developing advanced imaging technologies and AI-driven solutions to enhance diagnostic accuracy and patient outcomes. Regulatory frameworks, primarily governed by the FDA in the United States and Health Canada, play a crucial role in product approval and market access, influencing the pace of innovation and market entry. The availability of effective substitute products, while present in some diagnostic areas, is increasingly being offset by the superior real-time, non-invasive capabilities of ultrasound. End-user trends are shifting towards a greater demand for portable, point-of-care ultrasound (POCUS) devices, driven by the need for faster diagnoses in emergency settings and remote healthcare. Mergers and acquisitions (M&A) activities are a significant dynamic, with approximately 15-25 M&A deals anticipated within the forecast period, aimed at consolidating market share, acquiring novel technologies, and expanding product portfolios. Market share is distributed among key players, with GE Healthcare, Siemens Healthineers, and Koninklijke Philips NV holding substantial portions.

North America Ultrasound Devices Industry Industry Insights & Trends

The North America Ultrasound Devices Industry is poised for significant growth, projected to reach a market size of approximately $7,500 Million by 2033, with a Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period (2025–2033). This expansion is fueled by several key market growth drivers. The increasing prevalence of chronic diseases, such as cardiovascular diseases and cancer, is driving the demand for early and accurate diagnosis, for which ultrasound plays a pivotal role. Advances in medical imaging technology, including the development of high-resolution 2D, 3D, and 4D ultrasound, along with Doppler imaging, are enhancing diagnostic capabilities across various medical specialties. The growing adoption of portable and handheld ultrasound devices for point-of-care diagnostics in emergency departments, intensive care units, and remote healthcare settings is another major catalyst. Technological disruptions, such as the integration of artificial intelligence (AI) for image analysis and workflow optimization, are revolutionizing ultrasound imaging, improving efficiency and accuracy. Evolving consumer behaviors, including a preference for minimally invasive procedures and a focus on preventative healthcare, further bolster the demand for ultrasound technologies. The rising healthcare expenditure across North America, coupled with favorable reimbursement policies for diagnostic imaging procedures, also contributes to the market's upward trajectory. Furthermore, the increasing geriatric population, more susceptible to various medical conditions, is also a significant factor driving the demand for ultrasound devices. The growing emphasis on telemedicine and remote patient monitoring is also creating new avenues for ultrasound device utilization, particularly for specialized applications. The demand for advanced imaging techniques like elastography for tissue characterization is also on the rise, expanding the application scope of ultrasound.

Key Markets & Segments Leading North America Ultrasound Devices Industry

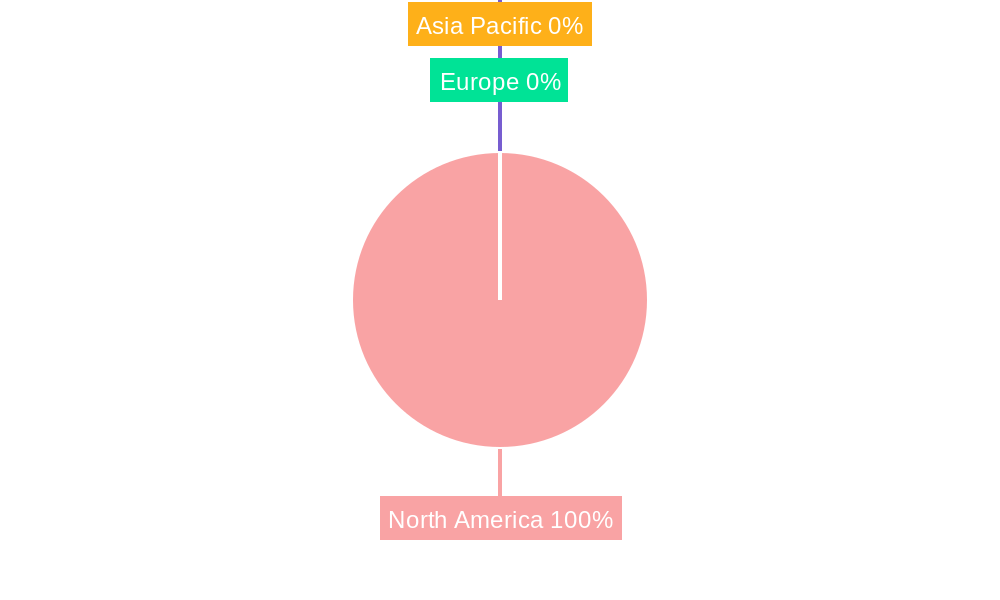

The United States dominates the North America Ultrasound Devices Industry, accounting for approximately 75% of the regional market share. This dominance is attributed to a robust healthcare infrastructure, high healthcare spending, advanced technological adoption, and a concentration of leading medical institutions and research centers. Canada and Mexico follow, with growing healthcare investments and increasing demand for advanced medical equipment.

Type:

- Stationary Ultrasound: Continues to be a significant segment, particularly in large hospital settings and specialized imaging centers, due to its advanced features and higher processing power. The demand for stationary units is driven by applications in radiology and cardiology requiring comprehensive diagnostic capabilities.

- Portable Ultrasound: This segment is experiencing the fastest growth, propelled by the increasing adoption of point-of-care ultrasound (POCUS) by clinicians in various settings, including emergency medicine, critical care, and anesthesia. The affordability, ease of use, and rapid diagnostic capabilities of portable devices are key drivers.

Technology:

- 2D Ultrasound Imaging: Remains the foundational technology, widely used across all applications due to its versatility and established diagnostic value.

- 3D and 4D Ultrasound Imaging: Witnessing substantial growth, especially in gynecology and obstetrics for fetal imaging, as well as in cardiology for detailed cardiac visualization. The ability to provide volumetric and real-time dynamic imaging enhances diagnostic precision.

- Doppler Imaging: Crucial for assessing blood flow, this technology is essential in cardiology, vascular studies, and critical care, driving its consistent demand.

- High-intensity Focused Ultrasound (HIFU): An emerging technology with significant growth potential, particularly in non-invasive treatment applications like fibroid ablation and tumor therapy.

Application:

- Radiology: This is the largest application segment, driven by the broad use of ultrasound for abdominal, breast, and musculoskeletal imaging, as well as interventional procedures.

- Cardiology: A key growth area, with increasing demand for advanced cardiac imaging to diagnose and manage heart conditions.

- Gynecology/Obstetrics: A consistently strong segment, driven by routine prenatal care and the diagnosis of gynecological disorders.

- Critical Care & Anesthesiology: These segments are experiencing rapid expansion due to the growing adoption of POCUS for bedside diagnostics, procedural guidance, and patient monitoring.

North America Ultrasound Devices Industry Product Developments

The North America Ultrasound Devices Industry is continuously driven by product innovations focused on enhancing diagnostic accuracy, portability, and workflow efficiency. Key developments include the integration of artificial intelligence (AI) for automated image analysis, lesion detection, and quantitative measurements, as well as the miniaturization of devices, leading to more advanced handheld and portable ultrasound systems. Vendors are also focusing on developing vendor-neutral solutions and cloud-based platforms for seamless data management and remote access, improving collaboration and accessibility of ultrasound imaging.

Challenges in the North America Ultrasound Devices Industry Market

Despite strong growth prospects, the North America Ultrasound Devices Industry faces several challenges. High initial costs of advanced ultrasound systems can be a barrier for smaller clinics and healthcare providers. Stringent regulatory approval processes, while ensuring safety and efficacy, can delay market entry for new products. Intense competition among established players and the emergence of new entrants can lead to price pressures. Furthermore, a shortage of trained ultrasound technicians and the need for continuous professional development to keep pace with technological advancements pose a challenge to widespread adoption and optimal utilization of these devices.

Forces Driving North America Ultrasound Devices Industry Growth

Several forces are propelling the growth of the North America Ultrasound Devices Industry. Technological advancements, such as the development of artificial intelligence-powered imaging, miniaturization for portability, and enhanced resolution, are key drivers. The increasing global burden of chronic diseases, including cardiovascular conditions and cancer, necessitates early and accurate diagnostic tools like ultrasound. The rising healthcare expenditure across the region, coupled with favorable reimbursement policies for diagnostic imaging, further supports market expansion. The growing demand for minimally invasive diagnostic and therapeutic procedures, where ultrasound plays a crucial role in guidance and visualization, is another significant growth catalyst.

Challenges in the North America Ultrasound Devices Industry Market

Long-term growth catalysts for the North America Ultrasound Devices Industry lie in continuous innovation and market expansion. The development of next-generation ultrasound technologies, such as advanced elastography, contrast-enhanced ultrasound, and interventional ultrasound, will unlock new clinical applications and treatment possibilities. Strategic partnerships between ultrasound device manufacturers and AI developers will accelerate the integration of smart diagnostic tools. Expanding the reach of POCUS into primary care settings and developing countries, alongside robust training programs, will broaden the market base. Furthermore, the increasing focus on value-based healthcare and the demonstration of ultrasound's cost-effectiveness in improving patient outcomes will be crucial for sustained long-term growth.

Emerging Opportunities in North America Ultrasound Devices Industry

Emerging opportunities in the North America Ultrasound Devices Industry are diverse and promising. The expansion of AI-powered diagnostic tools, offering automated analysis and decision support, presents a significant avenue for growth. The increasing adoption of point-of-care ultrasound (POCUS) in non-traditional settings, such as urgent care centers, athletic training facilities, and even in-home patient monitoring, opens new market segments. The development of specialized ultrasound probes for niche applications, like intracardiac echocardiography or intraoperative imaging, will cater to specific clinical needs. Furthermore, the growing interest in therapeutic ultrasound applications, such as non-invasive tumor ablation and drug delivery, represents a transformative opportunity for the industry. The demand for remote monitoring solutions integrated with portable ultrasound devices also presents a substantial growth area.

Leading Players in the North America Ultrasound Devices Industry Sector

- Mindray Medical International Ltd

- Siemens Healthineers

- Hologic Inc

- GE Healthcare

- Hitachi Medical Corporation

- Koninklijke Philips NV

- Canon Medical Systems Corporation

- Fujifilm Holdings Corporation

Key Milestones in North America Ultrasound Devices Industry Industry

- March 2022: Royal Philips launched the Ultrasound Workspace at the American College of Cardiology's Annual Scientific Session and Expo (ACC 2022). Philips Ultrasound Workspace is an industry-leading, vendor-neutral echocardiography image analysis and reporting solution that can be accessed remotely via a browser.

- January 2022: Clarius Mobile Health launched a third-generation product line of high-performance handheld wireless ultrasound scanners for all medical specialists.

Strategic Outlook for North America Ultrasound Devices Industry Market

The strategic outlook for the North America Ultrasound Devices Industry is exceptionally positive, driven by continuous innovation and expanding applications. The focus will remain on developing more intelligent, intuitive, and portable ultrasound systems that integrate AI for enhanced diagnostic accuracy and workflow efficiency. Strategic acquisitions and partnerships will continue to play a vital role in consolidating market positions and accessing new technologies. The increasing demand for value-based healthcare will push manufacturers to demonstrate the cost-effectiveness and clinical utility of their devices. Furthermore, the expansion of therapeutic ultrasound applications and the integration of ultrasound into telemedicine platforms will shape the future landscape, offering significant growth accelerators and market potential.

North America Ultrasound Devices Industry Segmentation

-

1. Type

- 1.1. Stationary Ultrasound

- 1.2. Portable Ultrasound

-

2. Technology

- 2.1. 2D Ultrasound Imaging

- 2.2. 3D and 4D Ultrasound Imaging

- 2.3. Doppler Imaging

- 2.4. High-intensity Focused Ultrasound

-

3. Application

- 3.1. Anesthesiology

- 3.2. Cardiology

- 3.3. Gynecology/Obstetrics

- 3.4. Musculoskeletal

- 3.5. Radiology

- 3.6. Critical Care

- 3.7. Other Applications

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Mexico

North America Ultrasound Devices Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Ultrasound Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.58% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Adoption of Diagnostic Imaging; Increasing Prevalence of Chronic Diseases; Rapid Technological Advancements

- 3.3. Market Restrains

- 3.3.1. Stringent Regulatory Reforms

- 3.4. Market Trends

- 3.4.1. Portable Ultrasound Segment is Expected to Witness a Healthy Growth Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Stationary Ultrasound

- 5.1.2. Portable Ultrasound

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. 2D Ultrasound Imaging

- 5.2.2. 3D and 4D Ultrasound Imaging

- 5.2.3. Doppler Imaging

- 5.2.4. High-intensity Focused Ultrasound

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Anesthesiology

- 5.3.2. Cardiology

- 5.3.3. Gynecology/Obstetrics

- 5.3.4. Musculoskeletal

- 5.3.5. Radiology

- 5.3.6. Critical Care

- 5.3.7. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Stationary Ultrasound

- 6.1.2. Portable Ultrasound

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. 2D Ultrasound Imaging

- 6.2.2. 3D and 4D Ultrasound Imaging

- 6.2.3. Doppler Imaging

- 6.2.4. High-intensity Focused Ultrasound

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Anesthesiology

- 6.3.2. Cardiology

- 6.3.3. Gynecology/Obstetrics

- 6.3.4. Musculoskeletal

- 6.3.5. Radiology

- 6.3.6. Critical Care

- 6.3.7. Other Applications

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Canada North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Stationary Ultrasound

- 7.1.2. Portable Ultrasound

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. 2D Ultrasound Imaging

- 7.2.2. 3D and 4D Ultrasound Imaging

- 7.2.3. Doppler Imaging

- 7.2.4. High-intensity Focused Ultrasound

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Anesthesiology

- 7.3.2. Cardiology

- 7.3.3. Gynecology/Obstetrics

- 7.3.4. Musculoskeletal

- 7.3.5. Radiology

- 7.3.6. Critical Care

- 7.3.7. Other Applications

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Mexico North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Stationary Ultrasound

- 8.1.2. Portable Ultrasound

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. 2D Ultrasound Imaging

- 8.2.2. 3D and 4D Ultrasound Imaging

- 8.2.3. Doppler Imaging

- 8.2.4. High-intensity Focused Ultrasound

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Anesthesiology

- 8.3.2. Cardiology

- 8.3.3. Gynecology/Obstetrics

- 8.3.4. Musculoskeletal

- 8.3.5. Radiology

- 8.3.6. Critical Care

- 8.3.7. Other Applications

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. United States North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Ultrasound Devices Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Mindray Medical International Ltd

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Siemens Healthineers

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Hologic Inc

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 GE Healthcare

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Hitachi Medical Corporation

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Koninklijke Philips NV

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Canon Medical Systems Corporation

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Fujifilm Holdings Corporation

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.1 Mindray Medical International Ltd

List of Figures

- Figure 1: North America Ultrasound Devices Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Ultrasound Devices Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Ultrasound Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Ultrasound Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: North America Ultrasound Devices Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: North America Ultrasound Devices Industry Volume K Unit Forecast, by Type 2019 & 2032

- Table 5: North America Ultrasound Devices Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 6: North America Ultrasound Devices Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 7: North America Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 8: North America Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 9: North America Ultrasound Devices Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 10: North America Ultrasound Devices Industry Volume K Unit Forecast, by Geography 2019 & 2032

- Table 11: North America Ultrasound Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 12: North America Ultrasound Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 13: North America Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: North America Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 15: United States North America Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: United States North America Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: Canada North America Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Canada North America Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: Mexico North America Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Mexico North America Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Rest of North America North America Ultrasound Devices Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Rest of North America North America Ultrasound Devices Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: North America Ultrasound Devices Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 24: North America Ultrasound Devices Industry Volume K Unit Forecast, by Type 2019 & 2032

- Table 25: North America Ultrasound Devices Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 26: North America Ultrasound Devices Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 27: North America Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 28: North America Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 29: North America Ultrasound Devices Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 30: North America Ultrasound Devices Industry Volume K Unit Forecast, by Geography 2019 & 2032

- Table 31: North America Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 32: North America Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 33: North America Ultrasound Devices Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 34: North America Ultrasound Devices Industry Volume K Unit Forecast, by Type 2019 & 2032

- Table 35: North America Ultrasound Devices Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 36: North America Ultrasound Devices Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 37: North America Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 38: North America Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 39: North America Ultrasound Devices Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 40: North America Ultrasound Devices Industry Volume K Unit Forecast, by Geography 2019 & 2032

- Table 41: North America Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: North America Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 43: North America Ultrasound Devices Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 44: North America Ultrasound Devices Industry Volume K Unit Forecast, by Type 2019 & 2032

- Table 45: North America Ultrasound Devices Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 46: North America Ultrasound Devices Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 47: North America Ultrasound Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 48: North America Ultrasound Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 49: North America Ultrasound Devices Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 50: North America Ultrasound Devices Industry Volume K Unit Forecast, by Geography 2019 & 2032

- Table 51: North America Ultrasound Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 52: North America Ultrasound Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Ultrasound Devices Industry?

The projected CAGR is approximately 5.58%.

2. Which companies are prominent players in the North America Ultrasound Devices Industry?

Key companies in the market include Mindray Medical International Ltd, Siemens Healthineers, Hologic Inc, GE Healthcare, Hitachi Medical Corporation, Koninklijke Philips NV, Canon Medical Systems Corporation, Fujifilm Holdings Corporation.

3. What are the main segments of the North America Ultrasound Devices Industry?

The market segments include Type, Technology, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.57 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Adoption of Diagnostic Imaging; Increasing Prevalence of Chronic Diseases; Rapid Technological Advancements.

6. What are the notable trends driving market growth?

Portable Ultrasound Segment is Expected to Witness a Healthy Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Regulatory Reforms.

8. Can you provide examples of recent developments in the market?

March 2022: Royal Philips launched the Ultrasound Workspace at the American College of Cardiology's Annual Scientific Session and Expo (ACC 2022). Philips Ultrasound Workspace is an industry-leading, vendor-neutral echocardiography image analysis and reporting solution that can be accessed remotely via a browser.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Ultrasound Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Ultrasound Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Ultrasound Devices Industry?

To stay informed about further developments, trends, and reports in the North America Ultrasound Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence