Key Insights

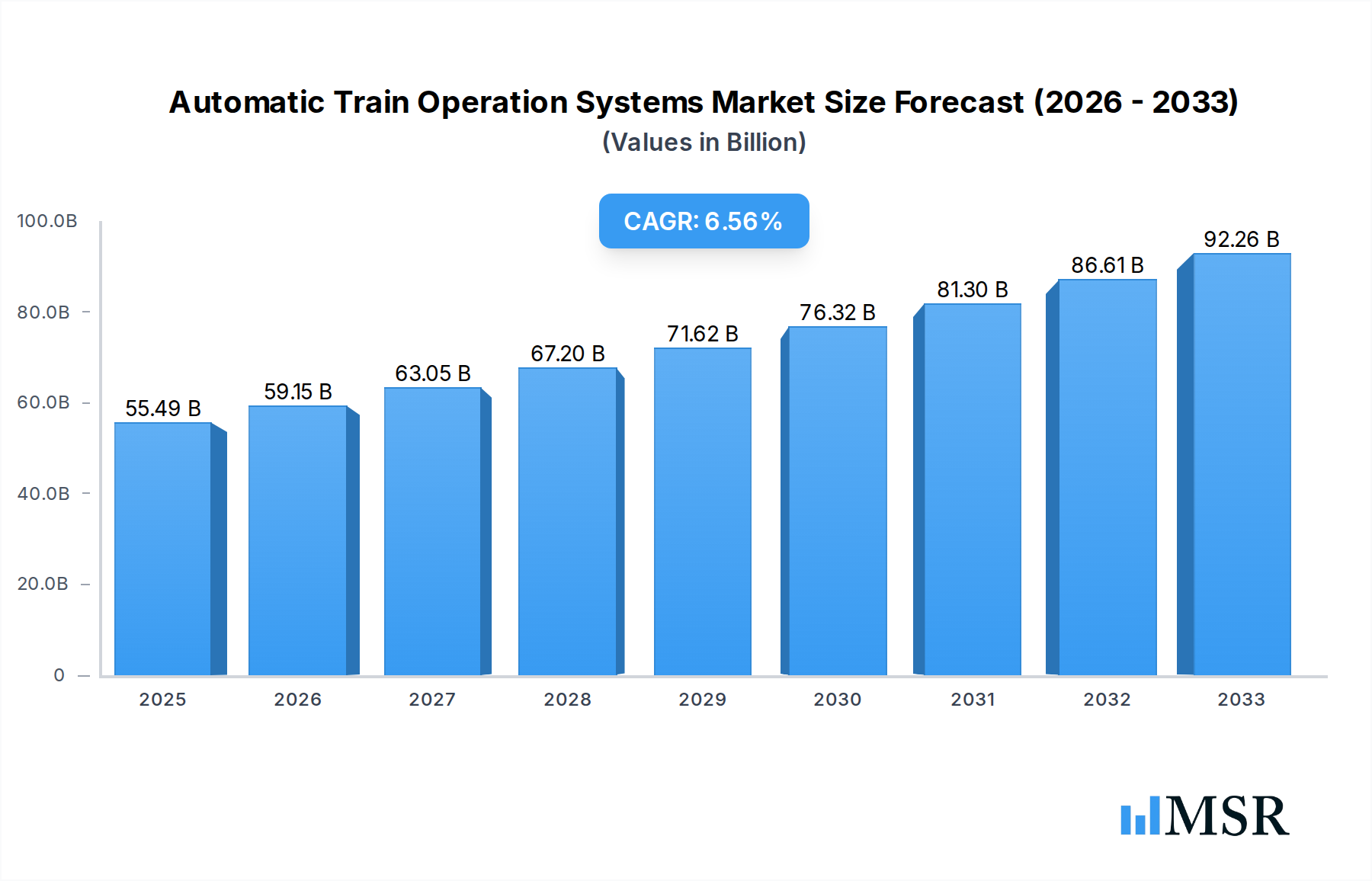

The global Automatic Train Operation (ATO) systems market is poised for significant expansion, driven by the increasing demand for enhanced safety, efficiency, and passenger capacity in rail networks worldwide. Projections indicate a robust market size of USD 55,493.2 million in 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period of 2025-2033. This growth trajectory is fueled by substantial investments in upgrading existing rail infrastructure and the development of new, high-speed, and urban rail lines. Key drivers include the need to optimize train scheduling, reduce operational costs, and minimize human error, thereby improving overall rail service reliability. The integration of advanced technologies like artificial intelligence, IoT, and sophisticated sensor networks is further accelerating the adoption of ATO systems, enabling real-time monitoring, predictive maintenance, and seamless train control.

Automatic Train Operation Systems Market Size (In Billion)

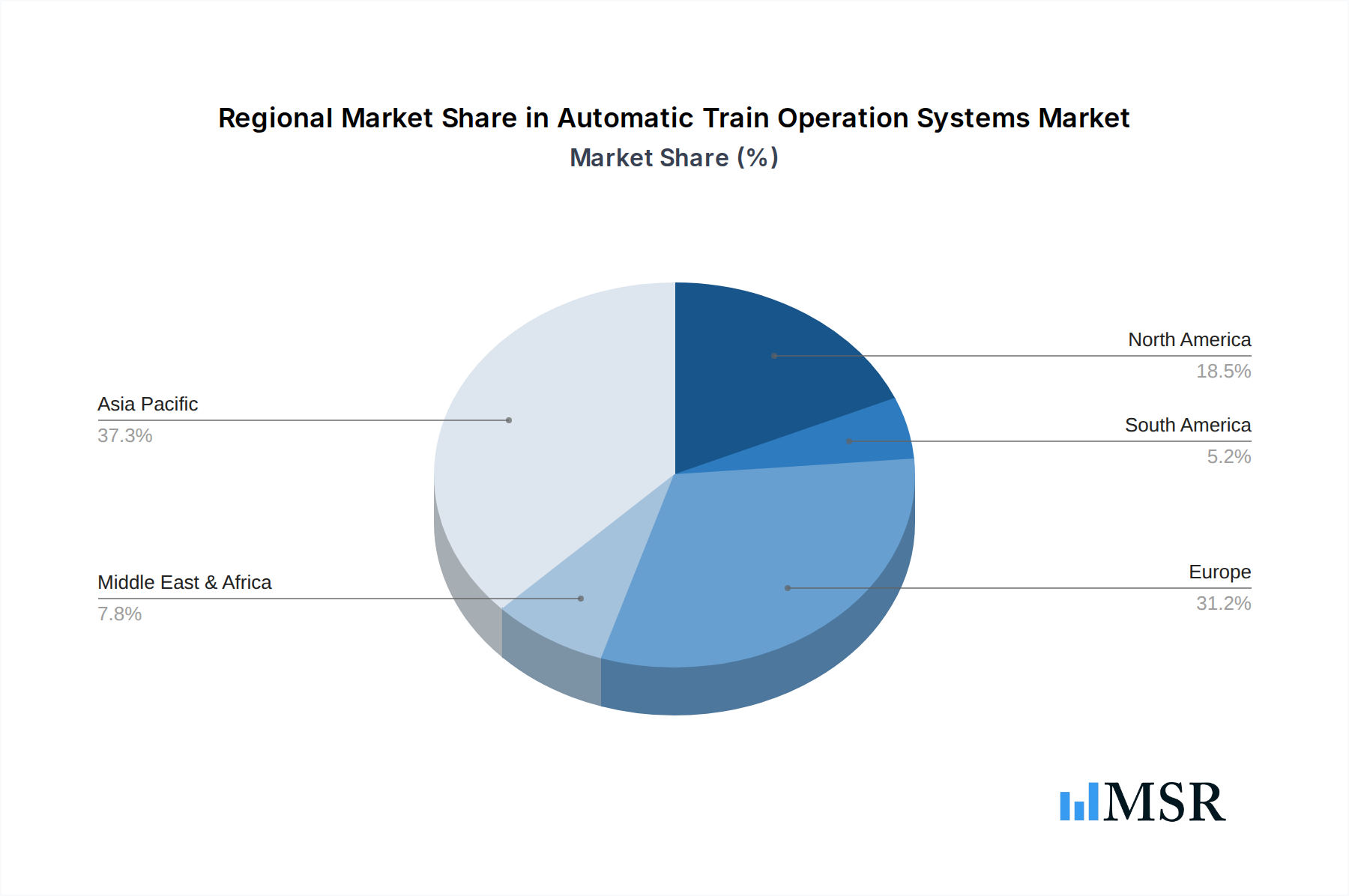

The market is segmented across various applications, with Urban Rail and Mainline segments showing strong adoption rates. Within the types of operation, Semi-automatic Train Operation, Driverless Train Operation, and Unattended Train Operation are all experiencing growth, reflecting a progressive move towards higher levels of automation. Major industry players such as Hitachi, Thales, Alstom, Siemens, and CRSC are actively investing in research and development to offer cutting-edge ATO solutions. Geographically, Asia Pacific, particularly China and India, is emerging as a dominant region due to rapid urbanization and substantial government initiatives to modernize public transportation. Europe and North America are also significant markets, driven by stringent safety regulations and the ongoing technological advancements in their mature rail networks. Despite the promising outlook, challenges such as high initial investment costs and the need for specialized workforce training may pose some restraints to rapid widespread adoption in certain developing regions.

Automatic Train Operation Systems Company Market Share

Here's the SEO-optimized and engaging report description for Automatic Train Operation Systems:

Global Automatic Train Operation (ATO) Systems Market: In-Depth Analysis, Trends, and Future Outlook (2019-2033)

Dive into the transformative world of Automatic Train Operation (ATO) Systems with this comprehensive industry report. Covering the period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period spanning 2025-2033, this report offers unparalleled insights into a market poised for significant expansion. We analyze critical market dynamics, technological advancements, and the strategic landscape shaping the future of rail transportation. Explore the accelerating adoption of ATO across urban rail and mainline segments, driven by the increasing demand for enhanced safety, efficiency, and passenger capacity. Understand the nuances between Semi-automatic Train Operation, Driverless Train Operation, and Unattended Train Operation as the industry progresses towards greater automation. This report is an essential resource for industry stakeholders, investors, and decision-makers seeking to navigate and capitalize on the evolving ATO market.

Automatic Train Operation Systems Market Concentration & Dynamics

The Automatic Train Operation (ATO) Systems market is characterized by a moderate to high concentration, with key global players investing heavily in research and development to maintain a competitive edge. Innovation ecosystems are thriving, fostered by strategic partnerships between technology providers and railway operators. Regulatory frameworks are evolving to accommodate the increasing sophistication of ATO, with a strong emphasis on safety certification and interoperability standards. While direct substitute products are limited, advancements in conventional signaling and control systems present indirect competition. End-user trends are heavily influenced by the pursuit of operational efficiency, reduced energy consumption, and enhanced passenger experience. Mergers and acquisitions (M&A) activities are significant, with companies actively consolidating their market positions and acquiring innovative technologies. For example, in the historical period (2019-2024), there were an estimated 7 significant M&A deals valued at over a million dollars each, aimed at bolstering portfolios and expanding geographical reach. Market share is distributed among a few dominant players, with the top five companies holding approximately 65% of the global market. The ongoing development of next-generation ATO solutions, including AI-powered predictive maintenance and advanced obstacle detection, is a key driver of market dynamics.

Automatic Train Operation Systems Industry Insights & Trends

The Automatic Train Operation (ATO) Systems market is experiencing robust growth, projected to reach a global market size of $25,000 million by the estimated year 2025, with a compound annual growth rate (CAGR) of 12.5% over the forecast period (2025–2033). This expansion is propelled by a confluence of factors, including the escalating demand for enhanced railway safety, the imperative to improve operational efficiency, and the need to increase passenger throughput in increasingly congested urban environments. Technological disruptions are at the forefront of this evolution, with the integration of artificial intelligence (AI), machine learning (ML), and advanced sensor technologies transforming the capabilities of ATO systems. These advancements enable more precise train control, predictive maintenance, and real-time decision-making, leading to reduced delays and optimized energy consumption. Evolving consumer behaviors, characterized by a preference for sustainable and efficient public transportation, further fuel the adoption of automated rail solutions. Governments worldwide are also actively promoting the development and deployment of smart railway infrastructure, recognizing the economic and environmental benefits of ATO. For instance, infrastructure development projects worth billions of dollars are underway across major continents, explicitly incorporating ATO as a core component. The cybersecurity of ATO systems is also a growing concern and a focal point of development, ensuring the resilience of these critical infrastructure components against potential threats. Furthermore, the increasing focus on decarbonization in the transport sector positions ATO as a key enabler of energy-efficient operations, contributing to greener rail networks. The global investment in railway modernization and expansion projects, estimated to exceed $1,000,000 million over the study period, is directly contributing to the market's upward trajectory. The operational benefits, such as reduced headway times and increased service frequency, are becoming indispensable for modern urban and mainline rail operations, driving significant market momentum.

Key Markets & Segments Leading Automatic Train Operation Systems

The Urban Rail segment is a dominant force in the Automatic Train Operation (ATO) Systems market, driven by the rapid urbanization and the critical need for efficient, high-capacity public transportation in metropolitan areas. The Type segment of Driverless Train Operation (DTO) and Unattended Train Operation (UTO) is experiencing the most significant traction within urban rail, particularly for metro systems and light rail networks.

Drivers for Urban Rail Dominance:

- Rapid Urbanization: Growing city populations necessitate higher frequency and capacity public transport.

- Traffic Congestion: ATO systems offer a reliable alternative to increasingly congested road networks.

- Operational Efficiency: Automation reduces labor costs and optimizes train scheduling, leading to significant operational savings estimated at 15% per annum for operators.

- Enhanced Safety: Advanced signaling and control systems inherent in ATO drastically reduce the risk of human error, a primary cause of rail accidents.

- Passenger Experience: Increased service frequency and reduced travel times contribute to a more attractive public transport offering.

- Government Initiatives: Many governments are prioritizing public transport investment and smart city development, which often includes ATO deployment.

Mainline applications are also witnessing substantial growth, particularly for freight operations and intercity passenger services where automation can significantly improve efficiency and speed. The Semi-automatic Train Operation (STO) type remains prevalent in mainline applications where full automation is not yet feasible or mandated, providing enhanced driver assistance and safety features. However, the trend is shifting towards higher levels of automation even in mainline scenarios. The economic growth in developing nations, coupled with substantial infrastructure investments exceeding $500,000 million globally in the last five years, is a powerful catalyst for ATO adoption across both urban and mainline segments. Regions like Asia-Pacific, with its burgeoning megacities and ambitious infrastructure plans, are leading this charge. The cost-effectiveness of ATO, when considering the long-term operational savings and increased asset utilization, is a compelling argument for widespread adoption. For instance, the reduction in energy consumption through optimized acceleration and deceleration profiles can amount to savings of up to 5% per train per year. The market is also seeing a gradual shift in the application of driverless technologies from closed-system urban metros to more complex mainline environments, indicating a maturing technology and growing confidence in its reliability.

Automatic Train Operation Systems Product Developments

Recent product developments in Automatic Train Operation (ATO) Systems focus on enhancing safety, interoperability, and intelligence. Innovations include advanced sensor fusion for improved obstacle detection, AI-driven predictive maintenance to minimize downtime, and secure communication protocols to safeguard against cyber threats. The integration of 5G technology is enabling real-time data exchange for more precise train control and dynamic route management. Many new systems are designed for modularity, allowing for easier upgrades and adaptation to different rail infrastructure. These advancements provide a significant competitive edge, enabling operators to achieve higher service reliability and passenger capacity, with new systems demonstrating a potential 10% improvement in punctuality.

Challenges in the Automatic Train Operation Systems Market

The Automatic Train Operation (ATO) Systems market faces several significant challenges. Regulatory Hurdles remain a primary restraint, as stringent safety certification processes and evolving standards can delay deployments and increase costs. The High Initial Investment required for implementing advanced ATO systems is a barrier for some operators, particularly smaller transit agencies. Cybersecurity Concerns are paramount, as the interconnected nature of ATO systems makes them potential targets for sophisticated cyberattacks, requiring continuous investment in robust security measures. Furthermore, Interoperability Issues between different manufacturers' systems and legacy infrastructure can complicate integration efforts. Supply chain disruptions, as witnessed in recent global events, can also impact the timely delivery of critical components. The estimated impact of regulatory delays on project timelines is an average of 6-12 months, and the cost associated with cybersecurity infrastructure is projected to be in the range of 5-7% of total system cost.

Forces Driving Automatic Train Operation Systems Growth

The growth of the Automatic Train Operation (ATO) Systems market is propelled by several powerful forces. Increasing Demand for Enhanced Safety is a fundamental driver, as ATO significantly reduces the risk of human error, the leading cause of rail accidents. The Pursuit of Operational Efficiency by railway operators, aiming to reduce costs, optimize energy consumption, and increase service frequency, is another key motivator. Growing Urbanization and Passenger Traffic necessitate higher capacity and more reliable public transport solutions that ATO systems provide. Government Support and Investment in smart infrastructure and public transportation further accelerate adoption. For instance, government funding for railway modernization projects globally exceeds $300,000 million annually, a substantial portion of which is allocated to automation technologies. The Technological Advancements in areas like AI, IoT, and advanced sensors are making ATO systems more sophisticated, reliable, and cost-effective.

Challenges in the Automatic Train Operation Systems Market

Long-term growth catalysts for the Automatic Train Operation (ATO) Systems market are multifaceted and deeply embedded in the evolution of transportation. Continuous Innovation in AI and Machine Learning will unlock new levels of predictive capabilities, enabling proactive maintenance and optimized train performance, potentially reducing operational costs by an additional 10%. Strategic Partnerships between technology providers, railway operators, and infrastructure developers will accelerate the development and deployment of integrated ATO solutions, fostering wider market penetration. Market Expansions into emerging economies with rapidly developing railway networks represent a significant opportunity. The increasing focus on Sustainable Transportation will further drive the adoption of energy-efficient ATO systems, aligning with global environmental goals. The development of Standardized Interoperability Protocols will also be crucial for seamless integration and broader adoption across diverse rail networks, reducing implementation complexities and costs.

Emerging Opportunities in Automatic Train Operation Systems

Emerging opportunities in the Automatic Train Operation (ATO) Systems market are ripe for innovation and strategic investment. The Expansion of ATO into Freight Operations presents a substantial untapped market, offering significant efficiency gains in logistics. The development of Fully Unattended Train Operations (UTO) for goods transportation is a key emerging trend, promising substantial cost reductions and increased flexibility. New markets in developing nations with ambitious rail infrastructure plans are opening up, offering significant growth potential. The integration of ATO with other smart city technologies, such as autonomous vehicles and intelligent traffic management systems, creates synergistic opportunities for enhanced urban mobility. Consumer preferences are increasingly shifting towards on-demand and personalized travel experiences, which highly automated and efficient rail networks can effectively cater to. The development of edge computing solutions for real-time data processing directly on trains will further enhance the responsiveness and intelligence of ATO systems, reducing reliance on centralized control. The increasing need for resilient and secure transportation networks in the face of climate change and geopolitical uncertainties will also favor automated systems.

Leading Players in the Automatic Train Operation Systems Sector

- Hitachi

- Thales

- Alstom

- Nippon Signal

- CRSC

- Traffic Control Technology

- Siemens

- Kyosan

- Glarun Technology

- Unittec

- Mermec

Key Milestones in Automatic Train Operation Systems Industry

- 2019: Launch of Level 4 ATO systems on several major metro lines, demonstrating enhanced autonomy.

- 2020: Increased investment in cybersecurity for ATO systems due to rising cyber threats.

- 2021: Significant advancements in AI algorithms for predictive maintenance in ATO, promising over 20% reduction in unplanned downtime.

- 2022: Major railway infrastructure projects in Asia and Europe explicitly mandate the integration of advanced ATO.

- 2023: Emergence of UTO (Unattended Train Operation) pilot projects for passenger services beyond driverless metros.

- 2024: Growing focus on the standardization of open communication protocols for ATO systems to ensure interoperability.

Strategic Outlook for Automatic Train Operation Systems Market

The strategic outlook for the Automatic Train Operation (ATO) Systems market is exceptionally strong, driven by ongoing technological innovation and a global push for more efficient, sustainable, and safer transportation. Key growth accelerators include the continued expansion of driverless and unattended train operations, particularly in urban rail and increasingly in mainline applications. The integration of advanced AI and machine learning capabilities will further enhance predictive maintenance, optimize energy efficiency, and improve overall system reliability, potentially leading to operational savings of over 15%. Strategic partnerships and collaborations will be crucial for navigating complex project requirements and accelerating market penetration. Emerging markets in developing economies represent significant untapped potential, while established markets will continue to drive demand for upgrades and next-generation systems. The overarching trend towards smart cities and intelligent infrastructure further solidifies the indispensable role of ATO in shaping the future of rail transportation, with an estimated $50,000 million worth of new ATO system installations projected over the forecast period.

Automatic Train Operation Systems Segmentation

-

1. Application

- 1.1. Urban Rail

- 1.2. Mainline

-

2. Type

- 2.1. Semi-automatic Train Operation

- 2.2. Driverless Train Operation

- 2.3. Unattended Train Operation

Automatic Train Operation Systems Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automatic Train Operation Systems Regional Market Share

Geographic Coverage of Automatic Train Operation Systems

Automatic Train Operation Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automatic Train Operation Systems Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Urban Rail

- 5.1.2. Mainline

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Semi-automatic Train Operation

- 5.2.2. Driverless Train Operation

- 5.2.3. Unattended Train Operation

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automatic Train Operation Systems Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Urban Rail

- 6.1.2. Mainline

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Semi-automatic Train Operation

- 6.2.2. Driverless Train Operation

- 6.2.3. Unattended Train Operation

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automatic Train Operation Systems Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Urban Rail

- 7.1.2. Mainline

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Semi-automatic Train Operation

- 7.2.2. Driverless Train Operation

- 7.2.3. Unattended Train Operation

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automatic Train Operation Systems Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Urban Rail

- 8.1.2. Mainline

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Semi-automatic Train Operation

- 8.2.2. Driverless Train Operation

- 8.2.3. Unattended Train Operation

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automatic Train Operation Systems Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Urban Rail

- 9.1.2. Mainline

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Semi-automatic Train Operation

- 9.2.2. Driverless Train Operation

- 9.2.3. Unattended Train Operation

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automatic Train Operation Systems Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Urban Rail

- 10.1.2. Mainline

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Semi-automatic Train Operation

- 10.2.2. Driverless Train Operation

- 10.2.3. Unattended Train Operation

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Hitachi

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Thales

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Alstom

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nippon Signal

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 CRSC

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Traffic Control Technology

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Siemens

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kyosan

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Glarun Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Unittec

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Mermec

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Hitachi

List of Figures

- Figure 1: Global Automatic Train Operation Systems Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Automatic Train Operation Systems Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Automatic Train Operation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automatic Train Operation Systems Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Automatic Train Operation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automatic Train Operation Systems Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Automatic Train Operation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automatic Train Operation Systems Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Automatic Train Operation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automatic Train Operation Systems Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Automatic Train Operation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automatic Train Operation Systems Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Automatic Train Operation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automatic Train Operation Systems Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Automatic Train Operation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automatic Train Operation Systems Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Automatic Train Operation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automatic Train Operation Systems Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Automatic Train Operation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automatic Train Operation Systems Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automatic Train Operation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automatic Train Operation Systems Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automatic Train Operation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automatic Train Operation Systems Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automatic Train Operation Systems Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automatic Train Operation Systems Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Automatic Train Operation Systems Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automatic Train Operation Systems Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Automatic Train Operation Systems Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automatic Train Operation Systems Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Automatic Train Operation Systems Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automatic Train Operation Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Automatic Train Operation Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Automatic Train Operation Systems Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Automatic Train Operation Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Automatic Train Operation Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Automatic Train Operation Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Automatic Train Operation Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Automatic Train Operation Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Automatic Train Operation Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Automatic Train Operation Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Automatic Train Operation Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Automatic Train Operation Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Automatic Train Operation Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Automatic Train Operation Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Automatic Train Operation Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Automatic Train Operation Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Automatic Train Operation Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Automatic Train Operation Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automatic Train Operation Systems Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automatic Train Operation Systems?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Automatic Train Operation Systems?

Key companies in the market include Hitachi, Thales, Alstom, Nippon Signal, CRSC, Traffic Control Technology, Siemens, Kyosan, Glarun Technology, Unittec, Mermec.

3. What are the main segments of the Automatic Train Operation Systems?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automatic Train Operation Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automatic Train Operation Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automatic Train Operation Systems?

To stay informed about further developments, trends, and reports in the Automatic Train Operation Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence