Key Insights

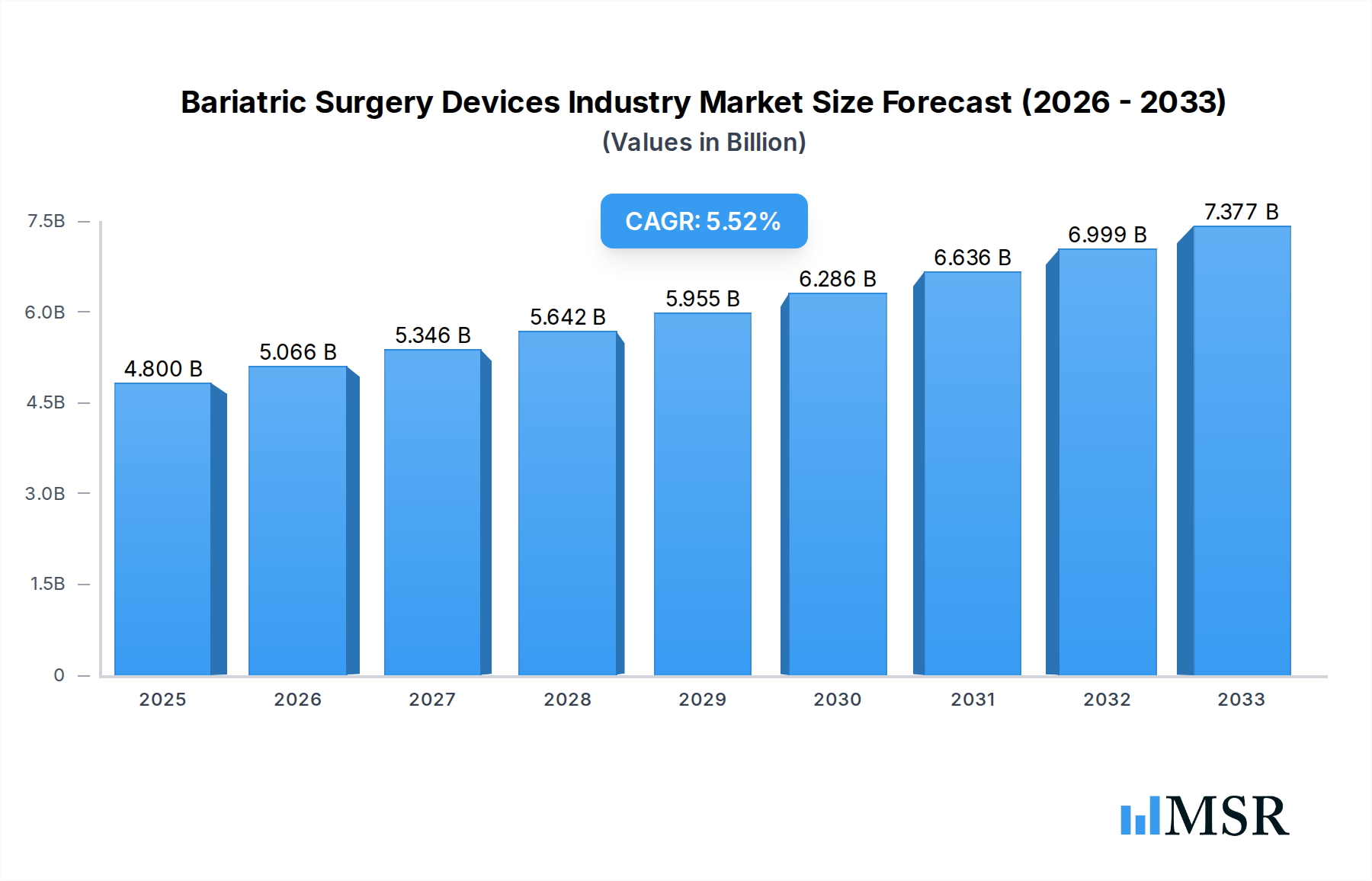

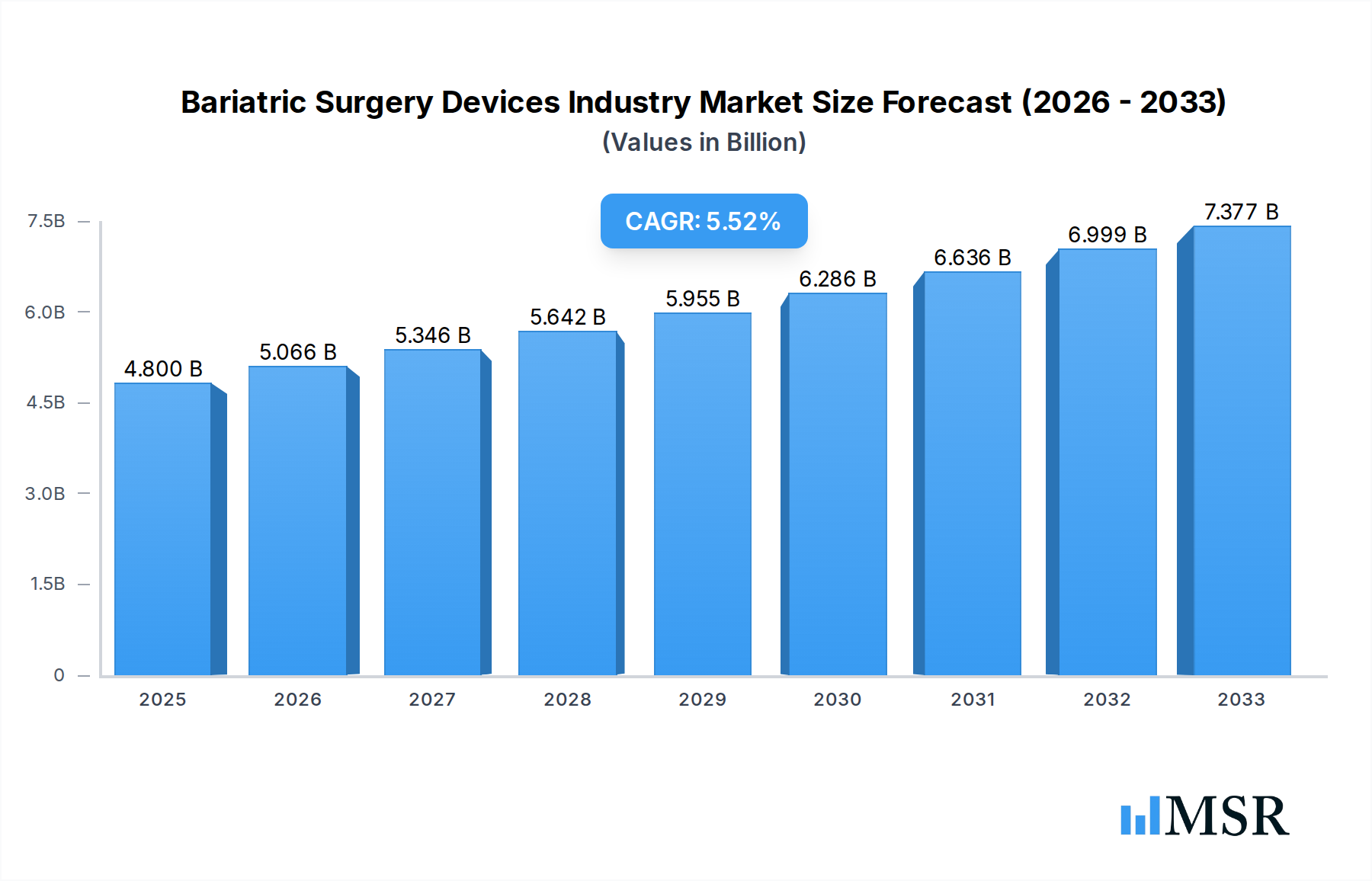

The global Bariatric Surgery Devices market is poised for substantial growth, projected to reach USD 4.8 billion in 2025, with a compelling Compound Annual Growth Rate (CAGR) of 5.46% through 2033. This upward trajectory is primarily fueled by the escalating global prevalence of obesity and its associated comorbidities, such as type 2 diabetes, hypertension, and cardiovascular diseases. Increased public awareness regarding the long-term health benefits and improved quality of life offered by bariatric surgery further acts as a significant market driver. Technological advancements in surgical devices, including the development of less invasive and more precise instruments like advanced stapling devices, robotic-assisted surgical systems, and novel implantable devices, are also contributing to market expansion by enhancing patient outcomes and reducing recovery times. The increasing adoption of these sophisticated devices by healthcare professionals and their subsequent reimbursement by insurance providers are also critical factors bolstering market momentum.

Bariatric Surgery Devices Industry Market Size (In Billion)

Despite the robust growth, certain restraints may temper the market's full potential. High costs associated with bariatric surgery and the devices themselves can limit accessibility for a significant portion of the population, particularly in developing economies. Furthermore, the availability of alternative weight-loss solutions, including pharmacological treatments and intensive lifestyle interventions, could pose a competitive challenge. However, the growing preference for minimally invasive procedures and the continuous innovation pipeline for more effective and affordable bariatric surgery devices are expected to outweigh these limitations. Key segments driving this growth include assisting devices, with stapling and closure devices witnessing significant demand, and implantable devices, with gastric balloons and electrical stimulation devices gaining traction due to their non-invasive nature and positive patient feedback.

Bariatric Surgery Devices Industry Company Market Share

Bariatric Surgery Devices Industry Market Report: Dominance, Innovation, and Future Growth (2019-2033)

This comprehensive report delves into the dynamic bariatric surgery devices market, a critical segment within the medical devices industry. Covering the historical period (2019-2024), base year (2025), and forecast period (2025-2033), this analysis provides actionable insights for medical device manufacturers, healthcare providers, investors, and industry stakeholders. We explore market concentration, key growth drivers, leading segments, product innovations, prevailing challenges, and emerging opportunities, offering a strategic outlook on the global bariatric surgery devices market. The report is essential for understanding the evolving landscape of obesity treatment devices, minimally invasive surgery tools, and implantable devices for weight loss.

Bariatric Surgery Devices Industry Market Concentration & Dynamics

The bariatric surgery devices industry exhibits a moderate level of market concentration, with key players like Ethicon Inc (Johnson and Johnson), Medtronic PLC, and Intuitive Surgical Inc holding significant market shares. The innovation ecosystem is driven by continuous research and development focused on improving patient outcomes, minimizing invasiveness, and enhancing device functionality. Regulatory frameworks, primarily governed by agencies like the FDA and EMA, play a crucial role in product approval and market access, influencing the pace of innovation. Substitute products, such as non-surgical weight loss interventions, pose a competitive threat but the demand for effective surgical solutions continues to grow. End-user trends are increasingly favoring minimally invasive procedures and patient-specific treatment options. Mergers and acquisition (M&A) activities, though not rampant, are strategic, aimed at expanding product portfolios and market reach. For instance, key M&A deals in the broader medical device market often spill over into the bariatric sector, consolidating capabilities and expertise. The market size is projected to reach over $6 billion by 2025, with M&A deal counts in the broader sector averaging 10-15 significant transactions annually.

Bariatric Surgery Devices Industry Industry Insights & Trends

The bariatric surgery devices market is poised for significant expansion, driven by the escalating global obesity epidemic and a growing awareness of its associated health risks. The market size is projected to exceed $9 billion by 2033, with a robust Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period. Technological disruptions are at the forefront of market evolution, with advancements in minimally invasive surgical instruments, robotic-assisted surgery, and smart implantable devices revolutionizing treatment modalities. The increasing adoption of bariatric surgery as a viable and effective long-term weight management solution, coupled with favorable reimbursement policies in developed economies, further fuels market growth. Evolving consumer behaviors reflect a growing demand for less invasive procedures with faster recovery times, pushing manufacturers to innovate and develop novel endoscopic bariatric devices and implantable gastric balloons. The prevalence of obesity worldwide, currently impacting over 1.5 billion individuals, directly translates to a burgeoning patient pool seeking effective bariatric interventions. Furthermore, the development of bariatric stapling devices and closure devices with enhanced safety features and improved surgical precision is a key trend shaping the market landscape. The rising prevalence of comorbidities like diabetes, hypertension, and cardiovascular diseases, often linked to obesity, also acts as a significant market driver, encouraging healthcare systems to invest more in bariatric interventions. The average length of hospital stay post-bariatric surgery has also seen a considerable reduction due to these technological advancements, making the procedures more appealing to both patients and healthcare providers.

Key Markets & Segments Leading Bariatric Surgery Devices Industry

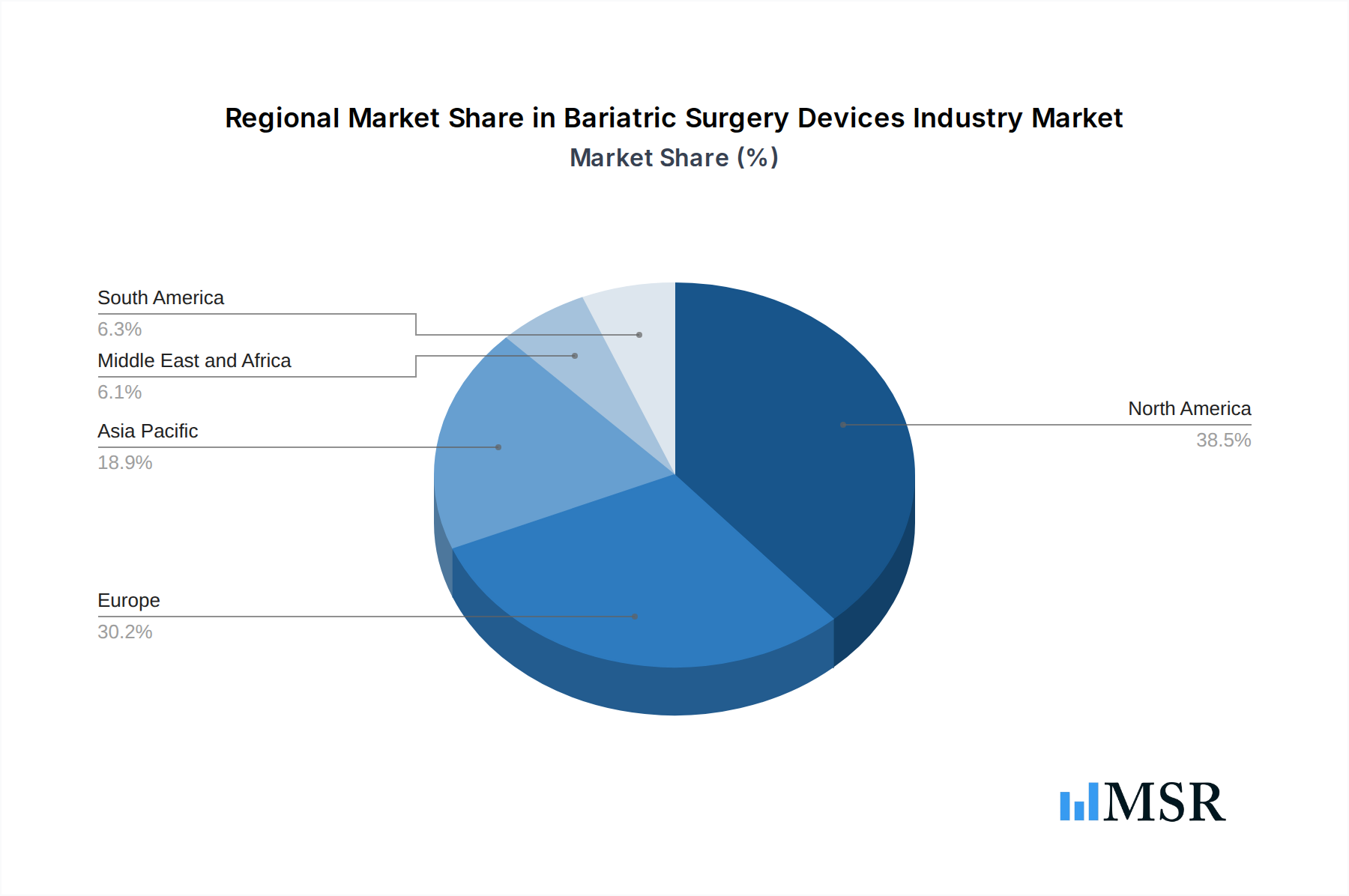

The bariatric surgery devices market is spearheaded by North America, particularly the United States, owing to its high prevalence of obesity, advanced healthcare infrastructure, and substantial healthcare spending. Economic growth and rising disposable incomes in emerging economies in Asia-Pacific and Latin America are also contributing to market expansion, albeit at a different pace.

- Assisting Devices: This segment is a dominant force, driven by the widespread use of stapling devices, suturing devices, and trocars in various bariatric procedures.

- Drivers: Increasing procedural volumes, demand for precision and safety in surgeries, and technological innovations leading to more efficient and less invasive instruments.

- Stapling Devices: These are integral to common procedures like sleeve gastrectomy and gastric bypass, witnessing continuous upgrades in terms of firing speed, staple line security, and ergonomic design. The market for advanced articulated staplers is particularly strong.

- Suturing Devices: Crucial for creating secure anastomoses and closing incisions, innovation here focuses on absorbable sutures and automated suturing systems to reduce surgical time and improve consistency.

- Trocars: Essential for laparoscopic access, the trend is towards smaller diameter and bladeless trocars to minimize port site complications and improve patient comfort.

- Implantable Devices: This segment is experiencing robust growth, with gastric balloons and gastric emptying devices gaining traction.

- Drivers: Growing preference for reversible and less invasive weight loss solutions, development of improved materials for longer implant durations, and increasing clinical evidence supporting their efficacy.

- Gastric Balloons: Devices like the Apollo ESG and Apollo REVISE, which received de novo authorization, exemplify the innovation in this space, offering non-surgical endoscopic solutions for obesity. The market is witnessing the introduction of dual balloon systems and balloons designed for longer indwelling periods.

- Gastric Emptying Devices: Emerging technologies aimed at improving gastric emptying offer a novel approach to weight management.

- Other Devices: This category includes a range of specialized instruments and accessories used in bariatric surgery, contributing to the overall market volume.

The adoption of robotic-assisted surgery further bolsters the demand for sophisticated assisting devices, integrating advanced technology into bariatric procedures. The reimbursement landscape in key markets significantly influences the uptake of these advanced devices.

Bariatric Surgery Devices Industry Product Developments

Product development in the bariatric surgery devices industry is characterized by a relentless pursuit of enhanced safety, efficacy, and patient experience. Innovations focus on creating more intuitive and ergonomic surgical instruments, advanced materials for implantable devices, and integrated technologies that improve procedural outcomes. The development of anatomical stapler technology, as exemplified by Standard Bariatrics, Inc.'s Titan SGS completing 1,000 clinical case uses, showcases a commitment to patient benefit through precise, anatomy-based approaches in bariatric surgery. Furthermore, the FDA's de novo authorization for Apollo Endosurgery's Apollo ESG and Apollo REVISE endoscopic systems highlights the significant advancements in less invasive, endoscopic bariatric solutions for obesity treatment. These product developments are crucial for maintaining a competitive edge and addressing the evolving needs of both surgeons and patients.

Challenges in the Bariatric Surgery Devices Industry Market

The bariatric surgery devices market faces several challenges that can hinder its growth trajectory. High initial costs associated with advanced surgical equipment and implantable devices can limit accessibility, particularly in developing economies. Stringent regulatory approvals by health authorities, while ensuring patient safety, can lead to extended product launch timelines and significant R&D investment. Reimbursement challenges and variations across different healthcare systems also pose a barrier to widespread adoption. Furthermore, the availability of skilled surgeons trained in performing complex bariatric procedures and the risk of complications associated with any surgical intervention remain ongoing concerns that impact market growth. Supply chain disruptions, as experienced globally in recent years, can also affect the availability and cost of essential medical devices.

Forces Driving Bariatric Surgery Devices Industry Growth

Several potent forces are propelling the growth of the bariatric surgery devices industry. The escalating global prevalence of obesity and related comorbidities creates a continuous and expanding patient pool demanding effective weight management solutions. Technological advancements, particularly in minimally invasive surgery and robotic-assisted surgery, are making procedures safer, more effective, and less daunting for patients, thus increasing adoption rates. Favorable reimbursement policies in developed nations for bariatric procedures are a significant economic driver. Growing awareness among patients and healthcare providers about the long-term health benefits and improved quality of life following successful bariatric surgery also contributes to market expansion. The development of innovative implantable devices and endoscopic solutions further broadens treatment options and enhances market appeal.

Challenges in the Bariatric Surgery Devices Industry Market

Long-term growth catalysts for the bariatric surgery devices industry lie in the continuous innovation of less invasive and reversible procedures, aimed at reducing patient risk and accelerating recovery times. The development of AI-powered surgical tools and smart implantable devices that offer real-time patient monitoring and personalized treatment adjustments holds immense potential. Strategic partnerships between device manufacturers and healthcare institutions for clinical research and training will foster wider adoption and product refinement. Expanding into emerging markets with tailored product offerings and accessible pricing models will unlock significant growth opportunities. Furthermore, advancements in biomaterials for implants and a focus on creating more cost-effective solutions will be crucial for sustainable long-term growth in this vital sector.

Emerging Opportunities in Bariatric Surgery Devices Industry

Emerging opportunities within the bariatric surgery devices industry are abundant, driven by evolving patient needs and technological frontiers. The increasing demand for non-surgical bariatric interventions presents a significant opportunity for endoscopic devices like gastric balloons and gastric emptying systems. The integration of digital health technologies, such as remote patient monitoring and AI-driven treatment adherence programs, can enhance post-operative care and patient outcomes. Expansion into underserved geographic regions with high obesity rates but limited access to advanced surgical care offers considerable growth potential. Furthermore, the development of personalized bariatric solutions tailored to individual patient physiology and metabolic profiles will likely become a key differentiator. The growing interest in sleeve gastroplasty devices and advancements in bariatric sealant technologies also represent lucrative avenues for innovation and market penetration.

Leading Players in the Bariatric Surgery Devices Industry Sector

- The Cooper Companies

- Ethicon Inc (Johnson and Johnson)

- Medtronic PLC

- Apollo Endosurgery Inc

- Cousin Biotech

- Intuitive Surgical Inc

- Conmed Corporation

- B Braun Melsungen AG

- Cook Medical

- Olympus Corporation

- Aspire Bariatrics Inc

Key Milestones in Bariatric Surgery Devices Industry Industry

- January 2022: Standard Bariatrics, Inc.'s Titan SGS surgical stapler technology successfully completed 1,000 clinical case uses, demonstrating the benefits of its anatomy-based approach in bariatric surgery.

- July 2021: The Food and Drug Administration (FDA) granted de novo authorization to Apollo Endosurgery for its Apollo ESG and Apollo REVISE endoscopic systems, expanding treatment options for patients with obesity.

Strategic Outlook for Bariatric Surgery Devices Industry Market

The strategic outlook for the bariatric surgery devices market is exceptionally positive, driven by a confluence of factors including the persistent global obesity crisis, rapid technological advancements, and a growing acceptance of bariatric surgery as a life-changing intervention. Key growth accelerators include the continued innovation in minimally invasive and robotic-assisted surgical platforms, enhancing precision and patient recovery. The burgeoning field of endoscopic bariatric devices offers a non-surgical avenue, significantly broadening market accessibility. Furthermore, strategic investments in research and development focused on implantable devices with improved safety profiles and longer lifespans will be crucial. Expanding market penetration into emerging economies by addressing affordability and accessibility challenges will unlock substantial future potential. The industry is poised for sustained growth, driven by a commitment to improving patient outcomes and addressing the complex healthcare needs associated with obesity.

Bariatric Surgery Devices Industry Segmentation

-

1. Device

-

1.1. Assisting Devices

- 1.1.1. Suturing Device

- 1.1.2. Closure Device

- 1.1.3. Stapling Device

- 1.1.4. Trocars

- 1.1.5. Other Assisting Devices

-

1.2. Implantable Devices

- 1.2.1. Gastric Bands

- 1.2.2. Electrical Stimulation Devices

- 1.2.3. Gastric Balloons

- 1.2.4. Gastric Emptying

- 1.3. Other Devices

-

1.1. Assisting Devices

Bariatric Surgery Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. Spain

- 2.4. Italy

- 2.5. France

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Bariatric Surgery Devices Industry Regional Market Share

Geographic Coverage of Bariatric Surgery Devices Industry

Bariatric Surgery Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.46% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Device

- 5.1.1. Assisting Devices

- 5.1.1.1. Suturing Device

- 5.1.1.2. Closure Device

- 5.1.1.3. Stapling Device

- 5.1.1.4. Trocars

- 5.1.1.5. Other Assisting Devices

- 5.1.2. Implantable Devices

- 5.1.2.1. Gastric Bands

- 5.1.2.2. Electrical Stimulation Devices

- 5.1.2.3. Gastric Balloons

- 5.1.2.4. Gastric Emptying

- 5.1.3. Other Devices

- 5.1.1. Assisting Devices

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Middle East and Africa

- 5.2.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Device

- 6. Global Bariatric Surgery Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Device

- 6.1.1. Assisting Devices

- 6.1.1.1. Suturing Device

- 6.1.1.2. Closure Device

- 6.1.1.3. Stapling Device

- 6.1.1.4. Trocars

- 6.1.1.5. Other Assisting Devices

- 6.1.2. Implantable Devices

- 6.1.2.1. Gastric Bands

- 6.1.2.2. Electrical Stimulation Devices

- 6.1.2.3. Gastric Balloons

- 6.1.2.4. Gastric Emptying

- 6.1.3. Other Devices

- 6.1.1. Assisting Devices

- 6.1. Market Analysis, Insights and Forecast - by Device

- 7. North America Bariatric Surgery Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Device

- 7.1.1. Assisting Devices

- 7.1.1.1. Suturing Device

- 7.1.1.2. Closure Device

- 7.1.1.3. Stapling Device

- 7.1.1.4. Trocars

- 7.1.1.5. Other Assisting Devices

- 7.1.2. Implantable Devices

- 7.1.2.1. Gastric Bands

- 7.1.2.2. Electrical Stimulation Devices

- 7.1.2.3. Gastric Balloons

- 7.1.2.4. Gastric Emptying

- 7.1.3. Other Devices

- 7.1.1. Assisting Devices

- 7.1. Market Analysis, Insights and Forecast - by Device

- 8. Europe Bariatric Surgery Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Device

- 8.1.1. Assisting Devices

- 8.1.1.1. Suturing Device

- 8.1.1.2. Closure Device

- 8.1.1.3. Stapling Device

- 8.1.1.4. Trocars

- 8.1.1.5. Other Assisting Devices

- 8.1.2. Implantable Devices

- 8.1.2.1. Gastric Bands

- 8.1.2.2. Electrical Stimulation Devices

- 8.1.2.3. Gastric Balloons

- 8.1.2.4. Gastric Emptying

- 8.1.3. Other Devices

- 8.1.1. Assisting Devices

- 8.1. Market Analysis, Insights and Forecast - by Device

- 9. Asia Pacific Bariatric Surgery Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Device

- 9.1.1. Assisting Devices

- 9.1.1.1. Suturing Device

- 9.1.1.2. Closure Device

- 9.1.1.3. Stapling Device

- 9.1.1.4. Trocars

- 9.1.1.5. Other Assisting Devices

- 9.1.2. Implantable Devices

- 9.1.2.1. Gastric Bands

- 9.1.2.2. Electrical Stimulation Devices

- 9.1.2.3. Gastric Balloons

- 9.1.2.4. Gastric Emptying

- 9.1.3. Other Devices

- 9.1.1. Assisting Devices

- 9.1. Market Analysis, Insights and Forecast - by Device

- 10. Middle East and Africa Bariatric Surgery Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Device

- 10.1.1. Assisting Devices

- 10.1.1.1. Suturing Device

- 10.1.1.2. Closure Device

- 10.1.1.3. Stapling Device

- 10.1.1.4. Trocars

- 10.1.1.5. Other Assisting Devices

- 10.1.2. Implantable Devices

- 10.1.2.1. Gastric Bands

- 10.1.2.2. Electrical Stimulation Devices

- 10.1.2.3. Gastric Balloons

- 10.1.2.4. Gastric Emptying

- 10.1.3. Other Devices

- 10.1.1. Assisting Devices

- 10.1. Market Analysis, Insights and Forecast - by Device

- 11. South America Bariatric Surgery Devices Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Device

- 11.1.1. Assisting Devices

- 11.1.1.1. Suturing Device

- 11.1.1.2. Closure Device

- 11.1.1.3. Stapling Device

- 11.1.1.4. Trocars

- 11.1.1.5. Other Assisting Devices

- 11.1.2. Implantable Devices

- 11.1.2.1. Gastric Bands

- 11.1.2.2. Electrical Stimulation Devices

- 11.1.2.3. Gastric Balloons

- 11.1.2.4. Gastric Emptying

- 11.1.3. Other Devices

- 11.1.1. Assisting Devices

- 11.1. Market Analysis, Insights and Forecast - by Device

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 The Cooper Companies

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ethicon Inc (Johnson and Johnson)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Medtronic PLC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Apollo Endosurgery Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cousin Biotech

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Intuitive Surgical Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Conmed Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 B Braun Melsungen AG

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Cook Medical

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Olympus Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Aspire Bariatrics Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 The Cooper Companies

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Bariatric Surgery Devices Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Bariatric Surgery Devices Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Bariatric Surgery Devices Industry Revenue (billion), by Device 2025 & 2033

- Figure 4: North America Bariatric Surgery Devices Industry Volume (K Unit), by Device 2025 & 2033

- Figure 5: North America Bariatric Surgery Devices Industry Revenue Share (%), by Device 2025 & 2033

- Figure 6: North America Bariatric Surgery Devices Industry Volume Share (%), by Device 2025 & 2033

- Figure 7: North America Bariatric Surgery Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 8: North America Bariatric Surgery Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 9: North America Bariatric Surgery Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Bariatric Surgery Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: Europe Bariatric Surgery Devices Industry Revenue (billion), by Device 2025 & 2033

- Figure 12: Europe Bariatric Surgery Devices Industry Volume (K Unit), by Device 2025 & 2033

- Figure 13: Europe Bariatric Surgery Devices Industry Revenue Share (%), by Device 2025 & 2033

- Figure 14: Europe Bariatric Surgery Devices Industry Volume Share (%), by Device 2025 & 2033

- Figure 15: Europe Bariatric Surgery Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: Europe Bariatric Surgery Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: Europe Bariatric Surgery Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Bariatric Surgery Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Asia Pacific Bariatric Surgery Devices Industry Revenue (billion), by Device 2025 & 2033

- Figure 20: Asia Pacific Bariatric Surgery Devices Industry Volume (K Unit), by Device 2025 & 2033

- Figure 21: Asia Pacific Bariatric Surgery Devices Industry Revenue Share (%), by Device 2025 & 2033

- Figure 22: Asia Pacific Bariatric Surgery Devices Industry Volume Share (%), by Device 2025 & 2033

- Figure 23: Asia Pacific Bariatric Surgery Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Asia Pacific Bariatric Surgery Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Asia Pacific Bariatric Surgery Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Bariatric Surgery Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Middle East and Africa Bariatric Surgery Devices Industry Revenue (billion), by Device 2025 & 2033

- Figure 28: Middle East and Africa Bariatric Surgery Devices Industry Volume (K Unit), by Device 2025 & 2033

- Figure 29: Middle East and Africa Bariatric Surgery Devices Industry Revenue Share (%), by Device 2025 & 2033

- Figure 30: Middle East and Africa Bariatric Surgery Devices Industry Volume Share (%), by Device 2025 & 2033

- Figure 31: Middle East and Africa Bariatric Surgery Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Middle East and Africa Bariatric Surgery Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Middle East and Africa Bariatric Surgery Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Bariatric Surgery Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: South America Bariatric Surgery Devices Industry Revenue (billion), by Device 2025 & 2033

- Figure 36: South America Bariatric Surgery Devices Industry Volume (K Unit), by Device 2025 & 2033

- Figure 37: South America Bariatric Surgery Devices Industry Revenue Share (%), by Device 2025 & 2033

- Figure 38: South America Bariatric Surgery Devices Industry Volume Share (%), by Device 2025 & 2033

- Figure 39: South America Bariatric Surgery Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 40: South America Bariatric Surgery Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 41: South America Bariatric Surgery Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Bariatric Surgery Devices Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Device 2020 & 2033

- Table 2: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Device 2020 & 2033

- Table 3: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 5: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Device 2020 & 2033

- Table 6: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Device 2020 & 2033

- Table 7: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 9: United States Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: United States Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 11: Canada Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 13: Mexico Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Mexico Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Device 2020 & 2033

- Table 16: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Device 2020 & 2033

- Table 17: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Germany Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Spain Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Spain Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Italy Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Italy Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: France Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: France Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Device 2020 & 2033

- Table 32: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Device 2020 & 2033

- Table 33: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 35: China Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: China Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Japan Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Japan Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: India Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: India Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Australia Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Australia Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: South Korea Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: South Korea Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Rest of Asia Pacific Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Device 2020 & 2033

- Table 48: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Device 2020 & 2033

- Table 49: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: GCC Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: GCC Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: South Africa Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: South Africa Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Rest of Middle East and Africa Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: Rest of Middle East and Africa Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Device 2020 & 2033

- Table 58: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Device 2020 & 2033

- Table 59: Global Bariatric Surgery Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Bariatric Surgery Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: Brazil Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Brazil Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Argentina Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Argentina Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of South America Bariatric Surgery Devices Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Rest of South America Bariatric Surgery Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Bariatric Surgery Devices Industry?

The projected CAGR is approximately 5.46%.

2. Which companies are prominent players in the Bariatric Surgery Devices Industry?

Key companies in the market include The Cooper Companies, Ethicon Inc (Johnson and Johnson), Medtronic PLC, Apollo Endosurgery Inc, Cousin Biotech, Intuitive Surgical Inc, Conmed Corporation, B Braun Melsungen AG, Cook Medical, Olympus Corporation, Aspire Bariatrics Inc.

3. What are the main segments of the Bariatric Surgery Devices Industry?

The market segments include Device.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.8 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Obesity Patients; Prevalence Rate of Type 2 Diabetes and Heart Diseases; Government Initiatives to Curb Obesity.

6. What are the notable trends driving market growth?

Gastric Balloons is Expected to Record a High CAGR in the Implantable Device Segment.

7. Are there any restraints impacting market growth?

High Cost of Surgery; Lack of Knowledge and Awareness in Developing and Underdeveloped Countries.

8. Can you provide examples of recent developments in the market?

In January 2022, Standard Bariatrics, Inc.'s Titan SGS has successfully completed 1,000 clinical case uses. The anatomy-based approach of Titan SGS surgical stapler technology in bariatric surgery is benefiting patients.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Bariatric Surgery Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Bariatric Surgery Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Bariatric Surgery Devices Industry?

To stay informed about further developments, trends, and reports in the Bariatric Surgery Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence