Key Insights

The global Polyurea market is poised for robust expansion, projected to reach a significant valuation with a Compound Annual Growth Rate (CAGR) exceeding 5.60%. This dynamic growth is fueled by the inherent properties of polyurea, including its exceptional durability, rapid curing times, and superior resistance to abrasion, chemicals, and corrosion. These attributes make it an increasingly sought-after material across a diverse range of end-user industries. The construction sector stands out as a primary driver, leveraging polyurea for protective coatings, waterproofing membranes, and joint sealants that enhance the longevity and performance of infrastructure. Similarly, the automotive industry is adopting polyurea for its impact resistance and aesthetic finishing capabilities, particularly in truck bed liners and underbody coatings. The paints and coatings sector also plays a crucial role, with polyurea formulations offering advanced protection for various surfaces.

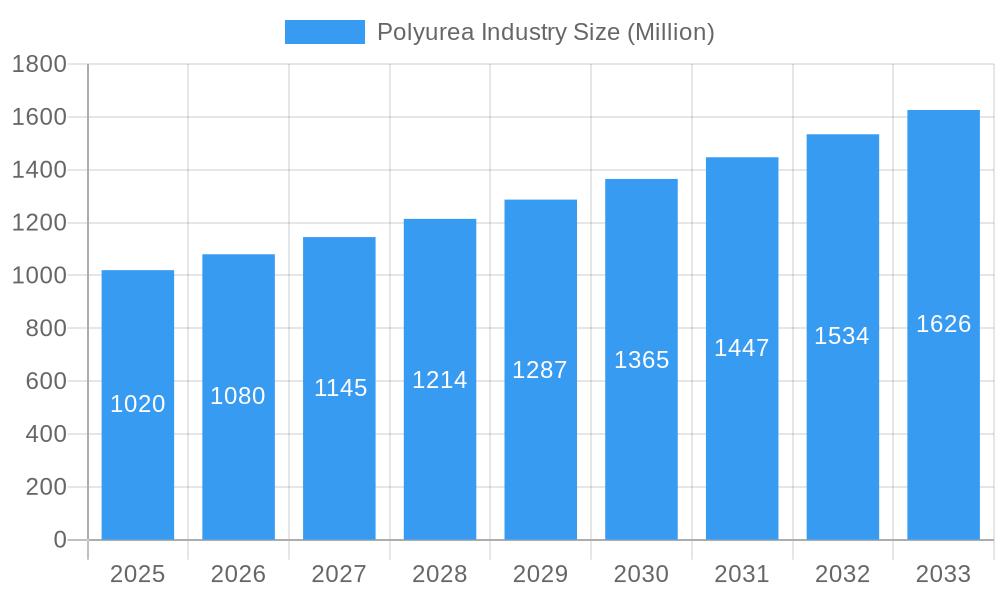

Polyurea Industry Market Size (In Billion)

Further propelling market growth are ongoing advancements in polyurea technology, leading to the development of specialized formulations tailored for specific applications. This includes innovations in hot polyurea and cold polyurea systems, catering to different application requirements and environmental conditions. The increasing demand for sustainable and long-lasting protective solutions across industrial, maritime, and transportation sectors also contributes to the positive market outlook. While challenges such as initial installation costs and the need for skilled application can pose some restraints, the long-term benefits and performance advantages of polyurea are steadily overcoming these hurdles. Emerging economies, particularly in the Asia Pacific region, are expected to be significant growth engines due to rapid industrialization and infrastructure development.

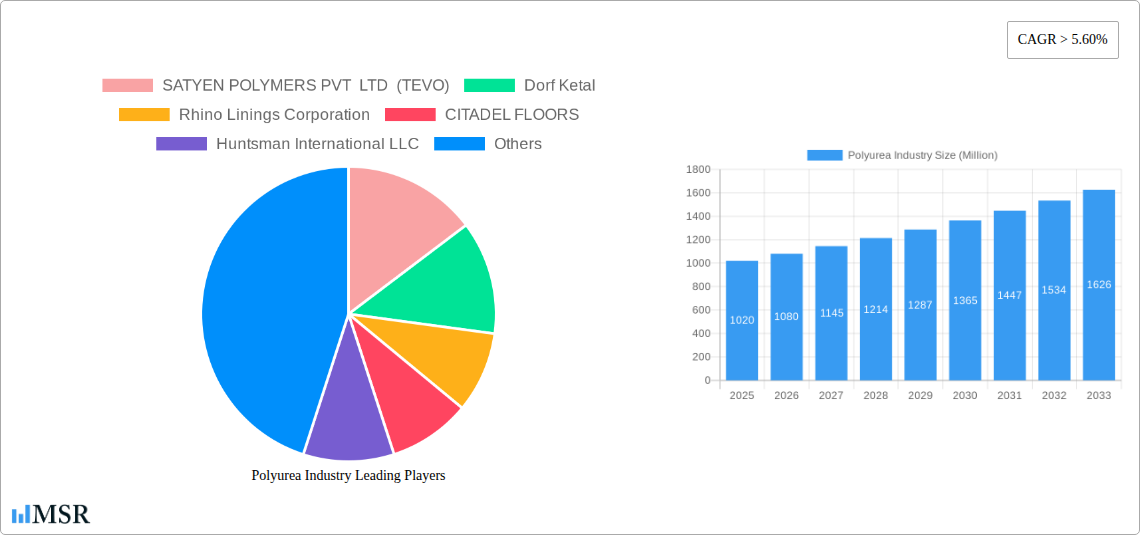

Polyurea Industry Company Market Share

Here is an SEO-optimized and engaging report description for the Polyurea Industry, incorporating the provided details and adhering to all formatting and content requirements.

This in-depth Polyurea Industry report offers a holistic view of the global polyurea market, encompassing historical performance (2019-2024), a robust base year analysis (2025), and an extensive forecast period (2025-2033). With a projected market size of xx Million USD and a compound annual growth rate (CAGR) of xx%, this report is an essential resource for stakeholders seeking to understand the intricate dynamics of the polyurea coatings, linings, and sealants market. Delving into key segments like Aromatic and Aliphatic chemical structures, Hot and Cold Polyurea types, and critical end-user industries such as Construction, Automotive, Industrial, and Maritime, this analysis provides actionable insights for strategic decision-making.

Polyurea Industry Market Concentration & Dynamics

The Polyurea Industry market exhibits a dynamic concentration, with key players actively engaged in innovation and strategic expansion. Market concentration is influenced by a blend of large multinational corporations and specialized manufacturers, contributing to an evolving innovation ecosystem. Regulatory frameworks are gradually shaping product development and adoption, particularly concerning environmental standards and safety protocols. Substitute products, such as epoxies and polyurethanes, present a constant competitive landscape, necessitating continuous technological advancements in polyurea formulations for superior performance. End-user trends are strongly leaning towards high-performance, durable, and sustainable solutions, driving demand for advanced polyurea applications. Mergers and acquisitions (M&A) activities are anticipated to play a significant role in market consolidation and capacity enhancement, with an estimated xx M&A deals projected over the forecast period. Market share is currently dominated by xx% held by the top 5 players.

Polyurea Industry Industry Insights & Trends

The global Polyurea Industry is poised for significant expansion, driven by escalating demand for protective coatings and sealants across diverse sectors. The market size is estimated to reach xx Million USD by 2025, with a projected CAGR of xx% during the 2025-2033 forecast period. This growth is propelled by several key factors. Firstly, the construction industry's robust expansion, particularly in emerging economies, fuels the demand for polyurea in roofing, flooring, and structural protection due to its superior waterproofing, chemical resistance, and rapid curing properties. Secondly, the automotive sector's increasing focus on lightweighting and enhanced durability is leading to wider adoption of polyurea for bed liners, underbody coatings, and impact-resistant components. Technological disruptions, including the development of faster-curing polyurea systems and eco-friendly formulations, are enhancing application efficiency and environmental compliance. Evolving consumer behaviors, characterized by a preference for long-lasting and low-maintenance solutions, further bolster the market's trajectory. The Industrial sector, demanding high-performance coatings for corrosive environments and heavy-duty applications, represents another significant growth avenue. The maritime industry's need for anti-corrosion and abrasion-resistant coatings for vessels and offshore structures also contributes substantially to market growth. The continuous innovation in spray application technology further optimizes the deployment of polyurea, making it a preferred choice for complex projects.

Key Markets & Segments Leading Polyurea Industry

The Construction end-user industry currently stands as the dominant market segment for polyurea, propelled by substantial investments in infrastructure development and commercial building projects globally. The Aromatic chemical structure segment is also a key driver, offering excellent physical properties and cost-effectiveness, though Aliphatic polyurea is gaining traction for its UV stability and aesthetic appeal, particularly in exposed applications. In terms of application Type, Hot Polyurea systems continue to lead due to their rapid cure times and seamless application, making them ideal for large-scale projects. However, the demand for Cold Polyurea systems is growing for smaller repairs and applications where heated equipment is not feasible. The Lining product category is a primary revenue generator, serving applications from industrial tank linings to protective coatings for concrete structures. Coating applications, encompassing protective and decorative finishes across various substrates, are also experiencing significant growth.

- Drivers for Construction Dominance:

- Global infrastructure spending surge, with an estimated xx Billion USD in 2025.

- Increasing demand for durable and waterproof roofing solutions, contributing xx% to the construction segment.

- Growth in residential and commercial construction projects, especially in Asia-Pacific and North America.

- Need for chemical-resistant flooring in industrial and institutional buildings.

- Dominance Analysis: The construction sector's reliance on polyurea for its exceptional adhesion, crack-bridging capabilities, and resistance to moisture and chemicals makes it a cornerstone of market demand. The rapid curing nature of hot polyurea systems in particular, allows for quicker project completion, a critical factor in the fast-paced construction environment. While automotive and industrial sectors are significant, the sheer scale of construction projects worldwide solidifies its leading position. The development of specialized polyurea formulations for specific construction challenges, such as seismic retrofitting and bridge deck protection, further cements its dominance.

Polyurea Industry Product Developments

Product innovations in the Polyurea Industry are focused on enhancing performance and sustainability. Advancements in low-VOC (Volatile Organic Compound) polyurea formulations are meeting stringent environmental regulations and appealing to eco-conscious consumers. Furthermore, the development of self-healing polyurea coatings is a significant technological leap, offering extended service life and reduced maintenance costs for critical infrastructure. Innovations in faster-reacting polyurea systems, even at lower temperatures, are expanding application windows and reducing project timelines. The integration of anti-microbial properties into polyurea coatings is also a notable development, particularly for applications in healthcare and food processing facilities.

Challenges in the Polyurea Industry Market

The Polyurea Industry market faces several challenges, including the relatively high initial cost of materials and equipment compared to traditional coatings, which can deter adoption in price-sensitive markets. Stringent regulatory hurdles regarding VOC emissions and disposal of chemical byproducts necessitate ongoing research and development for compliance. Supply chain disruptions and the fluctuating prices of raw materials can impact profitability and lead times, as seen with the recent xx% increase in isocyanate prices. Furthermore, the specialized application techniques required for polyurea demand skilled labor, which can be a limiting factor in certain regions, potentially impacting the market by xx% in terms of adoption rate.

Forces Driving Polyurea Industry Growth

Several forces are propelling the growth of the Polyurea Industry. Technological advancements in formulations, such as faster curing times and enhanced UV stability, are expanding application possibilities and performance expectations. The increasing global focus on infrastructure development and repair, particularly in emerging economies, creates substantial demand for durable and protective coatings. Economic factors, including rising construction spending and industrial output, directly correlate with polyurea market expansion. Regulatory tailwinds favoring high-performance, long-lasting protective materials that reduce lifecycle costs also contribute to market growth.

Challenges in the Polyurea Industry Market

Long-term growth catalysts for the Polyurea Industry are rooted in continuous innovation and strategic market expansion. The development of bio-based polyurea materials presents a significant opportunity to address sustainability concerns and tap into the growing green construction market. Strategic partnerships between raw material suppliers and polyurea manufacturers can optimize supply chains and drive cost efficiencies. Market expansion into underserved geographical regions with burgeoning construction and industrial sectors, such as Southeast Asia and Africa, will be crucial for sustained growth. Furthermore, the increasing demand for customized polyurea solutions tailored to specific industry needs will foster deeper market penetration.

Emerging Opportunities in Polyurea Industry

Emerging opportunities in the Polyurea Industry are diverse and promising. The growing trend of smart coatings, incorporating sensors or self-healing capabilities, offers a significant avenue for innovation. The expansion of polyurea applications in renewable energy sectors, such as protective coatings for wind turbine blades and solar panel installations, presents a substantial growth frontier. Furthermore, the increasing adoption of polyurea in the transportation sector for lightweighting and enhanced durability in electric vehicles and high-speed rail is a key emerging trend. The focus on durable, low-maintenance solutions for aging infrastructure worldwide also provides a fertile ground for polyurea adoption.

Leading Players in the Polyurea Industry Sector

- SATYEN POLYMERS PVT LTD (TEVO)

- Dorf Ketal

- Rhino Linings Corporation

- CITADEL FLOORS

- Huntsman International LLC

- Elastothane

- Speciality Products Inc

- Teknos Group

- Lonza

- Covestro AG

- Armorthane

Key Milestones in Polyurea Industry Industry

- January 2023: Teknos Deutschland GmbH plans to relocate its production from Fulda to the existing Brüggen site. The relocation aims to develop further the production and delivery capabilities of Teknos Deutschland GmbH in Germany. This enhancement of production capabilities is likely to boost the market for polyurea in Germany.

- September 2022: Teknos Group opened its new Commercial and Competence Centre with a technical application laboratory and warehouse facilities in Dong Nai Province to expand its business in Vietnam. This helps the company further develop its business, which in turn helps in the growth of the polyurea market.

Strategic Outlook for Polyurea Industry Market

The strategic outlook for the Polyurea Industry Market remains exceptionally positive, driven by an ongoing demand for high-performance protective solutions. Growth accelerators include the continued integration of sustainable practices, such as the development of low-VOC and bio-based polyurea formulations, which align with global environmental initiatives. Strategic focus on research and development to create polyurea with advanced functionalities, such as enhanced chemical resistance and extreme temperature tolerance, will unlock new market segments. Furthermore, expansion into developing economies with significant infrastructure needs and the increasing adoption of polyurea in niche applications like sports surfacing and theme park construction are key strategic opportunities to capitalize on.

Polyurea Industry Segmentation

-

1. Chemical Structure

- 1.1. Aromatic

- 1.2. Aliphatic

-

2. Type

- 2.1. Hot Polyurea

- 2.2. Cold Polyurea

-

3. Product

- 3.1. Lining

- 3.2. Coating

- 3.3. Sealants

-

4. End-user Industry

- 4.1. Construction

- 4.2. Paints and Coatings

- 4.3. Automotive

- 4.4. Industrial

- 4.5. Maritime

- 4.6. Other End-user Industries (Transportation, Etc.)

Polyurea Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

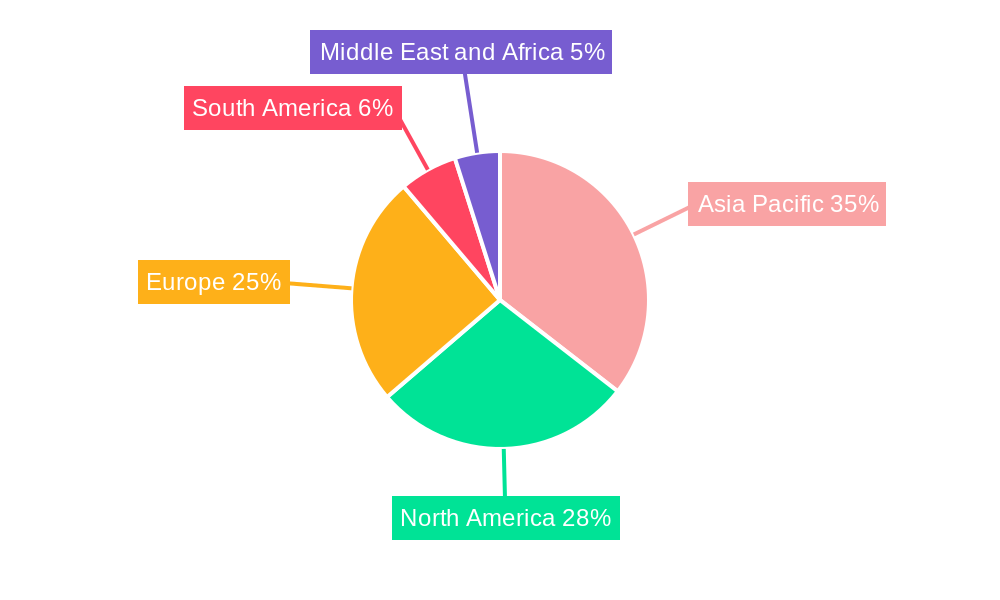

Polyurea Industry Regional Market Share

Geographic Coverage of Polyurea Industry

Polyurea Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 5.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 5.1.1. Aromatic

- 5.1.2. Aliphatic

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hot Polyurea

- 5.2.2. Cold Polyurea

- 5.3. Market Analysis, Insights and Forecast - by Product

- 5.3.1. Lining

- 5.3.2. Coating

- 5.3.3. Sealants

- 5.4. Market Analysis, Insights and Forecast - by End-user Industry

- 5.4.1. Construction

- 5.4.2. Paints and Coatings

- 5.4.3. Automotive

- 5.4.4. Industrial

- 5.4.5. Maritime

- 5.4.6. Other End-user Industries (Transportation, Etc.)

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Asia Pacific

- 5.5.2. North America

- 5.5.3. Europe

- 5.5.4. South America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 6. Global Polyurea Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 6.1.1. Aromatic

- 6.1.2. Aliphatic

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Hot Polyurea

- 6.2.2. Cold Polyurea

- 6.3. Market Analysis, Insights and Forecast - by Product

- 6.3.1. Lining

- 6.3.2. Coating

- 6.3.3. Sealants

- 6.4. Market Analysis, Insights and Forecast - by End-user Industry

- 6.4.1. Construction

- 6.4.2. Paints and Coatings

- 6.4.3. Automotive

- 6.4.4. Industrial

- 6.4.5. Maritime

- 6.4.6. Other End-user Industries (Transportation, Etc.)

- 6.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 7. Asia Pacific Polyurea Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 7.1.1. Aromatic

- 7.1.2. Aliphatic

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Hot Polyurea

- 7.2.2. Cold Polyurea

- 7.3. Market Analysis, Insights and Forecast - by Product

- 7.3.1. Lining

- 7.3.2. Coating

- 7.3.3. Sealants

- 7.4. Market Analysis, Insights and Forecast - by End-user Industry

- 7.4.1. Construction

- 7.4.2. Paints and Coatings

- 7.4.3. Automotive

- 7.4.4. Industrial

- 7.4.5. Maritime

- 7.4.6. Other End-user Industries (Transportation, Etc.)

- 7.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 8. North America Polyurea Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 8.1.1. Aromatic

- 8.1.2. Aliphatic

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Hot Polyurea

- 8.2.2. Cold Polyurea

- 8.3. Market Analysis, Insights and Forecast - by Product

- 8.3.1. Lining

- 8.3.2. Coating

- 8.3.3. Sealants

- 8.4. Market Analysis, Insights and Forecast - by End-user Industry

- 8.4.1. Construction

- 8.4.2. Paints and Coatings

- 8.4.3. Automotive

- 8.4.4. Industrial

- 8.4.5. Maritime

- 8.4.6. Other End-user Industries (Transportation, Etc.)

- 8.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 9. Europe Polyurea Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 9.1.1. Aromatic

- 9.1.2. Aliphatic

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Hot Polyurea

- 9.2.2. Cold Polyurea

- 9.3. Market Analysis, Insights and Forecast - by Product

- 9.3.1. Lining

- 9.3.2. Coating

- 9.3.3. Sealants

- 9.4. Market Analysis, Insights and Forecast - by End-user Industry

- 9.4.1. Construction

- 9.4.2. Paints and Coatings

- 9.4.3. Automotive

- 9.4.4. Industrial

- 9.4.5. Maritime

- 9.4.6. Other End-user Industries (Transportation, Etc.)

- 9.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 10. South America Polyurea Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 10.1.1. Aromatic

- 10.1.2. Aliphatic

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Hot Polyurea

- 10.2.2. Cold Polyurea

- 10.3. Market Analysis, Insights and Forecast - by Product

- 10.3.1. Lining

- 10.3.2. Coating

- 10.3.3. Sealants

- 10.4. Market Analysis, Insights and Forecast - by End-user Industry

- 10.4.1. Construction

- 10.4.2. Paints and Coatings

- 10.4.3. Automotive

- 10.4.4. Industrial

- 10.4.5. Maritime

- 10.4.6. Other End-user Industries (Transportation, Etc.)

- 10.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 11. Middle East and Africa Polyurea Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 11.1.1. Aromatic

- 11.1.2. Aliphatic

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Hot Polyurea

- 11.2.2. Cold Polyurea

- 11.3. Market Analysis, Insights and Forecast - by Product

- 11.3.1. Lining

- 11.3.2. Coating

- 11.3.3. Sealants

- 11.4. Market Analysis, Insights and Forecast - by End-user Industry

- 11.4.1. Construction

- 11.4.2. Paints and Coatings

- 11.4.3. Automotive

- 11.4.4. Industrial

- 11.4.5. Maritime

- 11.4.6. Other End-user Industries (Transportation, Etc.)

- 11.1. Market Analysis, Insights and Forecast - by Chemical Structure

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SATYEN POLYMERS PVT LTD (TEVO)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Dorf Ketal

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Rhino Linings Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 CITADEL FLOORS

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Huntsman International LLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Elastothane

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Speciality Products Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Teknos Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Lonza

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Covestro AG

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Armorthane

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 SATYEN POLYMERS PVT LTD (TEVO)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Polyurea Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Polyurea Industry Volume Breakdown (K Tons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Polyurea Industry Revenue (Million), by Chemical Structure 2025 & 2033

- Figure 4: Asia Pacific Polyurea Industry Volume (K Tons), by Chemical Structure 2025 & 2033

- Figure 5: Asia Pacific Polyurea Industry Revenue Share (%), by Chemical Structure 2025 & 2033

- Figure 6: Asia Pacific Polyurea Industry Volume Share (%), by Chemical Structure 2025 & 2033

- Figure 7: Asia Pacific Polyurea Industry Revenue (Million), by Type 2025 & 2033

- Figure 8: Asia Pacific Polyurea Industry Volume (K Tons), by Type 2025 & 2033

- Figure 9: Asia Pacific Polyurea Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Asia Pacific Polyurea Industry Volume Share (%), by Type 2025 & 2033

- Figure 11: Asia Pacific Polyurea Industry Revenue (Million), by Product 2025 & 2033

- Figure 12: Asia Pacific Polyurea Industry Volume (K Tons), by Product 2025 & 2033

- Figure 13: Asia Pacific Polyurea Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Asia Pacific Polyurea Industry Volume Share (%), by Product 2025 & 2033

- Figure 15: Asia Pacific Polyurea Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 16: Asia Pacific Polyurea Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 17: Asia Pacific Polyurea Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Asia Pacific Polyurea Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 19: Asia Pacific Polyurea Industry Revenue (Million), by Country 2025 & 2033

- Figure 20: Asia Pacific Polyurea Industry Volume (K Tons), by Country 2025 & 2033

- Figure 21: Asia Pacific Polyurea Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Polyurea Industry Volume Share (%), by Country 2025 & 2033

- Figure 23: North America Polyurea Industry Revenue (Million), by Chemical Structure 2025 & 2033

- Figure 24: North America Polyurea Industry Volume (K Tons), by Chemical Structure 2025 & 2033

- Figure 25: North America Polyurea Industry Revenue Share (%), by Chemical Structure 2025 & 2033

- Figure 26: North America Polyurea Industry Volume Share (%), by Chemical Structure 2025 & 2033

- Figure 27: North America Polyurea Industry Revenue (Million), by Type 2025 & 2033

- Figure 28: North America Polyurea Industry Volume (K Tons), by Type 2025 & 2033

- Figure 29: North America Polyurea Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: North America Polyurea Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: North America Polyurea Industry Revenue (Million), by Product 2025 & 2033

- Figure 32: North America Polyurea Industry Volume (K Tons), by Product 2025 & 2033

- Figure 33: North America Polyurea Industry Revenue Share (%), by Product 2025 & 2033

- Figure 34: North America Polyurea Industry Volume Share (%), by Product 2025 & 2033

- Figure 35: North America Polyurea Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 36: North America Polyurea Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 37: North America Polyurea Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 38: North America Polyurea Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 39: North America Polyurea Industry Revenue (Million), by Country 2025 & 2033

- Figure 40: North America Polyurea Industry Volume (K Tons), by Country 2025 & 2033

- Figure 41: North America Polyurea Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: North America Polyurea Industry Volume Share (%), by Country 2025 & 2033

- Figure 43: Europe Polyurea Industry Revenue (Million), by Chemical Structure 2025 & 2033

- Figure 44: Europe Polyurea Industry Volume (K Tons), by Chemical Structure 2025 & 2033

- Figure 45: Europe Polyurea Industry Revenue Share (%), by Chemical Structure 2025 & 2033

- Figure 46: Europe Polyurea Industry Volume Share (%), by Chemical Structure 2025 & 2033

- Figure 47: Europe Polyurea Industry Revenue (Million), by Type 2025 & 2033

- Figure 48: Europe Polyurea Industry Volume (K Tons), by Type 2025 & 2033

- Figure 49: Europe Polyurea Industry Revenue Share (%), by Type 2025 & 2033

- Figure 50: Europe Polyurea Industry Volume Share (%), by Type 2025 & 2033

- Figure 51: Europe Polyurea Industry Revenue (Million), by Product 2025 & 2033

- Figure 52: Europe Polyurea Industry Volume (K Tons), by Product 2025 & 2033

- Figure 53: Europe Polyurea Industry Revenue Share (%), by Product 2025 & 2033

- Figure 54: Europe Polyurea Industry Volume Share (%), by Product 2025 & 2033

- Figure 55: Europe Polyurea Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 56: Europe Polyurea Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 57: Europe Polyurea Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 58: Europe Polyurea Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 59: Europe Polyurea Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Europe Polyurea Industry Volume (K Tons), by Country 2025 & 2033

- Figure 61: Europe Polyurea Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Europe Polyurea Industry Volume Share (%), by Country 2025 & 2033

- Figure 63: South America Polyurea Industry Revenue (Million), by Chemical Structure 2025 & 2033

- Figure 64: South America Polyurea Industry Volume (K Tons), by Chemical Structure 2025 & 2033

- Figure 65: South America Polyurea Industry Revenue Share (%), by Chemical Structure 2025 & 2033

- Figure 66: South America Polyurea Industry Volume Share (%), by Chemical Structure 2025 & 2033

- Figure 67: South America Polyurea Industry Revenue (Million), by Type 2025 & 2033

- Figure 68: South America Polyurea Industry Volume (K Tons), by Type 2025 & 2033

- Figure 69: South America Polyurea Industry Revenue Share (%), by Type 2025 & 2033

- Figure 70: South America Polyurea Industry Volume Share (%), by Type 2025 & 2033

- Figure 71: South America Polyurea Industry Revenue (Million), by Product 2025 & 2033

- Figure 72: South America Polyurea Industry Volume (K Tons), by Product 2025 & 2033

- Figure 73: South America Polyurea Industry Revenue Share (%), by Product 2025 & 2033

- Figure 74: South America Polyurea Industry Volume Share (%), by Product 2025 & 2033

- Figure 75: South America Polyurea Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 76: South America Polyurea Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 77: South America Polyurea Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 78: South America Polyurea Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 79: South America Polyurea Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Polyurea Industry Volume (K Tons), by Country 2025 & 2033

- Figure 81: South America Polyurea Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Polyurea Industry Volume Share (%), by Country 2025 & 2033

- Figure 83: Middle East and Africa Polyurea Industry Revenue (Million), by Chemical Structure 2025 & 2033

- Figure 84: Middle East and Africa Polyurea Industry Volume (K Tons), by Chemical Structure 2025 & 2033

- Figure 85: Middle East and Africa Polyurea Industry Revenue Share (%), by Chemical Structure 2025 & 2033

- Figure 86: Middle East and Africa Polyurea Industry Volume Share (%), by Chemical Structure 2025 & 2033

- Figure 87: Middle East and Africa Polyurea Industry Revenue (Million), by Type 2025 & 2033

- Figure 88: Middle East and Africa Polyurea Industry Volume (K Tons), by Type 2025 & 2033

- Figure 89: Middle East and Africa Polyurea Industry Revenue Share (%), by Type 2025 & 2033

- Figure 90: Middle East and Africa Polyurea Industry Volume Share (%), by Type 2025 & 2033

- Figure 91: Middle East and Africa Polyurea Industry Revenue (Million), by Product 2025 & 2033

- Figure 92: Middle East and Africa Polyurea Industry Volume (K Tons), by Product 2025 & 2033

- Figure 93: Middle East and Africa Polyurea Industry Revenue Share (%), by Product 2025 & 2033

- Figure 94: Middle East and Africa Polyurea Industry Volume Share (%), by Product 2025 & 2033

- Figure 95: Middle East and Africa Polyurea Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 96: Middle East and Africa Polyurea Industry Volume (K Tons), by End-user Industry 2025 & 2033

- Figure 97: Middle East and Africa Polyurea Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 98: Middle East and Africa Polyurea Industry Volume Share (%), by End-user Industry 2025 & 2033

- Figure 99: Middle East and Africa Polyurea Industry Revenue (Million), by Country 2025 & 2033

- Figure 100: Middle East and Africa Polyurea Industry Volume (K Tons), by Country 2025 & 2033

- Figure 101: Middle East and Africa Polyurea Industry Revenue Share (%), by Country 2025 & 2033

- Figure 102: Middle East and Africa Polyurea Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Polyurea Industry Revenue Million Forecast, by Chemical Structure 2020 & 2033

- Table 2: Global Polyurea Industry Volume K Tons Forecast, by Chemical Structure 2020 & 2033

- Table 3: Global Polyurea Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 4: Global Polyurea Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 5: Global Polyurea Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 6: Global Polyurea Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 7: Global Polyurea Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Polyurea Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 9: Global Polyurea Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 10: Global Polyurea Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 11: Global Polyurea Industry Revenue Million Forecast, by Chemical Structure 2020 & 2033

- Table 12: Global Polyurea Industry Volume K Tons Forecast, by Chemical Structure 2020 & 2033

- Table 13: Global Polyurea Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Polyurea Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 15: Global Polyurea Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 16: Global Polyurea Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 17: Global Polyurea Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Polyurea Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 19: Global Polyurea Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Global Polyurea Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 21: China Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: China Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: India Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Japan Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Japan Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 27: South Korea Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: South Korea Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Asia Pacific Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 31: Global Polyurea Industry Revenue Million Forecast, by Chemical Structure 2020 & 2033

- Table 32: Global Polyurea Industry Volume K Tons Forecast, by Chemical Structure 2020 & 2033

- Table 33: Global Polyurea Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 34: Global Polyurea Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 35: Global Polyurea Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 36: Global Polyurea Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 37: Global Polyurea Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 38: Global Polyurea Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 39: Global Polyurea Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Polyurea Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 41: United States Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: United States Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 43: Canada Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Canada Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 45: Mexico Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Mexico Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 47: Global Polyurea Industry Revenue Million Forecast, by Chemical Structure 2020 & 2033

- Table 48: Global Polyurea Industry Volume K Tons Forecast, by Chemical Structure 2020 & 2033

- Table 49: Global Polyurea Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 50: Global Polyurea Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 51: Global Polyurea Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 52: Global Polyurea Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 53: Global Polyurea Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 54: Global Polyurea Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 55: Global Polyurea Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Global Polyurea Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 57: Germany Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Germany Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 59: United Kingdom Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: United Kingdom Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 61: France Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: France Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 63: Italy Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Italy Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 65: Rest of Europe Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: Rest of Europe Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 67: Global Polyurea Industry Revenue Million Forecast, by Chemical Structure 2020 & 2033

- Table 68: Global Polyurea Industry Volume K Tons Forecast, by Chemical Structure 2020 & 2033

- Table 69: Global Polyurea Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 70: Global Polyurea Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 71: Global Polyurea Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 72: Global Polyurea Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 73: Global Polyurea Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 74: Global Polyurea Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 75: Global Polyurea Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 76: Global Polyurea Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 77: Brazil Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: Brazil Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 79: Argentina Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 80: Argentina Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 81: Rest of South America Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 82: Rest of South America Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 83: Global Polyurea Industry Revenue Million Forecast, by Chemical Structure 2020 & 2033

- Table 84: Global Polyurea Industry Volume K Tons Forecast, by Chemical Structure 2020 & 2033

- Table 85: Global Polyurea Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 86: Global Polyurea Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 87: Global Polyurea Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 88: Global Polyurea Industry Volume K Tons Forecast, by Product 2020 & 2033

- Table 89: Global Polyurea Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 90: Global Polyurea Industry Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 91: Global Polyurea Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 92: Global Polyurea Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 93: Saudi Arabia Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 94: Saudi Arabia Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 95: South Africa Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 96: South Africa Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 97: Rest of Middle East and Africa Polyurea Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 98: Rest of Middle East and Africa Polyurea Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Polyurea Industry?

The projected CAGR is approximately > 5.60%.

2. Which companies are prominent players in the Polyurea Industry?

Key companies in the market include SATYEN POLYMERS PVT LTD (TEVO), Dorf Ketal, Rhino Linings Corporation, CITADEL FLOORS, Huntsman International LLC, Elastothane, Speciality Products Inc, Teknos Group, Lonza, Covestro AG, Armorthane.

3. What are the main segments of the Polyurea Industry?

The market segments include Chemical Structure, Type, Product, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.02 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand of Polyurea from Construction Industry; Growing Demand from Automotive Sector; Other Drivers.

6. What are the notable trends driving market growth?

Growing Demand for Polyurea from the Construction Industry.

7. Are there any restraints impacting market growth?

Volatility in Raw Material Price; Other Restraints.

8. Can you provide examples of recent developments in the market?

January 2023: Teknos Deutschland GmbH plans to relocate its production from Fulda to the existing Brüggen site. The relocation aims to develop further the production and delivery capabilities of Teknos Deutschland GmbH in Germany. This enhancement of production capabilities is likely to boost the market for polyurea in Germany.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Polyurea Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Polyurea Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Polyurea Industry?

To stay informed about further developments, trends, and reports in the Polyurea Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence