Key Insights

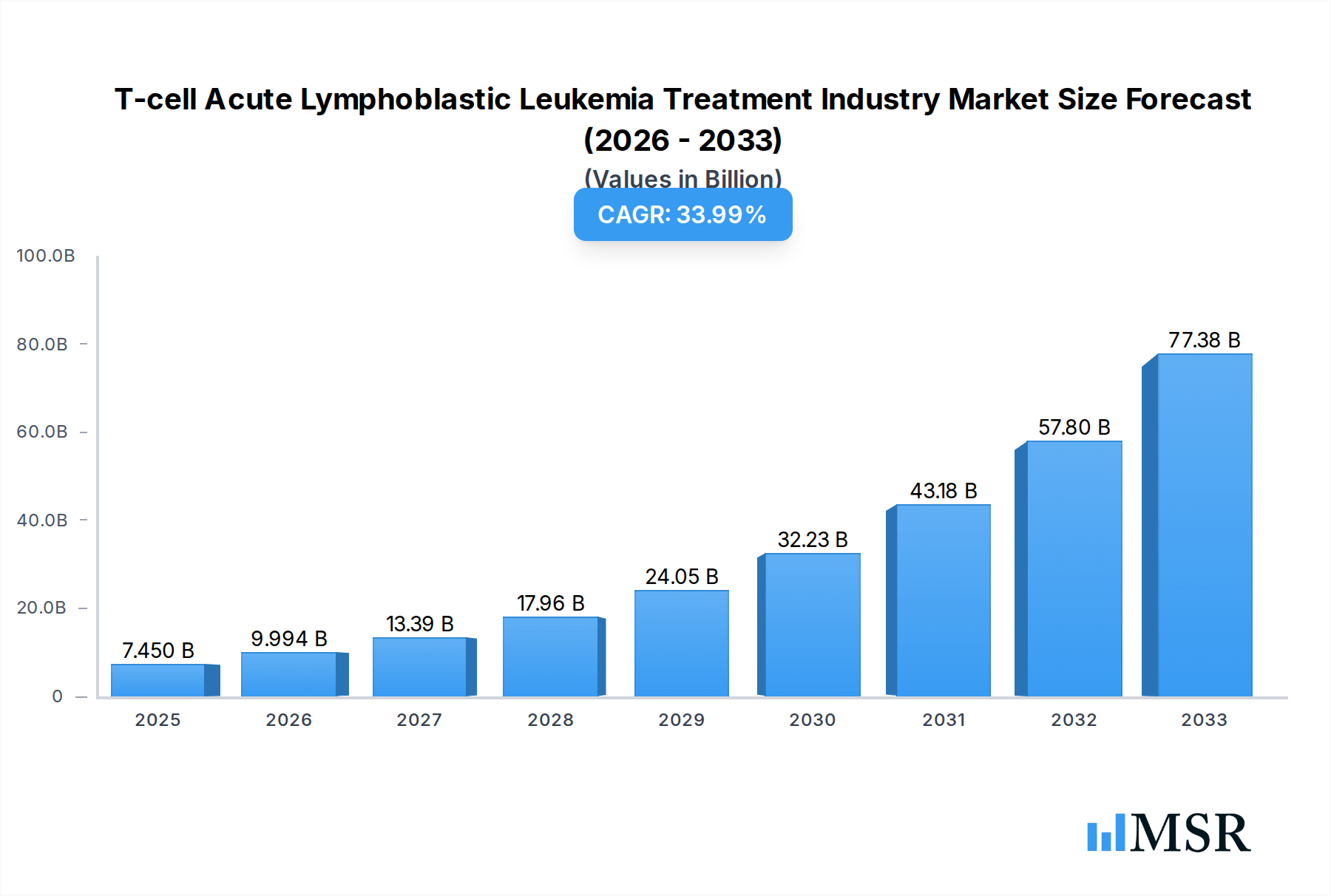

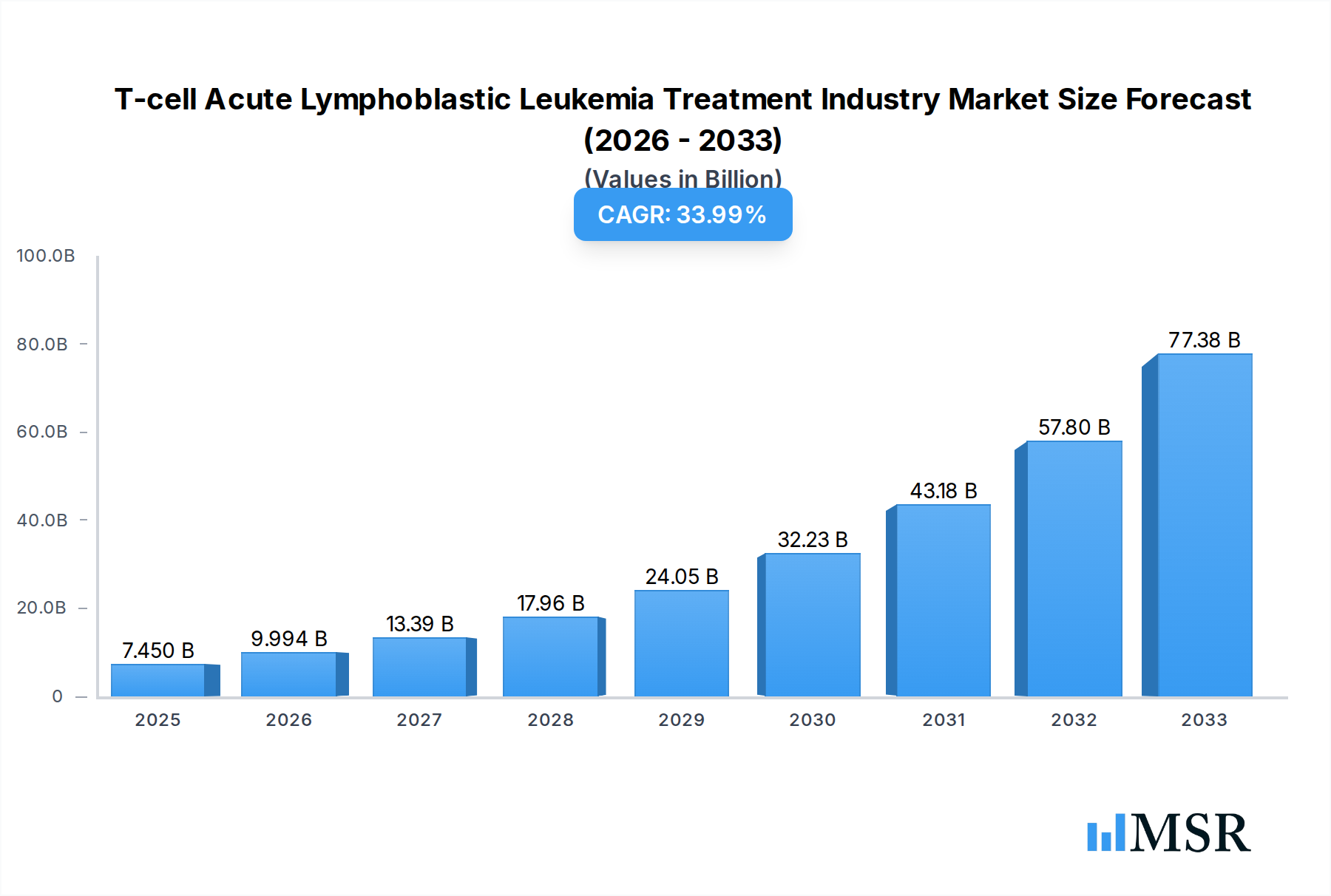

The T-cell Acute Lymphoblastic Leukemia (T-ALL) treatment market is poised for substantial growth, projected to reach $7.45 billion by 2025. This robust expansion is driven by an impressive CAGR of 35.39% throughout the forecast period. Key drivers fueling this market surge include advancements in targeted therapies and immunotherapies that offer more effective and less toxic treatment options for T-ALL patients. The increasing incidence of T-ALL, coupled with a growing awareness and improved diagnostic capabilities, also contributes significantly to market expansion. Furthermore, substantial investments in research and development by leading pharmaceutical and biotechnology companies are introducing novel treatment modalities, including CAR T-cell therapy and bispecific antibodies, which are showing promising results in clinical trials and patient outcomes. The market is also benefiting from a supportive regulatory landscape and initiatives aimed at increasing access to advanced cancer treatments.

T-cell Acute Lymphoblastic Leukemia Treatment Industry Market Size (In Billion)

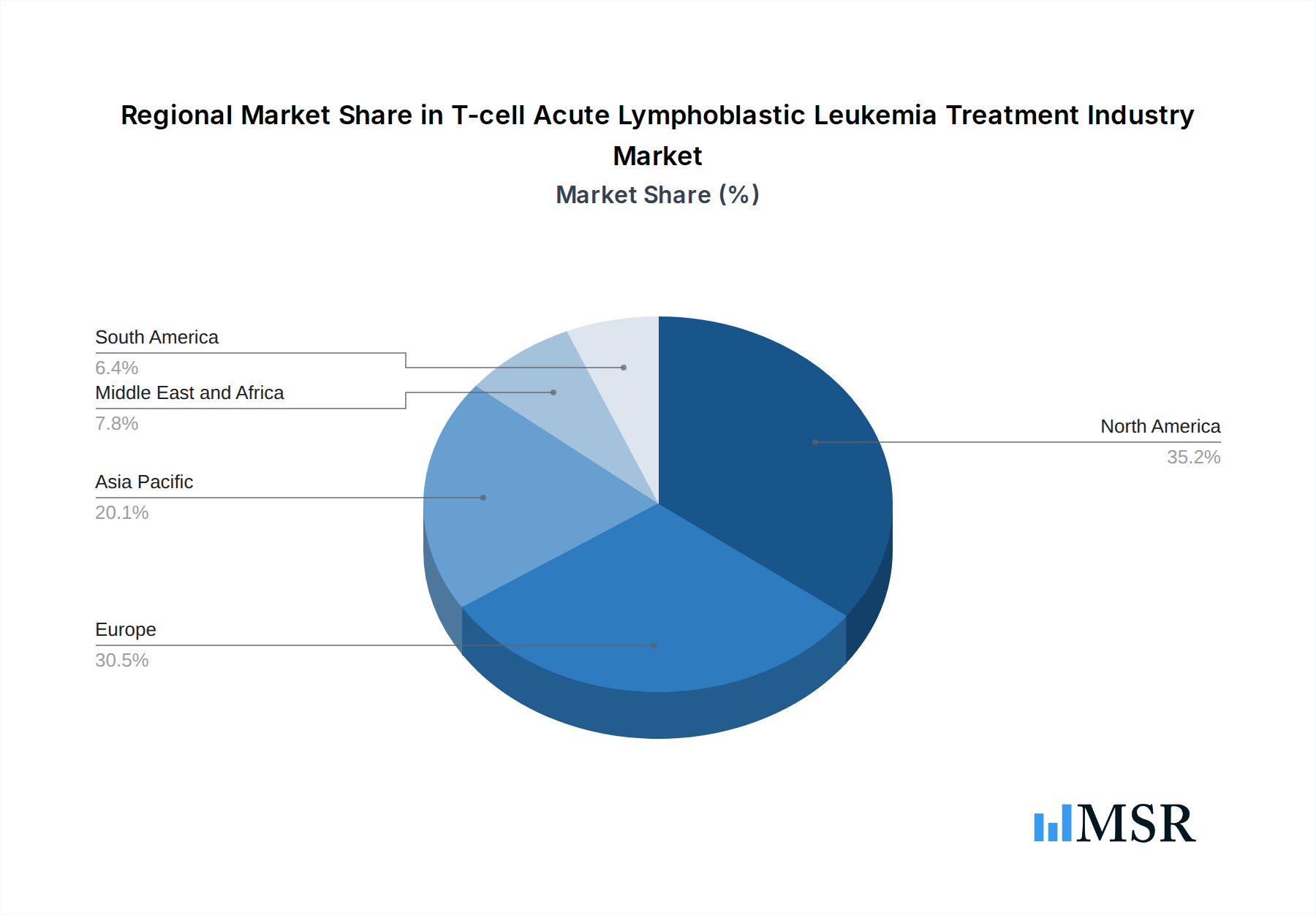

The competitive landscape is dynamic, with significant players like Genmab AS, Novartis AG, and F. Hoffmann-La Roche Ltd at the forefront. These companies are actively involved in the development and commercialization of innovative T-ALL therapies, including targeted agents and advanced cell-based treatments. The market is segmented by type of therapy, with chemotherapy, radiation therapy, and stem cell transplants remaining significant, alongside the rapid emergence of newer immunotherapies. Hospitals and specialized cancer and radiation therapy centers are the primary end-users, reflecting the complex and multidisciplinary nature of T-ALL treatment. Geographically, North America and Europe currently lead the market, driven by high healthcare expenditure and early adoption of new technologies. However, the Asia Pacific region is expected to witness the fastest growth due to rising healthcare infrastructure and increasing patient populations. Restraints, such as the high cost of advanced therapies and potential side effects, are being addressed through ongoing research and development aimed at improving safety profiles and cost-effectiveness.

T-cell Acute Lymphoblastic Leukemia Treatment Industry Company Market Share

This in-depth report offers a definitive analysis of the T-cell Acute Lymphoblastic Leukemia (T-ALL) treatment market, providing critical insights for pharmaceutical companies, biotech innovators, healthcare providers, and investors. Covering the historical period (2019-2024), base year (2025), and forecast period (2025-2033), this research delves into market dynamics, key trends, segmentation, competitive landscape, challenges, and emerging opportunities within the global T-ALL treatment industry. Gain a strategic advantage with actionable data on market size, CAGR, and future growth projections, crucial for navigating this rapidly evolving therapeutic area.

T-cell Acute Lymphoblastic Leukemia Treatment Industry Market Concentration & Dynamics

The T-cell Acute Lymphoblastic Leukemia (T-ALL) treatment market exhibits a moderate concentration, driven by a blend of established pharmaceutical giants and emerging biotechnology firms specializing in CAR T-cell therapy and other advanced treatments. Innovation plays a pivotal role, with significant investment in research and development of novel therapeutic modalities. The regulatory landscape, particularly approvals from the European Medicines Agency (EMA) and the Food and Drug Administration (FDA), significantly influences market access and product launches. Substitute products, primarily traditional chemotherapy and radiation therapy, still hold a considerable share, though their dominance is challenged by the efficacy of newer targeted therapies. End-user trends are shifting towards more personalized and effective treatments, increasing demand for advanced therapies. Mergers and acquisitions (M&A) activities are expected to shape market concentration, with larger entities acquiring innovative smaller companies to expand their portfolios.

- Market Share of Key Therapeutic Approaches: While chemotherapy remains a significant segment, the market share of CAR T-cell therapies is projected to grow substantially due to recent approvals and ongoing clinical trials.

- M&A Deal Counts: Expected to rise as companies seek to consolidate their market position and acquire promising T-ALL treatment technologies.

- Innovation Ecosystem: Characterized by strong collaborations between academic institutions, research organizations, and pharmaceutical companies.

- Regulatory Hurdles: Navigating stringent approval processes is a key dynamic for market entry.

T-cell Acute Lymphoblastic Leukemia Treatment Industry Industry Insights & Trends

The T-cell Acute Lymphoblastic Leukemia treatment market is projected to experience robust growth, driven by increasing incidence of T-ALL, advancements in targeted therapies, and expanding healthcare infrastructure globally. The market size, estimated to reach billions by 2033, is propelled by a compound annual growth rate (CAGR) of xx% during the forecast period. Technological disruptions, particularly the rise of CAR T-cell therapy, are transforming treatment paradigms. The approval of brexucabtagene autoleucel (Tecartus) by the FDA in October 2021, marking the first CAR T-cell therapy for adult ALL, signifies a major breakthrough. Further positive opinions, such as the EMA's CHMP positive opinion for Tecartus in July 2022, underscore the growing acceptance and efficacy of these advanced treatments. Evolving consumer behaviors reflect a demand for less toxic and more effective treatment options, further fueling the adoption of innovative therapies over traditional chemotherapy and radiation therapy. The continuous pipeline of new drug candidates and the increasing focus on personalized medicine are expected to sustain this upward trajectory, contributing significantly to the overall market value projected to be in the billions. The integration of stem cell transplant as a consolidative therapy and the exploration of novel other treatment modalities like bispecific antibodies and immunotherapy also contribute to the dynamic growth of this market, all contributing to a market value expected to be in the billions.

Key Markets & Segments Leading T-cell Acute Lymphoblastic Leukemia Treatment Industry

North America is poised to be a dominant region in the T-cell Acute Lymphoblastic Leukemia treatment market, driven by advanced healthcare infrastructure, high R&D spending, and early adoption of innovative therapies. The United States, in particular, leads due to significant investments in cancer research and a robust regulatory framework that facilitates the approval of novel treatments.

- Dominant Region: North America

- Drivers:

- High prevalence and diagnosis rates of T-ALL.

- Extensive clinical trial activity and rapid adoption of new therapies.

- Strong presence of leading pharmaceutical and biotechnology companies.

- Favorable reimbursement policies for advanced treatments.

- Well-established healthcare facilities and expertise in specialized oncology care.

- Drivers:

The Type of Therapy segment is witnessing a significant shift. While Chemotherapy has historically been the mainstay, its market share is gradually being complemented and, in some niches, surpassed by newer modalities. CAR T-cell therapy, a subset of "Others," is rapidly gaining traction following pivotal approvals, demonstrating superior efficacy in relapsed or refractory cases. Stem cell transplant continues to play a crucial role as a consolidative therapy, particularly for high-risk patients. The "Others" category also encompasses emerging treatments like bispecific antibodies and novel immunotherapies, which are poised for significant growth.

- Dominant Segment: CAR T-cell Therapy (within "Others")

- Drivers:

- Breakthrough FDA and EMA approvals for specific T-ALL indications.

- Demonstrated high response rates and improved survival outcomes in relapsed/refractory patients.

- Increasing investment in CAR T-cell research and manufacturing capabilities.

- Growing pipeline of CAR T-cell candidates targeting various T-ALL subtypes.

- Drivers:

In terms of End User, Hospitals are the primary consumers of T-ALL treatments, owing to their comprehensive facilities and specialized medical teams. This is followed closely by Cancer and Radiation Therapy Centers, which are equipped to administer various treatment modalities. The "Others" segment includes specialized treatment centers and research institutions.

- Dominant End User: Hospitals

- Drivers:

- Capability to administer complex treatments like CAR T-cell therapy and stem cell transplants.

- Presence of multidisciplinary oncology teams.

- Availability of advanced diagnostic and supportive care services.

- Established relationships with pharmaceutical manufacturers for drug procurement.

- Drivers:

The global market size, projected to reach billions, is a testament to the increasing demand for effective T-ALL treatments across these key regions and segments.

T-cell Acute Lymphoblastic Leukemia Treatment Industry Product Developments

Product development in the T-cell Acute Lymphoblastic Leukemia treatment industry is characterized by groundbreaking advancements in CAR T-cell therapy, with companies like Kite Pharma (Gilead Sciences) leading the charge. The approval of brexucabtagene autoleucel (Tecartus) for adult ALL signifies a major leap, offering a potentially curative option for patients with relapsed or refractory disease. Ongoing research focuses on enhancing CAR T-cell efficacy, reducing toxicity, and developing strategies to overcome antigen escape. Innovations also extend to novel small molecule inhibitors, bispecific antibodies, and refined chemotherapy regimens. These developments aim to improve patient outcomes, broaden treatment access, and address unmet needs in T-ALL care, contributing to a market valued in the billions.

Challenges in the T-cell Acute Lymphoblastic Leukemia Treatment Industry Market

The T-cell Acute Lymphoblastic Leukemia treatment market faces several significant challenges. The high cost of advanced therapies, particularly CAR T-cell therapy, presents a major barrier to accessibility for a broader patient population, impacting the overall market value. Manufacturing complexities and supply chain vulnerabilities for these personalized treatments can lead to production delays and shortages. Stringent regulatory hurdles and the need for extensive clinical trials to demonstrate long-term safety and efficacy add to the development timeline and cost. Intense competition from established players and emerging innovators also pressures pricing and market share, requiring substantial investment to maintain a competitive edge in this multi-billion dollar industry.

- High Treatment Costs: Leading to limited accessibility and impacting market penetration.

- Manufacturing & Supply Chain Complexity: Resulting in potential production bottlenecks.

- Stringent Regulatory Approvals: Prolonging time-to-market for new therapies.

- Competitive Pressures: Requiring significant R&D investment and strategic market positioning.

Forces Driving T-cell Acute Lymphoblastic Leukemia Treatment Industry Growth

Several powerful forces are driving the growth of the T-cell Acute Lymphoblastic Leukemia treatment industry, propelling its market value into the billions. Advancements in CAR T-cell therapy and other targeted immunotherapies represent a significant technological leap, offering improved efficacy and a better quality of life for patients with relapsed or refractory T-ALL. Increased global incidence of T-ALL, coupled with a growing awareness of the disease and available treatment options, fuels demand. Favorable regulatory environments in key markets, exemplified by recent FDA and EMA approvals, are accelerating market access for innovative therapies. Furthermore, substantial investments in research and development by leading pharmaceutical and biotechnology companies, alongside collaborations with academic institutions, are fostering a continuous pipeline of novel treatments and expanding the overall market size.

Challenges in the T-cell Acute Lymphoblastic Leukemia Treatment Industry Market

While growth is robust, the T-cell Acute Lymphoblastic Leukemia treatment industry encounters challenges that require strategic navigation. The prolonged and complex clinical trial process for novel therapies, coupled with the need for extensive post-market surveillance, can extend time-to-market and increase R&D expenditures, impacting the projected market value in the billions. The ongoing development of resistance mechanisms by cancer cells necessitates continuous innovation and the exploration of combination therapies. Furthermore, ensuring equitable access to highly specialized and expensive treatments like CAR T-cell therapy across diverse healthcare systems remains a significant hurdle. Building and maintaining robust manufacturing capabilities for these complex biological therapies is also a critical, ongoing challenge for sustained market growth in the billions.

Emerging Opportunities in T-cell Acute Lymphoblastic Leukemia Treatment Industry

The T-cell Acute Lymphoblastic Leukemia treatment industry is ripe with emerging opportunities that promise significant market expansion, contributing to its projected multi-billion dollar valuation. The exploration of novel CAR T-cell therapy targets for different T-ALL subtypes and the development of allogeneic (off-the-shelf) CAR T-cell products present substantial market potential. Advances in gene editing technologies and immunotherapy combinations offer avenues for more effective and less toxic treatment regimens. Expanding into emerging economies with growing healthcare expenditures and increasing diagnostic capabilities presents a vast untapped market. Furthermore, developing companion diagnostics to identify patients most likely to respond to specific therapies can optimize treatment selection and market penetration, further driving growth in the billions.

Leading Players in the T-cell Acute Lymphoblastic Leukemia Treatment Industry Sector

- Genmab AS

- Spectrum Pharmaceuticals

- Novartis AG

- F Hoffmann-La Roche Ltd

- Erytech Pharma

- Bristol Myer Squibb Company

- GlaxoSmithKline

- Kyowa Kirin Co Ltd

- Gilead Sciences (Kite Pharma)

- Pfizer Inc

Key Milestones in T-cell Acute Lymphoblastic Leukemia Treatment Industry Industry

- October 2021: The Food and Drug Administration (FDA) approved the use of the CAR T-cell therapy brexucabtagene autoleucel (Tecartus) for adults with B-cell precursor ALL that has not responded to treatment (refractory) or have returned after treatment (relapsed). This approval made brexucabtagene the first CAR T-cell therapy approved for adults with ALL, significantly impacting the market.

- July 2022: The European Medicines Agency (EMA) Committee for Medicinal Products for Human Use (CHMP) issued a positive opinion for Kite's Tecartus (brexucabtagene autoleucel) for the treatment of adult patients 26 years of age and above with relapsed or refractory (r/r) B-cell precursor acute lymphoblastic leukemia (ALL). This further validated the efficacy of CAR T-cell therapy in the European market.

Strategic Outlook for T-cell Acute Lymphoblastic Leukemia Treatment Industry Market

The strategic outlook for the T-cell Acute Lymphoblastic Leukemia treatment market is exceptionally positive, projecting substantial growth into the billions. Key accelerators include the ongoing refinement and expansion of CAR T-cell therapy, alongside the development of more accessible and cost-effective manufacturing processes. Strategic partnerships between pharmaceutical giants and innovative biotech firms will continue to drive pipeline advancements and market consolidation. Expanding into underserved geographical regions and focusing on personalized medicine approaches, including the use of companion diagnostics, will unlock new market segments. Continued investment in research for novel therapeutic targets and combination therapies will ensure sustained innovation, solidifying the market's trajectory for significant future growth and profitability within the billions.

T-cell Acute Lymphoblastic Leukemia Treatment Industry Segmentation

-

1. Type of Therapy

- 1.1. Chemotherapy

- 1.2. Radiation therapy

- 1.3. Stem cell transplant

- 1.4. Others

-

2. End User

- 2.1. Hospitals

- 2.2. Cancer and Radiation Therapy Centers

- 2.3. Others

T-cell Acute Lymphoblastic Leukemia Treatment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

T-cell Acute Lymphoblastic Leukemia Treatment Industry Regional Market Share

Geographic Coverage of T-cell Acute Lymphoblastic Leukemia Treatment Industry

T-cell Acute Lymphoblastic Leukemia Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 5.1.1. Chemotherapy

- 5.1.2. Radiation therapy

- 5.1.3. Stem cell transplant

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Cancer and Radiation Therapy Centers

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 6. Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 6.1.1. Chemotherapy

- 6.1.2. Radiation therapy

- 6.1.3. Stem cell transplant

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Cancer and Radiation Therapy Centers

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 7. North America T-cell Acute Lymphoblastic Leukemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 7.1.1. Chemotherapy

- 7.1.2. Radiation therapy

- 7.1.3. Stem cell transplant

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Cancer and Radiation Therapy Centers

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 8. Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 8.1.1. Chemotherapy

- 8.1.2. Radiation therapy

- 8.1.3. Stem cell transplant

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Cancer and Radiation Therapy Centers

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 9. Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 9.1.1. Chemotherapy

- 9.1.2. Radiation therapy

- 9.1.3. Stem cell transplant

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Cancer and Radiation Therapy Centers

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 10. Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 10.1.1. Chemotherapy

- 10.1.2. Radiation therapy

- 10.1.3. Stem cell transplant

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Cancer and Radiation Therapy Centers

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 11. South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 11.1.1. Chemotherapy

- 11.1.2. Radiation therapy

- 11.1.3. Stem cell transplant

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals

- 11.2.2. Cancer and Radiation Therapy Centers

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Type of Therapy

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Genmab AS

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Spectrum Pharmaceuticals*List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Novartis AG

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 F Hoffmann-La Roche Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Erytech Pharma

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Bristol Myer Squibb Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 GlaxoSmithKline

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Kyowa Kirin Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Gilead Sciences (Kite Pharma)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Pfizer Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Genmab AS

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Type of Therapy 2025 & 2033

- Figure 3: North America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Type of Therapy 2025 & 2033

- Figure 4: North America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Type of Therapy 2025 & 2033

- Figure 9: Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Type of Therapy 2025 & 2033

- Figure 10: Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Type of Therapy 2025 & 2033

- Figure 15: Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Type of Therapy 2025 & 2033

- Figure 16: Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Type of Therapy 2025 & 2033

- Figure 21: Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Type of Therapy 2025 & 2033

- Figure 22: Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Type of Therapy 2025 & 2033

- Figure 27: South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Type of Therapy 2025 & 2033

- Figure 28: South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Type of Therapy 2020 & 2033

- Table 2: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Type of Therapy 2020 & 2033

- Table 5: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Type of Therapy 2020 & 2033

- Table 11: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Type of Therapy 2020 & 2033

- Table 20: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Type of Therapy 2020 & 2033

- Table 29: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Type of Therapy 2020 & 2033

- Table 35: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 36: Global T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America T-cell Acute Lymphoblastic Leukemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the T-cell Acute Lymphoblastic Leukemia Treatment Industry?

The projected CAGR is approximately 7%.

2. Which companies are prominent players in the T-cell Acute Lymphoblastic Leukemia Treatment Industry?

Key companies in the market include Genmab AS, Spectrum Pharmaceuticals*List Not Exhaustive, Novartis AG, F Hoffmann-La Roche Ltd, Erytech Pharma, Bristol Myer Squibb Company, GlaxoSmithKline, Kyowa Kirin Co Ltd, Gilead Sciences (Kite Pharma), Pfizer Inc.

3. What are the main segments of the T-cell Acute Lymphoblastic Leukemia Treatment Industry?

The market segments include Type of Therapy, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.12 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of T-cell Acute Lymphoblastic Leukemia Market; Growing Research and Development Expenditure on Cancer Therapeutics.

6. What are the notable trends driving market growth?

Chemotherapy Segment Expects to Register a High CAGR Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Regulatory Scenario for the Drug Approvals; High Cost Asscoiated with the Treatment.

8. Can you provide examples of recent developments in the market?

In July 2022, European Medicines Agency (EMA) Committee for Medicinal Products for Human Use (CHMP) issued a positive opinion for Kite's Tecartus (brexucabtagene autoleucel) for the treatment of adult patients 26 years of age and above with relapsed or refractory (r/r) B-cell precursor acute lymphoblastic leukemia (ALL)

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "T-cell Acute Lymphoblastic Leukemia Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the T-cell Acute Lymphoblastic Leukemia Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the T-cell Acute Lymphoblastic Leukemia Treatment Industry?

To stay informed about further developments, trends, and reports in the T-cell Acute Lymphoblastic Leukemia Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence