Key Insights

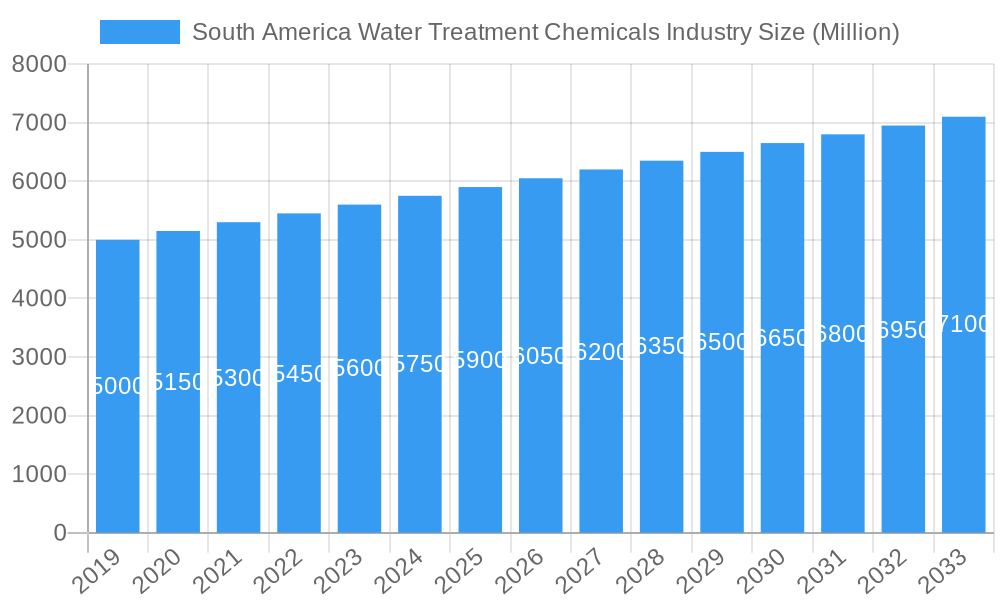

The South America Water Treatment Chemicals market is projected to experience substantial growth, reaching an estimated market size of $2.9 billion by 2024 and continuing its expansion through 2033. This dynamic sector is driven by a compound annual growth rate (CAGR) of 7.4%, fueled by the escalating demand for purified water across diverse industrial applications. Key growth drivers include the imperative for water conservation, stringent environmental mandates on industrial wastewater, and the sustained expansion of major end-user industries such as power generation, oil and gas, chemical manufacturing, mining, food and beverage, and pulp and paper. The ongoing need to upgrade aging infrastructure across South America further amplifies the requirement for advanced water treatment strategies to ensure water quality and operational longevity.

South America Water Treatment Chemicals Industry Market Size (In Billion)

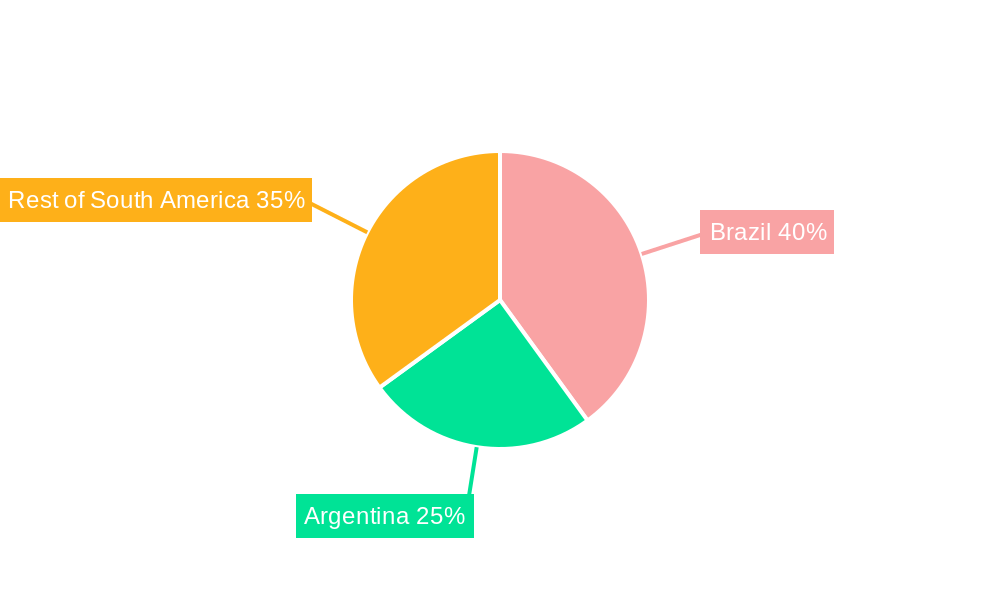

Within the South America Water Treatment Chemicals market, Flocculants & Coagulants and Biocides & Disinfectants are anticipated to dominate, owing to their critical functions in water purification and microbial control. Scale & Corrosion Inhibitors also play a vital role, especially in sectors like power and oil & gas, where equipment integrity is paramount. While opportunities abound, potential restraints include the significant initial capital investment for advanced treatment technologies and volatility in raw material pricing. Nevertheless, a steadfast commitment to sustainability, coupled with technological innovations yielding more efficient and cost-effective chemical solutions, is expected to mitigate these challenges. Brazil is forecasted to lead market share, supported by its robust industrial base and extensive water management initiatives, followed by Argentina and the broader South American region, each offering distinct growth avenues.

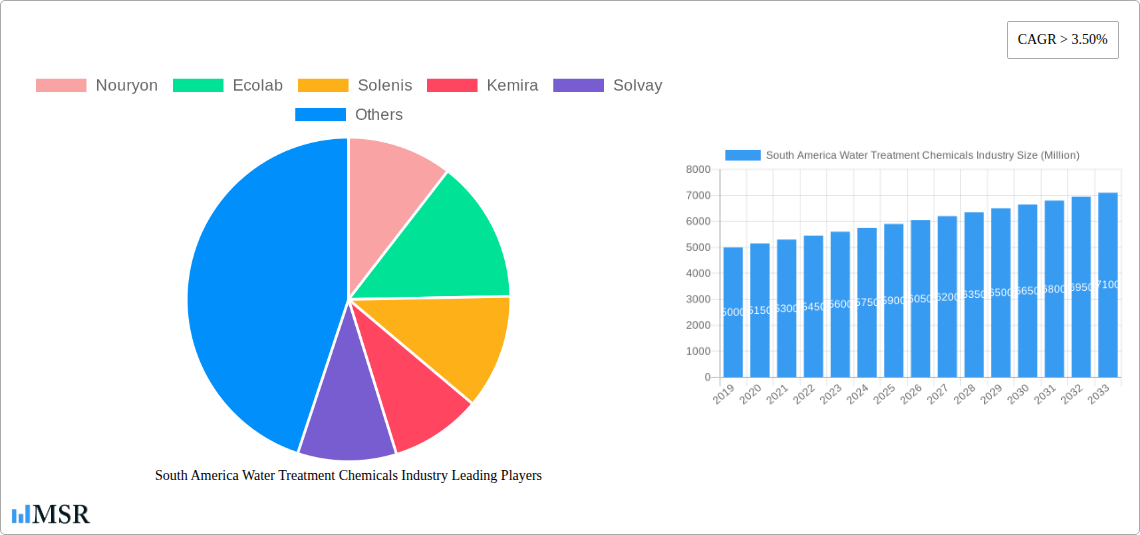

South America Water Treatment Chemicals Industry Company Market Share

South America Water Treatment Chemicals Market Analysis: Trends, Opportunities, and Forecasts (2024-2033)

This comprehensive market report offers in-depth analysis of the South America water treatment chemicals market, a crucial sector shaped by rising industrial demand, strict environmental regulations, and the global push for sustainable water management. Examining the period from 2019 to 2033, with a base year of 2024 and a forecast horizon of 2024–2033, this report is an essential resource for understanding market dynamics, identifying lucrative opportunities, and navigating the competitive landscape.

Key Market Insights:

- Market Size: Estimated at $2.9 billion in 2024, with a projected reach of $6.5 billion by 2033, exhibiting a CAGR of 7.4%.

- Dominant Segments: Flocculants & Coagulants and Biocides & Disinfectants lead market share.

- Key Geographies: Brazil and Argentina are identified as primary growth engines.

- Key Industry Players: Features strategic insights on leading companies including Nouryon, Ecolab, Solenis, Kemira, Solvay, Lonza, Kurita Water Industries Ltd, SNF, Suez, and others.

South America Water Treatment Chemicals Industry Market Concentration & Dynamics

The South America water treatment chemicals market is characterized by a moderate to high level of concentration, with a few key global players holding substantial market share. Innovation is primarily driven by research and development in advanced chemical formulations for enhanced efficiency, reduced environmental impact, and compliance with evolving regulations. The innovation ecosystem benefits from collaborations between chemical manufacturers, research institutions, and end-user industries seeking tailored solutions. Regulatory frameworks, while varied across countries, are increasingly emphasizing water quality standards and sustainable practices, acting as a significant market driver. Substitute products, such as membrane filtration technologies, present a competitive challenge but often complement chemical treatments rather than fully replace them. End-user trends point towards a growing preference for eco-friendly and high-performance chemicals, particularly in sectors like mining and food & beverage. Mergers and acquisitions (M&A) activities are observed as companies seek to expand their product portfolios, geographic reach, and technological capabilities. The M&A deal count has seen a steady increase in the past five years, reflecting strategic consolidation to capture market share and enhance competitive positioning.

South America Water Treatment Chemicals Industry Industry Insights & Trends

The South America water treatment chemicals industry is experiencing robust growth, propelled by a confluence of powerful market drivers. Foremost among these is the escalating demand for clean water across industrial and municipal sectors, fueled by population growth, urbanization, and the expansion of key industries such as mining and mineral processing, oil and gas, and chemical manufacturing. Stringent environmental regulations concerning wastewater discharge and water recycling are compelling industries to invest in advanced water treatment solutions, thereby boosting the consumption of water treatment chemicals. Technological disruptions are playing a pivotal role, with innovations in areas like advanced coagulants, biodegradable biocides, and smart dosing systems enhancing treatment efficacy and reducing operational costs. For instance, the development of novel flocculants with improved settling properties is significantly optimizing sludge dewatering processes. Evolving consumer behaviors, particularly a heightened awareness of water scarcity and environmental sustainability, are also influencing market trends. Consumers and industries alike are increasingly demanding environmentally responsible and chemically efficient solutions. The overall market size is projected to witness substantial expansion, driven by these synergistic factors. The Compound Annual Growth Rate (CAGR) for the forecast period is expected to be significant, reflecting sustained demand and innovation. Specific market trends include a growing preference for specialized chemicals tailored to unique water chemistries and industrial processes, and an increased adoption of digital solutions for real-time monitoring and control of water treatment operations. The shift towards circular economy principles is also encouraging the development of chemicals that facilitate water reuse and resource recovery. The demand for scale and corrosion inhibitors remains high, particularly in power generation and oil & gas operations where maintaining asset integrity is paramount. Similarly, biocides and disinfectants are crucial for ensuring water safety and preventing microbial contamination across diverse end-user industries. The "Others" category for product types is expanding due to the development of novel chemistries addressing niche treatment challenges.

Key Markets & Segments Leading South America Water Treatment Chemicals Industry

The South America water treatment chemicals industry is experiencing dynamic growth, with distinct regional and segment leaders emerging.

Dominant Geography: Brazil

Brazil stands as the largest and most influential market within South America for water treatment chemicals.

- Drivers of Dominance:

- Industrial Powerhouse: Brazil's robust industrial base, encompassing significant activity in oil and gas, mining and mineral processing, chemical manufacturing, and pulp and paper, necessitates substantial water treatment to meet operational demands and regulatory compliances.

- Agricultural Significance: The vast agricultural sector in Brazil, a major food producer, also requires extensive water treatment for irrigation, processing, and wastewater management.

- Urbanization and Infrastructure: Growing urban populations and ongoing infrastructure development projects, including water supply and sanitation improvements, contribute to consistent demand for municipal water treatment chemicals.

- Regulatory Landscape: Increasingly stringent environmental regulations and a growing focus on water resource management are compelling industries to adopt advanced treatment technologies.

Leading Product Type: Flocculant & Coagulants

Flocculants and coagulants represent the largest and most critical product segment in the South America water treatment chemicals market.

- Drivers of Dominance:

- Essential for Solid-Liquid Separation: These chemicals are fundamental to virtually all water and wastewater treatment processes, enabling the removal of suspended solids, colloids, and dissolved organic matter.

- Widespread Application: Their application spans across all major end-user industries, including municipal wastewater treatment, industrial process water, and potable water purification.

- Cost-Effectiveness: Compared to some advanced separation technologies, flocculants and coagulants offer a cost-effective solution for bulk impurity removal.

- Technological Advancements: Continuous innovation in developing more efficient, environmentally friendly, and application-specific flocculants and coagulants further solidifies their market leadership.

Leading End-User Industry: Mining & Mineral Processing

The mining and mineral processing sector is a significant consumer of water treatment chemicals in South America.

- Drivers of Dominance:

- High Water Consumption: Mining operations are inherently water-intensive, requiring large volumes for extraction, processing, and dust suppression.

- Complex Wastewater: The wastewater generated from mining activities often contains heavy metals, suspended solids, and other pollutants, necessitating robust chemical treatment to meet discharge standards.

- Resource Recovery: Water treatment chemicals play a crucial role in water recycling and resource recovery within mining operations, enhancing sustainability.

- Economic Importance: The significant contribution of the mining sector to the economies of several South American countries drives consistent investment in operational efficiency and environmental compliance.

Rest of South America:

While Brazil leads, countries like Argentina, Chile, Peru, and Colombia are also significant contributors to the South America water treatment chemicals market. Argentina, with its strong agricultural and energy sectors, is a notable market. Chile's extensive mining industry, and Peru's robust mining and aquaculture sectors, further drive demand. Colombia's growing industrialization and focus on environmental protection are also increasing its market share. The "Rest of South America" segment is characterized by diverse industrial activities and evolving regulatory frameworks, presenting unique opportunities for specialized water treatment chemical solutions.

South America Water Treatment Chemicals Industry Product Developments

Product development in the South America water treatment chemicals sector is intensely focused on sustainability, efficiency, and regulatory compliance. Innovations are emerging in the form of biodegradable biocides that minimize environmental impact, advanced flocculants with enhanced settling capabilities for improved dewatering, and specialized scale and corrosion inhibitors tailored for the unique water chemistries found in industries like oil and gas. The development of greener coagulants and pH adjusters that reduce sludge production and are safer to handle is also a significant trend. These advancements not only improve treatment outcomes but also offer cost benefits and reduce the environmental footprint of industrial operations. The market relevance of these innovations is high, as industries increasingly seek solutions that align with ESG (Environmental, Social, and Governance) goals and stricter environmental mandates.

Challenges in the South America Water Treatment Chemicals Industry Market

The South America water treatment chemicals market faces several significant challenges. Regulatory hurdles, including varying standards across different countries and frequent updates, can create complexity for manufacturers and users. Supply chain disruptions, particularly for imported raw materials and finished goods, can impact availability and pricing. Intense competition from both global and local players leads to price pressures, affecting profit margins. Furthermore, the upfront cost of implementing advanced water treatment solutions can be a barrier for some smaller enterprises. Ensuring consistent product quality across diverse geographies and addressing the specific needs of a wide range of end-user industries requires substantial technical expertise and localized support.

Forces Driving South America Water Treatment Chemicals Industry Growth

Several key forces are driving the growth of the South America water treatment chemicals industry. Firstly, escalating industrial activities, particularly in the mining, oil and gas, and chemical manufacturing sectors, demand more sophisticated water treatment solutions for process water and wastewater management. Secondly, increasingly stringent environmental regulations and government initiatives promoting water conservation and pollution control are compelling industries to invest in effective water treatment chemicals. Thirdly, technological advancements in chemical formulations, leading to higher efficiency, reduced environmental impact, and cost-effectiveness, are creating new market opportunities. Finally, the growing awareness of water scarcity and the need for sustainable water management practices among both industries and consumers is a significant growth catalyst.

Challenges in the South America Water Treatment Chemicals Industry Market

Long-term growth catalysts in the South America water treatment chemicals market are deeply intertwined with innovation and strategic expansion. The continuous development of eco-friendly and high-performance chemical solutions that address emerging contaminants and stricter discharge limits will be crucial. Partnerships between chemical manufacturers, technology providers, and end-user industries will foster the development of integrated water management strategies. Furthermore, market expansion into underserved regions within South America, driven by economic development and increasing environmental consciousness, presents significant growth potential. The adoption of digitalization and smart technologies for optimized chemical dosing and real-time monitoring will also enhance the value proposition of water treatment chemicals.

Emerging Opportunities in South America Water Treatment Chemicals Industry

Emerging opportunities in the South America water treatment chemicals industry are abundant and diverse. A significant opportunity lies in the development and adoption of advanced oxidation processes (AOPs) and their associated chemical reagents for the removal of recalcitrant organic pollutants. The burgeoning demand for water reuse and recycling technologies, driven by water scarcity, opens avenues for specialized chemicals that facilitate these processes. The growing food and beverage industry's focus on water quality and hygiene presents opportunities for advanced disinfection and sanitization chemicals. Furthermore, the increasing electrification of industries and the expansion of renewable energy sources, such as hydropower and solar, create demand for specialized water treatment chemicals for cooling towers and associated infrastructure. There's also a growing market for bio-based and biodegradable water treatment chemicals as industries prioritize sustainability.

Leading Players in the South America Water Treatment Chemicals Industry Sector

- Nouryon

- Ecolab

- Solenis

- Kemira

- Solvay

- Lonza

- Kurita Water Industries Ltd

- SNF

- Suez

Key Milestones in South America Water Treatment Chemicals Industry Industry

- 2019/Q1: Increased investment in R&D for sustainable water treatment chemicals by major players.

- 2020/Q2: Impact of global supply chain disruptions on raw material availability for water treatment chemicals.

- 2021/Q3: Growing regulatory focus on heavy metal removal in mining wastewater in several South American countries.

- 2022/Q4: Launch of new bio-based flocculants and coagulants by leading manufacturers.

- 2023/Q1: Strategic partnerships formed to enhance digital water treatment solutions.

- 2023/Q2: Acquisition activity aimed at expanding product portfolios in specialized water treatment segments.

- 2024/Q3: Increased demand for scale and corrosion inhibitors in the power generation sector.

Strategic Outlook for South America Water Treatment Chemicals Industry Market

The strategic outlook for the South America water treatment chemicals market is highly promising, driven by a confluence of sustained industrial growth, tightening environmental regulations, and technological innovation. Growth accelerators include the ongoing development of high-performance, eco-friendly chemicals that address complex water challenges, such as emerging contaminants and the need for water reuse. Strategic opportunities lie in expanding market penetration in emerging economies within the region and in developing tailored solutions for the rapidly evolving needs of sectors like renewable energy and advanced manufacturing. The increasing adoption of digital monitoring and control systems for water treatment will also create new service-based revenue streams and enhance customer loyalty, positioning companies for long-term success in this vital market.

South America Water Treatment Chemicals Industry Segmentation

-

1. Product Type

- 1.1. Flocculant & Coagulants

- 1.2. Biocides & Disinfectants

- 1.3. Defoamers & Defoaming Agents

- 1.4. pH & Adjusters & Softeners

- 1.5. Scale & Corrosion Inhibitors

- 1.6. Others

-

2. End-user Industry

- 2.1. Power

- 2.2. Oil & Gas

- 2.3. Chemical Manufcaturing

- 2.4. Mining & Mineral Processing

- 2.5. Mining and Mineral Processing

- 2.6. Food & Beverage

- 2.7. Pulp & Ppaer

- 2.8. Others

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Rest of South America

South America Water Treatment Chemicals Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Rest of South America

South America Water Treatment Chemicals Industry Regional Market Share

Geographic Coverage of South America Water Treatment Chemicals Industry

South America Water Treatment Chemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Flocculant & Coagulants

- 5.1.2. Biocides & Disinfectants

- 5.1.3. Defoamers & Defoaming Agents

- 5.1.4. pH & Adjusters & Softeners

- 5.1.5. Scale & Corrosion Inhibitors

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Power

- 5.2.2. Oil & Gas

- 5.2.3. Chemical Manufcaturing

- 5.2.4. Mining & Mineral Processing

- 5.2.5. Mining and Mineral Processing

- 5.2.6. Food & Beverage

- 5.2.7. Pulp & Ppaer

- 5.2.8. Others

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global South America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Flocculant & Coagulants

- 6.1.2. Biocides & Disinfectants

- 6.1.3. Defoamers & Defoaming Agents

- 6.1.4. pH & Adjusters & Softeners

- 6.1.5. Scale & Corrosion Inhibitors

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Power

- 6.2.2. Oil & Gas

- 6.2.3. Chemical Manufcaturing

- 6.2.4. Mining & Mineral Processing

- 6.2.5. Mining and Mineral Processing

- 6.2.6. Food & Beverage

- 6.2.7. Pulp & Ppaer

- 6.2.8. Others

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Brazil South America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Flocculant & Coagulants

- 7.1.2. Biocides & Disinfectants

- 7.1.3. Defoamers & Defoaming Agents

- 7.1.4. pH & Adjusters & Softeners

- 7.1.5. Scale & Corrosion Inhibitors

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Power

- 7.2.2. Oil & Gas

- 7.2.3. Chemical Manufcaturing

- 7.2.4. Mining & Mineral Processing

- 7.2.5. Mining and Mineral Processing

- 7.2.6. Food & Beverage

- 7.2.7. Pulp & Ppaer

- 7.2.8. Others

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Argentina South America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Flocculant & Coagulants

- 8.1.2. Biocides & Disinfectants

- 8.1.3. Defoamers & Defoaming Agents

- 8.1.4. pH & Adjusters & Softeners

- 8.1.5. Scale & Corrosion Inhibitors

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Power

- 8.2.2. Oil & Gas

- 8.2.3. Chemical Manufcaturing

- 8.2.4. Mining & Mineral Processing

- 8.2.5. Mining and Mineral Processing

- 8.2.6. Food & Beverage

- 8.2.7. Pulp & Ppaer

- 8.2.8. Others

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Rest of South America South America Water Treatment Chemicals Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Flocculant & Coagulants

- 9.1.2. Biocides & Disinfectants

- 9.1.3. Defoamers & Defoaming Agents

- 9.1.4. pH & Adjusters & Softeners

- 9.1.5. Scale & Corrosion Inhibitors

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Power

- 9.2.2. Oil & Gas

- 9.2.3. Chemical Manufcaturing

- 9.2.4. Mining & Mineral Processing

- 9.2.5. Mining and Mineral Processing

- 9.2.6. Food & Beverage

- 9.2.7. Pulp & Ppaer

- 9.2.8. Others

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Argentina

- 9.3.3. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Nouryon

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Ecolab

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Solenis

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Kemira

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Solvay

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Lonza

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Kurita Water industries Ltd

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 SNF

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Suez*List Not Exhaustive

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Nouryon

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global South America Water Treatment Chemicals Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Brazil South America Water Treatment Chemicals Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 3: Brazil South America Water Treatment Chemicals Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: Brazil South America Water Treatment Chemicals Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Brazil South America Water Treatment Chemicals Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Brazil South America Water Treatment Chemicals Industry Revenue (billion), by Geography 2025 & 2033

- Figure 7: Brazil South America Water Treatment Chemicals Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 8: Brazil South America Water Treatment Chemicals Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Brazil South America Water Treatment Chemicals Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Argentina South America Water Treatment Chemicals Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 11: Argentina South America Water Treatment Chemicals Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: Argentina South America Water Treatment Chemicals Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 13: Argentina South America Water Treatment Chemicals Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 14: Argentina South America Water Treatment Chemicals Industry Revenue (billion), by Geography 2025 & 2033

- Figure 15: Argentina South America Water Treatment Chemicals Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 16: Argentina South America Water Treatment Chemicals Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Argentina South America Water Treatment Chemicals Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Rest of South America South America Water Treatment Chemicals Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 19: Rest of South America South America Water Treatment Chemicals Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 20: Rest of South America South America Water Treatment Chemicals Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 21: Rest of South America South America Water Treatment Chemicals Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 22: Rest of South America South America Water Treatment Chemicals Industry Revenue (billion), by Geography 2025 & 2033

- Figure 23: Rest of South America South America Water Treatment Chemicals Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 24: Rest of South America South America Water Treatment Chemicals Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of South America South America Water Treatment Chemicals Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 7: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 10: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 11: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: Global South America Water Treatment Chemicals Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Water Treatment Chemicals Industry?

The projected CAGR is approximately 7.4%.

2. Which companies are prominent players in the South America Water Treatment Chemicals Industry?

Key companies in the market include Nouryon, Ecolab, Solenis, Kemira, Solvay, Lonza, Kurita Water industries Ltd, SNF, Suez*List Not Exhaustive.

3. What are the main segments of the South America Water Treatment Chemicals Industry?

The market segments include Product Type, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.9 billion as of 2022.

5. What are some drivers contributing to market growth?

; Conformance to Stringent Environmental Regulations; Other Drivers.

6. What are the notable trends driving market growth?

Oil & Gas Industry to Dominate the Market.

7. Are there any restraints impacting market growth?

; Conformance to Stringent Environmental Regulations; Other Drivers.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Water Treatment Chemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Water Treatment Chemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Water Treatment Chemicals Industry?

To stay informed about further developments, trends, and reports in the South America Water Treatment Chemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence