Key Insights

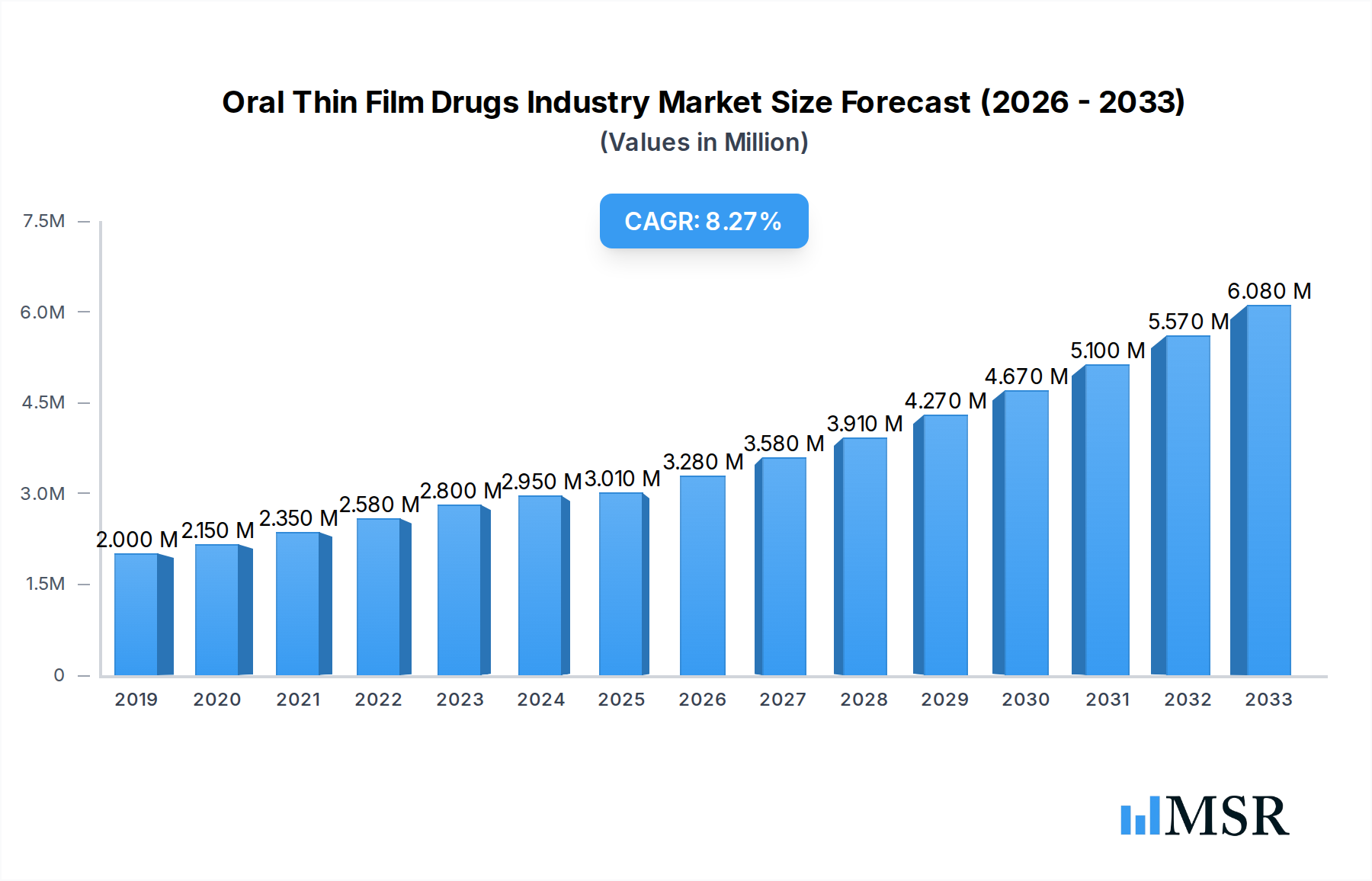

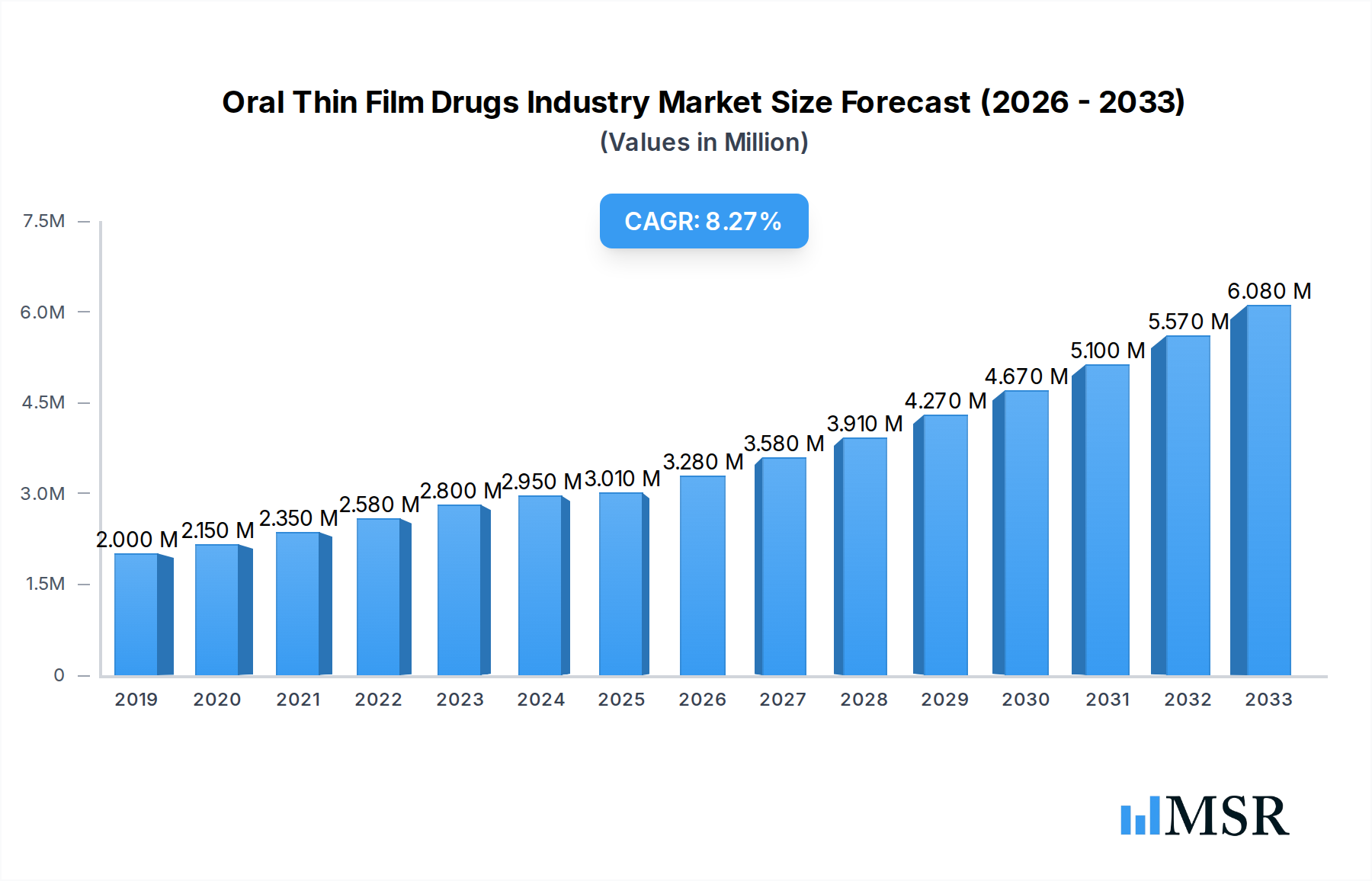

The Oral Thin Film Drugs market is poised for significant expansion, projected to reach a market size of 3.01 Million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 9.56% during the forecast period of 2025-2033. This remarkable growth is primarily fueled by the increasing demand for convenient and patient-friendly drug delivery systems. Oral thin films, offering rapid disintegration, enhanced bioavailability, and improved patient compliance compared to traditional oral dosage forms, are gaining substantial traction. Key drivers include the rising prevalence of chronic diseases, a growing geriatric population with swallowing difficulties, and advancements in pharmaceutical technology enabling the formulation of a wider range of therapeutics in this format. The market's trajectory is further propelled by the expanding application of oral thin films in critical therapeutic areas such as opioid dependence and the management of nausea and vomiting, reflecting a growing preference for discreet and easily administrable treatments. The Sublingual Film segment is expected to lead this expansion, owing to its rapid absorption and efficacy.

Oral Thin Film Drugs Industry Market Size (In Million)

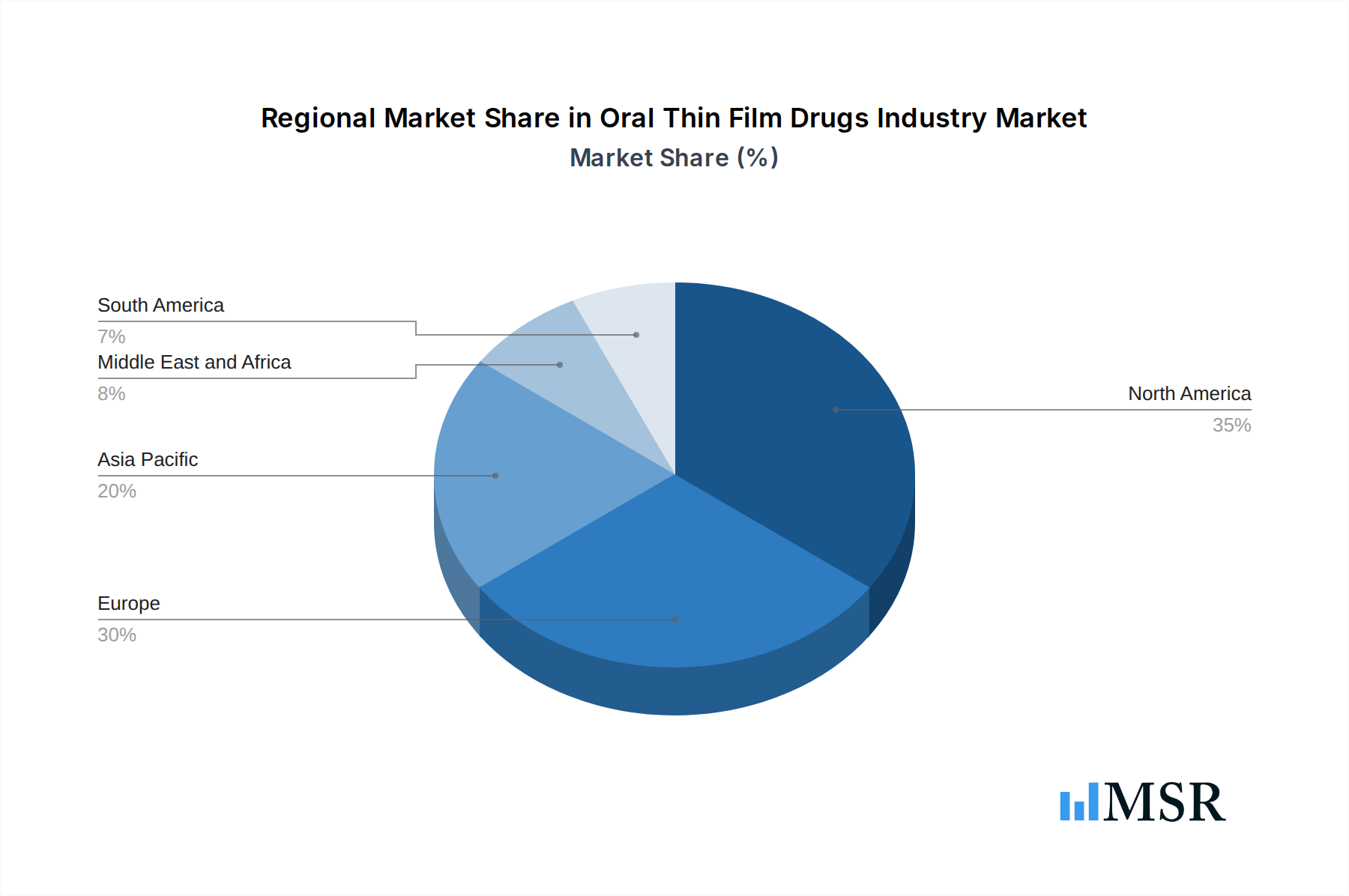

The market's growth is supported by a sophisticated distribution network, with Hospital Pharmacies and Retail Pharmacies playing crucial roles in ensuring accessibility. Innovations in product development, such as the introduction of novel excipients and manufacturing processes, are continually enhancing the efficacy and patient experience. While the market presents immense opportunities, certain restraints, such as the manufacturing complexities for certain sensitive drugs and the need for specialized packaging to maintain product integrity, require strategic attention. Nonetheless, the overarching trend towards patient-centric healthcare solutions and the ongoing research and development by key players like Sunovion Pharmaceuticals Inc., Aquestive Therapeutics Inc., and Viatris are expected to mitigate these challenges. Geographically, North America and Europe are anticipated to remain dominant markets, driven by high healthcare expenditure and the early adoption of innovative drug delivery systems. However, the Asia Pacific region is expected to witness substantial growth due to increasing healthcare awareness and a burgeoning pharmaceutical sector.

Oral Thin Film Drugs Industry Company Market Share

Unlock critical insights into the rapidly expanding Oral Thin Film Drugs market. This comprehensive report provides an in-depth analysis of market dynamics, key drivers, emerging trends, and future opportunities within the global oral thin film sector. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this research is essential for pharmaceutical manufacturers, biotech innovators, investors, and healthcare professionals seeking to capitalize on the lucrative oral thin film drug delivery systems market.

Oral Thin Film Drugs Industry Market Concentration & Dynamics

The Oral Thin Film Drugs industry exhibits a moderate to high level of market concentration, driven by significant investments in research and development, stringent regulatory approvals, and the specialized manufacturing processes required. Key players like Sunovion Pharmaceuticals Inc., Aquestive Therapeutics Inc., and LTS Lohmann Therapie-Systeme AG hold substantial market shares, leveraging their patented technologies and established distribution networks. The innovation ecosystem is characterized by a growing number of collaborations between pharmaceutical giants and specialized oral film technology developers, fostering the creation of novel drug delivery solutions. Regulatory frameworks, primarily governed by the FDA in the US and EMA in Europe, are crucial determinants of market entry and product commercialization, with a focus on patient safety, efficacy, and bioavailability. Substitute products, such as traditional tablets and capsules, continue to pose a competitive challenge, though the convenience and rapid onset of action offered by oral thin films are increasingly recognized by both healthcare providers and patients. End-user trends are leaning towards more discreet, convenient, and patient-friendly drug administration methods, particularly for pediatric and geriatric populations, and for conditions requiring rapid symptom relief. Merger and acquisition (M&A) activities, while not yet defining the market's structure, are anticipated to increase as larger pharmaceutical companies seek to integrate oral thin film technologies into their portfolios. In the historical period (2019-2024), approximately 5-10 significant M&A deals were observed, with an estimated market share concentration of the top 5 players at around 60-70%.

Oral Thin Film Drugs Industry Industry Insights & Trends

The Oral Thin Film Drugs industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of XX% from its current market size of approximately $5,000 Million in the base year of 2025. This growth is propelled by several key factors. Firstly, the increasing prevalence of chronic diseases and the demand for more convenient and patient-centric drug delivery methods are significant market growth drivers. Oral thin films offer advantages such as rapid disintegration and absorption, bypassing the gastrointestinal tract, which leads to faster onset of therapeutic action and improved bioavailability, especially for sensitive drugs. This is particularly relevant for indications like Opioid Dependence and Nausea and Vomiting, where rapid relief is critical. Technological disruptions are a constant feature of this market. Innovations in polymer science and manufacturing techniques are enabling the development of films with enhanced stability, controlled release properties, and improved palatability. The ability to mask bitter tastes and offer pleasant flavors is crucial for patient adherence, especially in pediatric formulations. Evolving consumer behaviors are also playing a pivotal role. Patients, particularly younger demographics and those with swallowing difficulties (dysphagia), are actively seeking alternatives to traditional pills. The discreet and easy-to-use nature of oral thin films aligns perfectly with modern lifestyles, promoting greater medication compliance. Furthermore, the expanding applications of oral thin films beyond traditional pharmaceuticals, including over-the-counter (OTC) medications and dietary supplements, are contributing to market expansion. The forecast period (2025–2033) is expected to witness a surge in the development and adoption of oral thin film formulations for a wider range of therapeutic areas, driven by ongoing clinical research and favorable regulatory pathways for novel drug delivery systems. The estimated market size for 2033 is projected to reach over $10,000 Million.

Key Markets & Segments Leading Oral Thin Film Drugs Industry

The Sublingual Film segment is a dominant force within the Oral Thin Film Drugs industry, driven by its superior absorption characteristics and rapid onset of action, making it ideal for medications requiring immediate therapeutic effects. This segment is further bolstered by its application in critical Disease Indications such as Opioid Dependence, where fast-acting formulations are paramount for managing withdrawal symptoms and cravings. The segment is also seeing significant growth in treating Nausea and Vomiting, offering a convenient and palatable alternative to oral liquids or injections.

- Drivers for Sublingual Film Dominance:

- Enhanced Bioavailability: Sublingual absorption bypasses first-pass metabolism, leading to higher drug concentrations in the bloodstream.

- Rapid Onset of Action: Crucial for acute conditions and pain management.

- Patient Compliance: Ease of administration and palatability, especially for pediatric and geriatric patients.

- Technological Advancements: Innovations in mucoadhesive polymers and film formulations.

The Hospital Pharmacies distribution channel plays a pivotal role in the uptake of oral thin film drugs, particularly for prescription medications and those requiring specialized handling or administration guidance. These settings often cater to patients with acute conditions or those undergoing complex treatments, where the advantages of oral thin films are most pronounced.

- Drivers for Hospital Pharmacy Dominance:

- Critical Care Applications: Facilitates rapid drug delivery in emergency situations.

- Specialized Patient Populations: Serving patients with dysphagia or other administration challenges.

- Controlled Substance Management: Secure dispensing of medications for opioid dependence.

- Healthcare Professional Recommendation: Pharmacists and physicians in hospitals often guide the choice of delivery systems.

Geographically, North America is leading the Oral Thin Film Drugs industry, propelled by advanced healthcare infrastructure, high R&D spending, and a receptive market for innovative drug delivery systems. The presence of major pharmaceutical companies and regulatory bodies like the FDA further strengthens its position.

- Drivers for North American Leadership:

- Strong Pharmaceutical R&D Landscape: Significant investment in novel drug formulations.

- Favorable Regulatory Environment: Expedited approvals for innovative drug delivery technologies.

- High Healthcare Expenditure: Greater patient and payer willingness to adopt advanced treatments.

- Established Market for Specialty Pharmaceuticals: Growing demand for patient-centric solutions.

The Other Products segment, encompassing buccal films and films for other administration routes, is also experiencing significant expansion. While sublingual films currently lead, advancements in buccal film technology, like the Buprenorphine Buccal Film and Diazepam Buccal Film, are carving out substantial market share. The Retail Pharmacies distribution channel is expected to grow substantially as more OTC and chronic condition medications are formulated as oral thin films, offering greater accessibility and convenience to a broader patient base.

Oral Thin Film Drugs Industry Product Developments

Product developments in the Oral Thin Film Drugs industry are characterized by a strong focus on enhancing drug delivery efficacy and patient experience. Innovations center on creating films with precise dosage control, improved mucoadhesion for optimal absorption, and advanced taste-masking technologies. Key advancements include the development of films for managing chronic pain, neurological disorders, and gastrointestinal ailments, offering a discreet and rapid alternative to traditional dosage forms. The increasing versatility of oral thin film technology allows for the incorporation of a wider range of active pharmaceutical ingredients (APIs), including challenging molecules.

Challenges in the Oral Thin Film Drugs Industry Market

The Oral Thin Film Drugs market faces several critical challenges. Regulatory hurdles remain significant, with stringent approval processes for novel drug delivery systems requiring extensive clinical trials to demonstrate safety and efficacy, potentially increasing development timelines and costs. Supply chain complexities, particularly in sourcing specialized excipients and ensuring consistent quality of film manufacturing, can also pose significant restraints. Competitive pressures from established dosage forms like tablets and capsules, which benefit from decades of market acceptance and lower manufacturing costs, are also a considerable factor.

Forces Driving Oral Thin Film Drugs Industry Growth

Several powerful forces are driving the growth of the Oral Thin Film Drugs industry. Technological advancements in polymer science and manufacturing are enabling the creation of more sophisticated and patient-friendly film formulations. The increasing demand for patient-centric drug delivery solutions, particularly from elderly populations and individuals with swallowing difficulties, is a major driver. Favorable regulatory pathways for innovative drug delivery systems and the growing pipeline of drugs suitable for oral thin film formulation are also contributing to expansion.

Challenges in the Oral Thin Film Drugs Industry Market

Long-term growth catalysts for the Oral Thin Film Drugs industry lie in continuous innovation and strategic market expansion. The development of films with advanced functionalities, such as extended-release profiles and combination therapies, will be crucial. Strategic partnerships between oral film technology developers and large pharmaceutical companies will accelerate product launches and market penetration. Expanding into emerging markets with growing healthcare needs and increasing disposable incomes will unlock significant new opportunities.

Emerging Opportunities in Oral Thin Film Drugs Industry

Emerging opportunities within the Oral Thin Film Drugs industry are vast and diverse. The expansion of applications into over-the-counter (OTC) products and supplements presents a substantial untapped market. The development of films for rare diseases and specialized therapeutic areas, where patient compliance is critical, offers significant potential. Furthermore, the integration of smart technologies, such as sensors within films for real-time therapeutic monitoring, represents a futuristic frontier for innovation.

Leading Players in the Oral Thin Film Drugs Industry Sector

- Sunovion Pharmaceuticals Inc.

- C L Pharm

- Aquestive Therapeutics Inc.

- ZIM Laboratories Limited

- LTS Lohmann Therapie-Systeme AG

- Viatris

- Cure Pharmaceutical

- IntelGenx Corp.

- NAL Pharma

Key Milestones in Oral Thin Film Drugs Industry Industry

- October 2022: IntelGenx Corp. announced the U.S. FDA Generic Drug User Fee Act ("GDUFA") approval for its Buprenorphine Buccal Film, a generic version of Belbuca, for long-term pain management.

- August 2022: Aquestive Therapeutics received FDA grant for Libervant (diazepam) Buccal Film for the acute treatment of intermittent, stereotypic episodes of frequent seizure activity.

Strategic Outlook for Oral Thin Film Drugs Industry Market

The strategic outlook for the Oral Thin Film Drugs industry is exceptionally promising, driven by a confluence of factors that position it for sustained and accelerated growth. Key growth accelerators include the increasing recognition of oral thin films as a superior alternative to traditional dosage forms for specific patient populations and therapeutic needs. Strategic opportunities lie in the continued innovation of film formulations to address unmet medical needs, such as the development of films for complex biologics and the expansion of indications into areas like mental health and oncology. Investments in advanced manufacturing technologies and robust clinical trial pipelines will be crucial for capitalizing on the market's immense potential.

Oral Thin Film Drugs Industry Segmentation

-

1. Product

- 1.1. Sublingual Film

- 1.2. Other Products

-

2. Disease Indication

- 2.1. Opioid Dependence

- 2.2. Nausea and Vomiting

- 2.3. Other Disease Indications

-

3. Distribution Channel

- 3.1. Hospital Pharmacies

- 3.2. Retail Pharmacies

- 3.3. Other Distribution Channels

Oral Thin Film Drugs Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Oral Thin Film Drugs Industry Regional Market Share

Geographic Coverage of Oral Thin Film Drugs Industry

Oral Thin Film Drugs Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Sublingual Film

- 5.1.2. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Disease Indication

- 5.2.1. Opioid Dependence

- 5.2.2. Nausea and Vomiting

- 5.2.3. Other Disease Indications

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Hospital Pharmacies

- 5.3.2. Retail Pharmacies

- 5.3.3. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global Oral Thin Film Drugs Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Sublingual Film

- 6.1.2. Other Products

- 6.2. Market Analysis, Insights and Forecast - by Disease Indication

- 6.2.1. Opioid Dependence

- 6.2.2. Nausea and Vomiting

- 6.2.3. Other Disease Indications

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Hospital Pharmacies

- 6.3.2. Retail Pharmacies

- 6.3.3. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America Oral Thin Film Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Sublingual Film

- 7.1.2. Other Products

- 7.2. Market Analysis, Insights and Forecast - by Disease Indication

- 7.2.1. Opioid Dependence

- 7.2.2. Nausea and Vomiting

- 7.2.3. Other Disease Indications

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Hospital Pharmacies

- 7.3.2. Retail Pharmacies

- 7.3.3. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe Oral Thin Film Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Sublingual Film

- 8.1.2. Other Products

- 8.2. Market Analysis, Insights and Forecast - by Disease Indication

- 8.2.1. Opioid Dependence

- 8.2.2. Nausea and Vomiting

- 8.2.3. Other Disease Indications

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Hospital Pharmacies

- 8.3.2. Retail Pharmacies

- 8.3.3. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Asia Pacific Oral Thin Film Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Sublingual Film

- 9.1.2. Other Products

- 9.2. Market Analysis, Insights and Forecast - by Disease Indication

- 9.2.1. Opioid Dependence

- 9.2.2. Nausea and Vomiting

- 9.2.3. Other Disease Indications

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Hospital Pharmacies

- 9.3.2. Retail Pharmacies

- 9.3.3. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East and Africa Oral Thin Film Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Sublingual Film

- 10.1.2. Other Products

- 10.2. Market Analysis, Insights and Forecast - by Disease Indication

- 10.2.1. Opioid Dependence

- 10.2.2. Nausea and Vomiting

- 10.2.3. Other Disease Indications

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Hospital Pharmacies

- 10.3.2. Retail Pharmacies

- 10.3.3. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. South America Oral Thin Film Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Sublingual Film

- 11.1.2. Other Products

- 11.2. Market Analysis, Insights and Forecast - by Disease Indication

- 11.2.1. Opioid Dependence

- 11.2.2. Nausea and Vomiting

- 11.2.3. Other Disease Indications

- 11.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.3.1. Hospital Pharmacies

- 11.3.2. Retail Pharmacies

- 11.3.3. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sunovion Pharmaceuticals Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 C L Pharm

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Aquestive Therapeutics Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ZIM Laboratories Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 LTS Lohmann Therapie-Systeme AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Viatris

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Cure Pharmaceutical

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 IntelGenx Corp

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 NAL Pharma

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Sunovion Pharmaceuticals Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Oral Thin Film Drugs Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Oral Thin Film Drugs Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Oral Thin Film Drugs Industry Revenue (Million), by Product 2025 & 2033

- Figure 4: North America Oral Thin Film Drugs Industry Volume (K Unit), by Product 2025 & 2033

- Figure 5: North America Oral Thin Film Drugs Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Oral Thin Film Drugs Industry Volume Share (%), by Product 2025 & 2033

- Figure 7: North America Oral Thin Film Drugs Industry Revenue (Million), by Disease Indication 2025 & 2033

- Figure 8: North America Oral Thin Film Drugs Industry Volume (K Unit), by Disease Indication 2025 & 2033

- Figure 9: North America Oral Thin Film Drugs Industry Revenue Share (%), by Disease Indication 2025 & 2033

- Figure 10: North America Oral Thin Film Drugs Industry Volume Share (%), by Disease Indication 2025 & 2033

- Figure 11: North America Oral Thin Film Drugs Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 12: North America Oral Thin Film Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 13: North America Oral Thin Film Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 14: North America Oral Thin Film Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 15: North America Oral Thin Film Drugs Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Oral Thin Film Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Oral Thin Film Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Oral Thin Film Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Oral Thin Film Drugs Industry Revenue (Million), by Product 2025 & 2033

- Figure 20: Europe Oral Thin Film Drugs Industry Volume (K Unit), by Product 2025 & 2033

- Figure 21: Europe Oral Thin Film Drugs Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Europe Oral Thin Film Drugs Industry Volume Share (%), by Product 2025 & 2033

- Figure 23: Europe Oral Thin Film Drugs Industry Revenue (Million), by Disease Indication 2025 & 2033

- Figure 24: Europe Oral Thin Film Drugs Industry Volume (K Unit), by Disease Indication 2025 & 2033

- Figure 25: Europe Oral Thin Film Drugs Industry Revenue Share (%), by Disease Indication 2025 & 2033

- Figure 26: Europe Oral Thin Film Drugs Industry Volume Share (%), by Disease Indication 2025 & 2033

- Figure 27: Europe Oral Thin Film Drugs Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 28: Europe Oral Thin Film Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 29: Europe Oral Thin Film Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Europe Oral Thin Film Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 31: Europe Oral Thin Film Drugs Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Oral Thin Film Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Oral Thin Film Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Oral Thin Film Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Oral Thin Film Drugs Industry Revenue (Million), by Product 2025 & 2033

- Figure 36: Asia Pacific Oral Thin Film Drugs Industry Volume (K Unit), by Product 2025 & 2033

- Figure 37: Asia Pacific Oral Thin Film Drugs Industry Revenue Share (%), by Product 2025 & 2033

- Figure 38: Asia Pacific Oral Thin Film Drugs Industry Volume Share (%), by Product 2025 & 2033

- Figure 39: Asia Pacific Oral Thin Film Drugs Industry Revenue (Million), by Disease Indication 2025 & 2033

- Figure 40: Asia Pacific Oral Thin Film Drugs Industry Volume (K Unit), by Disease Indication 2025 & 2033

- Figure 41: Asia Pacific Oral Thin Film Drugs Industry Revenue Share (%), by Disease Indication 2025 & 2033

- Figure 42: Asia Pacific Oral Thin Film Drugs Industry Volume Share (%), by Disease Indication 2025 & 2033

- Figure 43: Asia Pacific Oral Thin Film Drugs Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 44: Asia Pacific Oral Thin Film Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 45: Asia Pacific Oral Thin Film Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Asia Pacific Oral Thin Film Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: Asia Pacific Oral Thin Film Drugs Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Oral Thin Film Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Oral Thin Film Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Oral Thin Film Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Oral Thin Film Drugs Industry Revenue (Million), by Product 2025 & 2033

- Figure 52: Middle East and Africa Oral Thin Film Drugs Industry Volume (K Unit), by Product 2025 & 2033

- Figure 53: Middle East and Africa Oral Thin Film Drugs Industry Revenue Share (%), by Product 2025 & 2033

- Figure 54: Middle East and Africa Oral Thin Film Drugs Industry Volume Share (%), by Product 2025 & 2033

- Figure 55: Middle East and Africa Oral Thin Film Drugs Industry Revenue (Million), by Disease Indication 2025 & 2033

- Figure 56: Middle East and Africa Oral Thin Film Drugs Industry Volume (K Unit), by Disease Indication 2025 & 2033

- Figure 57: Middle East and Africa Oral Thin Film Drugs Industry Revenue Share (%), by Disease Indication 2025 & 2033

- Figure 58: Middle East and Africa Oral Thin Film Drugs Industry Volume Share (%), by Disease Indication 2025 & 2033

- Figure 59: Middle East and Africa Oral Thin Film Drugs Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 60: Middle East and Africa Oral Thin Film Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 61: Middle East and Africa Oral Thin Film Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 62: Middle East and Africa Oral Thin Film Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 63: Middle East and Africa Oral Thin Film Drugs Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Middle East and Africa Oral Thin Film Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Oral Thin Film Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Oral Thin Film Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Oral Thin Film Drugs Industry Revenue (Million), by Product 2025 & 2033

- Figure 68: South America Oral Thin Film Drugs Industry Volume (K Unit), by Product 2025 & 2033

- Figure 69: South America Oral Thin Film Drugs Industry Revenue Share (%), by Product 2025 & 2033

- Figure 70: South America Oral Thin Film Drugs Industry Volume Share (%), by Product 2025 & 2033

- Figure 71: South America Oral Thin Film Drugs Industry Revenue (Million), by Disease Indication 2025 & 2033

- Figure 72: South America Oral Thin Film Drugs Industry Volume (K Unit), by Disease Indication 2025 & 2033

- Figure 73: South America Oral Thin Film Drugs Industry Revenue Share (%), by Disease Indication 2025 & 2033

- Figure 74: South America Oral Thin Film Drugs Industry Volume Share (%), by Disease Indication 2025 & 2033

- Figure 75: South America Oral Thin Film Drugs Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 76: South America Oral Thin Film Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 77: South America Oral Thin Film Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 78: South America Oral Thin Film Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 79: South America Oral Thin Film Drugs Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Oral Thin Film Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Oral Thin Film Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Oral Thin Film Drugs Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 3: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Disease Indication 2020 & 2033

- Table 4: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Disease Indication 2020 & 2033

- Table 5: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 7: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 10: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 11: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Disease Indication 2020 & 2033

- Table 12: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Disease Indication 2020 & 2033

- Table 13: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 14: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 15: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 24: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 25: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Disease Indication 2020 & 2033

- Table 26: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Disease Indication 2020 & 2033

- Table 27: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 28: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 29: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 44: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 45: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Disease Indication 2020 & 2033

- Table 46: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Disease Indication 2020 & 2033

- Table 47: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 48: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 49: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 64: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 65: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Disease Indication 2020 & 2033

- Table 66: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Disease Indication 2020 & 2033

- Table 67: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 68: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 69: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: GCC Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: South Africa Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 78: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 79: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Disease Indication 2020 & 2033

- Table 80: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Disease Indication 2020 & 2033

- Table 81: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 82: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 83: Global Oral Thin Film Drugs Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 84: Global Oral Thin Film Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: Brazil Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: Argentina Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Oral Thin Film Drugs Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Oral Thin Film Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oral Thin Film Drugs Industry?

The projected CAGR is approximately 9.56%.

2. Which companies are prominent players in the Oral Thin Film Drugs Industry?

Key companies in the market include Sunovion Pharmaceuticals Inc, C L Pharm, Aquestive Therapeutics Inc, ZIM Laboratories Limited, LTS Lohmann Therapie-Systeme AG, Viatris, Cure Pharmaceutical, IntelGenx Corp, NAL Pharma.

3. What are the main segments of the Oral Thin Film Drugs Industry?

The market segments include Product, Disease Indication, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.01 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Burden of Target Diseases; Advantages Associated with the Thin Films.

6. What are the notable trends driving market growth?

The Sublingual Film Segment is Expected to Witness Considerable Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Technical Limitations of Oral Thin Films.

8. Can you provide examples of recent developments in the market?

In October 2022, IntelGenxCorp. announced that it had received a U.S. FDA Generic Drug User Fee Act ("GDUFA") for its Buprenorphine Buccal Film. Buprenorphine Buccal Film is a generic version of Belbuca, an opioid used to manage severe continuous pain and can be used for long-term treatment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oral Thin Film Drugs Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oral Thin Film Drugs Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oral Thin Film Drugs Industry?

To stay informed about further developments, trends, and reports in the Oral Thin Film Drugs Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence