Key Insights

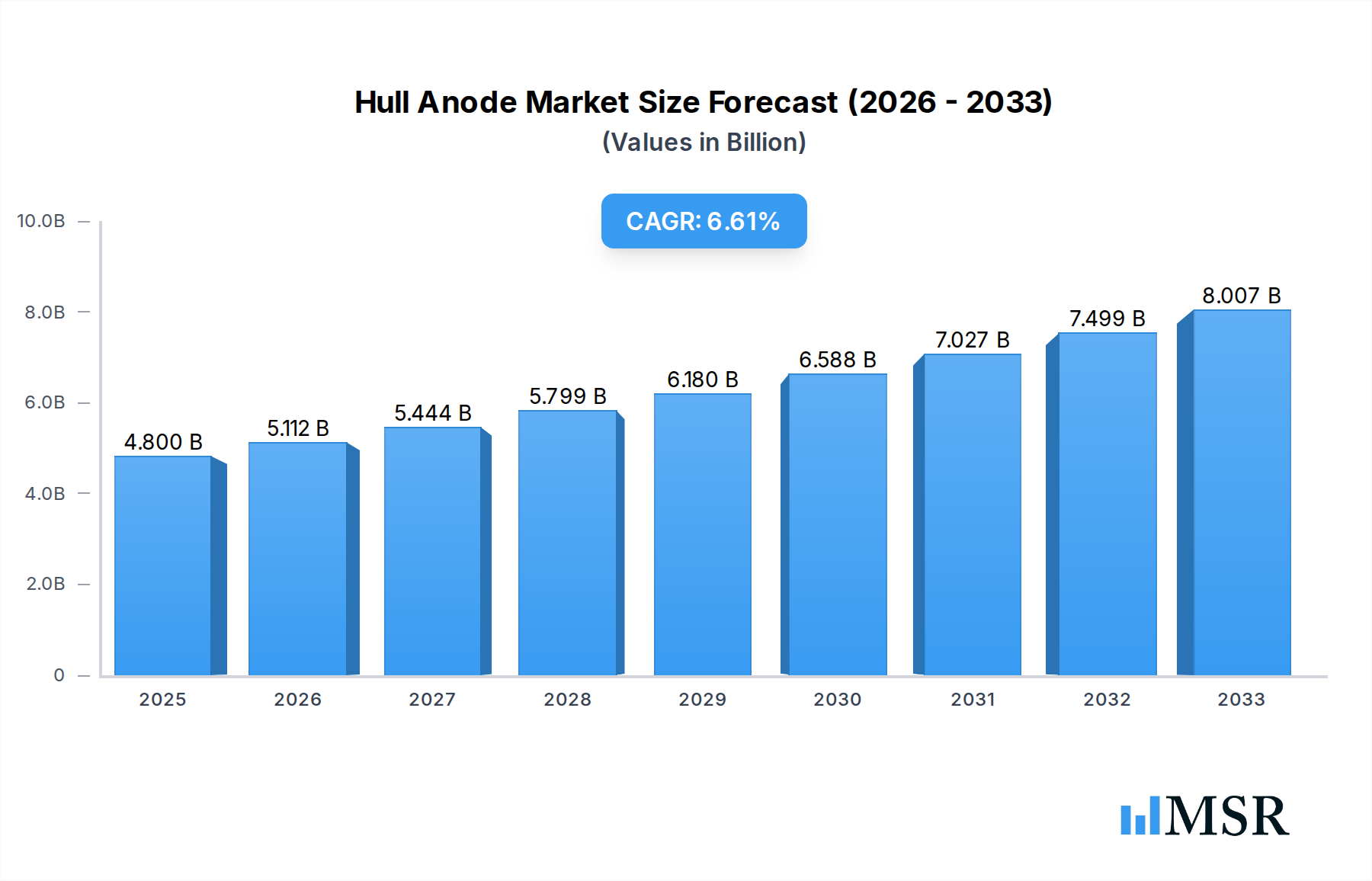

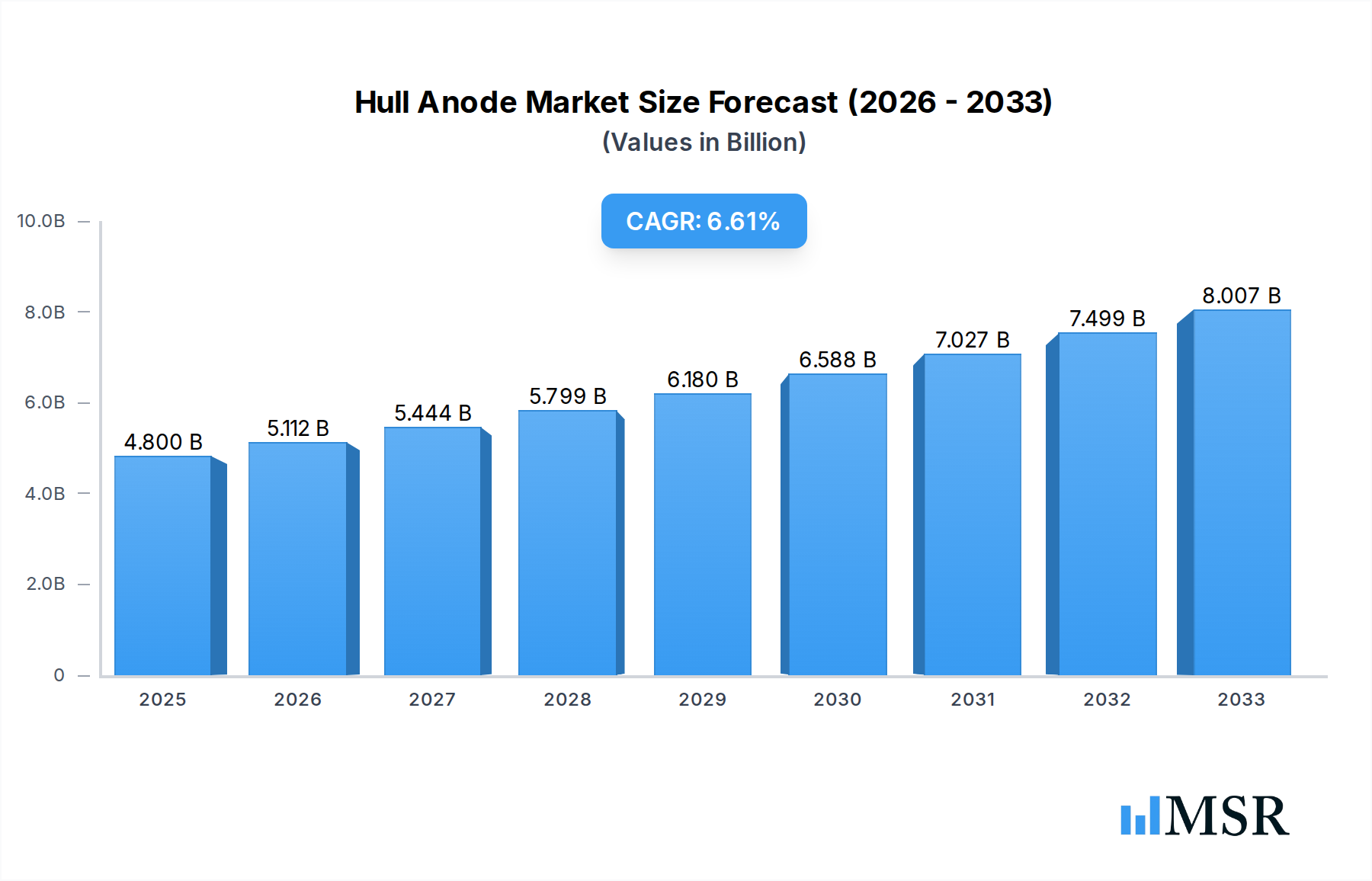

The global Hull Anode market is poised for significant growth, driven by the increasing demand for corrosion protection in the maritime industry. With a current market size of $4.8 billion in 2025 and projected to expand at a robust CAGR of 6.5% through 2033, the market indicates strong underlying growth factors. The primary drivers for this expansion include the escalating volume of global trade, leading to a higher number of container ships and bulk carriers requiring essential hull protection. Furthermore, the continued development and expansion of offshore energy infrastructure, such as oil tankers and exploration vessels, also contribute significantly to this demand. Strict maritime regulations mandating vessel integrity and extended service life further bolster the need for effective corrosion prevention solutions like hull anodes. The inherent properties of these anodes, offering sacrificial protection against the corrosive effects of saltwater, make them indispensable for maintaining the operational efficiency and longevity of marine assets.

Hull Anode Market Size (In Billion)

The market is segmented by application into Oil Tanker, Container Ship, Bulk Carrier, and Others, with Container Ships and Bulk Carriers expected to represent substantial shares due to their sheer numbers and operational cycles. By type, Aluminum Anodes and Zinc Anodes are the most prevalent, offering cost-effectiveness and high performance. Emerging trends like the development of more durable and environmentally friendly anode materials, alongside smart corrosion monitoring systems, are likely to shape the future of the market. However, challenges such as fluctuating raw material prices, particularly for metals like zinc and aluminum, and the increasing adoption of alternative anti-corrosion technologies in niche applications, could present moderate restraints. Despite these, the indispensable nature of hull anodes for safeguarding vast maritime fleets ensures sustained market expansion and innovation.

Hull Anode Company Market Share

This in-depth report provides a critical analysis of the global Hull Anode market, offering strategic insights and actionable intelligence for industry stakeholders. Covering a comprehensive study period from 2019–2033, with a base and estimated year of 2025, this report delves into market dynamics, key trends, segment dominance, product innovations, challenges, growth drivers, emerging opportunities, and the competitive landscape. Gain a competitive edge with unparalleled data and expert analysis on hull anode applications, aluminum anodes, zinc anodes, magnesium anodes, oil tanker corrosion protection, container ship cathodic protection, and bulk carrier anti-corrosion solutions.

Hull Anode Market Concentration & Dynamics

The global Hull Anode market exhibits a moderate to high concentration, driven by a few dominant players and a growing ecosystem of specialized manufacturers. Innovation is primarily fueled by the continuous need for enhanced corrosion prevention in harsh marine environments, leading to the development of advanced anode alloys and application methodologies. Regulatory frameworks, particularly those concerning environmental impact and maritime safety, play a significant role in shaping product development and market entry. The threat of substitute products, while present in the form of coatings and other protective measures, remains limited for critical sacrificial anode applications. End-user trends are strongly influenced by the economic health of the global shipping industry, vessel lifecycles, and increasing demands for extended operational efficiency and reduced maintenance costs. Mergers and acquisitions (M&A) are strategic maneuvers to consolidate market share and acquire technological expertise. Key M&A activities in the historical period (2019-2024) indicate a growing trend towards consolidation. For instance, strategic partnerships and acquisitions within the past three years have seen an average of xx deals annually, with a cumulative deal value estimated at xx billion. Leading companies such as Jennings Anodes and Galvotec have been active in expanding their geographical reach and product portfolios through targeted acquisitions.

Hull Anode Industry Insights & Trends

The Hull Anode industry is poised for substantial growth, projected to reach a market size of xx billion by 2033, with a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025–2033). This expansion is fundamentally driven by the escalating demand for effective and reliable corrosion protection solutions across the maritime sector. The increasing global trade volumes necessitate a larger fleet of vessels, including oil tankers, container ships, and bulk carriers, all of which require robust hull anode systems to prevent galvanic corrosion and extend their operational lifespan. Technological disruptions are a key factor, with ongoing research and development in alloy compositions yielding anodes with higher efficiency, longer service life, and improved environmental profiles. For example, advancements in aluminum anode alloys are enabling greater protection in varying salinity levels. Evolving consumer behaviors, primarily dictated by stringent maritime regulations and a growing emphasis on sustainability, are pushing manufacturers to develop eco-friendly and high-performance anode solutions. The increasing sophistication of vessel maintenance strategies, which prioritize preventative measures like effective cathodic protection, further fuels market demand. The historical period (2019–2024) witnessed a steady market growth of approximately xx% annually, setting a strong foundation for future expansion. The demand for specialized anodes for offshore structures and renewable energy installations is also emerging as a significant growth driver. The global market size for hull anodes in 2025 is estimated at xx billion.

Key Markets & Segments Leading Hull Anode

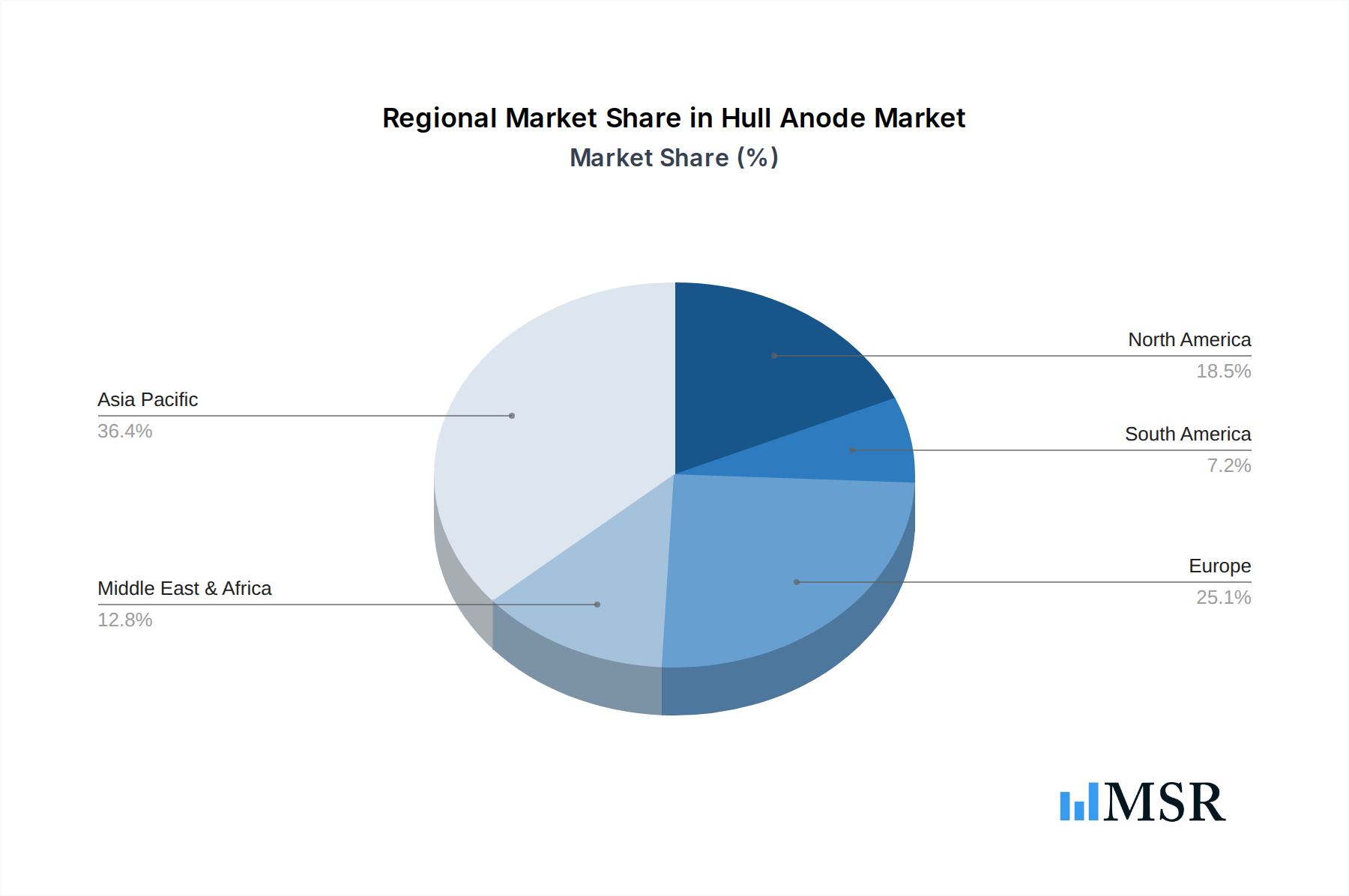

Asia Pacific stands out as the dominant region in the global Hull Anode market, driven by its colossal shipbuilding industry and extensive maritime trade routes. Countries like China, South Korea, and Japan are at the forefront of both new vessel construction and the maintenance of existing fleets, creating a substantial and consistent demand for all types of hull anodes.

Application Dominance:

- Container Ships: This segment leads due to the sheer volume of container vessels deployed globally and their continuous operation, requiring frequent and effective corrosion protection. Economic growth and global supply chain demands directly influence the expansion and maintenance needs of container fleets.

- Oil Tankers: As a critical component of global energy transportation, the large number of oil tankers necessitates robust and long-lasting anode systems to ensure operational integrity and prevent costly damage from corrosion. Infrastructure development supporting offshore oil exploration further amplifies this demand.

- Bulk Carriers: The increasing demand for raw materials and commodities worldwide fuels the expansion of bulk carrier fleets, making this segment a significant contributor to hull anode consumption.

- Others: This includes specialized vessels, offshore platforms, and naval fleets, each with unique corrosion protection requirements.

Type Dominance:

- Aluminum Anodes: These are increasingly favored for their high efficiency, lighter weight compared to zinc, and excellent performance in both saltwater and brackish water. Their cost-effectiveness and long service life make them a preferred choice for new builds and retrofits.

- Zinc Anodes: Historically a staple, zinc anodes continue to hold significant market share due to their proven reliability and widespread availability, particularly for applications requiring a more robust sacrificial action.

- Magnesium Anodes: While less prevalent in large-scale hull applications compared to aluminum and zinc, magnesium anodes find niche applications where higher driving potentials are required, such as in freshwater environments or for specific components.

The dominance of these segments is underpinned by factors such as robust economic growth in the Asia Pacific region, significant investments in port infrastructure, and favorable government policies supporting maritime trade and shipbuilding. The total market size within these dominant segments is projected to reach xx billion by 2033.

Hull Anode Product Developments

Recent Hull Anode product developments are focused on enhancing efficiency, longevity, and environmental sustainability. Innovations in alloy formulations for aluminum and zinc anodes are yielding improved sacrificial rates and extended service life, reducing the frequency of replacement and lowering total cost of ownership. Manufacturers are also developing customized anode solutions tailored to specific vessel types and operational conditions, optimizing corrosion protection for diverse marine environments. The integration of advanced monitoring systems with anode deployments is another significant trend, allowing for real-time assessment of anode consumption and proactive maintenance scheduling. These technological advancements are crucial for maintaining vessel integrity and minimizing operational downtime, contributing to a competitive edge in the market.

Challenges in the Hull Anode Market

The Hull Anode market faces several challenges that can impede growth and profitability. Regulatory hurdles, particularly concerning the environmental impact of anode materials and their disposal, can lead to increased compliance costs and product development complexities. Fluctuations in the prices of raw materials, such as aluminum and zinc, directly impact manufacturing costs and can create pricing volatility. Intense competition from established players and emerging manufacturers also puts pressure on profit margins. Furthermore, the long service life of high-quality anodes means that replacement cycles can be extended, leading to slower demand growth for new installations. Supply chain disruptions, as witnessed in recent global events, can also affect the availability and cost of raw materials and finished products, impacting market stability.

Forces Driving Hull Anode Growth

Several powerful forces are propelling the growth of the Hull Anode market. The continuous expansion of global maritime trade and the increasing size and complexity of the global shipping fleet are fundamental drivers. Escalating demand for enhanced vessel longevity and reduced maintenance expenses compels ship owners and operators to invest in effective corrosion protection systems like hull anodes. Stringent international maritime regulations aimed at improving safety and environmental protection also mandate the use of reliable corrosion prevention technologies. Technological advancements in anode materials and manufacturing processes are leading to more efficient, durable, and cost-effective solutions, further stimulating demand. The growing focus on extending the operational lifespan of vessels translates directly into a higher demand for robust cathodic protection.

Challenges in the Hull Anode Market

Long-term growth catalysts for the Hull Anode market lie in continued innovation and strategic market expansion. The development of novel anode materials with superior performance characteristics, such as enhanced resistance to fouling or improved efficiency in challenging water conditions, will unlock new market opportunities. Strategic partnerships and collaborations between anode manufacturers and shipyards, classification societies, and research institutions can accelerate the adoption of advanced solutions. Furthermore, expanding into emerging maritime markets and catering to the growing needs of offshore renewable energy installations represent significant avenues for sustained growth. The increasing emphasis on sustainability within the maritime industry will also drive demand for anodes with a reduced environmental footprint.

Emerging Opportunities in Hull Anode

Emerging opportunities in the Hull Anode market are abundant, driven by evolving industry needs and technological advancements. The growing offshore wind energy sector presents a significant opportunity, with wind turbine foundations and substructures requiring robust cathodic protection systems. The increasing demand for smart shipping and the integration of IoT devices offer opportunities for anodes equipped with sensors for real-time monitoring and predictive maintenance. Furthermore, the development of eco-friendly anode alternatives with reduced environmental impact is a growing consumer preference. The expansion of specialized anode applications for subsea pipelines, offshore platforms, and other marine infrastructure also represents a promising growth area.

Leading Players in the Hull Anode Sector

- Jennings Anodes

- Sea Shield Marine Products

- Galvotec

- Farwest Corrosion

- Skarpenord Corrosion

- Cathwell

- LIG International Marine Group

- Deyuan Marine Fitting

- ZINETI

- Corrosion Group

- BAC Corrosion Control

- M&M Industries

- Reliance Anodes

- Shanghai Chuhai Industrial

- TopCorr

Key Milestones in Hull Anode Industry

- 2019: Introduction of advanced aluminum anode alloys with extended service life by Jennings Anodes, improving efficiency for container ships.

- 2020: Galvotec expands its product line with new zinc anode formulations for increased effectiveness in varying water salinities.

- 2021: Farwest Corrosion partners with a major shipyard for the development of integrated cathodic protection systems for a fleet of new bulk carriers.

- 2022: Skarpenord Corrosion launches an innovative monitoring system for hull anodes, enabling real-time performance tracking.

- 2023: Cathwell introduces eco-friendly anode options, meeting growing environmental regulations and demands.

- 2024: LIG International Marine Group announces a strategic acquisition to strengthen its presence in the Asian market.

- 2025 (Estimated): Forecasted introduction of novel magnesium anode alloys with enhanced driving potential for specialized applications.

Strategic Outlook for Hull Anode Market

The strategic outlook for the Hull Anode market is overwhelmingly positive, characterized by sustained growth and innovation. Key accelerators include the ongoing expansion of the global maritime fleet, the persistent need for effective corrosion prevention to ensure vessel integrity and longevity, and the increasing adoption of advanced anode technologies offering superior performance and cost-efficiency. Strategic opportunities lie in leveraging the burgeoning offshore renewable energy sector, developing smart anodes for integrated monitoring, and focusing on environmentally sustainable product offerings. Collaborations with shipyards, regulatory bodies, and research institutions will be crucial for driving product adoption and shaping future market trends, ensuring continued market expansion and profitability.

Hull Anode Segmentation

-

1. Application

- 1.1. Oil Tanker

- 1.2. Container Ship

- 1.3. Bulk Carrier

- 1.4. Others

-

2. Type

- 2.1. Aluminum Anode

- 2.2. Zinc Anode

- 2.3. Magnesium Anode

Hull Anode Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Hull Anode Regional Market Share

Geographic Coverage of Hull Anode

Hull Anode REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Hull Anode Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Oil Tanker

- 5.1.2. Container Ship

- 5.1.3. Bulk Carrier

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Aluminum Anode

- 5.2.2. Zinc Anode

- 5.2.3. Magnesium Anode

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Hull Anode Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Oil Tanker

- 6.1.2. Container Ship

- 6.1.3. Bulk Carrier

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Aluminum Anode

- 6.2.2. Zinc Anode

- 6.2.3. Magnesium Anode

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Hull Anode Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Oil Tanker

- 7.1.2. Container Ship

- 7.1.3. Bulk Carrier

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Aluminum Anode

- 7.2.2. Zinc Anode

- 7.2.3. Magnesium Anode

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Hull Anode Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Oil Tanker

- 8.1.2. Container Ship

- 8.1.3. Bulk Carrier

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Aluminum Anode

- 8.2.2. Zinc Anode

- 8.2.3. Magnesium Anode

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Hull Anode Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Oil Tanker

- 9.1.2. Container Ship

- 9.1.3. Bulk Carrier

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Aluminum Anode

- 9.2.2. Zinc Anode

- 9.2.3. Magnesium Anode

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Hull Anode Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Oil Tanker

- 10.1.2. Container Ship

- 10.1.3. Bulk Carrier

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Aluminum Anode

- 10.2.2. Zinc Anode

- 10.2.3. Magnesium Anode

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Jennings Anodes

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Sea Shield Marine Products

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Galvotec

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Farwest Corrosion

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Skarpenord Corrosion

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Cathwell

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 LIG International Marine Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Deyuan Marine Fitting

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 ZINETI

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Corrosion Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 BAC Corrosion Control

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 M&M Industries

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Reliance Anodes

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shanghai Chuhai Industrial

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 TopCorr

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Jennings Anodes

List of Figures

- Figure 1: Global Hull Anode Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Hull Anode Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Hull Anode Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Hull Anode Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Hull Anode Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Hull Anode Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Hull Anode Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Hull Anode Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Hull Anode Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Hull Anode Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Hull Anode Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Hull Anode Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Hull Anode Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Hull Anode Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Hull Anode Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Hull Anode Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Hull Anode Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Hull Anode Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Hull Anode Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Hull Anode Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Hull Anode Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Hull Anode Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Hull Anode Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Hull Anode Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Hull Anode Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Hull Anode Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Hull Anode Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Hull Anode Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Hull Anode Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Hull Anode Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Hull Anode Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hull Anode Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Hull Anode Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Hull Anode Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Hull Anode Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Hull Anode Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Hull Anode Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Hull Anode Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Hull Anode Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Hull Anode Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Hull Anode Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Hull Anode Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Hull Anode Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Hull Anode Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Hull Anode Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Hull Anode Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Hull Anode Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Hull Anode Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Hull Anode Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Hull Anode Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hull Anode?

The projected CAGR is approximately 6.5%.

2. Which companies are prominent players in the Hull Anode?

Key companies in the market include Jennings Anodes, Sea Shield Marine Products, Galvotec, Farwest Corrosion, Skarpenord Corrosion, Cathwell, LIG International Marine Group, Deyuan Marine Fitting, ZINETI, Corrosion Group, BAC Corrosion Control, M&M Industries, Reliance Anodes, Shanghai Chuhai Industrial, TopCorr.

3. What are the main segments of the Hull Anode?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hull Anode," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hull Anode report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hull Anode?

To stay informed about further developments, trends, and reports in the Hull Anode, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence