Key Insights

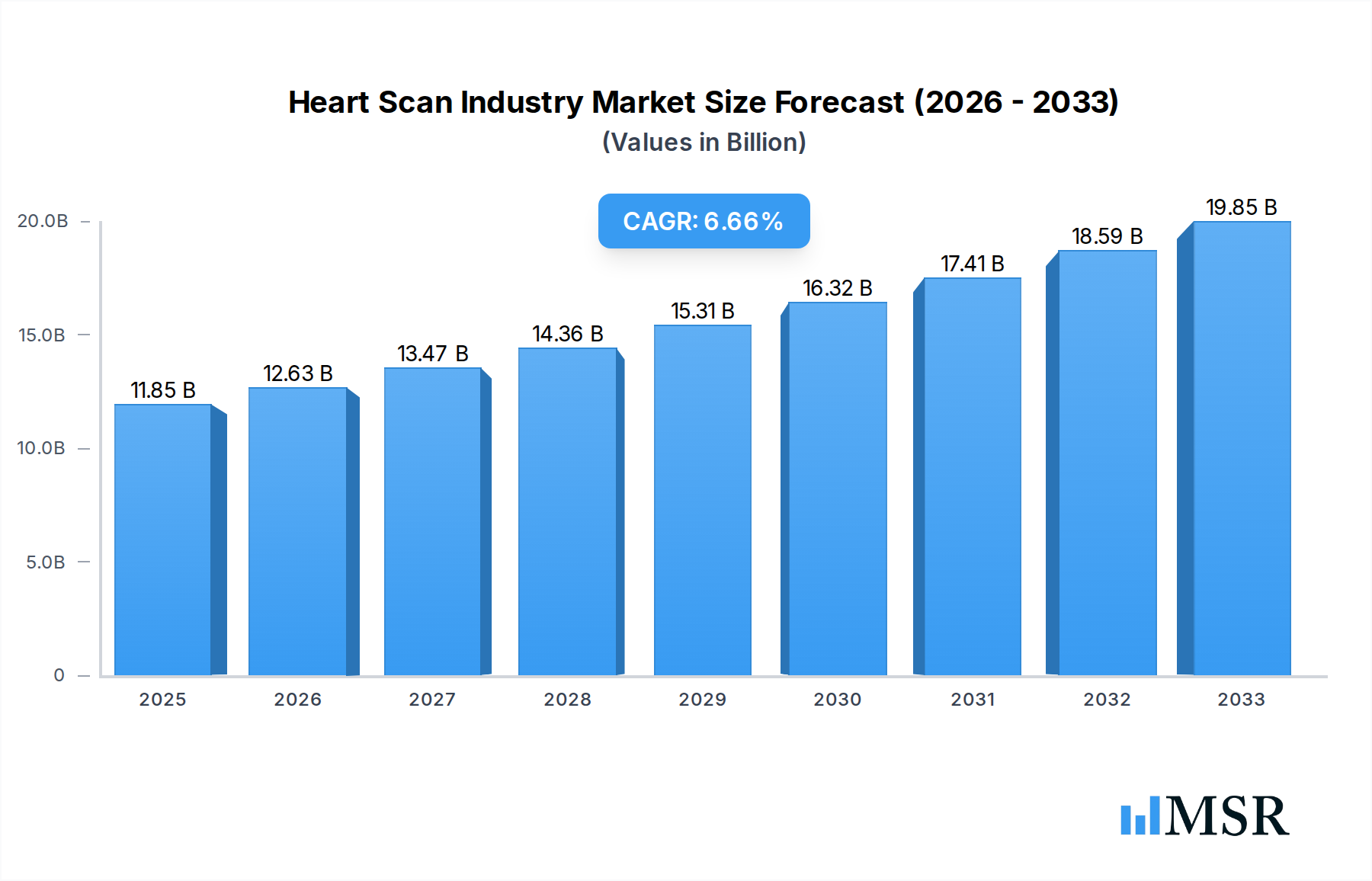

The global Heart Scan Industry is poised for substantial growth, projected to reach an estimated USD 11.85 billion in 2025, with a robust CAGR of 6.2% anticipated throughout the forecast period (2025-2033). This expansion is driven by a confluence of factors including the increasing prevalence of cardiovascular diseases (CVDs) worldwide, growing awareness among the population regarding heart health, and significant advancements in diagnostic imaging technologies. As CVDs remain a leading cause of mortality, the demand for accurate and timely diagnostic tools like electrocardiograms (ECG), blood tests, angiograms, and cardiac CT scans is steadily rising. Furthermore, the aging global population, coupled with lifestyle changes such as sedentary habits and unhealthy diets, contributes to a higher incidence of cardiac conditions, further fueling market growth. Healthcare providers are also increasingly investing in advanced imaging equipment to improve diagnostic accuracy and patient outcomes, thereby supporting market expansion.

Heart Scan Industry Market Size (In Billion)

The market's growth trajectory is also influenced by the evolving healthcare landscape, with a greater emphasis on preventive care and early detection. This is leading to increased adoption of heart scans in various healthcare settings, from large hospitals to smaller diagnostic centers and ambulatory surgical centers. The competitive landscape features prominent players like Siemens Healthineers, GE Healthcare, and Koninklijke Philips NV, who are continuously innovating and launching new products and solutions to meet the growing demand. While the market exhibits strong upward momentum, certain factors such as the high cost of advanced imaging equipment and the need for skilled personnel to operate them could present moderate restraints. However, the overall outlook remains highly positive, underscoring the critical role of heart scans in modern healthcare and their expanding market potential.

Heart Scan Industry Company Market Share

This in-depth report provides a definitive analysis of the global Heart Scan Industry, offering critical insights into market dynamics, technological advancements, and growth trajectories. Covering the study period of 2019–2033, with a base year of 2025, this comprehensive report forecasts the market size to reach an estimated value of xx billion by 2033. We delve into key segments including Electrocardiogram (ECG), Blood Tests, Angiogram, Computerized Cardiac Tomography (CCT), and Other Tests, alongside end-user segments such as Hospitals, Ambulatory Surgical Centers, Diagnostic Centers, and Other End Users. This report is an essential resource for stakeholders seeking to navigate the evolving landscape of cardiovascular diagnostics, from leading players like Siemens Healthineers and GE Healthcare to emerging innovators.

Heart Scan Industry Market Concentration & Dynamics

The Heart Scan Industry exhibits a moderate to high level of market concentration, driven by significant investments in research and development and the stringent regulatory approval processes for advanced diagnostic technologies. Key players such as Siemens Healthineers, GE Healthcare, and Koninklijke Philips NV dominate a substantial portion of the market share, leveraging their extensive product portfolios and established global distribution networks. The innovation ecosystem is characterized by continuous advancements in imaging resolution, AI-driven analytics, and less invasive diagnostic techniques. Regulatory frameworks, primarily governed by bodies like the FDA and EMA, play a crucial role in shaping market entry and product development, emphasizing safety and efficacy. Substitute products, while present in the form of less sophisticated screening methods, are increasingly being outperformed by advanced heart scan technologies in terms of diagnostic accuracy and predictive capabilities. End-user trends are shifting towards preventative care and early disease detection, fueling demand for more precise and accessible diagnostic solutions. Mergers and acquisitions (M&A) activities, with an estimated xx M&A deals in the historical period, are strategically employed by larger companies to acquire innovative technologies and expand their market reach.

- Market Share Dominance: Leading players like Siemens Healthineers, GE Healthcare, and Koninklijke Philips NV hold significant market share.

- Innovation Ecosystem: Focused on AI, high-resolution imaging, and non-invasive diagnostics.

- Regulatory Frameworks: FDA and EMA approval are critical for market access.

- Substitute Products: Basic screening methods face increasing competition from advanced scans.

- End-User Trends: Growing demand for preventative care and early detection.

- M&A Activities: Approximately xx M&A deals in the historical period 2019-2024, facilitating market consolidation and technological acquisition.

Heart Scan Industry Industry Insights & Trends

The global Heart Scan Industry is poised for robust growth, projected to reach an estimated market size of xx billion by 2033, with a compound annual growth rate (CAGR) of approximately xx% during the forecast period (2025–2033). This expansion is propelled by several interconnected factors. A primary driver is the escalating global prevalence of cardiovascular diseases (CVDs), including heart attacks and strokes, which necessitates early and accurate diagnosis. This demographic shift, coupled with an aging global population, directly fuels the demand for advanced diagnostic tools and services. Technological disruptions are fundamentally reshaping the industry. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into diagnostic imaging is revolutionizing the interpretation of scans, enabling faster, more accurate, and predictive diagnoses. AI-powered solutions can now identify subtle patterns indicative of future cardiac events years in advance, transforming preventative cardiology. Furthermore, the development of novel imaging techniques, such as ultra-high-field MRI and advanced CT angiography, offers unprecedented detail and clarity, allowing for more precise assessments of cardiac structure and function. Evolving consumer behaviors also play a significant role. There is a pronounced shift towards proactive health management and a greater awareness of cardiovascular risk factors. This has led to an increased demand for regular health check-ups and diagnostic screenings, particularly among individuals with a family history of heart disease or those exhibiting lifestyle-related risk factors. The growing adoption of telemedicine and remote diagnostics is further expanding access to heart scan services, especially in underserved regions, contributing to market growth. Moreover, reimbursement policies and government initiatives aimed at improving cardiovascular healthcare infrastructure and patient outcomes are creating a favorable market environment. The increasing investment in healthcare by both public and private sectors underscores the commitment to enhancing diagnostic capabilities and reducing the burden of heart disease.

Key Markets & Segments Leading Heart Scan Industry

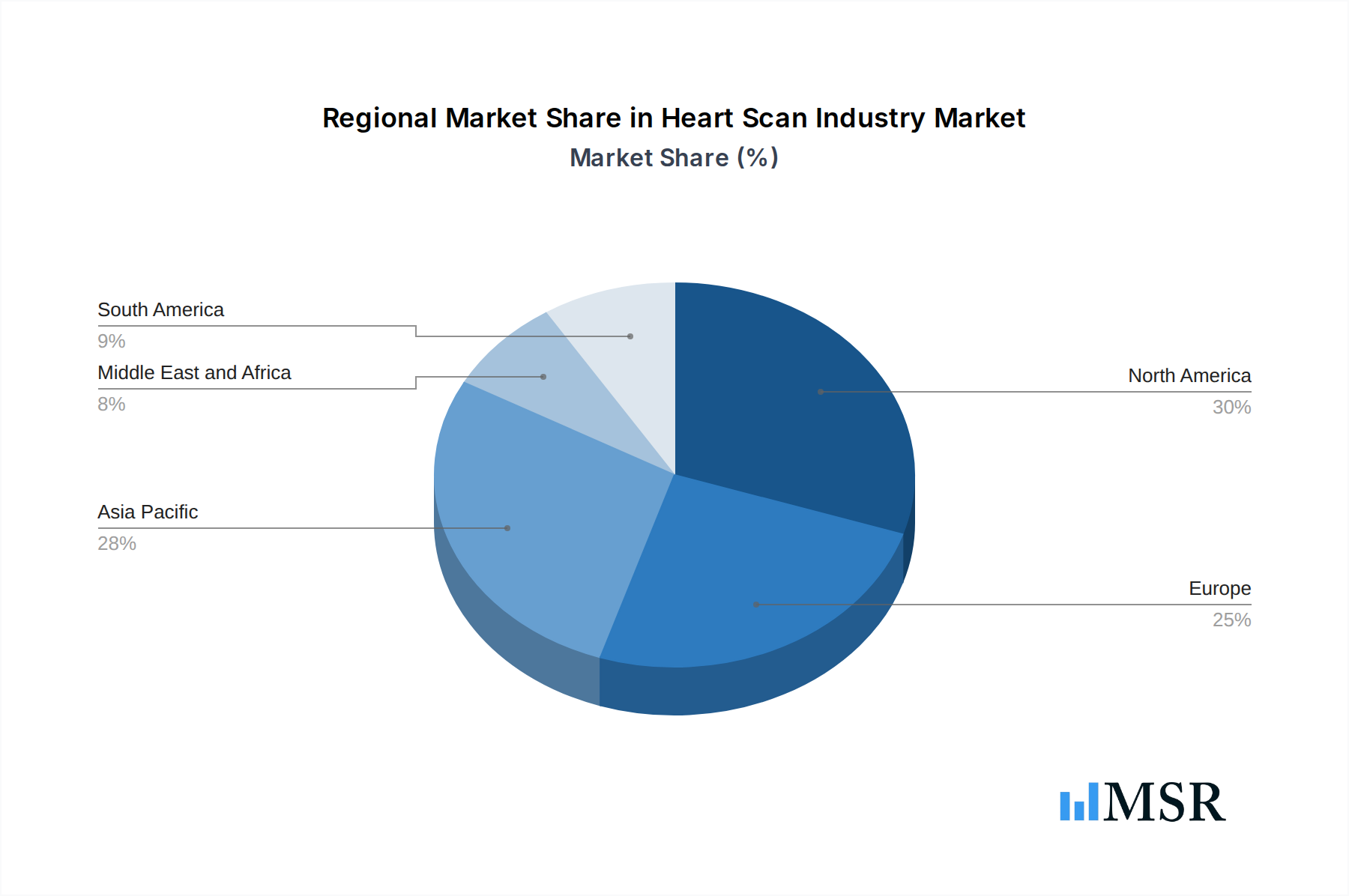

The Heart Scan Industry is experiencing significant growth across various key markets and segments, with North America and Europe currently leading in terms of market share due to advanced healthcare infrastructure and high adoption rates of sophisticated diagnostic technologies. The United States, in particular, stands out due to its high healthcare expenditure and proactive approach to cardiovascular disease management. Asia Pacific is emerging as a rapidly growing market, driven by increasing disposable incomes, a rising prevalence of lifestyle-related diseases, and significant investments in healthcare infrastructure.

Dominant Segments by Test:

- Electrocardiogram (ECG): Remains a foundational diagnostic tool, widely accessible and cost-effective for initial cardiac assessment. Its continued use in primary care and routine check-ups ensures consistent demand.

- Drivers: Ubiquitous availability, affordability, essential for baseline cardiac rhythm assessment.

- Blood Tests (Cardiac Biomarkers): Tests like troponin and NT-proBNP are critical for diagnosing acute cardiac events and assessing heart failure. The development of highly sensitive assays, as exemplified by Roche's recent launches, is enhancing their diagnostic accuracy.

- Drivers: Crucial for acute myocardial infarction diagnosis, advancements in biomarker detection sensitivity.

- Angiogram (Coronary Angiography): Remains the gold standard for visualizing blockages in coronary arteries, guiding interventional procedures.

- Drivers: Definitive visualization of coronary artery disease, essential for revascularization decisions.

- Computerized Cardiac Tomography (CCT): Including CCT angiography and calcium scoring, CCT offers non-invasive visualization of coronary arteries and calcium buildup, providing valuable prognostic information. The AI-driven CaRi-Heart Technology's approval by the EU signifies the growing predictive power of CCT.

- Drivers: Non-invasive assessment of coronary arteries and plaque burden, predictive risk stratification capabilities.

- Other Tests: This broad category includes echocardiography, stress tests, and cardiac MRI, each offering unique insights into cardiac function, structure, and perfusion.

- Drivers: Comprehensive assessment of cardiac structure and function, complementary diagnostic information.

Dominant Segments by End User:

- Hospitals: Represent the largest end-user segment, owing to their comprehensive cardiac care units, specialized equipment, and a high volume of patient admissions requiring diagnostic evaluations.

- Drivers: Centralized cardiac care, availability of advanced diagnostic suites, high patient throughput.

- Diagnostic Centers: These facilities are increasingly investing in advanced heart scan technologies to cater to the growing demand for outpatient cardiac diagnostics and preventative screenings.

- Drivers: Growing demand for outpatient diagnostic services, specialized focus on cardiac imaging.

- Ambulatory Surgical Centers (ASCs): While historically focused on procedures, ASCs are expanding their diagnostic capabilities, including some non-invasive cardiac imaging, to offer integrated patient care.

- Drivers: Integrated care models, increasing scope of diagnostic services offered.

- Other End Users: This includes research institutions, academic medical centers, and specialized cardiology clinics that utilize advanced heart scanning for research, training, and specialized patient care.

- Drivers: Advanced research capabilities, specialized clinical practice, educational purposes.

Heart Scan Industry Product Developments

The Heart Scan Industry is witnessing a continuous stream of product innovations, significantly enhancing diagnostic capabilities and patient care. Advancements in imaging technology, such as higher resolution scanners and faster acquisition times for CT and MRI, allow for more detailed visualization of cardiac structures and pathologies. The integration of Artificial Intelligence (AI) is a major trend, with AI algorithms now capable of automating image analysis, detecting subtle anomalies, and predicting disease progression with remarkable accuracy. For instance, the EU's approval of AI-based CaRi-Heart Technology underscores its potential to revolutionize early heart attack prediction. Furthermore, the development of more sensitive and specific cardiac biomarkers, exemplified by Roche's new Elecsys® applications for troponin T and NT-proBNP, is crucial for improved early diagnosis of myocardial damage and heart failure. These developments collectively enhance diagnostic precision, reduce invasiveness, and improve patient outcomes, providing a competitive edge to companies investing in R&D.

Challenges in the Heart Scan Industry Market

The Heart Scan Industry faces several significant challenges that can impact its growth trajectory. Regulatory hurdles remain a constant, with the rigorous approval processes for new diagnostic technologies and devices demanding substantial time and investment. The high cost of advanced imaging equipment and associated consumables can be a barrier to adoption, especially in resource-limited settings. Additionally, the scarcity of skilled personnel, including radiographers and cardiologists proficient in operating and interpreting advanced heart scan technologies, poses a significant challenge. Competitive pressures are intense, with numerous players vying for market share, often leading to price erosion for certain diagnostic services. Furthermore, the integration of disparate data streams from various diagnostic modalities and electronic health records presents interoperability issues, hindering seamless patient data management and analysis.

- Regulatory Hurdles: Lengthy and costly approval processes for new technologies.

- High Equipment Costs: Significant capital investment required for advanced imaging systems.

- Skilled Workforce Shortage: Difficulty in finding and retaining trained professionals.

- Intense Competition: Leading to price pressures and market saturation.

- Data Interoperability Issues: Challenges in integrating data from multiple sources.

Forces Driving Heart Scan Industry Growth

Several potent forces are driving the significant growth observed in the Heart Scan Industry. The escalating global burden of cardiovascular diseases, including heart attacks and strokes, is a primary catalyst, creating an urgent need for early and accurate diagnostic solutions. An aging global population further exacerbates this trend, as older individuals are more susceptible to cardiac conditions. Technological innovation is another major growth driver. The rapid integration of Artificial Intelligence (AI) and machine learning into diagnostic imaging is enhancing accuracy, efficiency, and predictive capabilities. For example, AI-powered tools are enabling earlier detection of subtle cardiac abnormalities, thereby facilitating timely intervention. Furthermore, advancements in imaging modalities, such as higher resolution CT and MRI scanners and novel echocardiography techniques, are providing unprecedented insights into cardiac health. Growing health consciousness and a shift towards preventative healthcare are also fueling demand for regular cardiac screenings and early detection services.

Challenges in the Heart Scan Industry Market

While growth is robust, the Heart Scan Industry navigates several long-term growth catalysts that are crucial for sustained expansion. Ongoing research and development efforts are continuously pushing the boundaries of diagnostic technology, leading to more precise, less invasive, and more predictive heart scan solutions. This innovation pipeline is essential for addressing unmet clinical needs and expanding the market. Strategic partnerships and collaborations between technology providers, healthcare institutions, and research organizations are fostering a more integrated approach to cardiovascular care and accelerating the adoption of new technologies. Market expansion into emerging economies, where the prevalence of cardiovascular diseases is rising and healthcare infrastructure is developing, presents a significant long-term growth opportunity. Government initiatives and increasing healthcare expenditure in these regions are creating a conducive environment for the penetration of advanced heart scan solutions.

Emerging Opportunities in Heart Scan Industry

The Heart Scan Industry is ripe with emerging opportunities poised to shape its future. The growing demand for personalized medicine is opening doors for advanced cardiac diagnostics that can tailor treatment plans based on individual patient risk profiles and genetic predispositions. Wearable technology and remote patient monitoring devices, integrated with sophisticated analytics, offer a significant opportunity for continuous cardiac health tracking and early detection of anomalies outside traditional clinical settings. The expanding role of Artificial Intelligence (AI) in predicting cardiovascular events years in advance, as demonstrated by technologies like CaRi-Heart, presents a transformative opportunity in preventative cardiology. Furthermore, the development of novel, less invasive imaging techniques and contrast agents will further enhance patient comfort and compliance, driving adoption. The focus on value-based healthcare is also creating opportunities for diagnostic solutions that can demonstrate improved patient outcomes and cost-effectiveness.

Leading Players in the Heart Scan Industry Sector

- Schiller AG

- Toshiba Corporation

- Siemens Healthineers

- Hitachi Corporation

- GE Healthcare

- F Hoffmann-La Roche Ltd

- Midmark Corporation

- Koninklijke Philips NV

- Astrazenca PLC

- Welch Allyn Inc

Key Milestones in Heart Scan Industry Industry

- April 2021: Roche launched five new intended uses for its Elecsys® technology, enhancing the diagnostic capabilities of highly sensitive cardiac troponin T (cTnT-hs) and N-terminal pro-brain natriuretic peptide test (NT-proBNP) for cardiac biomarker assessment.

- March 2021: The European Union approved the artificial intelligence-based CaRi-Heart Technology, developed by the British Heart Foundation and Caristo Diagnostics, for detecting and predicting the risk of severe heart attack years in advance.

Strategic Outlook for Heart Scan Industry Market

The strategic outlook for the Heart Scan Industry remains exceptionally positive, driven by an intensifying focus on preventative healthcare and early disease detection. Growth accelerators will be rooted in continued technological innovation, particularly in the realm of AI-powered diagnostics and advanced imaging techniques that offer greater precision and predictive power. Expansion into emerging markets, characterized by a rising prevalence of cardiovascular diseases and increasing healthcare investments, represents a significant avenue for market penetration. Strategic partnerships and collaborations will be crucial for integrating diagnostic solutions into broader healthcare ecosystems and for co-developing next-generation technologies. The industry's ability to adapt to evolving regulatory landscapes and demonstrate the value proposition of its advanced solutions in terms of improved patient outcomes and cost-effectiveness will be key to sustained market leadership and expansion.

Heart Scan Industry Segmentation

-

1. Test

- 1.1. Electrocardiogram

- 1.2. Blood Tests

- 1.3. Angiogram

- 1.4. Computarized Cardiac Tomography

- 1.5. Other Tests

-

2. End User

- 2.1. Hospitals

- 2.2. Ambulatory Surgical Centers

- 2.3. Diagnostic Centers

- 2.4. Other End Users

Heart Scan Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Heart Scan Industry Regional Market Share

Geographic Coverage of Heart Scan Industry

Heart Scan Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Test

- 5.1.1. Electrocardiogram

- 5.1.2. Blood Tests

- 5.1.3. Angiogram

- 5.1.4. Computarized Cardiac Tomography

- 5.1.5. Other Tests

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Ambulatory Surgical Centers

- 5.2.3. Diagnostic Centers

- 5.2.4. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Test

- 6. Global Heart Scan Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Test

- 6.1.1. Electrocardiogram

- 6.1.2. Blood Tests

- 6.1.3. Angiogram

- 6.1.4. Computarized Cardiac Tomography

- 6.1.5. Other Tests

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Ambulatory Surgical Centers

- 6.2.3. Diagnostic Centers

- 6.2.4. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Test

- 7. North America Heart Scan Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Test

- 7.1.1. Electrocardiogram

- 7.1.2. Blood Tests

- 7.1.3. Angiogram

- 7.1.4. Computarized Cardiac Tomography

- 7.1.5. Other Tests

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Ambulatory Surgical Centers

- 7.2.3. Diagnostic Centers

- 7.2.4. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Test

- 8. Europe Heart Scan Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Test

- 8.1.1. Electrocardiogram

- 8.1.2. Blood Tests

- 8.1.3. Angiogram

- 8.1.4. Computarized Cardiac Tomography

- 8.1.5. Other Tests

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Ambulatory Surgical Centers

- 8.2.3. Diagnostic Centers

- 8.2.4. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Test

- 9. Asia Pacific Heart Scan Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Test

- 9.1.1. Electrocardiogram

- 9.1.2. Blood Tests

- 9.1.3. Angiogram

- 9.1.4. Computarized Cardiac Tomography

- 9.1.5. Other Tests

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Ambulatory Surgical Centers

- 9.2.3. Diagnostic Centers

- 9.2.4. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Test

- 10. Middle East and Africa Heart Scan Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Test

- 10.1.1. Electrocardiogram

- 10.1.2. Blood Tests

- 10.1.3. Angiogram

- 10.1.4. Computarized Cardiac Tomography

- 10.1.5. Other Tests

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Ambulatory Surgical Centers

- 10.2.3. Diagnostic Centers

- 10.2.4. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Test

- 11. South America Heart Scan Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Test

- 11.1.1. Electrocardiogram

- 11.1.2. Blood Tests

- 11.1.3. Angiogram

- 11.1.4. Computarized Cardiac Tomography

- 11.1.5. Other Tests

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals

- 11.2.2. Ambulatory Surgical Centers

- 11.2.3. Diagnostic Centers

- 11.2.4. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Test

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Schiller AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Toshiba Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Siemens Healthineers

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Hitachi Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 GE Healthcare

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 F Hoffmann-La Roche Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Midmark Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Koninklijke Philips NV

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Astrazenca PLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Welch Allyn Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Schiller AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Heart Scan Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Heart Scan Industry Revenue (billion), by Test 2025 & 2033

- Figure 3: North America Heart Scan Industry Revenue Share (%), by Test 2025 & 2033

- Figure 4: North America Heart Scan Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America Heart Scan Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Heart Scan Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Heart Scan Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Heart Scan Industry Revenue (billion), by Test 2025 & 2033

- Figure 9: Europe Heart Scan Industry Revenue Share (%), by Test 2025 & 2033

- Figure 10: Europe Heart Scan Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe Heart Scan Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Heart Scan Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Heart Scan Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Heart Scan Industry Revenue (billion), by Test 2025 & 2033

- Figure 15: Asia Pacific Heart Scan Industry Revenue Share (%), by Test 2025 & 2033

- Figure 16: Asia Pacific Heart Scan Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific Heart Scan Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Heart Scan Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Heart Scan Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Heart Scan Industry Revenue (billion), by Test 2025 & 2033

- Figure 21: Middle East and Africa Heart Scan Industry Revenue Share (%), by Test 2025 & 2033

- Figure 22: Middle East and Africa Heart Scan Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Middle East and Africa Heart Scan Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East and Africa Heart Scan Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Heart Scan Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Heart Scan Industry Revenue (billion), by Test 2025 & 2033

- Figure 27: South America Heart Scan Industry Revenue Share (%), by Test 2025 & 2033

- Figure 28: South America Heart Scan Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: South America Heart Scan Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: South America Heart Scan Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: South America Heart Scan Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Heart Scan Industry Revenue billion Forecast, by Test 2020 & 2033

- Table 2: Global Heart Scan Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Heart Scan Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Heart Scan Industry Revenue billion Forecast, by Test 2020 & 2033

- Table 5: Global Heart Scan Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Heart Scan Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Heart Scan Industry Revenue billion Forecast, by Test 2020 & 2033

- Table 11: Global Heart Scan Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Heart Scan Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Heart Scan Industry Revenue billion Forecast, by Test 2020 & 2033

- Table 20: Global Heart Scan Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Heart Scan Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Heart Scan Industry Revenue billion Forecast, by Test 2020 & 2033

- Table 29: Global Heart Scan Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Heart Scan Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Heart Scan Industry Revenue billion Forecast, by Test 2020 & 2033

- Table 35: Global Heart Scan Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 36: Global Heart Scan Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Heart Scan Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Heart Scan Industry?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Heart Scan Industry?

Key companies in the market include Schiller AG, Toshiba Corporation, Siemens Healthineers, Hitachi Corporation, GE Healthcare, F Hoffmann-La Roche Ltd, Midmark Corporation, Koninklijke Philips NV, Astrazenca PLC, Welch Allyn Inc.

3. What are the main segments of the Heart Scan Industry?

The market segments include Test, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.85 billion as of 2022.

5. What are some drivers contributing to market growth?

Technological Advancements; Significant Rise in Cardiovascular Diseases; Increase in Quality of Life.

6. What are the notable trends driving market growth?

Rapid Blood Tests like Troponin Expected to Occupy a Significant Market Share.

7. Are there any restraints impacting market growth?

Expensive Diagnostics Products; Lack of Skilled Workforce in the Hospitals and Other Areas.

8. Can you provide examples of recent developments in the market?

In April 2021, Roche launched a series of five new intended uses for two key cardiac biomarkers using the Elecsys® technology, i.e., highly sensitive cardiac troponin T (cTnT-hs) and N-terminal pro-brain natriuretic peptide test (NT-proBNP).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Heart Scan Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Heart Scan Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Heart Scan Industry?

To stay informed about further developments, trends, and reports in the Heart Scan Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence