Key Insights

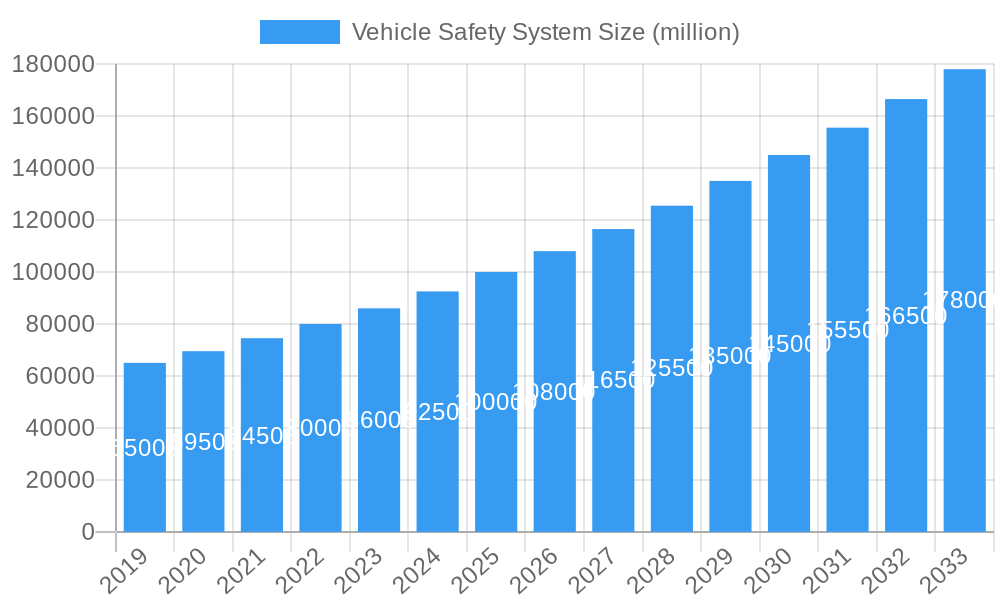

The global vehicle safety system market is poised for substantial growth, projected to reach an estimated market size of $100 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 8.5% through 2033. This expansion is primarily fueled by an increasing global focus on road safety regulations, the growing adoption of advanced driver-assistance systems (ADAS) in both passenger and commercial vehicles, and the escalating consumer demand for enhanced protection. Technological advancements, particularly in areas like artificial intelligence, sensor fusion, and connectivity, are continuously driving innovation in both active safety systems (e.g., automatic emergency braking, lane keeping assist) and passive safety systems (e.g., airbags, seatbelt pre-tensioners). The rising average selling price of vehicles equipped with these sophisticated safety features further contributes to the market's value growth. The sheer volume of vehicles produced globally, coupled with a proactive approach by automotive manufacturers to integrate cutting-edge safety technologies to meet stringent safety standards and consumer expectations, underscores the strong upward trajectory of this market.

Vehicle Safety System Market Size (In Billion)

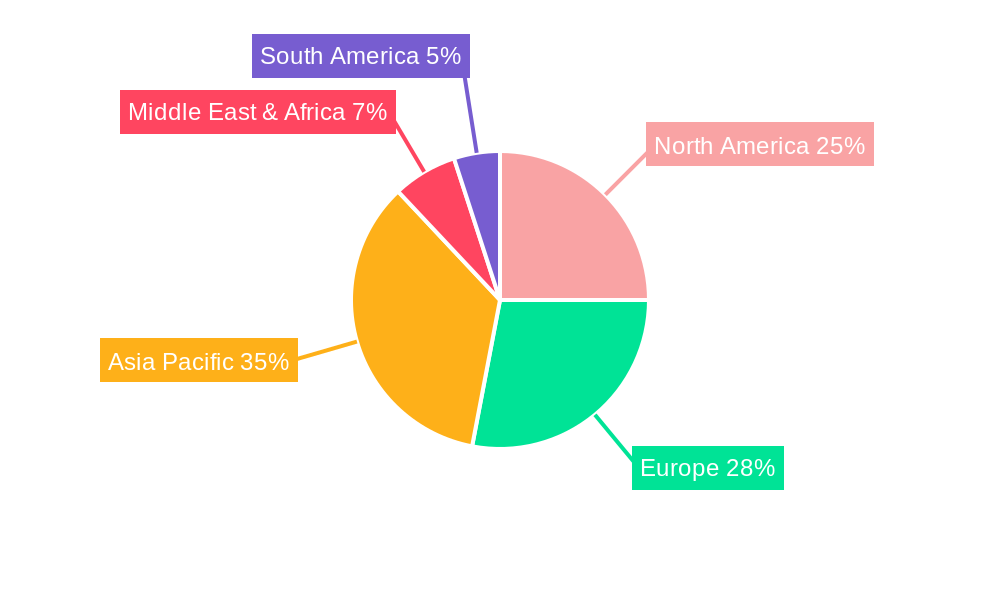

The market's expansion is further bolstered by evolving consumer perceptions, where vehicle safety is increasingly becoming a key purchasing criterion. The proactive implementation of stricter safety mandates by governmental bodies worldwide is a significant accelerator, pushing manufacturers to invest heavily in research and development of advanced safety solutions. While the market exhibits strong growth potential, certain restraints may influence its pace. These include the high cost of advanced safety system integration, potential consumer resistance to complex systems, and the ongoing challenge of ensuring robust cybersecurity for connected safety features. However, these challenges are being addressed through ongoing technological advancements and economies of scale in production. Geographically, the Asia Pacific region, particularly China and India, is emerging as a dominant force due to its massive automotive production and burgeoning demand for safer vehicles. North America and Europe remain mature yet significant markets, driven by stringent regulations and a high level of consumer awareness regarding vehicle safety. The market is segmented into applications such as passenger vehicles and commercial vehicles, with further division into active and passive safety systems, each experiencing distinct growth patterns driven by specific technological advancements and regulatory pressures.

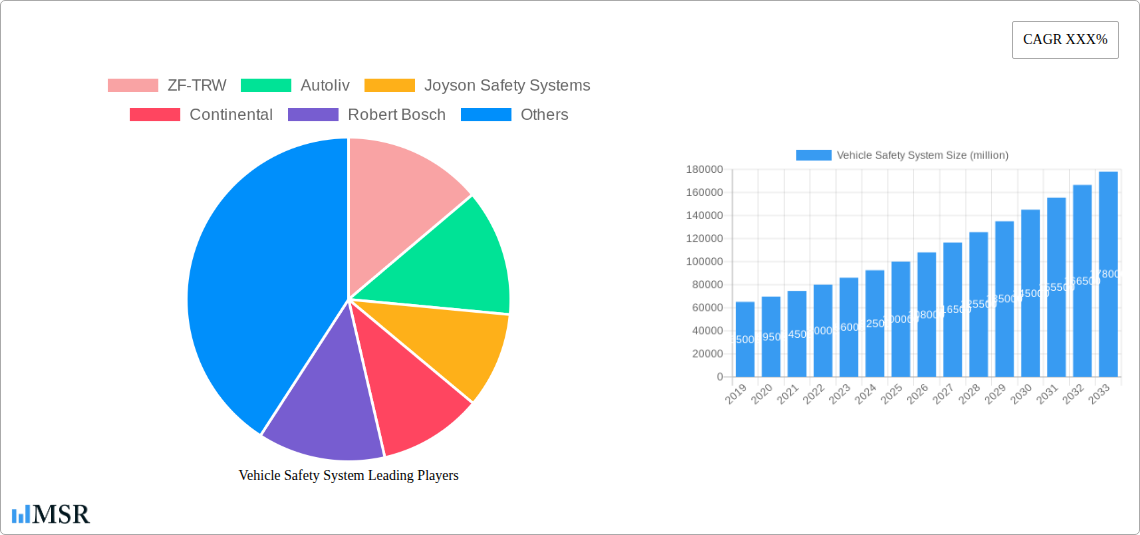

Vehicle Safety System Company Market Share

Here is an SEO-optimized, engaging report description for Vehicle Safety Systems, incorporating your specified keywords, timelines, headings, and structural requirements.

Report Title: Global Vehicle Safety System Market Analysis: Growth, Trends, and Opportunities (2019-2033)

Report Description:

Dive deep into the dynamic vehicle safety system market with this comprehensive analysis. Covering the study period 2019–2033, this report provides unparalleled insights into the evolving landscape of automotive safety technologies. The base year 2025 and forecast period 2025–2033 offer precise projections for this multi-million dollar industry. Explore the intricate interplay of active safety systems and passive safety systems, examining their adoption across passenger vehicles and commercial vehicles. Uncover the strategies of industry giants like ZF-TRW, Autoliv, Joyson Safety Systems, Continental, Robert Bosch, Denso, Toyota Gosei, Mobileye, Nihon Plast, Jinheng Automotive Safety System, Hyundai Mobis, Aisin, Tokai Rika, Ashimori Industry, MANDO, and others. This report is essential for stakeholders seeking to understand market concentration, key growth drivers, emerging opportunities, and the competitive strategies shaping the future of automotive safety.

Vehicle Safety System Market Concentration & Dynamics

The global vehicle safety system market exhibits a moderate to high concentration, with key players like ZF-TRW, Autoliv, and Continental dominating significant market shares. The innovation ecosystem is rapidly evolving, driven by advancements in AI, sensor technology, and connectivity. Regulatory frameworks are becoming increasingly stringent worldwide, mandating the adoption of advanced safety features, thereby pushing innovation and market growth. Substitute products, while existing, often fall short of the integrated safety solutions offered by dedicated vehicle safety system providers. End-user trends clearly favor enhanced safety, with consumers increasingly prioritizing vehicles equipped with sophisticated protection technologies. Mergers and acquisitions (M&A) activities remain a significant driver of consolidation and strategic realignment within the industry. For instance, the last five years (2019-2024) have witnessed approximately 25 significant M&A deals, with an estimated cumulative value of over $15,000 million, aimed at expanding product portfolios and market reach. The market size in 2025 is projected to exceed $65,000 million, with a significant portion of this revenue derived from the integration of these advanced safety solutions.

Vehicle Safety System Industry Insights & Trends

The vehicle safety system market is poised for substantial growth, driven by a confluence of technological advancements, evolving regulatory landscapes, and increasing consumer demand for secure mobility. The market size in the base year 2025 is estimated at $65,000 million, with a projected Compound Annual Growth Rate (CAGR) of 8.5% during the forecast period 2025–2033. This robust growth is fueled by the escalating adoption of active safety systems, which proactively work to prevent accidents. Technologies such as Automatic Emergency Braking (AEB), Lane Keeping Assist (LKA), Blind Spot Detection (BSD), and Adaptive Cruise Control (ACC) are becoming standard features in new vehicle models. The increasing complexity of vehicles, coupled with the rise of autonomous driving functionalities, necessitates more sophisticated integrated safety solutions. Furthermore, passive safety systems, including advanced airbag technologies and high-strength body structures, continue to be critical for occupant protection during unavoidable collisions. The historical period (2019-2024) saw consistent market expansion, with the market size growing from approximately $40,000 million in 2019 to an estimated $60,000 million by the end of 2024, reflecting a CAGR of 8.1% over this period. Evolving consumer behaviors also play a crucial role; as accident statistics are more widely disseminated and safety ratings become a key purchasing factor, consumers are actively seeking vehicles with superior safety performance. This heightened awareness, coupled with increasing disposable incomes in emerging economies, creates a fertile ground for market expansion. The integration of AI and machine learning in vehicle safety systems is a key trend, enabling predictive safety capabilities and personalized safety responses. For example, systems can now learn driver behavior to better anticipate potential hazards. The total market value in the forecast year 2033 is expected to surpass $120,000 million.

Key Markets & Segments Leading Vehicle Safety System

The passenger vehicle segment overwhelmingly leads the vehicle safety system market, accounting for an estimated 80% of the total market value in 2025. This dominance is driven by several factors, including the sheer volume of passenger car production globally and the increasing consumer preference for advanced safety features in personal transportation. The demand for active safety systems within the passenger vehicle segment is particularly strong, projected to reach over $55,000 million by 2025.

- Drivers for Passenger Vehicle Dominance:

- Consumer Demand: Safety is a primary purchasing criterion for individuals and families.

- Regulatory Mandates: Governments worldwide are increasingly mandating advanced safety features in passenger cars.

- Technological Integration: The rapid evolution of ADAS (Advanced Driver-Assistance Systems) is seamlessly integrated into passenger vehicle platforms.

- Brand Image & Differentiation: Automakers leverage advanced safety features to enhance brand perception and differentiate their offerings.

The active safety system segment is the fastest-growing category, projected to achieve a CAGR of 9.2% from 2025 to 2033, surpassing $95,000 million by 2033. This growth is attributed to the inherent ability of active systems to prevent accidents altogether, aligning with the zero-fatality vision in transportation. Regions such as North America and Europe are frontrunners in the adoption of active safety systems due to mature automotive markets and stringent safety regulations. For instance, the market size in North America for active safety systems is expected to reach approximately $22,000 million in 2025, driven by high vehicle penetration and strong consumer awareness.

Conversely, the commercial vehicle segment, while smaller in market share (estimated at 20% in 2025), presents significant growth opportunities, particularly for passive safety systems and specialized active safety solutions.

- Drivers for Commercial Vehicle Growth:

- Fleet Safety Initiatives: Companies are investing in safety to reduce operational costs associated with accidents and improve driver well-being.

- Regulatory Compliance: Increasingly strict regulations for commercial vehicle safety are being implemented globally.

- Technological Advancements: The development of robust and durable safety systems suitable for heavy-duty applications is expanding the market.

The market for commercial vehicle safety systems is expected to grow at a CAGR of 7.0% during the forecast period, reaching an estimated $25,000 million by 2033. The Asia-Pacific region, with its rapidly expanding logistics and transportation sectors, is a key growth market for commercial vehicle safety systems.

Vehicle Safety System Product Developments

Product innovation in vehicle safety systems is characterized by the integration of sophisticated sensors, AI-powered algorithms, and advanced connectivity. ZF-TRW is leading in advanced braking and steering systems, while Autoliv is at the forefront of airbag and seatbelt technologies. Mobileye's advanced driver-assistance systems (ADAS) and vision-based technologies are transforming perception and decision-making capabilities within vehicles. Continental is developing comprehensive integrated safety solutions, encompassing everything from sensors to electronic control units. Robert Bosch is a key player in radar, camera, and sensor technology, crucial for the functioning of many active safety systems. The trend is towards creating intelligent, interconnected systems that can communicate with each other and with the vehicle's infrastructure, enhancing overall safety performance and paving the way for higher levels of autonomous driving. These developments aim to reduce accident severity and frequency, thereby saving millions of lives annually.

Challenges in the Vehicle Safety System Market

The vehicle safety system market faces several significant challenges that could impede growth and adoption.

- High Cost of Integration: Advanced safety systems, particularly those involving complex sensor arrays and processing power, can significantly increase vehicle manufacturing costs, potentially impacting affordability for a broader consumer base.

- Regulatory Harmonization: While regulations are a driver, differing standards across various global markets can complicate development and deployment for manufacturers.

- Supply Chain Disruptions: The reliance on specialized components, such as semiconductor chips, makes the industry vulnerable to global supply chain disruptions, as seen in recent years, leading to production delays and increased costs. The estimated cost impact of a major chip shortage on the industry in 2022 was over $20,000 million.

- Consumer Education and Trust: For some advanced safety features, particularly those related to automation, building consumer trust and ensuring proper understanding of their capabilities and limitations is an ongoing challenge.

Forces Driving Vehicle Safety System Growth

The growth of the vehicle safety system market is propelled by a multifaceted set of drivers.

- Increasing Road Fatalities and Injuries: A persistent global concern, the drive to reduce the unacceptably high number of road casualties is a primary motivator for enhanced safety.

- Stringent Government Regulations and Safety Standards: Mandates for features like AEB and ESC in many regions compel automakers to integrate these technologies, directly boosting market demand.

- Advancements in Sensor and AI Technology: Innovations in radar, lidar, cameras, and AI algorithms enable more sophisticated and effective safety systems.

- Growing Consumer Awareness and Demand for Safety: As consumers become more informed about safety ratings and accident prevention technologies, their purchase decisions are increasingly influenced by these factors.

- Rise of Autonomous Driving: The development of autonomous vehicles inherently requires highly advanced and redundant safety systems.

Challenges in the Vehicle Safety System Market

The vehicle safety system market faces long-term growth catalysts that will shape its trajectory.

- Integration of AI and Machine Learning: The continued evolution of AI will lead to more predictive and adaptive safety systems that can learn from real-world scenarios and anticipate potential dangers with greater accuracy.

- Vehicle-to-Everything (V2X) Communication: The widespread adoption of V2X technology will enable vehicles to communicate with each other, infrastructure, and pedestrians, creating a more interconnected and safer transportation ecosystem.

- Expansion into Emerging Markets: As automotive markets mature in developing economies, the demand for advanced safety features will grow significantly, presenting substantial expansion opportunities.

- Development of Next-Generation Passive Safety: Ongoing research into novel materials and intelligent restraint systems will continue to improve occupant protection in the event of a collision.

Emerging Opportunities in Vehicle Safety System

Emerging opportunities within the vehicle safety system market are diverse and promising.

- Cybersecurity for Connected Safety Systems: As vehicles become more connected, ensuring the security of safety-critical systems against cyber threats presents a significant new market and development area.

- Personalized Safety Profiles: Leveraging AI to create individualized safety settings based on driver behavior, passenger profiles, and driving conditions offers a unique value proposition.

- Safety Solutions for Micromobility: The growing prevalence of e-scooters and other personal mobility devices creates a need for compact and integrated safety systems.

- Data Analytics for Predictive Maintenance: Utilizing safety system data to predict potential component failures before they occur can improve reliability and reduce unexpected downtime, a growing concern in fleet management.

Leading Players in the Vehicle Safety System Sector

- ZF-TRW

- Autoliv

- Joyson Safety Systems

- Continental

- Robert Bosch

- Denso

- Toyota Gosei

- Mobileye

- Nihon Plast

- Jinheng Automotive Safety System

- Hyundai Mobis

- Aisin

- Tokai Rika

- Ashimori Industry

- MANDO

Key Milestones in Vehicle Safety System Industry

- 2019: Launch of advanced driver-assistance systems (ADAS) with enhanced object recognition capabilities.

- 2020: Increased regulatory mandates for Automatic Emergency Braking (AEB) in major automotive markets.

- 2021: Significant advancements in AI-powered predictive safety algorithms by key players like Mobileye.

- 2022: Growing industry focus on cybersecurity for connected vehicle safety systems.

- 2023: Major acquisitions and partnerships aimed at consolidating the active and passive safety system segments.

- 2024 (Est.): Expected wider adoption of Level 2+ autonomous driving features incorporating advanced safety redundancies.

Strategic Outlook for Vehicle Safety System Market

The strategic outlook for the vehicle safety system market is exceptionally positive, driven by an unyielding commitment to reducing road fatalities and the relentless pace of technological innovation. Growth accelerators include the continued push for higher levels of vehicle autonomy, which necessitates more sophisticated and integrated safety solutions. Strategic opportunities lie in the global expansion of these technologies into emerging automotive markets and the development of cybersecurity measures for an increasingly connected vehicle fleet. Partnerships between automakers, technology providers, and regulatory bodies will be crucial for fostering a safe and sustainable future of mobility. The market is projected to witness sustained growth in both the active and passive safety system segments, with a significant focus on smart, predictive, and interconnected safety solutions, ensuring a multi-million dollar expansion for years to come.

Vehicle Safety System Segmentation

-

1. Application

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Type

- 2.1. Active Safety System

- 2.2. Passive Safety System

Vehicle Safety System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Vehicle Safety System Regional Market Share

Geographic Coverage of Vehicle Safety System

Vehicle Safety System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Active Safety System

- 5.2.2. Passive Safety System

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Vehicle Safety System Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Active Safety System

- 6.2.2. Passive Safety System

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Vehicle Safety System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Active Safety System

- 7.2.2. Passive Safety System

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Vehicle Safety System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Active Safety System

- 8.2.2. Passive Safety System

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Vehicle Safety System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Active Safety System

- 9.2.2. Passive Safety System

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Vehicle Safety System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Active Safety System

- 10.2.2. Passive Safety System

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Vehicle Safety System Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Vehicle

- 11.1.2. Commercial Vehicle

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Active Safety System

- 11.2.2. Passive Safety System

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ZF-TRW

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Autoliv

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Joyson Safety Systems

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Continental

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Robert Bosch

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Denso

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Toyota Gosei

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mobileye

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nihon Plast

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Jinheng Automotive Safety System

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Hyundai Mobis

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Aisin

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Tokai Rika

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Ashimori Industry

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 MANDO

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 ZF-TRW

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Vehicle Safety System Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Vehicle Safety System Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Vehicle Safety System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Vehicle Safety System Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Vehicle Safety System Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Vehicle Safety System Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Vehicle Safety System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Vehicle Safety System Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Vehicle Safety System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Vehicle Safety System Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Vehicle Safety System Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Vehicle Safety System Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Vehicle Safety System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Vehicle Safety System Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Vehicle Safety System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Vehicle Safety System Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Vehicle Safety System Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Vehicle Safety System Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Vehicle Safety System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Vehicle Safety System Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Vehicle Safety System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Vehicle Safety System Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Vehicle Safety System Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Vehicle Safety System Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Vehicle Safety System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Vehicle Safety System Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Vehicle Safety System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Vehicle Safety System Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Vehicle Safety System Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Vehicle Safety System Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Vehicle Safety System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Vehicle Safety System Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Vehicle Safety System Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Vehicle Safety System Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Vehicle Safety System Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Vehicle Safety System Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Vehicle Safety System Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Vehicle Safety System Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Vehicle Safety System Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Vehicle Safety System Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Vehicle Safety System Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Vehicle Safety System Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Vehicle Safety System Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Vehicle Safety System Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Vehicle Safety System Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Vehicle Safety System Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Vehicle Safety System Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Vehicle Safety System Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Vehicle Safety System Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Vehicle Safety System Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vehicle Safety System?

The projected CAGR is approximately 13.4%.

2. Which companies are prominent players in the Vehicle Safety System?

Key companies in the market include ZF-TRW, Autoliv, Joyson Safety Systems, Continental, Robert Bosch, Denso, Toyota Gosei, Mobileye, Nihon Plast, Jinheng Automotive Safety System, Hyundai Mobis, Aisin, Tokai Rika, Ashimori Industry, MANDO.

3. What are the main segments of the Vehicle Safety System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vehicle Safety System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vehicle Safety System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vehicle Safety System?

To stay informed about further developments, trends, and reports in the Vehicle Safety System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence