Key Insights

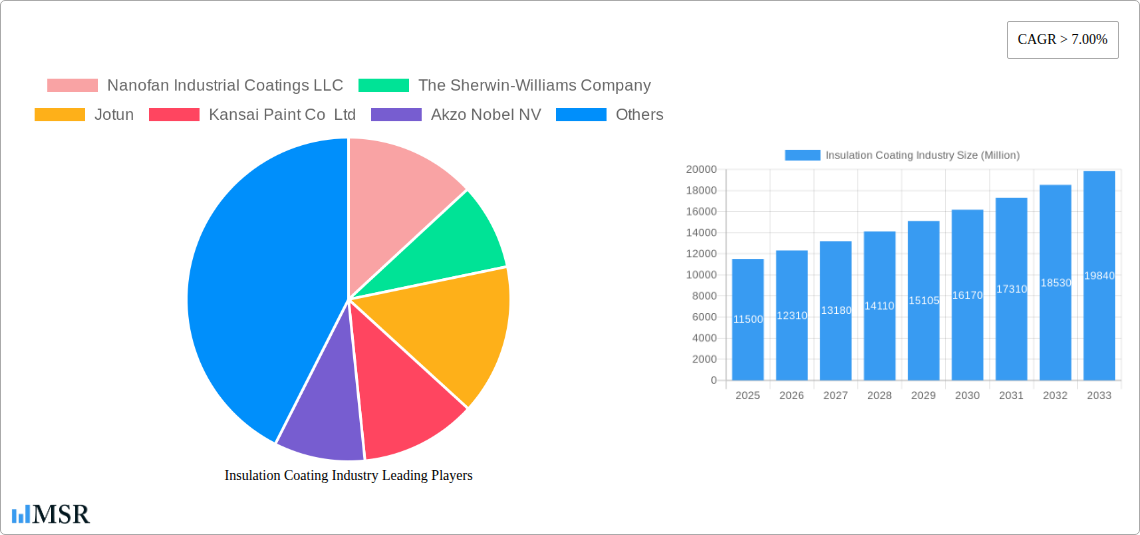

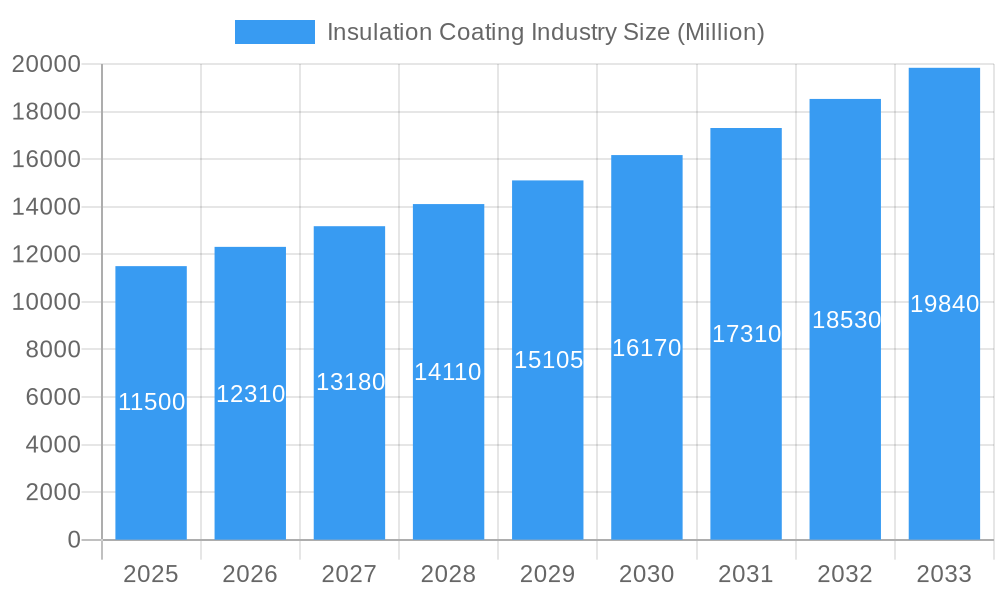

The Insulation Coating market is poised for significant expansion, projected to reach a valuation of approximately $11,500 million by the base year 2025, with a robust Compound Annual Growth Rate (CAGR) exceeding 7.00% throughout the forecast period of 2025-2033. This impressive growth trajectory is primarily fueled by an escalating demand for energy efficiency solutions across a multitude of industries. The inherent ability of insulation coatings to reduce heat transfer, thereby minimizing energy consumption for heating and cooling, makes them indispensable in a world increasingly focused on sustainability and operational cost reduction. Key drivers include stringent environmental regulations promoting energy conservation, rising global energy prices, and a growing awareness among end-users regarding the long-term economic and environmental benefits of investing in high-performance insulation. Furthermore, advancements in coating formulations, leading to enhanced durability, application ease, and superior thermal resistance, are continuously expanding the market's potential.

Insulation Coating Industry Market Size (In Billion)

The market's diversification across various product types and end-user industries underscores its widespread applicability. Acrylic, Epoxy, and Polyurethane coatings represent significant segments due to their versatility and proven performance. However, specialized materials like Yttria Stabilized Zirconia are gaining traction in high-temperature applications. The Chemical and Petrochemical, Oil and Gas, Aerospace, Construction, and Automotive and Marine sectors are the primary beneficiaries and consumers of these advanced coatings. Within these sectors, the persistent need to protect infrastructure from extreme temperatures, corrosive environments, and to improve operational efficiency drives innovation and adoption. Emerging trends indicate a stronger focus on eco-friendly and low-VOC (Volatile Organic Compound) insulation coatings, responding to environmental concerns and regulatory pressures. While the market exhibits strong growth, potential restraints such as the high initial cost of specialized coatings and the availability of alternative insulation materials in certain applications need to be strategically addressed by market participants through value proposition enhancement and targeted marketing efforts.

Insulation Coating Industry Company Market Share

Global Insulation Coating Industry Report: Market Size, Trends, and Forecast (2019-2033)

This comprehensive report offers an in-depth analysis of the global insulation coating industry, a critical sector driven by demand for energy efficiency, asset protection, and advanced material performance. The study covers the period from 2019 to 2033, with the base year and estimated year as 2025, and a forecast period from 2025 to 2033. Historical data from 2019 to 2024 is also analyzed. We explore key segments including Acrylic, Epoxy, Polyurethane, Yttria Stabilized Zirconia, and Others, serving vital end-user industries such as Chemical and Petrochemical, Oil and Gas, Aerospace, Construction, Automotive and Marine, and Others. Discover actionable insights, market dynamics, and growth strategies shaping the future of insulation coatings.

Insulation Coating Industry Market Concentration & Dynamics

The global insulation coating industry exhibits a moderate to high market concentration, with a few dominant players holding significant market share, alongside a growing number of niche manufacturers specializing in advanced formulations. Innovation is a key differentiator, fueled by substantial R&D investments from leading companies. The innovation ecosystem thrives on collaborations between material science firms, research institutions, and end-user industries seeking tailored solutions for extreme temperature resistance, corrosion prevention, and enhanced energy conservation. Regulatory frameworks, particularly those promoting energy efficiency standards and environmental protection, play a crucial role in shaping product development and market penetration. The threat of substitute products, such as traditional insulation materials, is diminishing as the performance benefits and lifecycle cost savings of advanced insulation coatings become increasingly evident. End-user trends are leaning towards high-performance, durable, and environmentally friendly coatings. Merger and acquisition (M&A) activities are present, with strategic acquisitions aimed at expanding product portfolios, geographical reach, and technological capabilities. For instance, recent years have seen approximately 5-10 significant M&A deals annually within the broader coatings sector, with insulation coatings being a strategic focus for several major players.

- Market Share Dominance: Top players collectively account for an estimated 60-70% of the global market revenue.

- Innovation Drivers: Focus on low VOC, high thermal resistance, and self-healing coatings.

- Regulatory Impact: Growing emphasis on eco-friendly formulations and energy-saving mandates.

- Substitute Threat: Moderate, with advanced coatings offering superior performance.

Insulation Coating Industry Industry Insights & Trends

The insulation coating industry is poised for significant growth, projected to reach a global market size of USD 18,500 Million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 7.8% during the forecast period of 2025–2033. This robust expansion is primarily driven by an escalating global focus on energy conservation and operational efficiency across various industrial sectors. The imperative to reduce greenhouse gas emissions and combat climate change is compelling industries to adopt advanced insulation solutions that minimize heat loss and gain, thereby lowering energy consumption. Technological disruptions are continuously redefining the landscape of insulation coatings. The development of nanotechnology-based coatings, offering superior thermal resistance and durability, and intumescent coatings for fire protection, are gaining traction. Furthermore, the integration of smart functionalities, such as self-monitoring and self-healing capabilities, represents a significant future trend. Evolving consumer behaviors are also influencing the market; end-users are increasingly prioritizing long-term cost savings, reduced environmental impact, and enhanced asset lifespan, making high-performance insulation coatings an attractive investment. The chemical and petrochemical industry and the oil and gas sector remain key consumers, demanding robust protection against extreme temperatures and corrosive environments. The aerospace sector seeks lightweight, high-performance insulation for thermal management, while the construction industry is adopting these coatings for energy-efficient buildings. The automotive and marine sectors are also witnessing growing adoption for improved fuel efficiency and component protection.

Key Markets & Segments Leading Insulation Coating Industry

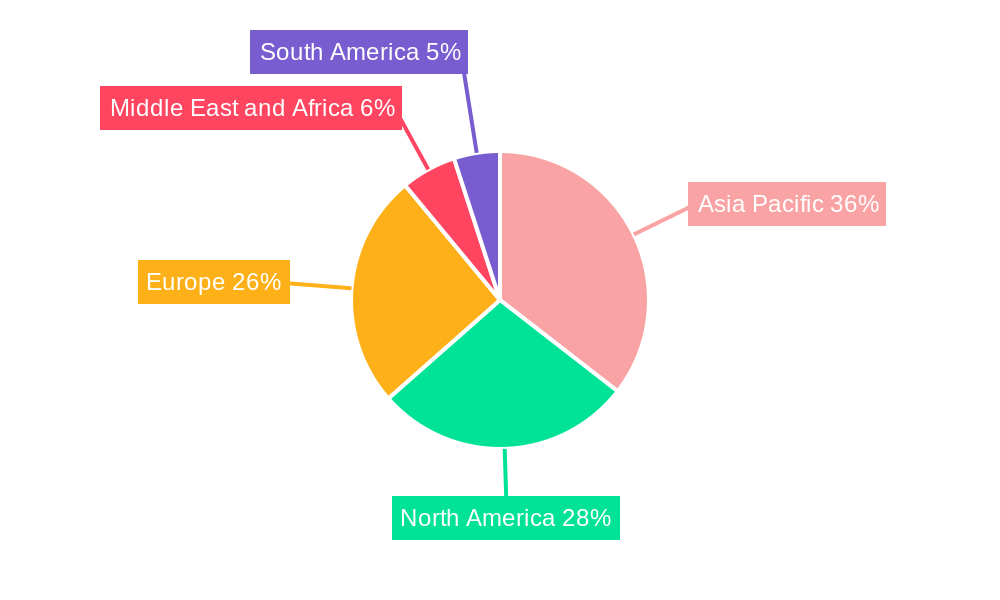

The Asia Pacific region is emerging as the dominant market for insulation coatings, driven by rapid industrialization, burgeoning infrastructure development, and increasing investments in energy-efficient technologies. Countries like China and India are at the forefront, with substantial growth fueled by government initiatives promoting sustainable construction and industrial expansion. Within the Product Type segment, Epoxy coatings continue to hold a significant market share due to their excellent adhesion, chemical resistance, and mechanical strength, making them ideal for demanding industrial applications. However, Polyurethane coatings are witnessing robust growth owing to their superior flexibility, thermal insulation properties, and ease of application. Acrylic coatings are also gaining prominence, particularly in construction and automotive sectors, due to their cost-effectiveness and good weatherability. The niche but high-growth segment of Yttria Stabilized Zirconia (YSZ) coatings is crucial for high-temperature applications in aerospace and industrial furnaces, showcasing exceptional thermal barrier properties.

- Dominant Region: Asia Pacific – driven by rapid industrial growth, construction boom, and energy efficiency mandates.

- Key Drivers: Government support for sustainable development, increasing manufacturing output, and urbanization.

- Dominant Product Type: Epoxy and Polyurethane coatings – valued for their durability, chemical resistance, and thermal performance.

- Drivers: Wide range of applications in heavy industries and infrastructure, superior protective qualities.

- Dominant End-user Industry: Chemical and Petrochemical, Oil and Gas – requiring protection against extreme temperatures and corrosive environments.

- Drivers: Strict safety regulations, need for asset integrity and operational efficiency, high-temperature processes.

Insulation Coating Industry Product Developments

Product development in the insulation coating industry is characterized by a strong focus on enhancing performance and sustainability. Innovations are centered on creating coatings with superior thermal insulation capabilities, advanced corrosion resistance, and improved fire retardancy. Nanomaterials are being integrated to create coatings with self-healing properties and exceptional durability. For instance, the development of low-VOC (Volatile Organic Compound) formulations is a significant trend, addressing environmental concerns and regulatory requirements. New applications are emerging in areas such as cryogenic insulation, industrial equipment protection, and energy-efficient building envelopes. The market relevance of these advancements is high, as they directly address the growing demand for energy savings, extended asset lifespan, and improved safety standards across all end-user industries.

Challenges in the Insulation Coating Industry Market

Despite the positive outlook, the insulation coating industry faces several challenges. High raw material costs, particularly for specialized resins and additives, can impact profitability and pricing strategies. Stringent environmental regulations regarding VOC emissions and the disposal of hazardous materials necessitate continuous product reformulation and investment in cleaner production processes. Supply chain disruptions, as witnessed in recent years, can lead to production delays and increased costs. Furthermore, the initial cost of high-performance insulation coatings can be a barrier for some smaller enterprises or in price-sensitive markets, requiring strong emphasis on demonstrating long-term return on investment.

- Raw Material Price Volatility: Fluctuations impact production costs.

- Regulatory Compliance: Evolving environmental standards demand continuous adaptation.

- Supply Chain Vulnerabilities: Global events can disrupt material availability.

- Perceived High Initial Cost: Educational efforts are needed to highlight lifecycle benefits.

Forces Driving Insulation Coating Industry Growth

Several powerful forces are propelling the growth of the insulation coating industry. The escalating global emphasis on energy efficiency and sustainability is a primary driver, pushing industries to adopt solutions that reduce energy consumption and operational costs. Increasing infrastructure development in emerging economies, coupled with the need to protect these assets from harsh environmental conditions, is creating substantial demand. Technological advancements in material science, particularly in nanotechnology and advanced polymer chemistry, are leading to the development of more effective and specialized insulation coatings. Furthermore, stringent safety regulations in sectors like oil and gas and aerospace mandate the use of high-performance coatings for asset protection and personnel safety.

Challenges in the Insulation Coating Industry Market

The long-term growth catalysts for the insulation coating industry are deeply rooted in continuous innovation and strategic market expansion. The development of next-generation insulation coatings with enhanced thermal performance, fire resistance, and self-cleaning properties will be crucial. Strategic partnerships and collaborations between coating manufacturers, material suppliers, and end-users will foster the development of customized solutions and accelerate market penetration. Exploring and tapping into emerging markets, particularly in regions undergoing rapid industrialization and infrastructure upgrades, presents significant growth potential. The ongoing shift towards a circular economy and the development of eco-friendly and recyclable insulation coatings will also be key long-term drivers.

Emerging Opportunities in Insulation Coating Industry

The insulation coating industry is ripe with emerging opportunities. The growing demand for smart coatings with embedded functionalities like temperature sensing and structural health monitoring presents a significant avenue for innovation. The renewable energy sector, including wind turbines and solar panels, requires specialized coatings for protection against harsh weather and environmental degradation, creating new application areas. The increasing focus on green building initiatives worldwide is driving demand for energy-efficient construction materials, including insulation coatings for buildings. Furthermore, the development of bio-based and sustainable insulation coatings is an emerging trend that aligns with global environmental consciousness and offers a competitive edge.

Leading Players in the Insulation Coating Industry Sector

- Nanofan Industrial Coatings LLC

- The Sherwin-Williams Company

- Jotun

- Kansai Paint Co Ltd

- Akzo Nobel NV

- Mascoat

- PPG Industries Inc

- SK FORMULATIONS INDIA PVT LTD

- Nippon Paint

- Carboline

- Ugam Chemicals

- Synavax

Key Milestones in Insulation Coating Industry Industry

- 2019: Introduction of advanced nano-ceramic insulation coatings with enhanced thermal reflectivity.

- 2020: Increased adoption of low-VOC and water-based insulation coating formulations driven by environmental regulations.

- 2021: Significant investment in R&D for self-healing and fire-retardant insulation coatings by major players.

- 2022: Growing demand for high-temperature insulation coatings for industrial furnace and aerospace applications.

- 2023: Emergence of smart insulation coatings with integrated monitoring capabilities.

- 2024: Expansion of insulation coating applications in the renewable energy sector.

Strategic Outlook for Insulation Coating Industry Market

The strategic outlook for the insulation coating industry is exceptionally positive, driven by sustained global demand for energy efficiency and asset protection. The market will continue to witness a strong focus on product innovation, particularly in developing coatings with superior thermal performance, enhanced durability, and environmental sustainability. Key growth accelerators will include strategic expansion into emerging economies, the development of specialized coatings for niche applications, and a continued emphasis on R&D to integrate advanced functionalities. Collaborations between manufacturers and end-users will be crucial in tailoring solutions to meet evolving industry needs, ensuring the insulation coating industry remains a vital component of global industrial and infrastructure development for years to come.

Insulation Coating Industry Segmentation

-

1. Product Type

- 1.1. Acrylic

- 1.2. Epoxy

- 1.3. Polyurethane

- 1.4. Yttria Stabilized Zirconia

- 1.5. Others

-

2. End-user Industry

- 2.1. Chemical and Petrochemical

- 2.2. Oil and Gas

- 2.3. Aerospace

- 2.4. Construction

- 2.5. Automotive and Marine

- 2.6. Others

Insulation Coating Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Insulation Coating Industry Regional Market Share

Geographic Coverage of Insulation Coating Industry

Insulation Coating Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Acrylic

- 5.1.2. Epoxy

- 5.1.3. Polyurethane

- 5.1.4. Yttria Stabilized Zirconia

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Chemical and Petrochemical

- 5.2.2. Oil and Gas

- 5.2.3. Aerospace

- 5.2.4. Construction

- 5.2.5. Automotive and Marine

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Insulation Coating Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Acrylic

- 6.1.2. Epoxy

- 6.1.3. Polyurethane

- 6.1.4. Yttria Stabilized Zirconia

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Chemical and Petrochemical

- 6.2.2. Oil and Gas

- 6.2.3. Aerospace

- 6.2.4. Construction

- 6.2.5. Automotive and Marine

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Asia Pacific Insulation Coating Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Acrylic

- 7.1.2. Epoxy

- 7.1.3. Polyurethane

- 7.1.4. Yttria Stabilized Zirconia

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Chemical and Petrochemical

- 7.2.2. Oil and Gas

- 7.2.3. Aerospace

- 7.2.4. Construction

- 7.2.5. Automotive and Marine

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. North America Insulation Coating Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Acrylic

- 8.1.2. Epoxy

- 8.1.3. Polyurethane

- 8.1.4. Yttria Stabilized Zirconia

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Chemical and Petrochemical

- 8.2.2. Oil and Gas

- 8.2.3. Aerospace

- 8.2.4. Construction

- 8.2.5. Automotive and Marine

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Europe Insulation Coating Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Acrylic

- 9.1.2. Epoxy

- 9.1.3. Polyurethane

- 9.1.4. Yttria Stabilized Zirconia

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Chemical and Petrochemical

- 9.2.2. Oil and Gas

- 9.2.3. Aerospace

- 9.2.4. Construction

- 9.2.5. Automotive and Marine

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Insulation Coating Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Acrylic

- 10.1.2. Epoxy

- 10.1.3. Polyurethane

- 10.1.4. Yttria Stabilized Zirconia

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Chemical and Petrochemical

- 10.2.2. Oil and Gas

- 10.2.3. Aerospace

- 10.2.4. Construction

- 10.2.5. Automotive and Marine

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Insulation Coating Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Acrylic

- 11.1.2. Epoxy

- 11.1.3. Polyurethane

- 11.1.4. Yttria Stabilized Zirconia

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by End-user Industry

- 11.2.1. Chemical and Petrochemical

- 11.2.2. Oil and Gas

- 11.2.3. Aerospace

- 11.2.4. Construction

- 11.2.5. Automotive and Marine

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Nanofan Industrial Coatings LLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 The Sherwin-Williams Company

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Jotun

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Kansai Paint Co Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Akzo Nobel NV

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Mascoat

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 PPG Industries Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 SK FORMULATIONS INDIA PVT LTD

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nippon Paint

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Carboline

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ugam Chemicals*List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Synavax

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Nanofan Industrial Coatings LLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Insulation Coating Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Insulation Coating Industry Volume Breakdown (liter , %) by Region 2025 & 2033

- Figure 3: Asia Pacific Insulation Coating Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 4: Asia Pacific Insulation Coating Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 5: Asia Pacific Insulation Coating Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: Asia Pacific Insulation Coating Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: Asia Pacific Insulation Coating Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 8: Asia Pacific Insulation Coating Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 9: Asia Pacific Insulation Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 10: Asia Pacific Insulation Coating Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 11: Asia Pacific Insulation Coating Industry Revenue (billion), by Country 2025 & 2033

- Figure 12: Asia Pacific Insulation Coating Industry Volume (liter ), by Country 2025 & 2033

- Figure 13: Asia Pacific Insulation Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Insulation Coating Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: North America Insulation Coating Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 16: North America Insulation Coating Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 17: North America Insulation Coating Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: North America Insulation Coating Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 19: North America Insulation Coating Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 20: North America Insulation Coating Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 21: North America Insulation Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 22: North America Insulation Coating Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 23: North America Insulation Coating Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: North America Insulation Coating Industry Volume (liter ), by Country 2025 & 2033

- Figure 25: North America Insulation Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Insulation Coating Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Insulation Coating Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 28: Europe Insulation Coating Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 29: Europe Insulation Coating Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Europe Insulation Coating Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 31: Europe Insulation Coating Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 32: Europe Insulation Coating Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 33: Europe Insulation Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 34: Europe Insulation Coating Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 35: Europe Insulation Coating Industry Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Insulation Coating Industry Volume (liter ), by Country 2025 & 2033

- Figure 37: Europe Insulation Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Insulation Coating Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: South America Insulation Coating Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 40: South America Insulation Coating Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 41: South America Insulation Coating Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 42: South America Insulation Coating Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 43: South America Insulation Coating Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 44: South America Insulation Coating Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 45: South America Insulation Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 46: South America Insulation Coating Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 47: South America Insulation Coating Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: South America Insulation Coating Industry Volume (liter ), by Country 2025 & 2033

- Figure 49: South America Insulation Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Insulation Coating Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Insulation Coating Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 52: Middle East and Africa Insulation Coating Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 53: Middle East and Africa Insulation Coating Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 54: Middle East and Africa Insulation Coating Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 55: Middle East and Africa Insulation Coating Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 56: Middle East and Africa Insulation Coating Industry Volume (liter ), by End-user Industry 2025 & 2033

- Figure 57: Middle East and Africa Insulation Coating Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 58: Middle East and Africa Insulation Coating Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 59: Middle East and Africa Insulation Coating Industry Revenue (billion), by Country 2025 & 2033

- Figure 60: Middle East and Africa Insulation Coating Industry Volume (liter ), by Country 2025 & 2033

- Figure 61: Middle East and Africa Insulation Coating Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Insulation Coating Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Insulation Coating Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Insulation Coating Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 3: Global Insulation Coating Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Insulation Coating Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 5: Global Insulation Coating Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Insulation Coating Industry Volume liter Forecast, by Region 2020 & 2033

- Table 7: Global Insulation Coating Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Insulation Coating Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 9: Global Insulation Coating Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 10: Global Insulation Coating Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Insulation Coating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Insulation Coating Industry Volume liter Forecast, by Country 2020 & 2033

- Table 13: China Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: China Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 15: India Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: India Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 17: Japan Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Japan Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 19: South Korea Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: South Korea Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 23: Global Insulation Coating Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 24: Global Insulation Coating Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 25: Global Insulation Coating Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 26: Global Insulation Coating Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 27: Global Insulation Coating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Global Insulation Coating Industry Volume liter Forecast, by Country 2020 & 2033

- Table 29: United States Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: United States Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 31: Canada Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Canada Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 33: Mexico Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Mexico Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 35: Global Insulation Coating Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 36: Global Insulation Coating Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 37: Global Insulation Coating Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Insulation Coating Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 39: Global Insulation Coating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: Global Insulation Coating Industry Volume liter Forecast, by Country 2020 & 2033

- Table 41: Germany Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Germany Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 43: United Kingdom Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: United Kingdom Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 45: France Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: France Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 47: Italy Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Italy Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 49: Rest of Europe Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Rest of Europe Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 51: Global Insulation Coating Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 52: Global Insulation Coating Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 53: Global Insulation Coating Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 54: Global Insulation Coating Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 55: Global Insulation Coating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 56: Global Insulation Coating Industry Volume liter Forecast, by Country 2020 & 2033

- Table 57: Brazil Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Brazil Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 59: Argentina Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Argentina Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 61: Rest of South America Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of South America Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 63: Global Insulation Coating Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 64: Global Insulation Coating Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 65: Global Insulation Coating Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 66: Global Insulation Coating Industry Volume liter Forecast, by End-user Industry 2020 & 2033

- Table 67: Global Insulation Coating Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 68: Global Insulation Coating Industry Volume liter Forecast, by Country 2020 & 2033

- Table 69: Saudi Arabia Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: Saudi Arabia Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 71: South Africa Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: South Africa Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 73: Rest of Middle East and Africa Insulation Coating Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: Rest of Middle East and Africa Insulation Coating Industry Volume (liter ) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Insulation Coating Industry?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Insulation Coating Industry?

Key companies in the market include Nanofan Industrial Coatings LLC, The Sherwin-Williams Company, Jotun, Kansai Paint Co Ltd, Akzo Nobel NV, Mascoat, PPG Industries Inc, SK FORMULATIONS INDIA PVT LTD, Nippon Paint, Carboline, Ugam Chemicals*List Not Exhaustive, Synavax.

3. What are the main segments of the Insulation Coating Industry?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.7 billion as of 2022.

5. What are some drivers contributing to market growth?

; Growing Construction Industry; Increasing Demand from Automotive and Marine Industries.

6. What are the notable trends driving market growth?

Automotive and Marine Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

; High Initial Cost of Insulation Coating; Unfavorable Conditions Arising Due to COVID-19 Outbreak.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Insulation Coating Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Insulation Coating Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Insulation Coating Industry?

To stay informed about further developments, trends, and reports in the Insulation Coating Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence