Key Insights

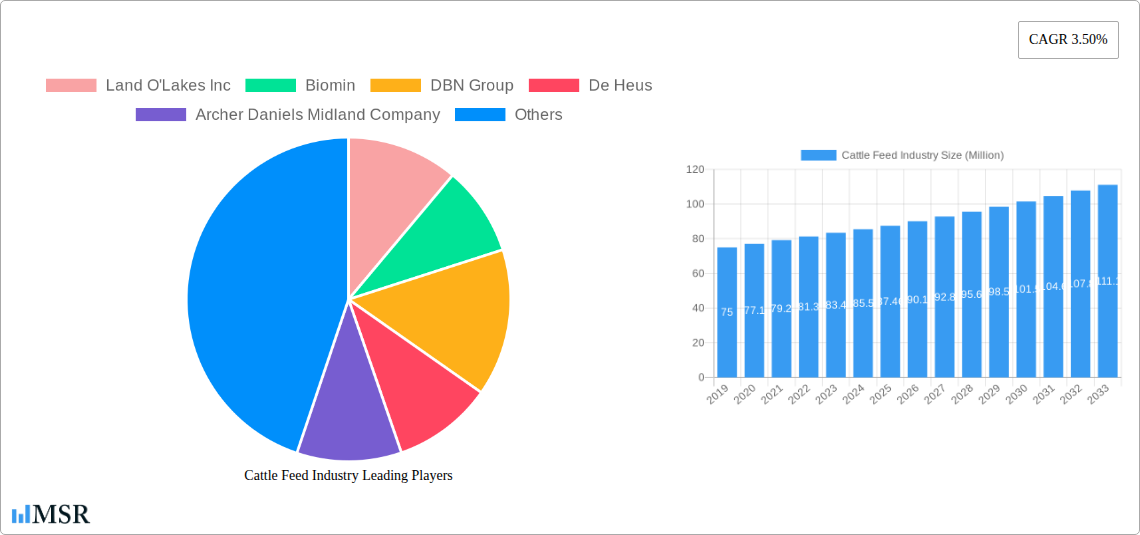

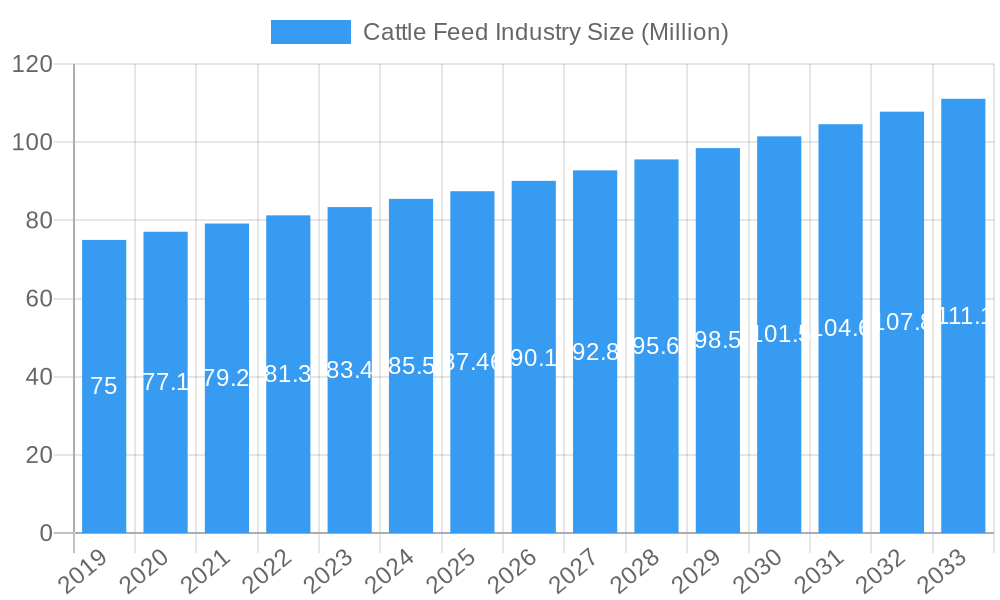

The global Cattle Feed Industry is poised for steady growth, projected to reach a market size of USD 87.46 million by 2025, with a Compound Annual Growth Rate (CAGR) of 3.50% through 2033. This expansion is underpinned by a confluence of factors driving demand for high-quality animal nutrition. Key among these drivers is the increasing global demand for protein, particularly beef and dairy products, which directly fuels the need for efficient and nutrient-rich cattle feed. Furthermore, advancements in animal husbandry practices and a growing awareness among farmers about the link between feed quality and animal health, productivity, and profitability are significant catalysts. The industry is also witnessing a pronounced trend towards the development and adoption of specialized feed formulations tailored to the specific nutritional requirements of different cattle types, including dairy cattle, beef cattle, and other breeds. This includes a growing emphasis on feed additives that enhance digestibility, promote growth, and prevent diseases, contributing to overall herd health and reducing reliance on antibiotics.

Cattle Feed Industry Market Size (In Million)

Despite the positive outlook, the industry faces certain restraints that warrant strategic attention. Rising raw material costs, particularly for key ingredients like cereals, can impact feed manufacturers' profit margins and potentially lead to higher feed prices for farmers. The volatility in grain markets, influenced by weather patterns, geopolitical events, and global supply chain disruptions, presents an ongoing challenge. Moreover, stringent regulations regarding feed safety, quality, and environmental sustainability can add to operational complexities and costs. However, the industry is actively addressing these challenges through innovation, such as exploring alternative feed ingredients like food waste and by-products, which not only offer cost benefits but also contribute to a more circular economy. The focus on research and development for more sustainable and efficient feed production methods will be crucial in navigating these headwinds and ensuring continued growth in the cattle feed market.

Cattle Feed Industry Company Market Share

This comprehensive report delves into the dynamic Cattle Feed Industry, providing an in-depth analysis of market size, growth drivers, emerging trends, and competitive landscape. With a focus on actionable insights for stakeholders, this study covers the period from 2019 to 2033, with a base year of 2025. We dissect critical segments including Dairy Cattle Feed, Beef Cattle Feed, and Other Cattle Types, alongside key ingredients such as Cereals, Cakes and Mixes, Food Wastages, Feed Additives, and Other Ingredients. Uncover the strategic moves of leading players like Land O'Lakes Inc, Biomin, DBN Group, De Heus, Archer Daniels Midland Company, New Hope Lihue, For Farmers Inc, Godrej Agrovet Limited, and Wen's Food Group.

Cattle Feed Industry Market Concentration & Dynamics

The global cattle feed market exhibits a moderate level of concentration, with several large multinational corporations and a significant number of regional and local players. Innovation in this sector is driven by a strong focus on animal health, productivity enhancement, and sustainability. Research and development efforts are concentrated on formulating scientifically advanced feed solutions that address specific nutritional requirements and improve feed conversion ratios. The regulatory landscape for animal feed production is becoming increasingly stringent globally, emphasizing safety, quality control, and traceability. This includes adherence to Good Manufacturing Practices (GMP) and specific regional food safety standards. Substitute products, such as forage and pasture grazing, remain significant but are often complemented by formulated feeds for optimal herd performance. End-user trends are increasingly influenced by consumer demand for sustainably sourced and high-quality animal protein. This translates into a growing demand for feed that supports animal welfare and minimizes environmental impact. Mergers and Acquisitions (M&A) activities are a key dynamic, indicating consolidation and strategic expansion. The cattle feed industry has witnessed numerous M&A deals aimed at expanding market reach, acquiring new technologies, and enhancing product portfolios. For instance, the acquisition of MNS Feed by De Heus in Vietnam significantly bolstered its position in the Southeast Asian market, underscoring the strategic importance of M&A in capturing market share. The market share of major players is constantly being reshaped by these strategic maneuvers and ongoing innovation.

Cattle Feed Industry Industry Insights & Trends

The cattle feed industry is experiencing robust growth, driven by a confluence of factors that are reshaping agricultural practices and food production worldwide. The increasing global population, projected to reach over 9.7 billion by 2050, directly translates into a higher demand for animal protein, particularly beef and dairy products. This escalating demand serves as a primary catalyst for the expansion of the cattle farming sector and, consequently, the cattle feed market. Furthermore, rising disposable incomes in developing economies have led to a shift in dietary patterns, with consumers increasingly incorporating meat and dairy into their diets, further fueling the need for efficient and high-quality cattle feed solutions. Technological advancements are revolutionizing feed formulation and production. Innovations in precision nutrition, feed additives (such as enzymes, probiotics, and prebiotics), and the utilization of novel ingredients are enhancing feed efficiency, improving animal health, and reducing the environmental footprint of cattle farming. The integration of digital technologies, including AI and data analytics, in feed management is optimizing feeding strategies and improving farm profitability. Evolving consumer behaviors are also playing a pivotal role. There is a growing consumer preference for ethically produced, sustainable, and traceable food products. This trend is compelling cattle farmers and feed manufacturers to adopt practices that prioritize animal welfare, reduce greenhouse gas emissions, and minimize waste. The increasing adoption of sustainable feeding practices, including the use of by-products and alternative protein sources, reflects this shift. The global cattle feed market size is estimated to be in the hundreds of billions of dollars, with a projected Compound Annual Growth Rate (CAGR) of approximately 4-6% over the forecast period. The market is witnessing a surge in demand for specialized feeds tailored to specific life stages, breeds, and production goals of cattle. This includes a growing emphasis on beef cattle feed for meat production and dairy cattle feed for milk yield optimization. The development of cost-effective and nutrient-dense feed formulations remains a critical focus for industry players seeking to maximize profitability and sustainability in the competitive animal feed sector. The strategic importance of feed additives in enhancing nutritional value and promoting animal health is also a significant trend, driving innovation and market growth.

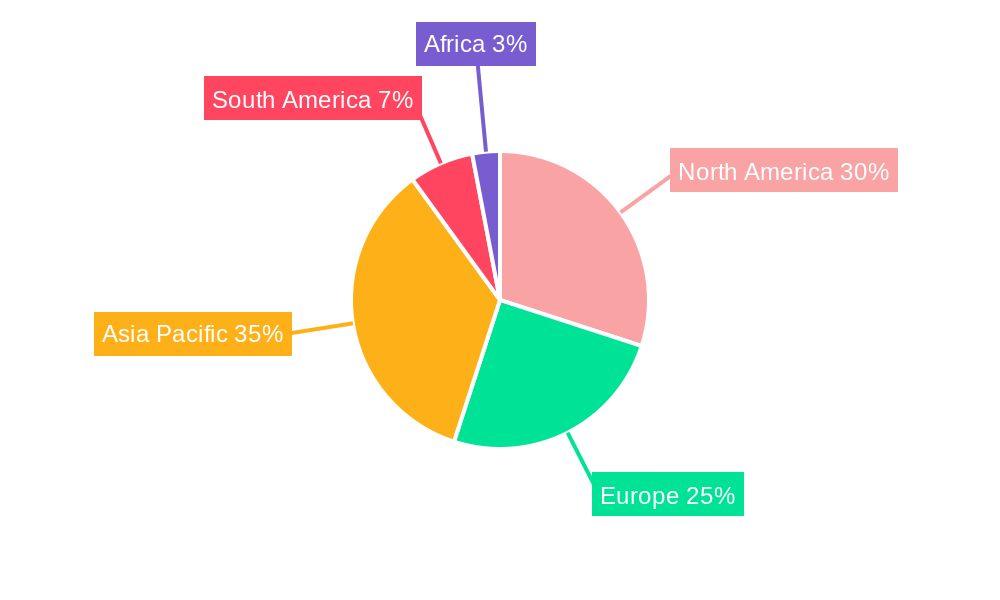

Key Markets & Segments Leading Cattle Feed Industry

The cattle feed industry is characterized by distinct regional dominance and segment leadership, driven by a variety of economic, environmental, and demographic factors. North America, particularly the United States, and Europe remain significant markets due to their established large-scale cattle operations and high per capita consumption of beef and dairy products. However, the Asia-Pacific region is emerging as the fastest-growing market, propelled by economic development, a burgeoning middle class, and increasing demand for animal protein. Countries like China, India, and Brazil are witnessing substantial growth in their cattle populations and feed consumption.

Animal Type Dominance:

- Dairy Cattle: This segment is a dominant force in the cattle feed market, driven by the consistent global demand for milk and dairy products. Advanced nutritional formulations aimed at maximizing milk yield, improving milk quality, and ensuring reproductive health are key to this segment's success. The economic viability of dairy farming is intrinsically linked to the efficiency of dairy cattle feed, making it a focal point for innovation.

- Beef Cattle: The beef cattle feed segment is also a major contributor, catering to the substantial global demand for beef. Feed formulations in this segment focus on optimizing growth rates, improving carcass quality, and enhancing feed conversion efficiency to ensure profitability for ranchers. Growing consumer preferences for lean and healthy beef further influence feed composition.

- Other Cattle Types: This segment encompasses feed for dual-purpose cattle and specialized breeds. While smaller in volume compared to dairy and beef, it represents a niche market with specific nutritional requirements.

Ingredient Dominance:

- Cereals: Grains such as corn, wheat, barley, and sorghum are foundational ingredients in most cattle feed formulations. Their prevalence is due to their high energy content and widespread availability, making them cost-effective staples for cattle nutrition.

- Cakes and Mixes: These often include oilseed cakes (like soybean meal and cottonseed meal) which are crucial sources of protein. They are expertly formulated and mixed with other ingredients to create balanced animal feed rations.

- Feed Additives: This segment is experiencing significant growth. It includes vitamins, minerals, amino acids, enzymes, probiotics, prebiotics, and other performance enhancers. Feed additives are vital for improving digestibility, boosting immunity, optimizing growth, and addressing specific health concerns in cattle, significantly impacting the cattle feed market growth.

- Food Wastages: The utilization of safe and processed food waste as an ingredient in cattle feed is a growing trend, driven by the need for sustainable and cost-effective solutions. This practice aligns with circular economy principles and reduces reliance on traditional feed crops.

The dominance of specific regions and segments is influenced by factors such as the size of the cattle population, the prevalence of dairy versus beef farming, economic prosperity, government policies supporting agriculture, and the availability of raw materials for feed production. The ongoing expansion of infrastructure for feed processing and distribution in emerging economies is further accelerating growth across these key markets and segments within the cattle feed industry.

Cattle Feed Industry Product Developments

Product innovation in the cattle feed industry is intensely focused on enhancing nutritional efficacy, promoting animal health, and improving sustainability. Key developments include the introduction of advanced feed additives such as improved enzyme formulations for enhanced nutrient digestibility, probiotics and prebiotics for gut health optimization, and encapsulated nutrients for targeted delivery. Furthermore, there is a growing trend towards developing specialized feed blends tailored to specific cattle breeds, age groups, and production stages, whether for intensive beef finishing or high-yield dairy operations. The incorporation of novel ingredients, including insect protein and algae-based supplements, is also gaining traction as manufacturers seek more sustainable and cost-effective protein sources. These advancements are crucial for meeting the evolving demands of the global cattle feed market and providing competitive edges for industry players.

Challenges in the Cattle Feed Industry Market

The cattle feed industry faces several significant challenges that impact its growth trajectory and operational efficiency. Volatility in raw material prices, particularly for key ingredients like corn and soybeans, poses a constant threat to profitability and can lead to price instability for end-users. Stringent and evolving regulatory frameworks regarding feed safety, ingredient sourcing, and environmental impact can increase compliance costs and necessitate significant investment in quality control and infrastructure. Supply chain disruptions, exacerbated by geopolitical events, climate change impacts, and logistical complexities, can hinder the timely and cost-effective delivery of feed ingredients and finished products. Furthermore, competitive pressures from numerous domestic and international players necessitate continuous innovation and cost optimization strategies. The increasing focus on animal welfare and sustainability also presents a challenge, requiring producers to invest in new technologies and practices to meet evolving consumer and regulatory expectations.

Forces Driving Cattle Feed Industry Growth

The cattle feed industry is propelled by a potent mix of technological, economic, and environmental forces. Technological advancements in animal nutrition science are leading to the development of more efficient and targeted feed formulations. This includes the use of advanced feed additives like enzymes and probiotics, which enhance nutrient absorption and improve animal health, directly contributing to increased productivity and profitability for farmers. Economic growth, particularly in developing nations, is fueling a rising global demand for animal protein, consequently boosting the need for high-quality cattle feed. Government initiatives supporting agricultural modernization and livestock development further stimulate market expansion. Environmental concerns are also driving innovation, leading to the development of sustainable feed solutions that minimize environmental impact, such as the utilization of by-products and the reduction of greenhouse gas emissions from cattle. The increasing adoption of precision feeding technologies, leveraging data analytics and AI, is optimizing feed utilization and resource management, making the cattle feed market more efficient.

Challenges in the Cattle Feed Industry Market

Long-term growth catalysts in the cattle feed industry are deeply intertwined with continuous innovation and strategic market expansion. The ongoing development of novel feed ingredients, including alternative protein sources like insect meal and microalgae, represents a significant opportunity to enhance sustainability and reduce reliance on traditional feed crops. Further research into the microbiome of cattle and the development of scientifically backed probiotics and prebiotics will drive advancements in animal health and feed efficiency. Strategic partnerships and collaborations between feed manufacturers, research institutions, and technology providers are crucial for accelerating the adoption of new technologies and product development. Market expansion into emerging economies, coupled with tailoring product offerings to local needs and preferences, will unlock significant growth potential. The increasing focus on a circular economy model, where by-products from other industries are utilized as feed ingredients, also presents a substantial long-term growth opportunity for a more sustainable cattle feed sector.

Emerging Opportunities in Cattle Feed Industry

Emerging trends and opportunities within the cattle feed industry are numerous and varied. The growing consumer demand for ethically produced and sustainable meat and dairy products is creating significant opportunities for feed manufacturers that can offer transparent sourcing and environmentally conscious feed solutions. The development and widespread adoption of precision livestock farming technologies, including AI-powered feeding systems and real-time health monitoring, offer avenues for optimizing feed intake and animal well-being, leading to increased efficiency and reduced waste. The increasing interest in regenerative agriculture practices presents an opportunity to integrate cattle into broader sustainable farming systems, with feed playing a crucial role in supporting soil health and ecosystem balance. Furthermore, the rise of alternative protein sources as feed ingredients, such as plant-based proteins and insect meal, is opening new markets and driving innovation in feed formulation. The development of functional feeds designed to improve specific aspects of animal health, such as immune function or stress reduction, also presents a significant and growing opportunity.

Leading Players in the Cattle Feed Industry Sector

- Land O'Lakes Inc

- Biomin

- DBN Group

- De Heus

- Archer Daniels Midland Company

- New Hope Lihue

- For Farmers Inc

- Godrej Agrovet Limited

- Wen's Food Group

Key Milestones in Cattle Feed Industry Industry

- January 2023: De Heus Animal Nutrition established a new greenfield animal feed factory in Ivory Coast with an initial capacity of producing 120,000 metric ton of feed for animals including cattle, marking a strategic expansion in Africa.

- May 2022: Archer Daniels Midland Co. acquired a feed mill in Southern Mindanao, the Philippines, expanding its Animal Nutrition footprint and market reach in the region.

- November 2021: De Heus Vietnam signed a strategic agreement with Masan, after which De Heus obtained control of 100% of the feed-related business of MNS Feed. The feed business of MNS Feed covers thirteen animal feed mills, with a total production capacity of nearly 4 million metric ton, significantly strengthening De Heus' position in Southeast Asia's largest animal feed market.

Strategic Outlook for Cattle Feed Industry Market

The strategic outlook for the cattle feed industry is exceptionally positive, characterized by sustained growth and evolving market dynamics. Key growth accelerators include the ongoing global demand for animal protein, driven by population growth and rising disposable incomes, particularly in emerging economies. The continuous advancement in feed additives and nutritional science is enabling more efficient and healthier livestock production, further boosting demand for sophisticated feed solutions. The increasing integration of digital technologies in farm management and feed delivery systems promises to enhance operational efficiency and profitability for stakeholders. Furthermore, the growing emphasis on sustainability and ethical farming practices is creating opportunities for companies that can offer environmentally friendly and welfare-conscious feed products. Strategic investments in research and development, market expansion into high-growth regions, and a focus on product diversification will be crucial for companies aiming to capitalize on the substantial future market potential within the cattle feed sector.

Cattle Feed Industry Segmentation

-

1. Animal Type

- 1.1. Dairy Cattle

- 1.2. Beef Cattle

- 1.3. Other Cattle Types

-

2. Ingredient

- 2.1. Cereals

- 2.2. Cakes and Mixes

- 2.3. Food Wastages

- 2.4. Feed Additives

- 2.5. Other Ingredients

Cattle Feed Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Russia

- 2.6. Italy

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of the Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Africa

- 5.1. South Africa

- 5.2. Rest of Africa

Cattle Feed Industry Regional Market Share

Geographic Coverage of Cattle Feed Industry

Cattle Feed Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Animal Type

- 5.1.1. Dairy Cattle

- 5.1.2. Beef Cattle

- 5.1.3. Other Cattle Types

- 5.2. Market Analysis, Insights and Forecast - by Ingredient

- 5.2.1. Cereals

- 5.2.2. Cakes and Mixes

- 5.2.3. Food Wastages

- 5.2.4. Feed Additives

- 5.2.5. Other Ingredients

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Africa

- 5.1. Market Analysis, Insights and Forecast - by Animal Type

- 6. Global Cattle Feed Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Animal Type

- 6.1.1. Dairy Cattle

- 6.1.2. Beef Cattle

- 6.1.3. Other Cattle Types

- 6.2. Market Analysis, Insights and Forecast - by Ingredient

- 6.2.1. Cereals

- 6.2.2. Cakes and Mixes

- 6.2.3. Food Wastages

- 6.2.4. Feed Additives

- 6.2.5. Other Ingredients

- 6.1. Market Analysis, Insights and Forecast - by Animal Type

- 7. North America Cattle Feed Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Animal Type

- 7.1.1. Dairy Cattle

- 7.1.2. Beef Cattle

- 7.1.3. Other Cattle Types

- 7.2. Market Analysis, Insights and Forecast - by Ingredient

- 7.2.1. Cereals

- 7.2.2. Cakes and Mixes

- 7.2.3. Food Wastages

- 7.2.4. Feed Additives

- 7.2.5. Other Ingredients

- 7.1. Market Analysis, Insights and Forecast - by Animal Type

- 8. Europe Cattle Feed Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Animal Type

- 8.1.1. Dairy Cattle

- 8.1.2. Beef Cattle

- 8.1.3. Other Cattle Types

- 8.2. Market Analysis, Insights and Forecast - by Ingredient

- 8.2.1. Cereals

- 8.2.2. Cakes and Mixes

- 8.2.3. Food Wastages

- 8.2.4. Feed Additives

- 8.2.5. Other Ingredients

- 8.1. Market Analysis, Insights and Forecast - by Animal Type

- 9. Asia Pacific Cattle Feed Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Animal Type

- 9.1.1. Dairy Cattle

- 9.1.2. Beef Cattle

- 9.1.3. Other Cattle Types

- 9.2. Market Analysis, Insights and Forecast - by Ingredient

- 9.2.1. Cereals

- 9.2.2. Cakes and Mixes

- 9.2.3. Food Wastages

- 9.2.4. Feed Additives

- 9.2.5. Other Ingredients

- 9.1. Market Analysis, Insights and Forecast - by Animal Type

- 10. South America Cattle Feed Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Animal Type

- 10.1.1. Dairy Cattle

- 10.1.2. Beef Cattle

- 10.1.3. Other Cattle Types

- 10.2. Market Analysis, Insights and Forecast - by Ingredient

- 10.2.1. Cereals

- 10.2.2. Cakes and Mixes

- 10.2.3. Food Wastages

- 10.2.4. Feed Additives

- 10.2.5. Other Ingredients

- 10.1. Market Analysis, Insights and Forecast - by Animal Type

- 11. Africa Cattle Feed Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Animal Type

- 11.1.1. Dairy Cattle

- 11.1.2. Beef Cattle

- 11.1.3. Other Cattle Types

- 11.2. Market Analysis, Insights and Forecast - by Ingredient

- 11.2.1. Cereals

- 11.2.2. Cakes and Mixes

- 11.2.3. Food Wastages

- 11.2.4. Feed Additives

- 11.2.5. Other Ingredients

- 11.1. Market Analysis, Insights and Forecast - by Animal Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Land O'Lakes Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Biomin

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DBN Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 De Heus

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Archer Daniels Midland Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 New Hope Lihue

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 For Farmers Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Godrej Agrovet Limite

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Wen's Food Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Land O'Lakes Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cattle Feed Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Cattle Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 3: North America Cattle Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 4: North America Cattle Feed Industry Revenue (Million), by Ingredient 2025 & 2033

- Figure 5: North America Cattle Feed Industry Revenue Share (%), by Ingredient 2025 & 2033

- Figure 6: North America Cattle Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Cattle Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Cattle Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 9: Europe Cattle Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 10: Europe Cattle Feed Industry Revenue (Million), by Ingredient 2025 & 2033

- Figure 11: Europe Cattle Feed Industry Revenue Share (%), by Ingredient 2025 & 2033

- Figure 12: Europe Cattle Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Cattle Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Cattle Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 15: Asia Pacific Cattle Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 16: Asia Pacific Cattle Feed Industry Revenue (Million), by Ingredient 2025 & 2033

- Figure 17: Asia Pacific Cattle Feed Industry Revenue Share (%), by Ingredient 2025 & 2033

- Figure 18: Asia Pacific Cattle Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Cattle Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Cattle Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 21: South America Cattle Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 22: South America Cattle Feed Industry Revenue (Million), by Ingredient 2025 & 2033

- Figure 23: South America Cattle Feed Industry Revenue Share (%), by Ingredient 2025 & 2033

- Figure 24: South America Cattle Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: South America Cattle Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Africa Cattle Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 27: Africa Cattle Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 28: Africa Cattle Feed Industry Revenue (Million), by Ingredient 2025 & 2033

- Figure 29: Africa Cattle Feed Industry Revenue Share (%), by Ingredient 2025 & 2033

- Figure 30: Africa Cattle Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Africa Cattle Feed Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cattle Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 2: Global Cattle Feed Industry Revenue Million Forecast, by Ingredient 2020 & 2033

- Table 3: Global Cattle Feed Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Cattle Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 5: Global Cattle Feed Industry Revenue Million Forecast, by Ingredient 2020 & 2033

- Table 6: Global Cattle Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Rest of North America Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Cattle Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 12: Global Cattle Feed Industry Revenue Million Forecast, by Ingredient 2020 & 2033

- Table 13: Global Cattle Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 14: Germany Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: United Kingdom Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: France Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Russia Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Italy Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Cattle Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 22: Global Cattle Feed Industry Revenue Million Forecast, by Ingredient 2020 & 2033

- Table 23: Global Cattle Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: China Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: India Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Japan Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Australia Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Rest of the Asia Pacific Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Global Cattle Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 30: Global Cattle Feed Industry Revenue Million Forecast, by Ingredient 2020 & 2033

- Table 31: Global Cattle Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 32: Brazil Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Argentina Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Rest of South America Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Global Cattle Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 36: Global Cattle Feed Industry Revenue Million Forecast, by Ingredient 2020 & 2033

- Table 37: Global Cattle Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 38: South Africa Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of Africa Cattle Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cattle Feed Industry?

The projected CAGR is approximately 3.50%.

2. Which companies are prominent players in the Cattle Feed Industry?

Key companies in the market include Land O'Lakes Inc, Biomin, DBN Group, De Heus, Archer Daniels Midland Company, New Hope Lihue, For Farmers Inc, Godrej Agrovet Limite, Wen's Food Group.

3. What are the main segments of the Cattle Feed Industry?

The market segments include Animal Type, Ingredient.

4. Can you provide details about the market size?

The market size is estimated to be USD 87.46 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Meat; Initiatives By the Key Players; Focus on Animal nutrition and Health.

6. What are the notable trends driving market growth?

Increasing Industrialization of Livestock Production in Developing Countries.

7. Are there any restraints impacting market growth?

Shift Toward Vegan- Based Diet; Changing Raw Material Prices and Strict Government Rules to Restrict Market Growth.

8. Can you provide examples of recent developments in the market?

January 2023: De Heus Animal Nutrition established a new greenfield animal feed factory in Ivory Coast with an initial capacity of producing 120,000 metric ton of feed for animals including cattle.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cattle Feed Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cattle Feed Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cattle Feed Industry?

To stay informed about further developments, trends, and reports in the Cattle Feed Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence