Key Insights

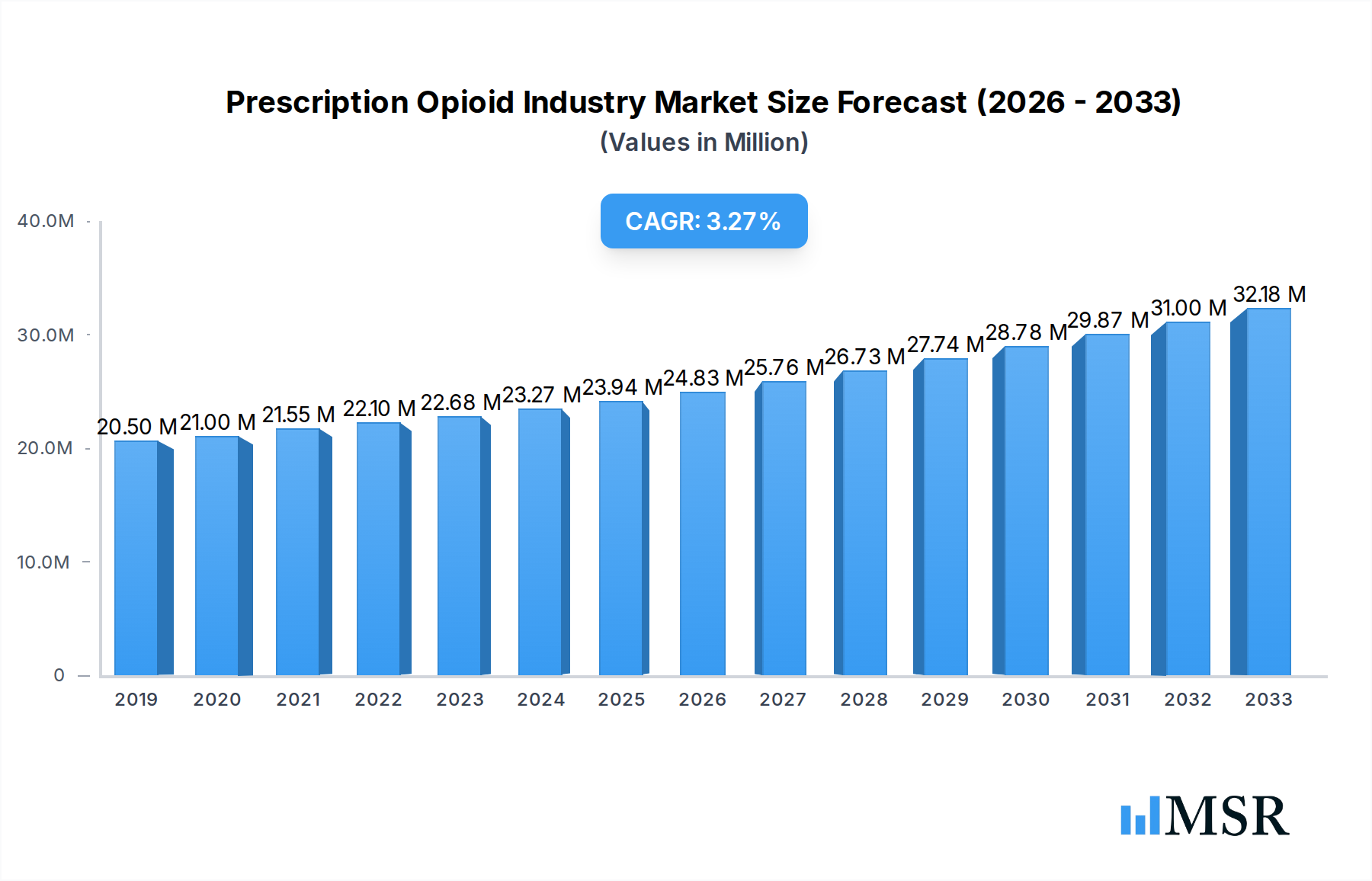

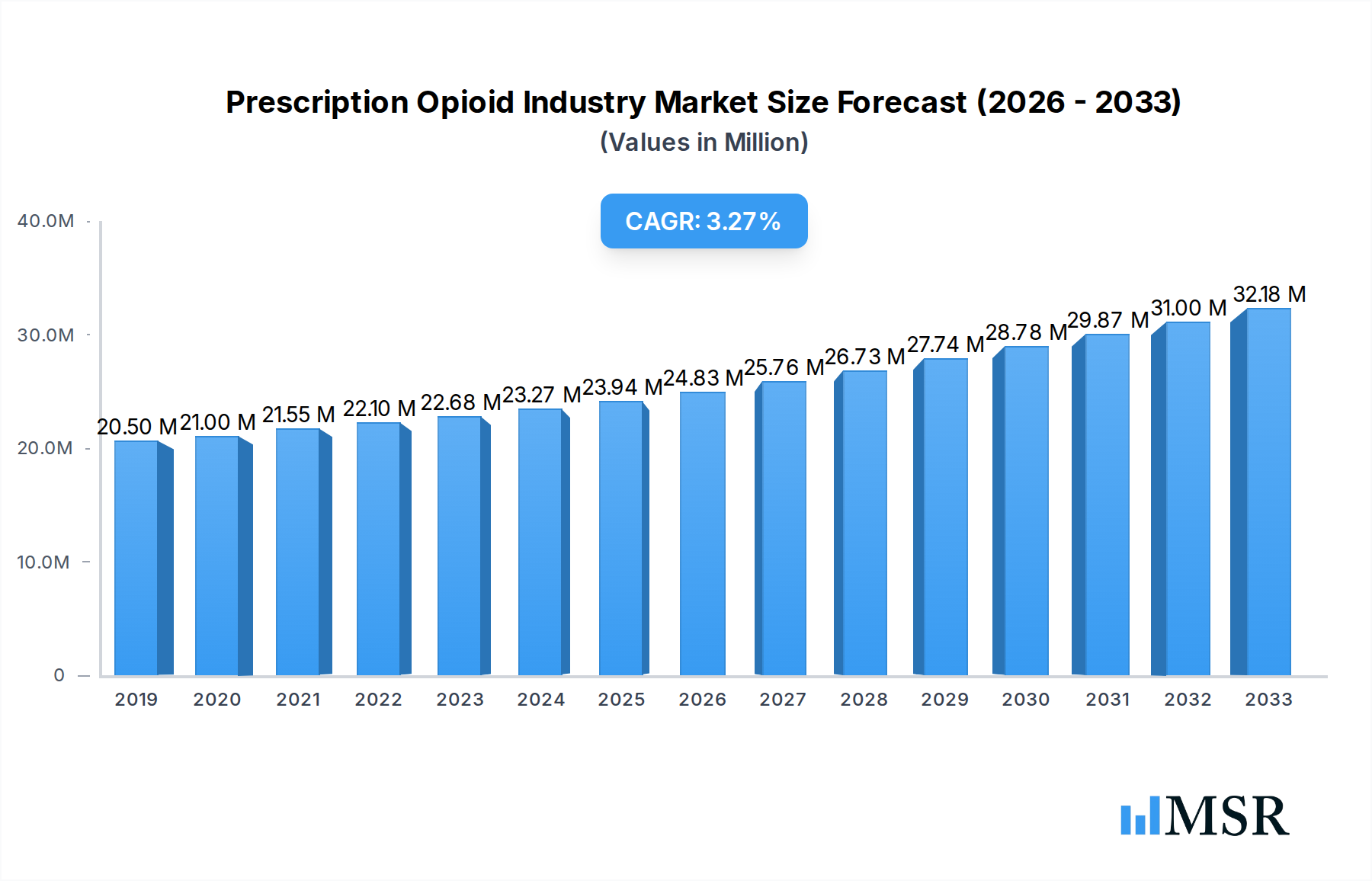

The global Prescription Opioid Industry is poised for steady growth, projected to reach $23.94 Million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 3.75% during the forecast period of 2025-2033. This expansion is primarily driven by the escalating prevalence of chronic pain conditions, including neuropathic pain and osteoarthritis, coupled with an aging global population that often requires effective pain management solutions. The increasing demand for potent analgesics for severe pain, particularly cancer-related pain, also significantly contributes to market dynamics. Furthermore, the segment for "Other Product Types" is expected to witness considerable development due to ongoing research and development efforts aimed at discovering novel opioid formulations with improved efficacy and reduced side effects. The Cold and Cough segment, though smaller, also presents a consistent revenue stream, amplified by the recurring nature of respiratory ailments.

Prescription Opioid Industry Market Size (In Million)

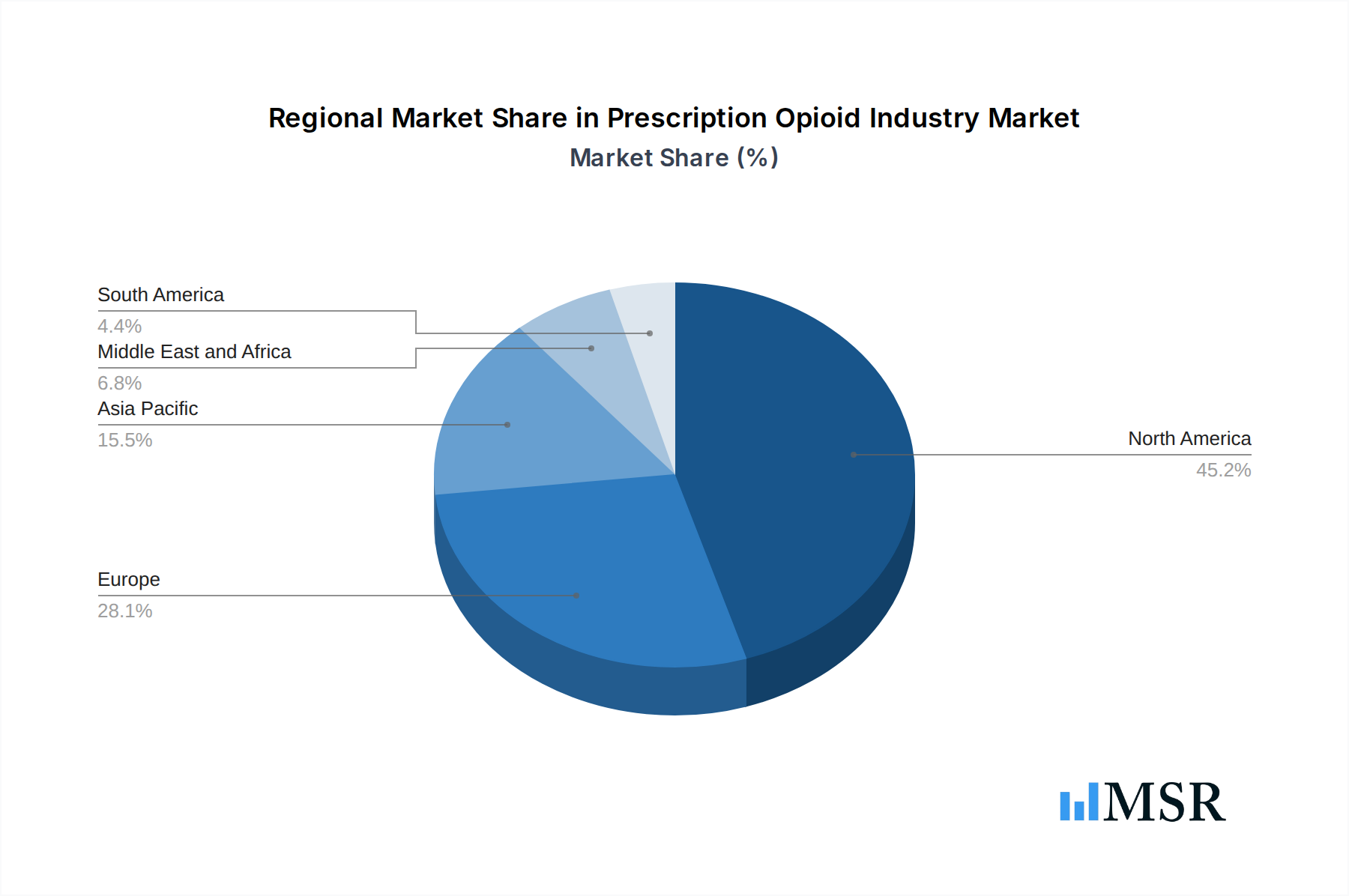

While the market benefits from strong drivers, it also faces certain restraints that warrant strategic consideration. Regulatory scrutiny and evolving guidelines surrounding opioid prescription and dispensing, aimed at curbing the opioid crisis, present a significant challenge. Heightened public awareness regarding the addictive potential of opioids and the subsequent push for non-opioid alternatives in pain management could temper overall market growth. However, the inherent efficacy of opioids for moderate to severe pain ensures their continued relevance, especially in settings where other treatments fall short. The Fentanyl and Codeine segments are expected to maintain their dominance due to their established therapeutic profiles and widespread use. North America and Europe are anticipated to remain the leading regions in terms of market share, owing to advanced healthcare infrastructure and a higher incidence of chronic pain disorders, though the Asia Pacific region is expected to exhibit the fastest growth rate driven by increasing healthcare expenditure and a growing patient pool.

Prescription Opioid Industry Company Market Share

This comprehensive report delves deep into the global Prescription Opioid Market, offering critical insights and actionable intelligence for pharmaceutical companies, healthcare providers, investors, and regulatory bodies. Analyzing the period from 2019 to 2033, with a base year of 2025, this report provides an in-depth examination of market dynamics, growth drivers, challenges, and emerging opportunities within the pain management market, oncology pain relief, and neuropathic pain treatments.

Prescription Opioid Industry Market Concentration & Dynamics

The Prescription Opioid Industry exhibits a moderate level of market concentration, with key players like Teva Pharmaceuticals Inc, Mallinckrodt Pharmaceuticals LLC, Purdue Pharmaceuticals L P, Johnson and Johnson, and Pfizer Inc holding significant market share. Innovation ecosystems are driven by ongoing research into novel analgesic formulations and delivery systems, particularly for managing chronic and severe pain conditions. Regulatory frameworks, including stringent FDA and EMA guidelines, significantly influence market entry and product development. Substitute products, such as non-opioid analgesics and alternative pain therapies, pose a competitive challenge. End-user trends are shifting towards demand for safer, non-addictive alternatives, prompting a focus on abuse-deterrent formulations and diversified pain management strategies. Merger and acquisition (M&A) activities, while subject to regulatory scrutiny, remain a strategic avenue for market consolidation and portfolio expansion. The market share of leading companies is estimated to be in the high single digits to low double digits for specific product segments. M&A deal counts have seen fluctuations, with an estimated 5-10 significant transactions annually during the historical period.

Prescription Opioid Industry Industry Insights & Trends

The global Prescription Opioid Market is poised for significant expansion, driven by an aging global population and the increasing prevalence of chronic pain conditions such as cancer pain, neuropathic pain, and osteoarthritis pain. The market size is projected to reach $XX Billion by 2033, with a Compound Annual Growth Rate (CAGR) of approximately X.X% during the forecast period (2025-2033). Technological disruptions, including advancements in targeted drug delivery systems and the development of potent yet safer opioid agonists, are reshaping the therapeutic landscape. Evolving consumer behaviors, influenced by increased awareness of opioid addiction risks and a growing preference for integrated pain management solutions, are prompting manufacturers to invest in responsible prescribing initiatives and alternative treatment options. The demand for effective pain management continues to be the primary growth driver, fueled by unmet medical needs in post-operative care and chronic debilitating conditions. The market is expected to witness substantial growth in the strong agonist segment, particularly for severe pain management, alongside continued development in mild to moderate agonist applications.

Key Markets & Segments Leading Prescription Opioid Industry

North America currently dominates the Prescription Opioid Market, driven by high healthcare expenditure, advanced medical infrastructure, and a significant prevalence of chronic pain disorders. The United States, in particular, represents a substantial market share.

Product Type Dominance:

- Fentanyl and Morphine are leading segments within the strong agonist category, essential for managing severe and acute pain, including cancer pain. Their widespread use in hospital settings and palliative care contributes to their market dominance.

- Codeine remains a significant product type, primarily utilized for moderate pain and as a component in cough suppressants, though its usage is increasingly scrutinized due to addiction potential.

- Methadone continues to play a crucial role in pain management and opioid addiction treatment, demonstrating consistent demand.

- Other Product Types are emerging, focusing on novel formulations and abuse-deterrent properties.

Receptor Binding Insights:

- Strong Agonists are critical for managing severe and intractable pain, particularly in applications like cancer pain and post-surgical recovery. Their high efficacy, despite associated risks, ensures their continued market presence.

- Mild to Moderate Agonists are vital for managing less severe pain conditions and are often preferred for their perceived lower risk profile, though careful patient selection remains paramount.

Application Landscape:

- Pain Management is the overarching application, with sub-segments like Cancer Pain, Neuropathic Pain, and Osteoarthritis Pain driving significant market volume. The increasing incidence of these conditions fuels sustained demand.

- Cold and Cough applications, while smaller, contribute to the overall demand for certain opioid compounds like codeine, albeit with increasing regulatory oversight.

- Diarrhoea management also utilizes some opioid derivatives, though this segment is less prominent compared to pain management.

Economic growth, an aging demographic, and advancements in pharmaceutical research are key drivers for the dominance of these segments. The continuous need for effective pain relief solutions across various chronic and acute conditions underpins the sustained demand for these opioid types and applications.

Prescription Opioid Industry Product Developments

Recent product developments in the Prescription Opioid Industry are characterized by a strong emphasis on innovation aimed at enhancing patient safety and therapeutic efficacy. Companies are actively pursuing the development of abuse-deterrent formulations (ADFs) to mitigate the risk of misuse and diversion. Novel delivery systems, such as extended-release formulations and transdermal patches, are being explored to provide more consistent pain relief and improve patient compliance. The introduction of new molecular entities with improved pharmacological profiles, offering potent analgesia with potentially fewer side effects, represents a key area of advancement. For instance, the recent FDA approval of novel IV analgesics signifies a push towards more targeted and effective acute pain management solutions, aiming to address severe pain requiring immediate intervention. These developments are crucial for maintaining market relevance and competitive advantage in an evolving regulatory and clinical environment.

Challenges in the Prescription Opioid Industry Market

The Prescription Opioid Industry faces significant challenges, primarily stemming from the ongoing opioid crisis and heightened regulatory scrutiny. Stringent regulations and evolving prescribing guidelines by bodies like the FDA and DEA can restrict market access and product promotion. Public perception and increasing awareness of addiction risks lead to a demand for non-opioid alternatives, pressuring manufacturers to innovate towards safer options. Supply chain complexities, including the sourcing of raw materials and the management of controlled substances, add operational hurdles. Competitive pressures from established players and emerging biotechnology firms developing novel pain therapies intensify market dynamics. Quantifiable impacts include potential revenue losses due to tighter controls and the significant investment required for research and development of abuse-deterrent formulations and non-opioid alternatives.

Forces Driving Prescription Opioid Industry Growth

Several key forces are driving growth in the Prescription Opioid Industry. The persistent and growing global burden of chronic pain, including conditions like cancer pain, neuropathic pain, and osteoarthritis pain, remains the primary demand generator. Advancements in pharmaceutical R&D are leading to the development of more targeted and potentially safer opioid formulations, including abuse-deterrent products, which are crucial for navigating regulatory hurdles and addressing prescriber concerns. An aging global population, with a higher propensity for developing chronic pain conditions, further fuels market expansion. Furthermore, the increasing acceptance of certain opioid formulations in post-operative pain management and palliative care continues to support market demand, provided they are prescribed responsibly and within established guidelines.

Challenges in the Prescription Opioid Industry Market

Long-term growth in the Prescription Opioid Industry hinges on several critical factors. Continued investment in research and development for novel analgesics that offer effective pain relief with a significantly improved safety profile is paramount. Strategic partnerships and collaborations between pharmaceutical companies, academic institutions, and pain management specialists can accelerate the discovery and development of innovative therapies. Market expansions into underserved regions with a growing demand for effective pain management, coupled with a focus on patient education and responsible prescribing practices, will be crucial for sustainable growth. The industry's ability to adapt to evolving regulatory landscapes and public health concerns by championing evidence-based pain management strategies will ultimately shape its long-term trajectory.

Emerging Opportunities in Prescription Opioid Industry

Emerging opportunities in the Prescription Opioid Industry lie in the development of non-addictive pain therapeutics and novel drug delivery systems. There is a significant unmet need for effective treatments for chronic pain that do not carry the risk of addiction, presenting a fertile ground for innovation. The exploration of alternative pain management modalities, including biologics and gene therapies, could redefine the landscape. Furthermore, the increasing focus on personalized medicine, tailoring pain treatments based on individual genetic profiles and pain mechanisms, offers a promising avenue for market growth. Digital health solutions and remote patient monitoring can also play a role in optimizing pain management and ensuring adherence to safer treatment regimens, opening new avenues for service integration and market penetration.

Leading Players in the Prescription Opioid Industry Sector

- Teva Pharmaceuticals Inc

- Mallinckrodt Pharmaceuticals LLC

- Purdue Pharmaceuticals L P

- AcelRx Pharmaceuticals Inc

- Zyla Life Sciences (Egalet Corporation)

- Alcaliber SA

- Hikma Pharmaceuticals PLC

- Johnson and Johnson

- Amneal Pharmaceuticals Inc

- Vertice Pharma LLC

- AbbVie Inc (Allergan PLC)

- Endo Pharmaceuticals Inc

- Sun Pharmaceutical Industries Ltd

- Pfizer Inc

Key Milestones in Prescription Opioid Industry Industry

- January 2022: Trevena, Inc. announced that China's National Medical Products Administration (NMPA) accepted the submission of a New Drug Application (NDA) for OLINVYK (oliceridine) injection, a novel IV analgesic, signaling global expansion efforts for advanced pain management.

- October 2021: Esteve Pharmaceuticals received approval from the United States Food and Drug Administration (FDA) for SEGLENTIS (celecoxib and tramadol hydrochloride) for the management of acute pain in adults severe enough to require an opioid analgesic, highlighting advancements in combination therapies for pain relief.

Strategic Outlook for Prescription Opioid Industry Market

The strategic outlook for the Prescription Opioid Market centers on innovation, responsible stewardship, and adaptation to evolving healthcare needs. Companies that prioritize the development of abuse-deterrent formulations and explore novel non-opioid analgesic pathways will be well-positioned for sustained growth. Strategic partnerships to advance research into the underlying mechanisms of pain and to develop personalized treatment approaches will be crucial. Furthermore, a commitment to robust pharmacovigilance, patient education, and collaborative efforts with healthcare providers and regulatory bodies to promote safe prescribing practices will be essential for navigating the complex regulatory environment and maintaining market access. Focusing on unmet medical needs in severe and chronic pain management, while simultaneously investing in alternatives, represents a balanced approach for future success.

Prescription Opioid Industry Segmentation

-

1. Product Type

- 1.1. Codeine

- 1.2. Fentanyl

- 1.3. Morphine

- 1.4. Meperidine

- 1.5. Methadone

- 1.6. Other Product Types

-

2. Receptor Binding

- 2.1. Strong Agonist

- 2.2. Mild to Moderate Agonist

-

3. Application

-

3.1. Pain Management

- 3.1.1. Cancer Pain

- 3.1.2. Neuropathic Pain

- 3.1.3. Osteoarthritis Pain

- 3.1.4. Other Pain Managements

- 3.2. Cold and Cough

- 3.3. Diarrhoea

- 3.4. Other Applications

-

3.1. Pain Management

Prescription Opioid Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Prescription Opioid Industry Regional Market Share

Geographic Coverage of Prescription Opioid Industry

Prescription Opioid Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Codeine

- 5.1.2. Fentanyl

- 5.1.3. Morphine

- 5.1.4. Meperidine

- 5.1.5. Methadone

- 5.1.6. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 5.2.1. Strong Agonist

- 5.2.2. Mild to Moderate Agonist

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Pain Management

- 5.3.1.1. Cancer Pain

- 5.3.1.2. Neuropathic Pain

- 5.3.1.3. Osteoarthritis Pain

- 5.3.1.4. Other Pain Managements

- 5.3.2. Cold and Cough

- 5.3.3. Diarrhoea

- 5.3.4. Other Applications

- 5.3.1. Pain Management

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Prescription Opioid Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Codeine

- 6.1.2. Fentanyl

- 6.1.3. Morphine

- 6.1.4. Meperidine

- 6.1.5. Methadone

- 6.1.6. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 6.2.1. Strong Agonist

- 6.2.2. Mild to Moderate Agonist

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Pain Management

- 6.3.1.1. Cancer Pain

- 6.3.1.2. Neuropathic Pain

- 6.3.1.3. Osteoarthritis Pain

- 6.3.1.4. Other Pain Managements

- 6.3.2. Cold and Cough

- 6.3.3. Diarrhoea

- 6.3.4. Other Applications

- 6.3.1. Pain Management

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Prescription Opioid Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Codeine

- 7.1.2. Fentanyl

- 7.1.3. Morphine

- 7.1.4. Meperidine

- 7.1.5. Methadone

- 7.1.6. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 7.2.1. Strong Agonist

- 7.2.2. Mild to Moderate Agonist

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Pain Management

- 7.3.1.1. Cancer Pain

- 7.3.1.2. Neuropathic Pain

- 7.3.1.3. Osteoarthritis Pain

- 7.3.1.4. Other Pain Managements

- 7.3.2. Cold and Cough

- 7.3.3. Diarrhoea

- 7.3.4. Other Applications

- 7.3.1. Pain Management

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Prescription Opioid Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Codeine

- 8.1.2. Fentanyl

- 8.1.3. Morphine

- 8.1.4. Meperidine

- 8.1.5. Methadone

- 8.1.6. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 8.2.1. Strong Agonist

- 8.2.2. Mild to Moderate Agonist

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Pain Management

- 8.3.1.1. Cancer Pain

- 8.3.1.2. Neuropathic Pain

- 8.3.1.3. Osteoarthritis Pain

- 8.3.1.4. Other Pain Managements

- 8.3.2. Cold and Cough

- 8.3.3. Diarrhoea

- 8.3.4. Other Applications

- 8.3.1. Pain Management

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Prescription Opioid Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Codeine

- 9.1.2. Fentanyl

- 9.1.3. Morphine

- 9.1.4. Meperidine

- 9.1.5. Methadone

- 9.1.6. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 9.2.1. Strong Agonist

- 9.2.2. Mild to Moderate Agonist

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Pain Management

- 9.3.1.1. Cancer Pain

- 9.3.1.2. Neuropathic Pain

- 9.3.1.3. Osteoarthritis Pain

- 9.3.1.4. Other Pain Managements

- 9.3.2. Cold and Cough

- 9.3.3. Diarrhoea

- 9.3.4. Other Applications

- 9.3.1. Pain Management

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Prescription Opioid Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Codeine

- 10.1.2. Fentanyl

- 10.1.3. Morphine

- 10.1.4. Meperidine

- 10.1.5. Methadone

- 10.1.6. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 10.2.1. Strong Agonist

- 10.2.2. Mild to Moderate Agonist

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Pain Management

- 10.3.1.1. Cancer Pain

- 10.3.1.2. Neuropathic Pain

- 10.3.1.3. Osteoarthritis Pain

- 10.3.1.4. Other Pain Managements

- 10.3.2. Cold and Cough

- 10.3.3. Diarrhoea

- 10.3.4. Other Applications

- 10.3.1. Pain Management

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. South America Prescription Opioid Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Codeine

- 11.1.2. Fentanyl

- 11.1.3. Morphine

- 11.1.4. Meperidine

- 11.1.5. Methadone

- 11.1.6. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Receptor Binding

- 11.2.1. Strong Agonist

- 11.2.2. Mild to Moderate Agonist

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Pain Management

- 11.3.1.1. Cancer Pain

- 11.3.1.2. Neuropathic Pain

- 11.3.1.3. Osteoarthritis Pain

- 11.3.1.4. Other Pain Managements

- 11.3.2. Cold and Cough

- 11.3.3. Diarrhoea

- 11.3.4. Other Applications

- 11.3.1. Pain Management

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Teva Pharmaceuticals Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Mallinckrodt Pharmaceuticals LLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Purdue Pharmaceuticals L P

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AcelRx Pharmaceuticals Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Zyla Life Sciences (Egalet Corporation)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Alcaliber SA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hikma Pharmaceuticals PLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Johnson and Johnson

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Amneal Pharmaceuticals Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Vertice Pharma LLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 AbbVie Inc (Allergan PLC)

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Endo Pharmaceuticals Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sun Pharmaceutical Industries Ltd

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Pfizer Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Teva Pharmaceuticals Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Prescription Opioid Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Prescription Opioid Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 4: North America Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 5: North America Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 8: North America Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 9: North America Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 10: North America Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 11: North America Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 12: North America Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 13: North America Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 15: North America Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 20: Europe Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 21: Europe Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Europe Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 23: Europe Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 24: Europe Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 25: Europe Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 26: Europe Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 27: Europe Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 28: Europe Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 29: Europe Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 36: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 37: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Asia Pacific Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 39: Asia Pacific Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 40: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 41: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 42: Asia Pacific Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 43: Asia Pacific Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 44: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Asia Pacific Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Asia Pacific Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 52: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 53: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 54: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 55: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 56: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 57: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 58: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 59: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 60: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 61: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 62: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 63: Middle East and Africa Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Middle East and Africa Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Prescription Opioid Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 68: South America Prescription Opioid Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 69: South America Prescription Opioid Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 70: South America Prescription Opioid Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 71: South America Prescription Opioid Industry Revenue (Million), by Receptor Binding 2025 & 2033

- Figure 72: South America Prescription Opioid Industry Volume (K Unit), by Receptor Binding 2025 & 2033

- Figure 73: South America Prescription Opioid Industry Revenue Share (%), by Receptor Binding 2025 & 2033

- Figure 74: South America Prescription Opioid Industry Volume Share (%), by Receptor Binding 2025 & 2033

- Figure 75: South America Prescription Opioid Industry Revenue (Million), by Application 2025 & 2033

- Figure 76: South America Prescription Opioid Industry Volume (K Unit), by Application 2025 & 2033

- Figure 77: South America Prescription Opioid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 78: South America Prescription Opioid Industry Volume Share (%), by Application 2025 & 2033

- Figure 79: South America Prescription Opioid Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Prescription Opioid Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Prescription Opioid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Prescription Opioid Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 3: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 4: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 5: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 7: Global Prescription Opioid Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Prescription Opioid Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 11: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 12: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 13: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 15: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 24: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 25: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 26: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 27: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 44: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 45: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 46: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 47: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 48: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 49: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 64: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 65: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 66: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 67: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 68: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 69: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: GCC Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: South Africa Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Prescription Opioid Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 78: Global Prescription Opioid Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 79: Global Prescription Opioid Industry Revenue Million Forecast, by Receptor Binding 2020 & 2033

- Table 80: Global Prescription Opioid Industry Volume K Unit Forecast, by Receptor Binding 2020 & 2033

- Table 81: Global Prescription Opioid Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 82: Global Prescription Opioid Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 83: Global Prescription Opioid Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 84: Global Prescription Opioid Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: Brazil Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: Argentina Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Prescription Opioid Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Prescription Opioid Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Prescription Opioid Industry?

The projected CAGR is approximately 3.75%.

2. Which companies are prominent players in the Prescription Opioid Industry?

Key companies in the market include Teva Pharmaceuticals Inc, Mallinckrodt Pharmaceuticals LLC, Purdue Pharmaceuticals L P, AcelRx Pharmaceuticals Inc, Zyla Life Sciences (Egalet Corporation), Alcaliber SA, Hikma Pharmaceuticals PLC, Johnson and Johnson, Amneal Pharmaceuticals Inc, Vertice Pharma LLC, AbbVie Inc (Allergan PLC), Endo Pharmaceuticals Inc, Sun Pharmaceutical Industries Ltd, Pfizer Inc.

3. What are the main segments of the Prescription Opioid Industry?

The market segments include Product Type, Receptor Binding, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 23.94 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Orthopedic Diseases and Chronic Pain; Inclination toward Extended Release Formulations from Immediate Release of Opioids; Rising Focus on Abuse-deterrent Formulation (ADF) by Generic Manufacturers.

6. What are the notable trends driving market growth?

Strong Agonists are Expected to Hold Significant Market Share in the Receptor Binding Segment.

7. Are there any restraints impacting market growth?

Advent and Legalization of Cannabis as an Alternative to Opioids; Prescription Drug Abuse.

8. Can you provide examples of recent developments in the market?

In January 2022, Trevena, Inc. announced that China's National Medical Products Administration (NMPA) has accepted the submission of a New Drug Application (NDA) for OLINVYK (oliceridine) injection, a novel IV analgesic that has been approved in the United States by the Food and Drug Administration (FDA) for use in adults for the management of acute pain severe enough to require an intravenous opioid analgesic

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Prescription Opioid Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Prescription Opioid Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Prescription Opioid Industry?

To stay informed about further developments, trends, and reports in the Prescription Opioid Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence