Key Insights

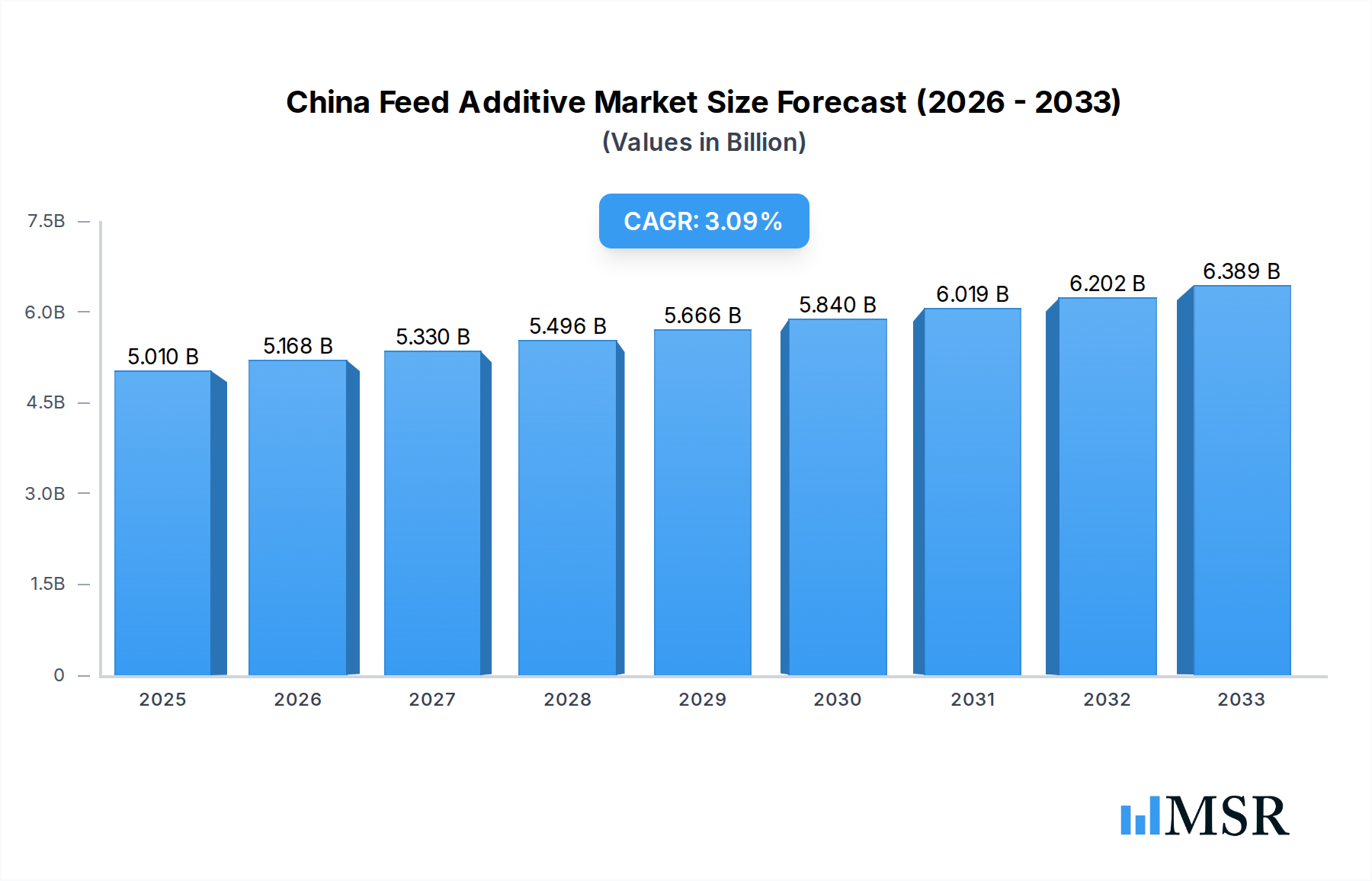

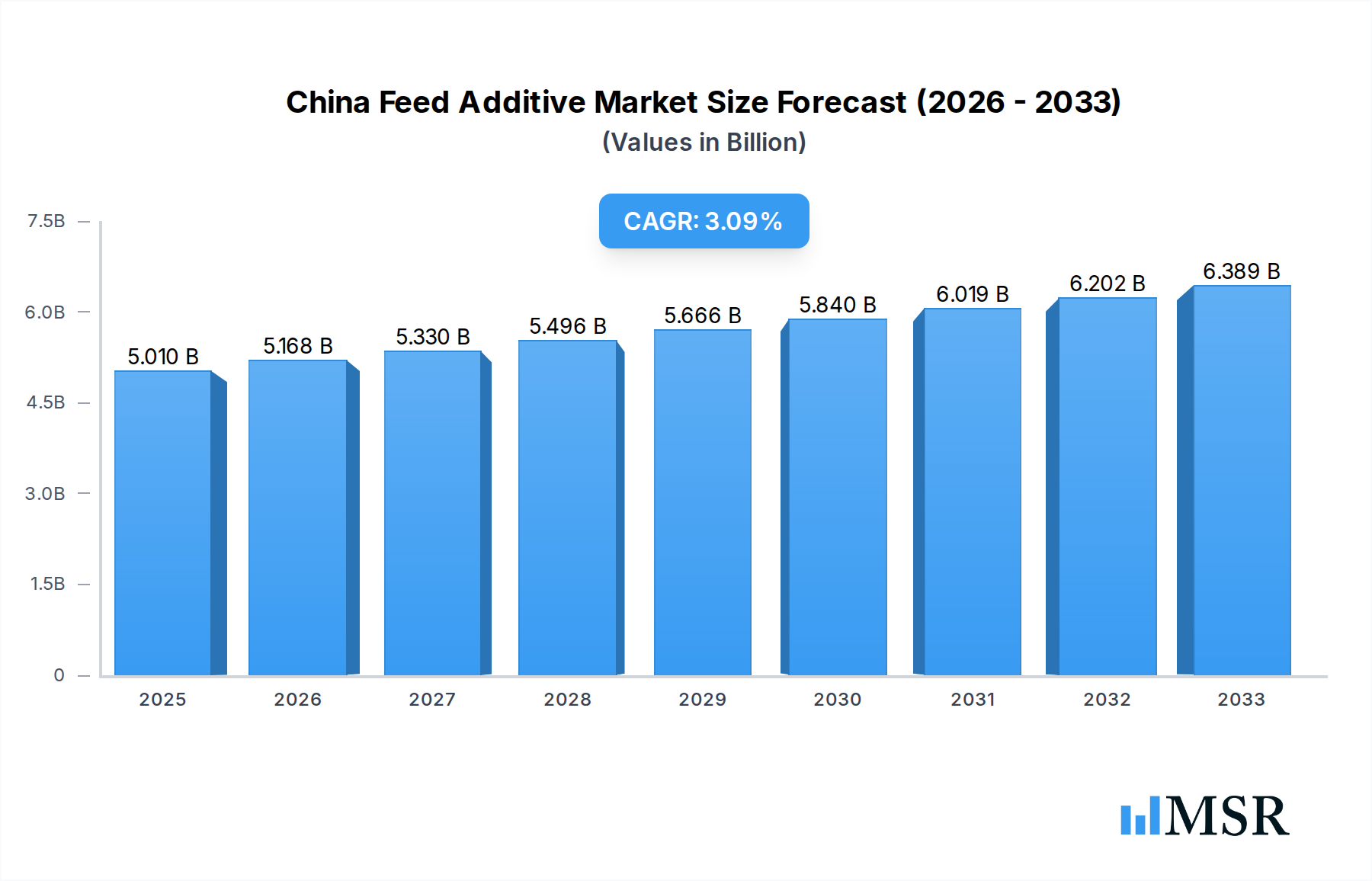

The China Feed Additive Market is poised for robust expansion, projected to reach a significant USD 5.01 billion in 2025, with an estimated Compound Annual Growth Rate (CAGR) of 3.18% during the forecast period of 2025-2033. This growth is underpinned by the escalating demand for high-quality animal protein, driven by China's burgeoning population and increasing disposable incomes. The nation's drive to enhance livestock productivity and ensure animal health and welfare, coupled with stringent regulations promoting the safe and efficient use of feed additives, are key market catalysts. Furthermore, the growing emphasis on sustainable animal agriculture practices is fostering innovation in the development of eco-friendly and highly effective feed additive solutions, contributing to market momentum.

China Feed Additive Market Market Size (In Billion)

The market is characterized by a diverse range of additive segments, each catering to specific nutritional and functional needs in animal feed. Acidifiers, amino acids, antioxidants, probiotics, prebiotics, and vitamins are among the prominent categories experiencing substantial uptake. The aquaculture and poultry sectors are anticipated to be major growth drivers, owing to their significant contributions to China's food security and the increasing adoption of advanced feeding practices. While the market presents immense opportunities, potential restraints such as fluctuating raw material prices and the cost-effectiveness of certain advanced additives may pose challenges. However, continuous research and development, alongside strategic collaborations among key market players, are expected to mitigate these challenges and unlock further growth avenues within the dynamic Chinese feed additive landscape.

China Feed Additive Market Company Market Share

China Feed Additive Market: Comprehensive Analysis and Forecast (2019-2033)

Unlock the lucrative China Feed Additive Market with our in-depth report, meticulously forecasting growth from 2019-2033, with a base year of 2025. This essential industry analysis provides unparalleled insights into the dynamic landscape of animal nutrition, poultry feed additives, swine feed additives, and aquaculture feed additives. Discover the projected market size of over $XX billion in 2025, driven by a robust CAGR of approximately XX% during the forecast period. Our report delves deep into key additive categories including amino acids (Lysine, Methionine, Threonine), vitamins, enzymes, probiotics, prebiotics, acidifiers, and phytogenics.

Explore the growth trajectories across various animal segments such as poultry, swine, ruminants, and aquaculture, identifying the primary drivers and market opportunities. We analyze critical industry developments, from Adisseo's strategic acquisitions and plant expansions to collaborations between Cargill and Delacon, all shaping the future of China's animal feed industry. This report is an indispensable resource for industry stakeholders, including feed manufacturers, animal nutrition companies, veterinary professionals, and investors, seeking to capitalize on the burgeoning Chinese feed additive market.

China Feed Additive Market Market Concentration & Dynamics

The China Feed Additive Market exhibits a moderate to high level of market concentration, characterized by the presence of a few dominant global players and a significant number of regional and domestic manufacturers. Innovation ecosystems are rapidly evolving, driven by the demand for sustainable and efficient animal production. Regulatory frameworks are becoming more stringent, focusing on feed safety, efficacy, and environmental impact, which influences product development and market entry. Substitute products, particularly natural and functional alternatives to traditional additives like antibiotics, are gaining traction. End-user trends are shifting towards a greater emphasis on animal welfare, gut health, and reduced antibiotic usage, propelling the demand for probiotics, prebiotics, phytogenics, and enzymes. Merger and Acquisition (M&A) activities are a key dynamic, as companies strategically consolidate to expand their product portfolios, geographical reach, and technological capabilities. For instance, recent M&A activities are aimed at acquiring specialized additive technologies and expanding into niche animal segments. The market share for key players is constantly being reshaped by these strategic moves and their ability to adapt to evolving market demands.

- Innovation Ecosystems: Driven by research in novel enzymes, gut health solutions, and sustainable sourcing of ingredients.

- Regulatory Frameworks: Increasing alignment with international standards, impacting product registration and usage.

- Substitute Products: Growing preference for natural and plant-based alternatives over synthetic or antibiotic-based additives.

- End-User Trends: Focus on antibiotic-free production, improved animal performance, and feed efficiency.

- M&A Activities: Strategic acquisitions and partnerships to enhance market position and product offerings.

China Feed Additive Market Industry Insights & Trends

The China Feed Additive Market is poised for significant expansion, fueled by several interconnected industry insights and trends that are reshaping the landscape of animal nutrition and feed production. The burgeoning demand for animal protein, driven by a growing middle class and increasing disposable incomes in China, directly translates to a higher volume of animal feed production. This surge in feed demand necessitates the use of advanced feed additives to optimize animal growth, improve feed conversion ratios, enhance animal health, and reduce the environmental footprint of livestock farming. Technological disruptions are playing a pivotal role, with ongoing advancements in biotechnology leading to the development of more effective and sustainable feed additives. For example, the discovery and application of novel enzymes that improve nutrient digestibility, the development of highly potent probiotics and prebiotics for gut health management, and the increasing integration of phytogenics as natural growth promoters are transforming traditional feeding practices.

Furthermore, evolving consumer behaviors are indirectly influencing the feed additive market. As Chinese consumers become more health-conscious and concerned about food safety, there is a heightened demand for meat and dairy products produced with minimal or no antibiotic residues. This consumer preference is a strong impetus for feed manufacturers to reduce their reliance on antibiotic growth promoters and adopt alternative solutions like organic acids, essential oils, and yeast derivatives. The market is also witnessing a growing emphasis on personalized nutrition, where feed additives are tailored to specific animal breeds, life stages, and production goals, leading to greater efficiency and improved animal welfare. Economic factors, such as government support for agricultural modernization and investments in research and development, are further bolstering the market's growth trajectory. The projected market size of over $XX billion in 2025, with an estimated CAGR of XX% during the forecast period, underscores the immense potential and the transformative trends shaping the China Feed Additive Market.

Key Markets & Segments Leading China Feed Additive Market

The China Feed Additive Market is experiencing robust growth across several key segments, with specific additive categories and animal types emerging as dominant forces.

Dominant Additive Segments:

- Amino Acids: This segment is a cornerstone of the China Feed Additive Market, driven by the critical need for essential amino acids to optimize animal growth and performance, particularly in poultry and swine. Lysine, Methionine, and Threonine are paramount, directly impacting feed formulation efficiency and cost-effectiveness. The increasing adoption of precision feeding strategies further amplifies the demand for these precise amino acid supplements.

- Vitamins: Essential for overall animal health, immune function, and metabolic processes, Vitamins remain a high-demand category. Vitamin A, Vitamin B complex, Vitamin C, and Vitamin E are crucial components of balanced animal feed, supporting everything from growth and reproduction to stress management.

- Enzymes: The growing emphasis on improving feed digestibility and nutrient utilization has propelled the Enzymes segment. Carbohydrases to break down complex carbohydrates and Phytases to release phosphorus from phytic acid are vital for reducing feed costs and environmental impact.

- Probiotics and Prebiotics: With the global push for antibiotic-free production, Probiotics (such as Lactobacilli, Bifidobacteria) and Prebiotics (like Fructo Oligosaccharides, Mannan Oligosaccharides) are experiencing exceptional growth. These additives enhance gut health, boost immunity, and improve nutrient absorption, offering a sustainable alternative to antibiotics.

- Acidifiers: Acidifiers like Fumaric Acid, Lactic Acid, and Propionic Acid are increasingly used to improve gut health, inhibit the growth of pathogenic bacteria, and enhance nutrient digestibility, particularly in young animals.

Dominant Animal Segments:

- Poultry: This remains the largest and fastest-growing animal segment in the China Feed Additive Market. The high consumption of poultry meat and eggs, coupled with intensive farming practices, drives substantial demand for a wide array of feed additives. Broilers and layers benefit from specialized formulations designed to maximize growth rates, improve meat quality, and enhance egg production.

- Swine: As China's primary source of pork, the Swine segment is another significant consumer of feed additives. Optimization of growth, feed efficiency, and disease prevention are key drivers for the use of amino acids, vitamins, minerals, and gut health promoters in swine feed.

- Aquaculture: With China's vast aquaculture industry, Aquaculture feed additives are gaining considerable traction. Shrimp and fish nutrition demands specialized additives to improve growth, disease resistance, and water quality.

- Ruminants: While perhaps not as rapidly growing as poultry or swine, the Ruminant segment, including Dairy Cattle and Beef Cattle, also represents a substantial market for feed additives, particularly those that enhance digestive efficiency and milk or meat production.

Drivers of Dominance:

- Economic Growth & Increased Protein Consumption: Rising disposable incomes drive demand for meat, dairy, and fish, consequently boosting animal feed production.

- Government Support for Agricultural Modernization: Policies promoting efficient and sustainable farming practices encourage the adoption of advanced feed additives.

- Technological Advancements: Innovations in enzymes, probiotics, prebiotics, and phytogenics offer superior performance and address specific animal health and production challenges.

- Focus on Food Safety and Reduced Antibiotic Usage: Consumer demand and regulatory pressures are accelerating the shift towards antibiotic-free production, favoring alternative feed additives.

- Cost-Effectiveness: Amino acids and enzymes directly contribute to reducing feed formulation costs and improving feed conversion ratios, making them indispensable.

China Feed Additive Market Product Developments

The China Feed Additive Market is witnessing a surge in product developments focused on enhancing animal health, optimizing performance, and promoting sustainability. Innovations are prominently seen in the Enzymes category, with new formulations designed for more efficient nutrient digestion and reduced environmental impact. The Probiotics and Prebiotics segments are also experiencing rapid advancement, with a focus on developing targeted strains for specific gut health benefits and immune modulation, crucial for antibiotic-free production. Phytogenics, including Essential Oils and Herbs & Spices, are seeing increased research and development for their antimicrobial and antioxidant properties as natural alternatives. Furthermore, advancements in Amino Acid production and delivery systems aim for enhanced bioavailability and cost-effectiveness. The market relevance of these developments lies in their ability to address critical industry challenges such as disease prevention, improved feed conversion, reduced antibiotic reliance, and the overall sustainability of animal agriculture in China, thereby providing competitive advantages to adopting stakeholders.

Challenges in the China Feed Additive Market Market

The China Feed Additive Market faces several significant challenges that can impede its growth trajectory. Stringent and evolving regulatory hurdles present a major barrier, with lengthy approval processes for new additives and inconsistencies in enforcement across regions. Supply chain disruptions, exacerbated by geopolitical factors and logistical complexities, can lead to price volatility and availability issues for key raw materials. Intense competition from both domestic and international players exerts considerable pressure on profit margins, forcing companies to innovate and optimize costs continuously. Furthermore, the initial investment required for adopting advanced feed additive technologies can be a deterrent for smaller enterprises, limiting widespread adoption. The need for extensive farmer education and technical support to effectively implement and utilize novel feed additives also poses an ongoing challenge.

Forces Driving China Feed Additive Market Growth

The China Feed Additive Market is propelled by a confluence of powerful growth drivers. The escalating demand for animal protein, fueled by a growing population and rising living standards, directly translates to increased animal feed consumption. Technological advancements in feed additive research and development, particularly in areas like enzymes, probiotics, prebiotics, and phytogenics, are creating more effective and sustainable solutions for animal nutrition. Government initiatives promoting agricultural modernization, food safety, and sustainable farming practices provide a supportive regulatory and economic environment. The global trend towards reducing antibiotic use in animal agriculture is a significant catalyst, driving the demand for alternative growth promoters and health enhancers. Furthermore, the increasing focus on improving feed conversion ratios and reducing production costs incentivizes the adoption of performance-enhancing feed additives.

Challenges in the China Feed Additive Market Market

While growth is robust, the China Feed Additive Market faces long-term challenges that require strategic navigation. The ongoing need to address increasing global scrutiny and domestic policies regarding environmental sustainability in animal agriculture necessitates the development of additives that minimize waste and pollution. The potential for the emergence of new animal diseases or drug-resistant pathogens could necessitate rapid adaptation and innovation in feed additive solutions. Maintaining consistent quality and efficacy across a vast and diverse production landscape, from large industrial farms to smaller operations, remains a challenge. The continuous need for farmer education and extension services to ensure proper application and maximum benefit from sophisticated feed additives requires significant investment in human capital and outreach. Addressing these long-term challenges will be crucial for sustained and responsible market expansion.

Emerging Opportunities in China Feed Additive Market

The China Feed Additive Market is ripe with emerging opportunities, particularly in the realm of sustainable and precision nutrition. The growing consumer demand for antibiotic-free and natural products is creating a significant market for Phytogenics, Probiotics, Prebiotics, and Organic Acids. The expanding Aquaculture sector presents a distinct opportunity for specialized feed additives tailored to enhance fish and shrimp health and growth. Advancements in biotechnology are enabling the development of highly targeted enzymes and amino acids that optimize nutrient utilization and reduce feed costs, aligning with precision farming objectives. Furthermore, the increasing focus on animal welfare and gut health management opens avenues for novel feed additives that improve digestive physiology and immune function. The "Belt and Road Initiative" may also present opportunities for market expansion into neighboring regions.

Leading Players in the China Feed Additive Market Sector

- Prinova Group LLC

- Solvay S A

- SHV (Nutreco NV)

- DSM Nutritional Products AG

- Kerry Group Plc

- Ajinomoto Co Inc

- Archer Daniel Midland Co

- BASF SE

- Alltech Inc

- Cargill Inc

- Adisseo

Key Milestones in China Feed Additive Market Industry

- December 2022: Adisseo group agreed to acquire Nor-Feed and its subsidiaries, signaling a strategic move to develop and register botanical feed additives for use in animal feed, enhancing its natural additive portfolio.

- September 2022: Adisseo's new 180,000-ton liquid methionine plant in Nanjing, China, commenced production. This facility, one of the largest global liquid methionine production capacities, significantly boosted the company's penetration of the global market for this crucial amino acid.

- June 2022: Delacon and Cargill collaborated to establish a global plant-based phytogenic feed additives business. This partnership leveraged extensive feed additive expertise and aimed to increase global presence in the rapidly growing natural additive segment.

Strategic Outlook for China Feed Additive Market Market

The strategic outlook for the China Feed Additive Market is characterized by sustained growth and a significant shift towards innovation and sustainability. Accelerating the adoption of advanced feed additives, particularly those that promote gut health, enhance immunity, and reduce antibiotic reliance, will be a key strategy. Investments in research and development for novel enzymes, probiotics, prebiotics, and phytogenics will be crucial for maintaining a competitive edge. Strategic partnerships and acquisitions will continue to play a vital role in expanding market reach and product portfolios, particularly in catering to the growing aquaculture and poultry segments. Furthermore, a focus on providing comprehensive technical support and education to farmers will be essential for driving the effective utilization of these advanced solutions, ensuring long-term market penetration and customer loyalty within this dynamic animal nutrition landscape.

China Feed Additive Market Segmentation

-

1. Additive

-

1.1. Acidifiers

-

1.1.1. By Sub Additive

- 1.1.1.1. Fumaric Acid

- 1.1.1.2. Lactic Acid

- 1.1.1.3. Propionic Acid

- 1.1.1.4. Other Acidifiers

-

1.1.1. By Sub Additive

-

1.2. Amino Acids

- 1.2.1. Lysine

- 1.2.2. Methionine

- 1.2.3. Threonine

- 1.2.4. Tryptophan

- 1.2.5. Other Amino Acids

-

1.3. Antibiotics

- 1.3.1. Bacitracin

- 1.3.2. Penicillins

- 1.3.3. Tetracyclines

- 1.3.4. Tylosin

- 1.3.5. Other Antibiotics

-

1.4. Antioxidants

- 1.4.1. Butylated Hydroxyanisole (BHA)

- 1.4.2. Butylated Hydroxytoluene (BHT)

- 1.4.3. Citric Acid

- 1.4.4. Ethoxyquin

- 1.4.5. Propyl Gallate

- 1.4.6. Tocopherols

- 1.4.7. Other Antioxidants

-

1.5. Binders

- 1.5.1. Natural Binders

- 1.5.2. Synthetic Binders

-

1.6. Enzymes

- 1.6.1. Carbohydrases

- 1.6.2. Phytases

- 1.6.3. Other Enzymes

- 1.7. Flavors & Sweeteners

-

1.8. Minerals

- 1.8.1. Macrominerals

- 1.8.2. Microminerals

-

1.9. Mycotoxin Detoxifiers

- 1.9.1. Biotransformers

-

1.10. Phytogenics

- 1.10.1. Essential Oil

- 1.10.2. Herbs & Spices

- 1.10.3. Other Phytogenics

-

1.11. Pigments

- 1.11.1. Carotenoids

- 1.11.2. Curcumin & Spirulina

-

1.12. Prebiotics

- 1.12.1. Fructo Oligosaccharides

- 1.12.2. Galacto Oligosaccharides

- 1.12.3. Inulin

- 1.12.4. Lactulose

- 1.12.5. Mannan Oligosaccharides

- 1.12.6. Xylo Oligosaccharides

- 1.12.7. Other Prebiotics

-

1.13. Probiotics

- 1.13.1. Bifidobacteria

- 1.13.2. Enterococcus

- 1.13.3. Lactobacilli

- 1.13.4. Pediococcus

- 1.13.5. Streptococcus

- 1.13.6. Other Probiotics

-

1.14. Vitamins

- 1.14.1. Vitamin A

- 1.14.2. Vitamin B

- 1.14.3. Vitamin C

- 1.14.4. Vitamin E

- 1.14.5. Other Vitamins

-

1.15. Yeast

- 1.15.1. Live Yeast

- 1.15.2. Selenium Yeast

- 1.15.3. Spent Yeast

- 1.15.4. Torula Dried Yeast

- 1.15.5. Whey Yeast

- 1.15.6. Yeast Derivatives

-

1.1. Acidifiers

-

2. Animal

-

2.1. Aquaculture

-

2.1.1. By Sub Animal

- 2.1.1.1. Fish

- 2.1.1.2. Shrimp

- 2.1.1.3. Other Aquaculture Species

-

2.1.1. By Sub Animal

-

2.2. Poultry

- 2.2.1. Broiler

- 2.2.2. Layer

- 2.2.3. Other Poultry Birds

-

2.3. Ruminants

- 2.3.1. Beef Cattle

- 2.3.2. Dairy Cattle

- 2.3.3. Other Ruminants

- 2.4. Swine

- 2.5. Other Animals

-

2.1. Aquaculture

China Feed Additive Market Segmentation By Geography

- 1. China

China Feed Additive Market Regional Market Share

Geographic Coverage of China Feed Additive Market

China Feed Additive Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.18% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Additive

- 5.1.1. Acidifiers

- 5.1.1.1. By Sub Additive

- 5.1.1.1.1. Fumaric Acid

- 5.1.1.1.2. Lactic Acid

- 5.1.1.1.3. Propionic Acid

- 5.1.1.1.4. Other Acidifiers

- 5.1.1.1. By Sub Additive

- 5.1.2. Amino Acids

- 5.1.2.1. Lysine

- 5.1.2.2. Methionine

- 5.1.2.3. Threonine

- 5.1.2.4. Tryptophan

- 5.1.2.5. Other Amino Acids

- 5.1.3. Antibiotics

- 5.1.3.1. Bacitracin

- 5.1.3.2. Penicillins

- 5.1.3.3. Tetracyclines

- 5.1.3.4. Tylosin

- 5.1.3.5. Other Antibiotics

- 5.1.4. Antioxidants

- 5.1.4.1. Butylated Hydroxyanisole (BHA)

- 5.1.4.2. Butylated Hydroxytoluene (BHT)

- 5.1.4.3. Citric Acid

- 5.1.4.4. Ethoxyquin

- 5.1.4.5. Propyl Gallate

- 5.1.4.6. Tocopherols

- 5.1.4.7. Other Antioxidants

- 5.1.5. Binders

- 5.1.5.1. Natural Binders

- 5.1.5.2. Synthetic Binders

- 5.1.6. Enzymes

- 5.1.6.1. Carbohydrases

- 5.1.6.2. Phytases

- 5.1.6.3. Other Enzymes

- 5.1.7. Flavors & Sweeteners

- 5.1.8. Minerals

- 5.1.8.1. Macrominerals

- 5.1.8.2. Microminerals

- 5.1.9. Mycotoxin Detoxifiers

- 5.1.9.1. Biotransformers

- 5.1.10. Phytogenics

- 5.1.10.1. Essential Oil

- 5.1.10.2. Herbs & Spices

- 5.1.10.3. Other Phytogenics

- 5.1.11. Pigments

- 5.1.11.1. Carotenoids

- 5.1.11.2. Curcumin & Spirulina

- 5.1.12. Prebiotics

- 5.1.12.1. Fructo Oligosaccharides

- 5.1.12.2. Galacto Oligosaccharides

- 5.1.12.3. Inulin

- 5.1.12.4. Lactulose

- 5.1.12.5. Mannan Oligosaccharides

- 5.1.12.6. Xylo Oligosaccharides

- 5.1.12.7. Other Prebiotics

- 5.1.13. Probiotics

- 5.1.13.1. Bifidobacteria

- 5.1.13.2. Enterococcus

- 5.1.13.3. Lactobacilli

- 5.1.13.4. Pediococcus

- 5.1.13.5. Streptococcus

- 5.1.13.6. Other Probiotics

- 5.1.14. Vitamins

- 5.1.14.1. Vitamin A

- 5.1.14.2. Vitamin B

- 5.1.14.3. Vitamin C

- 5.1.14.4. Vitamin E

- 5.1.14.5. Other Vitamins

- 5.1.15. Yeast

- 5.1.15.1. Live Yeast

- 5.1.15.2. Selenium Yeast

- 5.1.15.3. Spent Yeast

- 5.1.15.4. Torula Dried Yeast

- 5.1.15.5. Whey Yeast

- 5.1.15.6. Yeast Derivatives

- 5.1.1. Acidifiers

- 5.2. Market Analysis, Insights and Forecast - by Animal

- 5.2.1. Aquaculture

- 5.2.1.1. By Sub Animal

- 5.2.1.1.1. Fish

- 5.2.1.1.2. Shrimp

- 5.2.1.1.3. Other Aquaculture Species

- 5.2.1.1. By Sub Animal

- 5.2.2. Poultry

- 5.2.2.1. Broiler

- 5.2.2.2. Layer

- 5.2.2.3. Other Poultry Birds

- 5.2.3. Ruminants

- 5.2.3.1. Beef Cattle

- 5.2.3.2. Dairy Cattle

- 5.2.3.3. Other Ruminants

- 5.2.4. Swine

- 5.2.5. Other Animals

- 5.2.1. Aquaculture

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Additive

- 6. China Feed Additive Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Additive

- 6.1.1. Acidifiers

- 6.1.1.1. By Sub Additive

- 6.1.1.1.1. Fumaric Acid

- 6.1.1.1.2. Lactic Acid

- 6.1.1.1.3. Propionic Acid

- 6.1.1.1.4. Other Acidifiers

- 6.1.1.1. By Sub Additive

- 6.1.2. Amino Acids

- 6.1.2.1. Lysine

- 6.1.2.2. Methionine

- 6.1.2.3. Threonine

- 6.1.2.4. Tryptophan

- 6.1.2.5. Other Amino Acids

- 6.1.3. Antibiotics

- 6.1.3.1. Bacitracin

- 6.1.3.2. Penicillins

- 6.1.3.3. Tetracyclines

- 6.1.3.4. Tylosin

- 6.1.3.5. Other Antibiotics

- 6.1.4. Antioxidants

- 6.1.4.1. Butylated Hydroxyanisole (BHA)

- 6.1.4.2. Butylated Hydroxytoluene (BHT)

- 6.1.4.3. Citric Acid

- 6.1.4.4. Ethoxyquin

- 6.1.4.5. Propyl Gallate

- 6.1.4.6. Tocopherols

- 6.1.4.7. Other Antioxidants

- 6.1.5. Binders

- 6.1.5.1. Natural Binders

- 6.1.5.2. Synthetic Binders

- 6.1.6. Enzymes

- 6.1.6.1. Carbohydrases

- 6.1.6.2. Phytases

- 6.1.6.3. Other Enzymes

- 6.1.7. Flavors & Sweeteners

- 6.1.8. Minerals

- 6.1.8.1. Macrominerals

- 6.1.8.2. Microminerals

- 6.1.9. Mycotoxin Detoxifiers

- 6.1.9.1. Biotransformers

- 6.1.10. Phytogenics

- 6.1.10.1. Essential Oil

- 6.1.10.2. Herbs & Spices

- 6.1.10.3. Other Phytogenics

- 6.1.11. Pigments

- 6.1.11.1. Carotenoids

- 6.1.11.2. Curcumin & Spirulina

- 6.1.12. Prebiotics

- 6.1.12.1. Fructo Oligosaccharides

- 6.1.12.2. Galacto Oligosaccharides

- 6.1.12.3. Inulin

- 6.1.12.4. Lactulose

- 6.1.12.5. Mannan Oligosaccharides

- 6.1.12.6. Xylo Oligosaccharides

- 6.1.12.7. Other Prebiotics

- 6.1.13. Probiotics

- 6.1.13.1. Bifidobacteria

- 6.1.13.2. Enterococcus

- 6.1.13.3. Lactobacilli

- 6.1.13.4. Pediococcus

- 6.1.13.5. Streptococcus

- 6.1.13.6. Other Probiotics

- 6.1.14. Vitamins

- 6.1.14.1. Vitamin A

- 6.1.14.2. Vitamin B

- 6.1.14.3. Vitamin C

- 6.1.14.4. Vitamin E

- 6.1.14.5. Other Vitamins

- 6.1.15. Yeast

- 6.1.15.1. Live Yeast

- 6.1.15.2. Selenium Yeast

- 6.1.15.3. Spent Yeast

- 6.1.15.4. Torula Dried Yeast

- 6.1.15.5. Whey Yeast

- 6.1.15.6. Yeast Derivatives

- 6.1.1. Acidifiers

- 6.2. Market Analysis, Insights and Forecast - by Animal

- 6.2.1. Aquaculture

- 6.2.1.1. By Sub Animal

- 6.2.1.1.1. Fish

- 6.2.1.1.2. Shrimp

- 6.2.1.1.3. Other Aquaculture Species

- 6.2.1.1. By Sub Animal

- 6.2.2. Poultry

- 6.2.2.1. Broiler

- 6.2.2.2. Layer

- 6.2.2.3. Other Poultry Birds

- 6.2.3. Ruminants

- 6.2.3.1. Beef Cattle

- 6.2.3.2. Dairy Cattle

- 6.2.3.3. Other Ruminants

- 6.2.4. Swine

- 6.2.5. Other Animals

- 6.2.1. Aquaculture

- 6.1. Market Analysis, Insights and Forecast - by Additive

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Prinova Group LLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Solvay S A

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 SHV (Nutreco NV)

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 DSM Nutritional Products AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kerry Group Plc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Ajinomoto Co Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Archer Daniel Midland Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 BASF SE

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Alltech Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Cargill Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Adisseo

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Prinova Group LLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Feed Additive Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Feed Additive Market Share (%) by Company 2025

List of Tables

- Table 1: China Feed Additive Market Revenue billion Forecast, by Additive 2020 & 2033

- Table 2: China Feed Additive Market Revenue billion Forecast, by Animal 2020 & 2033

- Table 3: China Feed Additive Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: China Feed Additive Market Revenue billion Forecast, by Additive 2020 & 2033

- Table 5: China Feed Additive Market Revenue billion Forecast, by Animal 2020 & 2033

- Table 6: China Feed Additive Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Feed Additive Market?

The projected CAGR is approximately 3.18%.

2. Which companies are prominent players in the China Feed Additive Market?

Key companies in the market include Prinova Group LLC, Solvay S A, SHV (Nutreco NV), DSM Nutritional Products AG, Kerry Group Plc, Ajinomoto Co Inc, Archer Daniel Midland Co, BASF SE, Alltech Inc, Cargill Inc, Adisseo.

3. What are the main segments of the China Feed Additive Market?

The market segments include Additive, Animal.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.01 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Livestock Population; Area Under Forage Production is Increasing; Increasing Demand for Animal Products.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Competition Amongst Industries and High Input Prices; Growing Shift Toward Vegan-Based Diet.

8. Can you provide examples of recent developments in the market?

December 2022: Adisseo group had agreed to acquire Nor-Feed and its subsidiaries to develop and register botanical additives for use in animal feed.September 2022: The new 180,000-ton liquid methionine plant of Adisseo in Nanjing, China, started production. The facility is one of the largest global liquid methionine production capacities that boosted the penetration of liquid methionine manufactured by the company in the global market.June 2022: Delacon and Cargill collaborated to establish a global plant-based phytogenic feed additives business for enhanced animal nutrition. The partnership has helped in extensive feed additives expertise as well as an increase in the global presence.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Feed Additive Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Feed Additive Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Feed Additive Market?

To stay informed about further developments, trends, and reports in the China Feed Additive Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence