Key Insights

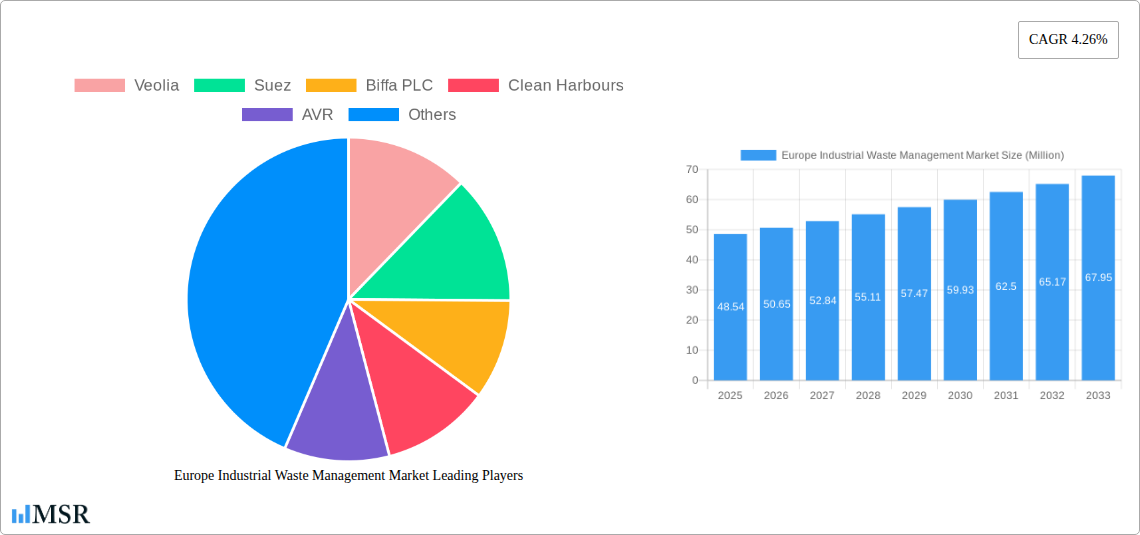

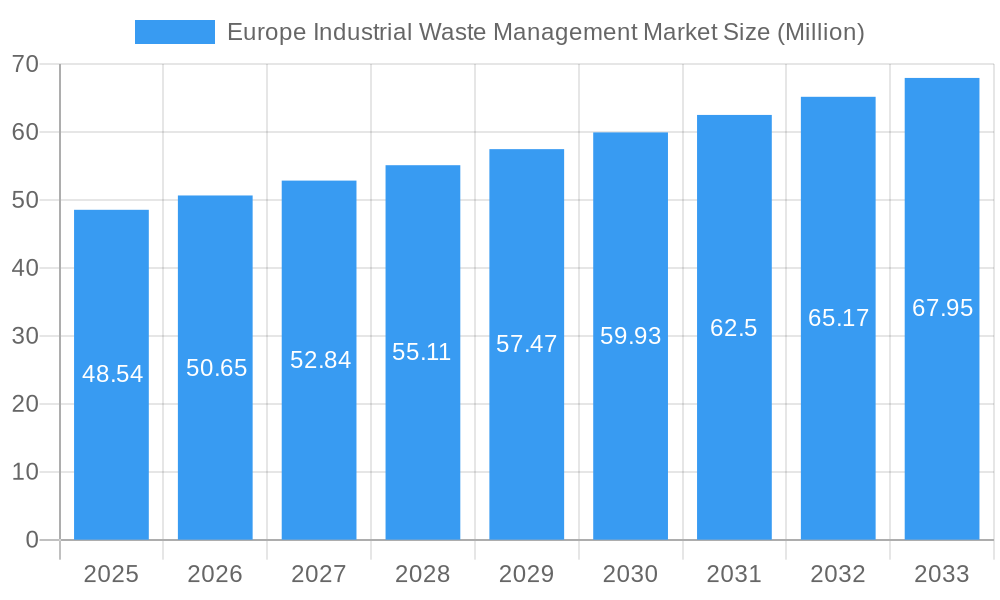

The Europe Industrial Waste Management Market is projected for substantial growth, with an estimated market size of USD 48.54 million in the base year of 2025. This expansion is underpinned by a robust Compound Annual Growth Rate (CAGR) of 4.26%, indicating a steady and significant upward trajectory for the forecast period spanning from 2025 to 2033. The market's vitality is driven by increasingly stringent environmental regulations across European nations, compelling industries to adopt more sustainable waste management practices. Furthermore, a growing awareness of the economic benefits associated with waste valorization and the circular economy is spurring investment in advanced recycling and resource recovery technologies. Key sectors contributing to industrial waste generation include Construction and Demolition, Manufacturing, and the Oil and Gas industry, each presenting unique challenges and opportunities for waste management service providers.

Europe Industrial Waste Management Market Market Size (In Million)

The market segmentation reveals a dynamic landscape. In terms of waste types, Construction and Demolition waste is expected to hold a significant share due to ongoing infrastructure development and renovation projects. Manufacturing waste, driven by evolving production processes and product lifecycles, also presents a substantial segment. The Oil and Gas waste segment, though potentially volatile due to fluctuating energy prices, requires specialized and often hazardous waste management solutions. On the service front, Recycling is emerging as a dominant segment, fueled by legislative push for higher recycling rates and the development of innovative recycling technologies. Landfill, while still a part of the waste management infrastructure, is gradually seeing its share diminish as European countries prioritize waste reduction and diversion. Incineration, particularly with energy recovery, offers a valuable alternative for non-recyclable waste. Leading companies like Veolia, Suez, and Biffa PLC are actively shaping this market through strategic acquisitions, technological advancements, and expanded service offerings to meet the diverse needs of industrial clients across key European regions such as the United Kingdom, Germany, and France.

Europe Industrial Waste Management Market Company Market Share

Unlock critical insights into the burgeoning Europe Industrial Waste Management market, valued at an estimated USD XXX Million in 2025 and projected for significant expansion through 2033. This in-depth report provides unparalleled analysis of market dynamics, key segments, emerging trends, and strategic opportunities. Essential for industry leaders, investors, and stakeholders seeking to navigate the complexities of industrial waste solutions across Europe.

Europe Industrial Waste Management Market Market Concentration & Dynamics

The Europe industrial waste management market exhibits a moderately concentrated landscape, with dominant players like Veolia, Suez, and Remondis holding significant market share. Innovation ecosystems are flourishing, driven by increasing regulatory stringency and the pursuit of circular economy principles. Key regulatory frameworks, such as the EU's Waste Framework Directive and REACH regulations, are profoundly shaping waste management practices, pushing for higher recycling rates and stricter disposal standards. The threat of substitute products, while present in niche areas, is largely mitigated by the specialized nature of industrial waste streams and the integrated service offerings of established providers. End-user trends are shifting towards sustainable and cost-effective waste valorization, with a growing demand for energy-from-waste solutions and advanced recycling technologies. Mergers and acquisitions (M&A) activity remains a key dynamic, with companies consolidating their positions and expanding their service portfolios. Recent M&A deals have focused on acquiring specialized treatment capabilities and geographical reach, signaling a strategic push for market dominance. The overall market concentration is influenced by substantial capital investments required for advanced infrastructure and compliance.

Europe Industrial Waste Management Market Industry Insights & Trends

The Europe industrial waste management market is poised for robust growth, driven by a confluence of economic, environmental, and technological factors. Market size, estimated at USD XXX Million in 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This expansion is primarily fueled by increasing industrial output across sectors, coupled with a growing awareness and stringent enforcement of environmental regulations. Technological disruptions are revolutionizing waste processing, with advancements in artificial intelligence for sorting, chemical recycling of complex materials, and the development of advanced waste-to-energy technologies significantly improving efficiency and resource recovery. Evolving consumer behaviors, particularly in the business-to-business (B2B) sector, are pushing for greater corporate social responsibility (CSR) and sustainable supply chain management, creating a demand for comprehensive and eco-friendly waste solutions. The transition towards a circular economy is a paramount driver, encouraging industries to view waste not as a liability but as a valuable resource. Furthermore, the increasing emphasis on reducing landfill dependency and promoting the reuse and recycling of materials are key trends shaping the market landscape. The rising cost of raw materials also incentivizes industries to invest in effective waste management solutions that facilitate material recovery and reuse.

Key Markets & Segments Leading Europe Industrial Waste Management Market

The Europe industrial waste management market is characterized by the dominance of specific segments and geographical regions, driven by unique economic and industrial profiles.

Dominant Waste Type:

- Construction and Demolition Waste: This segment consistently leads due to ongoing infrastructure development and building renovation projects across the continent. Stringent regulations on landfilling C&D waste and the growing demand for recycled construction materials are key growth enablers. Countries with significant construction activity, such as Germany, the UK, and France, exhibit high volumes of this waste stream.

- Manufacturing Waste: As Europe remains an industrial powerhouse, manufacturing waste, encompassing a broad spectrum of materials from plastics and metals to chemicals, represents a substantial and growing segment. Efforts to decarbonize manufacturing processes and implement closed-loop systems are driving innovation in this area.

- Oil and Gas Waste: While subject to cyclical fluctuations, the oil and gas sector continues to generate significant volumes of specialized waste, requiring sophisticated treatment and disposal methods. Environmental concerns and stricter regulations are pushing for more sustainable practices in this industry.

- Other Waste: This broad category includes diverse industrial by-products and specialized waste streams, each with its own market dynamics and growth potential.

Dominant Service Type:

- Recycling: The circular economy agenda has propelled recycling to the forefront of industrial waste management services. Advanced sorting technologies, material recovery facilities (MRFs), and chemical recycling processes are key to maximizing resource value.

- Incineration (Waste-to-Energy): With a focus on reducing landfill reliance and generating energy, incineration with energy recovery is a significant and growing service. This offers a dual benefit of waste volume reduction and renewable energy production, aligning with Europe's climate goals.

- Landfill: While its dominance is declining due to regulatory pressures and environmental concerns, landfilling remains a necessary service for certain residual waste streams, particularly in regions with less developed alternative infrastructure.

- Other Services: This encompasses a range of specialized services including hazardous waste treatment, industrial cleaning, waste collection and logistics, and consulting, all critical for comprehensive industrial waste management.

The dominance of specific countries is often linked to their industrial base, population density, and the strictness of their environmental policies. Germany, with its strong manufacturing sector and advanced waste management infrastructure, is a significant market. Similarly, France, the UK, and Italy represent substantial opportunities due to their industrial activities and regulatory frameworks.

Europe Industrial Waste Management Market Product Developments

Innovations in the Europe industrial waste management market are centered on enhancing efficiency, sustainability, and resource recovery. Advancements in AI-powered sorting robots are revolutionizing the separation of complex waste streams, leading to higher purity rates for recyclables. Chemical recycling technologies, such as pyrolysis and gasification, are gaining traction for their ability to break down plastics and other materials into their molecular components, enabling the creation of high-quality new products. The development of specialized treatment solutions for hazardous waste, including advanced oxidation processes and bioremediation, is crucial for environmental protection. Furthermore, the integration of digital platforms for waste tracking, reporting, and analytics is improving transparency and operational oversight. These product developments are crucial for meeting evolving regulatory requirements and achieving ambitious circular economy goals.

Challenges in the Europe Industrial Waste Management Market Market

The Europe industrial waste management market faces several critical challenges that can impede growth and operational efficiency.

- Regulatory Complexity: Navigating diverse and often stringent environmental regulations across EU member states poses a significant hurdle.

- Infrastructure Gaps: While advanced, there remain regional disparities in the availability of specialized waste treatment and recycling facilities, particularly for niche or hazardous waste streams.

- Supply Chain Volatility: Fluctuations in the commodity markets for recycled materials can impact the economic viability of recycling operations.

- Public Perception and NIMBYism: Opposition to new waste processing facilities ("Not In My Backyard") can lead to delays in project development and expansion.

- Cost Pressures: The high capital and operational costs associated with advanced waste management technologies can be a barrier for smaller enterprises.

Forces Driving Europe Industrial Waste Management Market Growth

Several powerful forces are propelling the Europe industrial waste management market forward.

- Stringent Environmental Regulations: EU and national policies mandating higher recycling rates, reduced landfill dependency, and extended producer responsibility are primary growth catalysts.

- Circular Economy Transition: The global shift towards a circular economy, emphasizing resource efficiency and waste valorization, creates significant demand for innovative waste management solutions.

- Technological Advancements: Innovations in sorting, recycling, and waste-to-energy technologies are enhancing the economic viability and environmental effectiveness of industrial waste management.

- Increasing Industrial Output: Continued industrial activity across various sectors generates a consistent stream of industrial waste, necessitating efficient management services.

- Corporate Sustainability Goals: Growing pressure from consumers and investors is driving companies to adopt more sustainable waste management practices, including the adoption of advanced recycling and waste reduction strategies.

Challenges in the Europe Industrial Waste Management Market Market

Addressing long-term growth in the Europe industrial waste management market requires overcoming persistent challenges. The ongoing need for substantial investment in advanced infrastructure, such as chemical recycling plants and specialized hazardous waste treatment facilities, remains a significant hurdle. Furthermore, the market faces the challenge of harmonizing differing national approaches to waste classification and management, which can complicate cross-border operations. Developing robust and stable markets for recycled materials is also crucial to ensure the economic sustainability of recycling initiatives. Educating and engaging industries in adopting proactive waste reduction and valorization strategies, rather than merely focusing on disposal, is another key area for development.

Emerging Opportunities in Europe Industrial Waste Management Market

The Europe industrial waste management market is rife with emerging opportunities. The burgeoning bioeconomy presents opportunities for the valorization of organic industrial waste into biofuels and biochemicals. Advances in plastics recycling, particularly chemical recycling, are opening new avenues for turning challenging plastic waste into valuable feedstocks. The growing focus on decarbonization is driving demand for carbon capture technologies integrated with waste-to-energy plants. Furthermore, the expansion of digital solutions for waste management, including IoT-enabled tracking and data analytics, offers opportunities for enhanced operational efficiency and transparency. The increasing emphasis on Extended Producer Responsibility (EPR) schemes is also creating new business models and service requirements for manufacturers.

Leading Players in the Europe Industrial Waste Management Market Sector

- Veolia

- Suez

- Biffa PLC

- Clean Harbours

- AVR

- Cleanaway Germnay

- Remondis

- Urbaser

- Prezero International

- ALBA Group

- 7 3 Other Companie

Key Milestones in Europe Industrial Waste Management Market Industry

- October 2023: Veolia opened the doors of more than 100 sites operated by the group in France. The sites include drinking water production plants, wastewater treatment plants, waste sorting centers, or energy recovery units, enabling the general public to go behind the scenes of ecological transformation. A unique opportunity to discover the group's innovative solutions and expertise in its core businesses of water, energy, and waste management.

- September 2023: In order to secure the supply of End-of-life mattress foams, Evonik entered into an agreement with Remondis Group, one of the world's most prominent recyclers. As Evonik develops its chemical recycling process to the next level, this cooperation would be beneficial for it. In the production of new mattresses, it is possible to recover core components of polyurethane foam and use them as premium-quality block-building materials with Evonik's innovative material and hydrolysis technology. The recycling process is currently being tested at a pilot plant in Hanau and will be tested at a larger demonstration plant in the future.

Strategic Outlook for Europe Industrial Waste Management Market Market

The strategic outlook for the Europe industrial waste management market is characterized by continued innovation and a strong commitment to sustainability. Growth accelerators will include the further development and scaling of advanced recycling technologies, particularly chemical recycling, to tackle complex waste streams. Strategic partnerships between waste management companies, manufacturers, and technology providers will be crucial for driving the circular economy agenda. The increasing adoption of digital transformation, including AI and IoT for waste optimization, will enhance operational efficiency and data-driven decision-making. Furthermore, a proactive approach to policy engagement and advocacy will be essential for shaping future regulations that support sustainable waste management practices and incentivize investments in green infrastructure. The market is expected to witness consolidation and specialization as key players aim to offer comprehensive, end-to-end waste management solutions.

Europe Industrial Waste Management Market Segmentation

-

1. Type

- 1.1. Construction and Demolition

- 1.2. Manufacturing Waste

- 1.3. Oil and Gas Waste

- 1.4. Other Wa

-

2. Service

- 2.1. Recycling

- 2.2. Landfill

- 2.3. Incineration

- 2.4. Other Services

Europe Industrial Waste Management Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Industrial Waste Management Market Regional Market Share

Geographic Coverage of Europe Industrial Waste Management Market

Europe Industrial Waste Management Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.26% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Construction and Demolition

- 5.1.2. Manufacturing Waste

- 5.1.3. Oil and Gas Waste

- 5.1.4. Other Wa

- 5.2. Market Analysis, Insights and Forecast - by Service

- 5.2.1. Recycling

- 5.2.2. Landfill

- 5.2.3. Incineration

- 5.2.4. Other Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Industrial Waste Management Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Construction and Demolition

- 6.1.2. Manufacturing Waste

- 6.1.3. Oil and Gas Waste

- 6.1.4. Other Wa

- 6.2. Market Analysis, Insights and Forecast - by Service

- 6.2.1. Recycling

- 6.2.2. Landfill

- 6.2.3. Incineration

- 6.2.4. Other Services

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Veolia

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Suez

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Biffa PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Clean Harbours

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 AVR

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cleanaway Germnay

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Remondis

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Urbaser

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Prezero International

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 ALBA Group**List Not Exhaustive 7 3 Other Companie

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Veolia

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Industrial Waste Management Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Industrial Waste Management Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Industrial Waste Management Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Europe Industrial Waste Management Market Volume Billion Forecast, by Type 2020 & 2033

- Table 3: Europe Industrial Waste Management Market Revenue Million Forecast, by Service 2020 & 2033

- Table 4: Europe Industrial Waste Management Market Volume Billion Forecast, by Service 2020 & 2033

- Table 5: Europe Industrial Waste Management Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Industrial Waste Management Market Volume Billion Forecast, by Region 2020 & 2033

- Table 7: Europe Industrial Waste Management Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Europe Industrial Waste Management Market Volume Billion Forecast, by Type 2020 & 2033

- Table 9: Europe Industrial Waste Management Market Revenue Million Forecast, by Service 2020 & 2033

- Table 10: Europe Industrial Waste Management Market Volume Billion Forecast, by Service 2020 & 2033

- Table 11: Europe Industrial Waste Management Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Europe Industrial Waste Management Market Volume Billion Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 15: Germany Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 17: France Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Italy Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Italy Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: Spain Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Spain Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: Netherlands Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Netherlands Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Belgium Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Belgium Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: Sweden Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Sweden Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Norway Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Norway Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Poland Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Poland Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Denmark Europe Industrial Waste Management Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Denmark Europe Industrial Waste Management Market Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Industrial Waste Management Market?

The projected CAGR is approximately 4.26%.

2. Which companies are prominent players in the Europe Industrial Waste Management Market?

Key companies in the market include Veolia, Suez, Biffa PLC, Clean Harbours, AVR, Cleanaway Germnay, Remondis, Urbaser, Prezero International, ALBA Group**List Not Exhaustive 7 3 Other Companie.

3. What are the main segments of the Europe Industrial Waste Management Market?

The market segments include Type, Service.

4. Can you provide details about the market size?

The market size is estimated to be USD 48.54 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Industrial Waste Generation; Growing Environmental Awareness; Investing in Advanced Recycling Technologies.

6. What are the notable trends driving market growth?

Germany Leads the Highest Contribution in the Waste Generation.

7. Are there any restraints impacting market growth?

Increasing Industrial Waste Generation; Growing Environmental Awareness; Investing in Advanced Recycling Technologies.

8. Can you provide examples of recent developments in the market?

October 2023: Veolia opened the doors of more than 100 sites operated by the group in France. The sites include drinking water production plants, wastewater treatment plants, waste sorting centers, or energy recovery units, enabling the general public to go behind the scenes of ecological transformation. A unique opportunity to discover the group's innovative solutions and expertise in its core businesses of water, energy, and waste management.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Industrial Waste Management Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Industrial Waste Management Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Industrial Waste Management Market?

To stay informed about further developments, trends, and reports in the Europe Industrial Waste Management Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence