Key Insights

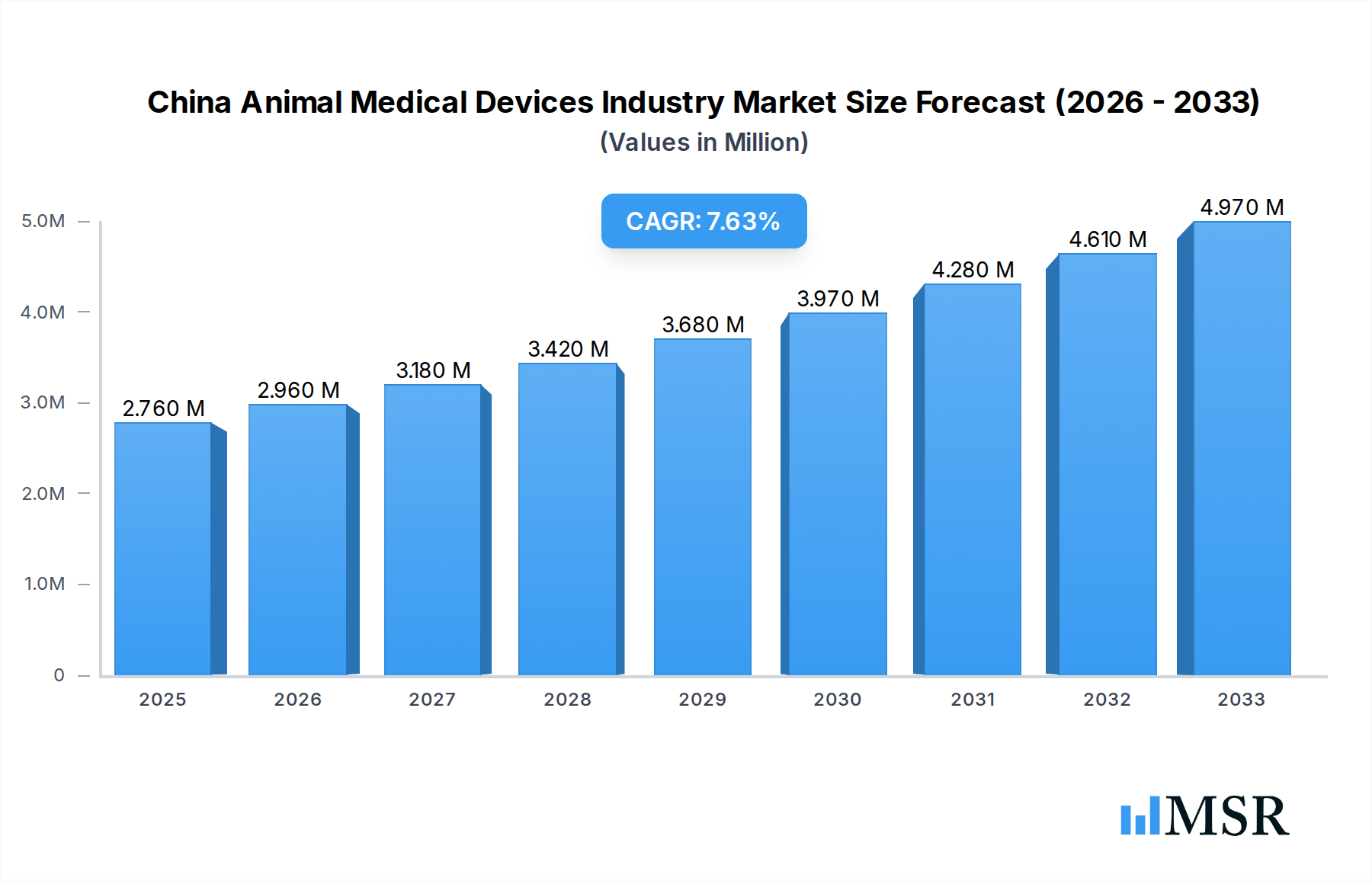

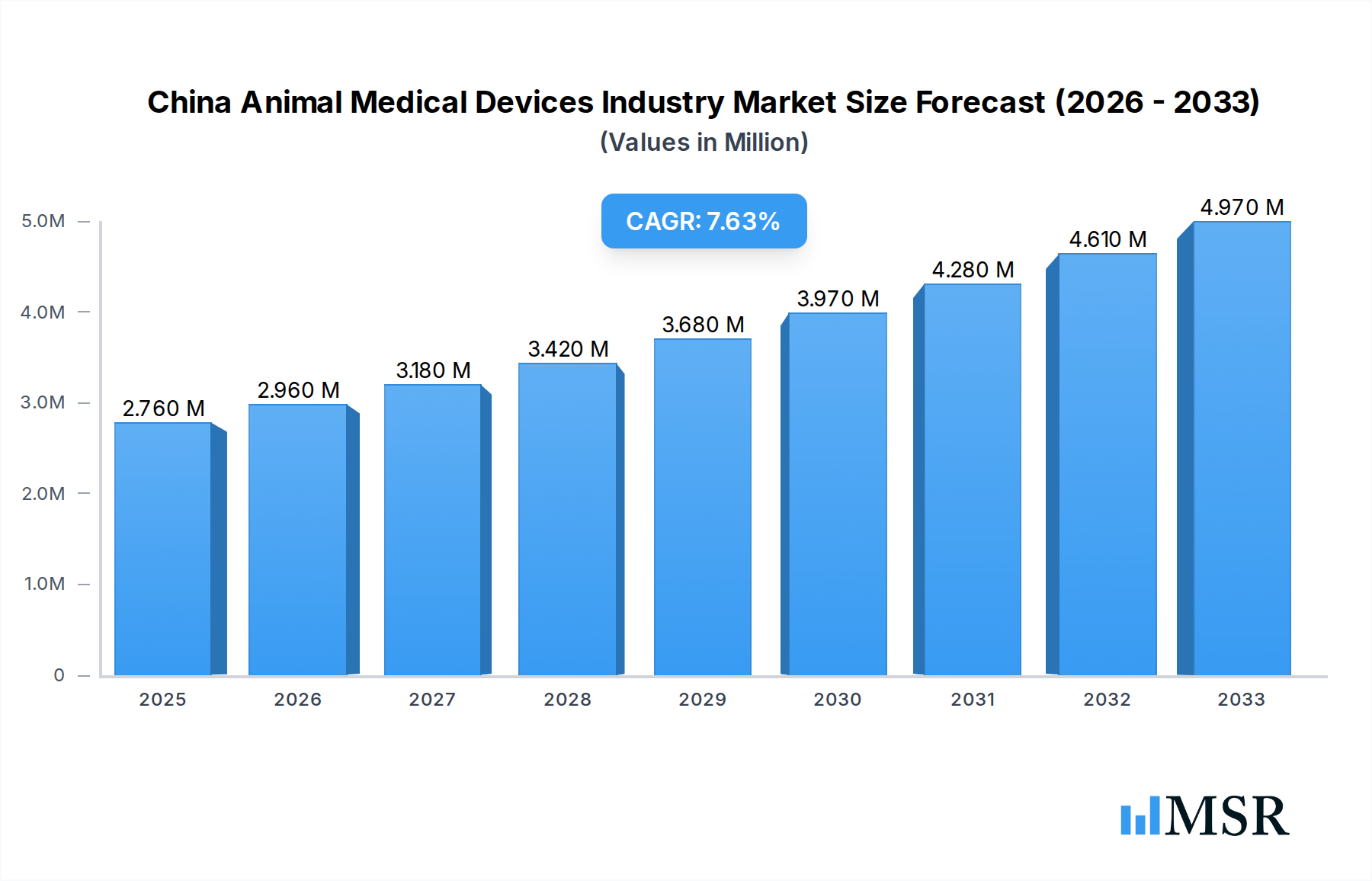

The China Animal Medical Devices Industry is poised for significant expansion, projecting a market size of 2.76 Million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 7.29%. This upward trajectory is fueled by a confluence of escalating pet ownership, a growing emphasis on companion animal health and welfare, and increasing government initiatives to enhance veterinary care infrastructure. The demand for advanced diagnostic tools, therapeutic solutions like vaccines and anti-infectives, and innovative medical devices for a wide range of animal types, from companion animals like dogs and cats to vital livestock such as poultry and swine, is a key catalyst. Furthermore, the growing awareness among farmers and pet owners regarding the economic benefits of disease prevention and early detection in animals contributes significantly to market growth.

China Animal Medical Devices Industry Market Size (In Million)

Emerging trends within the China Animal Medical Devices Industry indicate a strong shift towards precision medicine and digital health solutions. The increasing adoption of immunodiagnostic tests, molecular diagnostics, and diagnostic imaging technologies is enabling more accurate and faster disease identification, leading to improved treatment outcomes. While the market is characterized by a competitive landscape with major global players like Zoetis Inc., Merck & Co. Inc., and Bayer AG, alongside burgeoning domestic companies, the growth is also supported by an increasing number of veterinary clinics and hospitals adopting sophisticated equipment. Potential restraints might include regulatory hurdles for new product approvals and the initial cost of advanced technology for smaller veterinary practices, though the overall growth outlook remains exceptionally positive.

China Animal Medical Devices Industry Company Market Share

This comprehensive report delves into the dynamic China Animal Medical Devices Industry, a rapidly expanding sector driven by increasing pet ownership, a growing livestock industry, and advancements in veterinary technology. Analyze critical market segments, identify key growth drivers, and understand the competitive landscape from 2019–2033, with a base year of 2025. This report offers actionable insights for veterinary device manufacturers, pharmaceutical companies, diagnostic kit providers, animal health investors, and industry stakeholders seeking to capitalize on the immense potential of the Chinese animal healthcare market.

China Animal Medical Devices Industry Market Concentration & Dynamics

The China Animal Medical Devices Industry exhibits a moderately concentrated market, with a few dominant global players and a growing number of domestic innovators vying for market share. The market concentration is influenced by high barriers to entry, including stringent regulatory approvals and the need for significant R&D investment. Innovation ecosystems are flourishing, particularly around advancements in veterinary diagnostics and therapeutic devices. Regulatory frameworks, overseen by the Ministry of Agriculture and Rural Affairs of China, are evolving to align with global standards, fostering both opportunities and challenges for market participants. Substitute products are emerging, particularly in the realm of biologics and advanced animal nutrition, impacting traditional device markets. End-user trends are characterized by a growing demand for premium pet care and a greater emphasis on herd health and productivity in the livestock sector. Merger and acquisition (M&A) activities are on the rise, signaling consolidation and strategic expansion by major companies. We observed XX M&A deals within the historical period. The market share of leading players is estimated to be between 10-15% each, with smaller players holding significant combined market influence.

China Animal Medical Devices Industry Industry Insights & Trends

The China Animal Medical Devices Industry is poised for substantial growth, with a projected market size of over $15,000 Million by 2025 and an estimated Compound Annual Growth Rate (CAGR) of 8.5% during the forecast period of 2025–2033. This robust expansion is fueled by several interconnected factors. A primary growth driver is the escalating pet humanization trend in China, where pet owners increasingly view their animals as family members and are willing to invest in advanced medical care, including sophisticated veterinary diagnostic tests, surgical equipment, and therapeutic solutions. Concurrently, the modernization of China's livestock industry, driven by food safety concerns and the need for increased efficiency, is creating a significant demand for animal health monitoring devices, vaccines, and medical feed additives.

Technological disruptions are playing a pivotal role in shaping the industry. The rapid adoption of digital health technologies, such as telemedicine platforms for animal health and AI-powered diagnostic imaging analysis, is enhancing accessibility and precision in veterinary care. Furthermore, advancements in areas like genomic sequencing for disease prediction and the development of novel biologics are creating new product categories and expanding the therapeutic arsenal. Evolving consumer behaviors, characterized by a greater awareness of preventative healthcare for animals and a demand for high-quality, accessible veterinary services, are directly influencing product development and market strategies. The increasing disposable income of the Chinese population further underpins this growing expenditure on animal health.

Key Markets & Segments Leading China Animal Medical Devices Industry

The China Animal Medical Devices Industry is experiencing rapid growth across multiple segments, with significant dominance observed in specific areas.

By Product: Therapeutics

- Vaccines: This segment is a major revenue generator, driven by the continuous need for preventative healthcare in both companion animals and livestock. Economic growth and government initiatives promoting animal disease control are key drivers.

- Parasiticides: With the increasing prevalence of zoonotic diseases and a growing awareness of parasite control, this segment shows strong performance. Increased pet ownership and stringent regulations in the livestock sector contribute to its dominance.

- Anti-infectives: The demand for effective treatments for bacterial, viral, and fungal infections in animals remains consistently high, supported by advancements in drug discovery and formulation.

- Medical Feed Additives: Essential for optimizing animal growth, health, and feed efficiency in the livestock sector, this segment is crucial for meeting the demand for safe and affordable animal protein. Economic growth and the drive for improved agricultural productivity are key factors.

- Other Therapeutics: This category encompasses a wide range of innovative treatments and supportive care products, reflecting the expanding scope of veterinary medicine.

By Product: Diagnostics

- Immunodiagnostic Tests: These tests are widely adopted due to their speed, affordability, and accuracy in detecting various diseases, particularly in companion animals and poultry. Increased pet owner engagement and herd health management practices are drivers.

- Molecular Diagnostics: The growing sophistication of veterinary diagnostics, coupled with the demand for early disease detection and genetic testing, is fueling the growth of this segment. Technological advancements and research funding contribute to its expansion.

- Diagnostic Imaging: Investments in advanced imaging equipment like X-ray, ultrasound, and MRI are crucial for accurate diagnosis and treatment planning, especially in specialized veterinary practices and large animal hospitals. Economic growth and the development of sophisticated veterinary infrastructure are key.

- Clinical Chemistry: Essential for assessing the physiological state of animals and monitoring treatment efficacy, clinical chemistry analyzers and reagents are in high demand. Routine health checks and disease management protocols drive this segment.

- Other Diagnostics: This includes a broad spectrum of laboratory tests and tools that support comprehensive animal health assessments.

By Animal Type

- Dogs and Cats: This segment is experiencing explosive growth due to increasing pet ownership and the humanization trend. Owners are willing to spend significantly on advanced medical devices and treatments for their pets.

- Poultry: As a cornerstone of China's food supply, the poultry industry’s focus on disease prevention and efficient production drives substantial demand for vaccines, diagnostics, and medical feed additives.

- Swine: Similar to poultry, the swine sector is a significant consumer of veterinary medical devices due to its economic importance and the need for disease control and productivity enhancement.

- Ruminants: While a substantial market, the ruminant segment's growth is influenced by factors like dairy and beef production trends and the prevalence of specific diseases.

- Horses: With the growing popularity of equestrian sports and recreational riding, the horse segment is witnessing increasing demand for specialized medical devices and treatments.

- Other Animals: This segment encompasses a diverse range of animals, including small mammals and exotic pets, representing a niche but growing market.

China Animal Medical Devices Industry Product Developments

Product development in the China Animal Medical Devices Industry is characterized by a strong emphasis on innovation and customization. Companies are focusing on creating more advanced veterinary diagnostic kits with faster turnaround times and higher accuracy, leveraging technologies like point-of-care diagnostics and molecular testing. In the therapeutics space, there's a growing trend towards the development of novel vaccines with broader spectrum protection, less invasive anti-infective formulations, and targeted parasiticides. Furthermore, the integration of smart technologies, such as implantable microchips for animal identification and health monitoring, and sophisticated diagnostic imaging equipment with AI-driven analysis capabilities, are emerging as key areas of innovation, promising to enhance precision and efficiency in animal healthcare delivery.

Challenges in the China Animal Medical Devices Industry Market

The China Animal Medical Devices Industry faces several challenges that can impact growth and market penetration. These include navigating complex and evolving regulatory pathways for product approval, which can lead to extended market entry timelines and increased R&D costs. Supply chain disruptions, exacerbated by global events, can affect the availability of raw materials and finished products, impacting production schedules and pricing. Intense competition from both global giants and burgeoning domestic players can put pressure on profit margins and necessitate continuous innovation to maintain market share. Furthermore, the cost sensitivity of certain market segments, particularly in some agricultural regions, can limit the adoption of high-end devices.

Forces Driving China Animal Medical Devices Industry Growth

The growth of the China Animal Medical Devices Industry is propelled by several key forces. The escalating pet humanization trend is a significant economic driver, leading to increased consumer spending on premium veterinary care. Government initiatives aimed at improving animal welfare, food safety, and the modernization of the agricultural sector provide a favorable regulatory and economic environment. Technological advancements in areas such as biotechnology, data analytics, and minimally invasive surgical techniques are creating new product opportunities and enhancing the efficacy of existing solutions. The increasing demand for animal-derived protein, coupled with the need for efficient livestock management, further fuels the adoption of advanced veterinary devices and diagnostics.

Challenges in the China Animal Medical Devices Industry Market

Long-term growth catalysts for the China Animal Medical Devices Industry include the ongoing investment in research and development by both multinational corporations and domestic enterprises, leading to a pipeline of innovative products. Strategic partnerships and collaborations between device manufacturers, research institutions, and veterinary clinics are fostering knowledge exchange and accelerating product commercialization. Market expansion into underserved rural areas and the development of more affordable and accessible veterinary solutions will unlock significant growth potential. Furthermore, the continuous evolution of animal health regulations towards international standards will likely create a more predictable and conducive market environment for sustained growth.

Emerging Opportunities in China Animal Medical Devices Industry

Emerging opportunities in the China Animal Medical Devices Industry are abundant. The rapid growth of the companion animal segment presents significant opportunities for innovative pet care devices, advanced diagnostic imaging equipment, and specialized therapeutic solutions. The increasing focus on preventative healthcare and early disease detection is driving demand for sophisticated veterinary diagnostic tests, including molecular diagnostics and biomarker analysis. The development of connected devices and digital health platforms for remote animal health monitoring and telemedicine offers a substantial growth avenue. Furthermore, exploring the potential of regenerative medicine and personalized veterinary treatments represents a frontier for future innovation and market leadership.

Leading Players in the China Animal Medical Devices Industry Sector

- Merck & Co Inc

- Bayer AG

- China Animal Husbandry Co Ltd

- Vetoquinol SA

- Boehringer Ingelheim GMBH

- Virbac Corporation

- BioChek BV

- Ceva Sante Animale

- Elanco Animal Health Incorporated

- Zoetis Inc

Key Milestones in China Animal Medical Devices Industry Industry

- May 2021: Boehringer Ingelheim launched GastroGard (omeprazole oral paste) in the Chinese market, receiving the Registration Certificate of Imported Veterinary Drug from the Ministry of Agriculture and Rural Affairs of China, marking the first imported equine drug approval.

- September 2020: Boehringer Ingelheim acquired an equity stake in China-based New Ruipeng Group (NRP Group), a rapidly growing business offering veterinary care, e-commerce, and other services to pet owners and the broader animal health market across China.

Strategic Outlook for China Animal Medical Devices Industry Market

The strategic outlook for the China Animal Medical Devices Industry is highly positive, characterized by sustained growth and significant opportunities for market leaders. The increasing disposable income, coupled with a deepening emotional connection to pets, will continue to drive demand for premium veterinary care. Advancements in technology will facilitate the introduction of more precise, efficient, and less invasive diagnostic and therapeutic devices. Companies that focus on R&D, strategic partnerships, and localized market strategies will be best positioned to capitalize on this burgeoning market. Expansion into emerging segments like exotic pets and the integration of digital health solutions will be crucial for long-term success and market dominance.

China Animal Medical Devices Industry Segmentation

-

1. Product

-

1.1. By Therapeutics

- 1.1.1. Vaccines

- 1.1.2. Parasiticides

- 1.1.3. Anti-infectives

- 1.1.4. Medical Feed Additives

- 1.1.5. Other Therapeutics

-

1.2. By Diagnostics

- 1.2.1. Immunodiagnostic Tests

- 1.2.2. Molecular Diagnostics

- 1.2.3. Diagnostic Imaging

- 1.2.4. Clinical Chemistry

- 1.2.5. Other Diagnostics

-

1.1. By Therapeutics

-

2. Animal Type

- 2.1. Dogs and Cats

- 2.2. Horses

- 2.3. Ruminants

- 2.4. Swine

- 2.5. Poultry

- 2.6. Other Animals

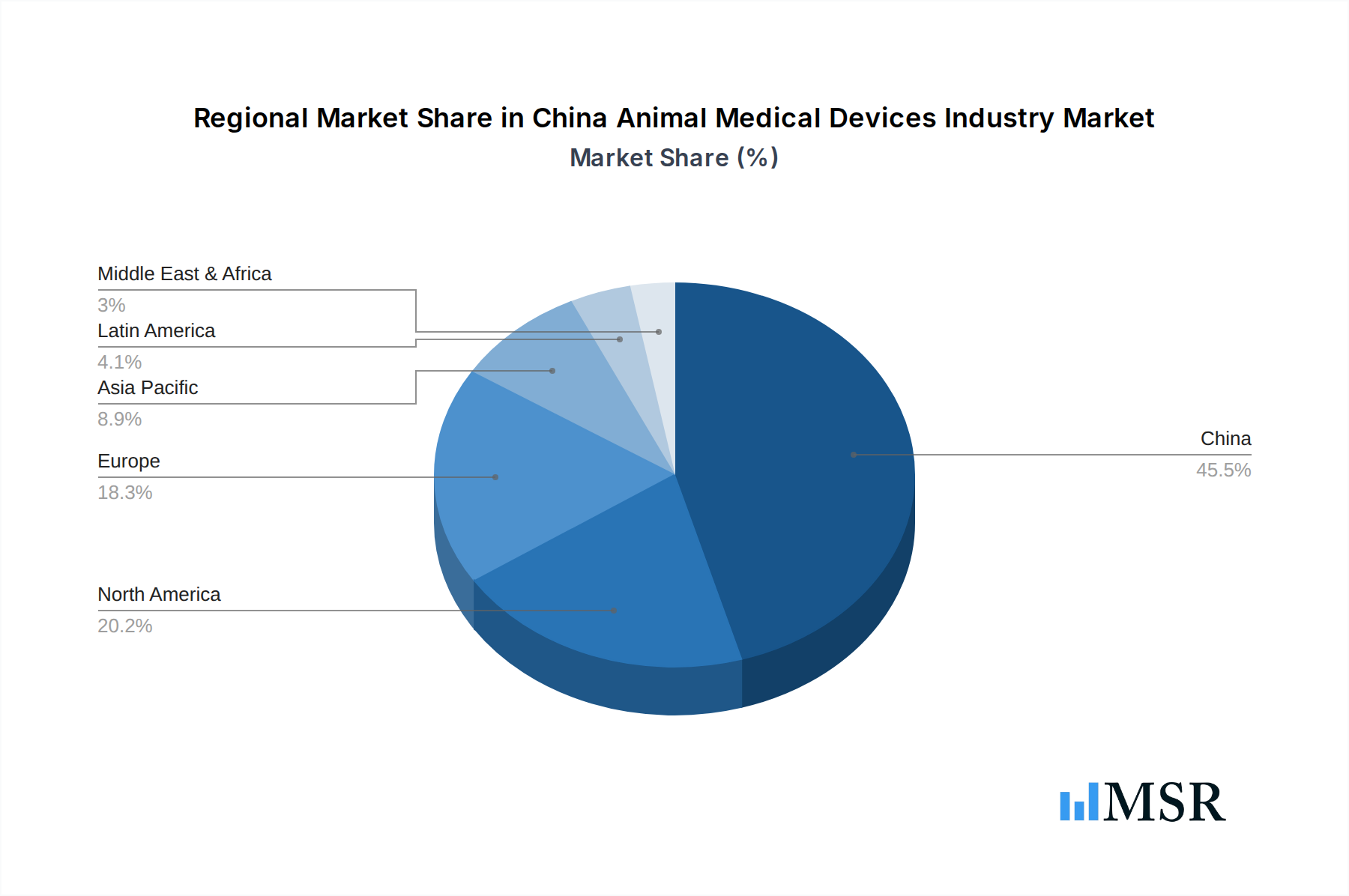

China Animal Medical Devices Industry Segmentation By Geography

- 1. China

China Animal Medical Devices Industry Regional Market Share

Geographic Coverage of China Animal Medical Devices Industry

China Animal Medical Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. By Therapeutics

- 5.1.1.1. Vaccines

- 5.1.1.2. Parasiticides

- 5.1.1.3. Anti-infectives

- 5.1.1.4. Medical Feed Additives

- 5.1.1.5. Other Therapeutics

- 5.1.2. By Diagnostics

- 5.1.2.1. Immunodiagnostic Tests

- 5.1.2.2. Molecular Diagnostics

- 5.1.2.3. Diagnostic Imaging

- 5.1.2.4. Clinical Chemistry

- 5.1.2.5. Other Diagnostics

- 5.1.1. By Therapeutics

- 5.2. Market Analysis, Insights and Forecast - by Animal Type

- 5.2.1. Dogs and Cats

- 5.2.2. Horses

- 5.2.3. Ruminants

- 5.2.4. Swine

- 5.2.5. Poultry

- 5.2.6. Other Animals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. China Animal Medical Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. By Therapeutics

- 6.1.1.1. Vaccines

- 6.1.1.2. Parasiticides

- 6.1.1.3. Anti-infectives

- 6.1.1.4. Medical Feed Additives

- 6.1.1.5. Other Therapeutics

- 6.1.2. By Diagnostics

- 6.1.2.1. Immunodiagnostic Tests

- 6.1.2.2. Molecular Diagnostics

- 6.1.2.3. Diagnostic Imaging

- 6.1.2.4. Clinical Chemistry

- 6.1.2.5. Other Diagnostics

- 6.1.1. By Therapeutics

- 6.2. Market Analysis, Insights and Forecast - by Animal Type

- 6.2.1. Dogs and Cats

- 6.2.2. Horses

- 6.2.3. Ruminants

- 6.2.4. Swine

- 6.2.5. Poultry

- 6.2.6. Other Animals

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Merck & Co Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bayer AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 China Animal Husbandry Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Vetoquinol SA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Boehringer Ingelheim GMBH

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Virbac Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BioChek BV

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ceva Sante Animale

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Elanco Animal Health Incorporated

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Zoetis Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Merck & Co Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Animal Medical Devices Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Animal Medical Devices Industry Share (%) by Company 2025

List of Tables

- Table 1: China Animal Medical Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: China Animal Medical Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 3: China Animal Medical Devices Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 4: China Animal Medical Devices Industry Volume K Unit Forecast, by Animal Type 2020 & 2033

- Table 5: China Animal Medical Devices Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: China Animal Medical Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: China Animal Medical Devices Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 8: China Animal Medical Devices Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 9: China Animal Medical Devices Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 10: China Animal Medical Devices Industry Volume K Unit Forecast, by Animal Type 2020 & 2033

- Table 11: China Animal Medical Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: China Animal Medical Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Animal Medical Devices Industry?

The projected CAGR is approximately 7.29%.

2. Which companies are prominent players in the China Animal Medical Devices Industry?

Key companies in the market include Merck & Co Inc, Bayer AG, China Animal Husbandry Co Ltd, Vetoquinol SA, Boehringer Ingelheim GMBH, Virbac Corporation, BioChek BV, Ceva Sante Animale, Elanco Animal Health Incorporated, Zoetis Inc.

3. What are the main segments of the China Animal Medical Devices Industry?

The market segments include Product, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.76 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Pet Adoption; Advanced Technology in Animal Healthcare; Rise in the number of Initiatives by Governments and Animal Welfare Associations.

6. What are the notable trends driving market growth?

The Dogs and Cats Segment Dominates the China Veterinary Healthcare Market.

7. Are there any restraints impacting market growth?

Use of Counterfeit Medicines; Increasing Costs of Animal Testing and Veterinary Care.

8. Can you provide examples of recent developments in the market?

In May 2021, Boehringer Ingelheim has launched GastroGard(omeprazole oral paste) in the Chinese market, has been granted by the Registration Certificate of Imported Veterinary Drug by the Ministry of Agriculture and Rural Affairs of China, making it the first equine drug approved to be imported into the China market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Animal Medical Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Animal Medical Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Animal Medical Devices Industry?

To stay informed about further developments, trends, and reports in the China Animal Medical Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence