Key Insights

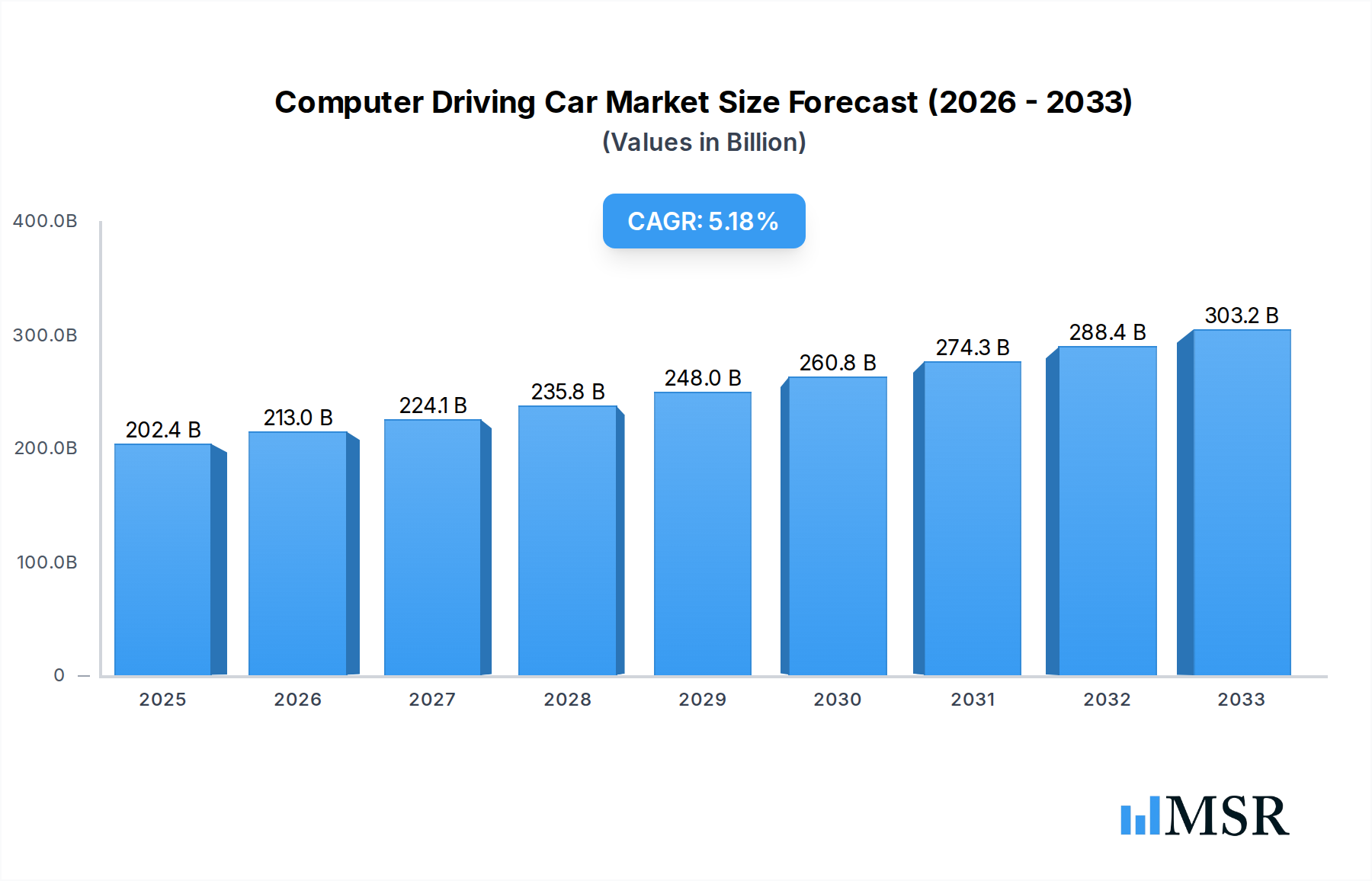

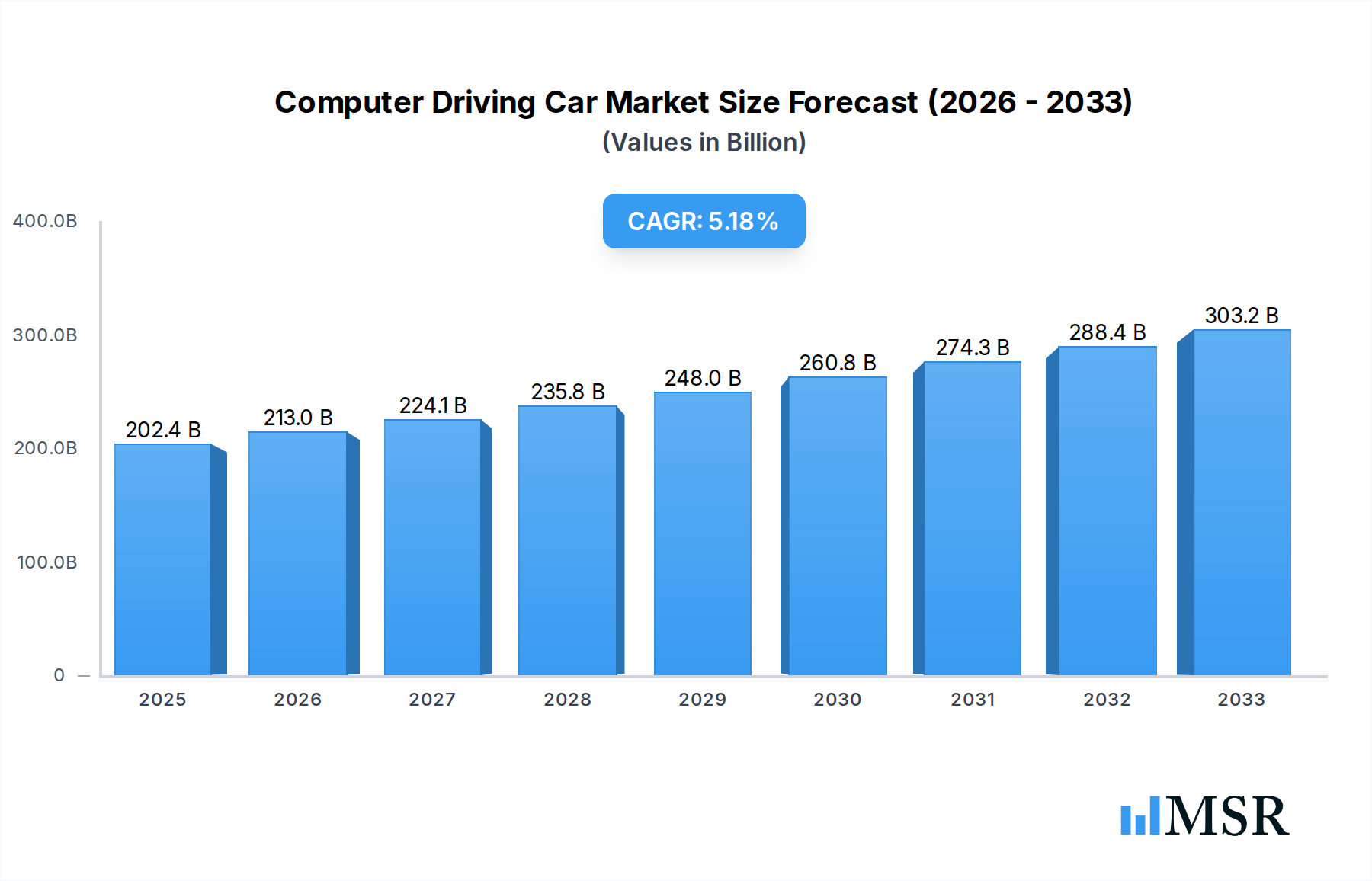

The Computer Driving Car market is poised for substantial expansion, projected to reach USD 202.4 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.4% expected throughout the forecast period of 2025-2033. This significant growth is propelled by a confluence of powerful drivers, including advancements in Artificial Intelligence (AI) and machine learning, the increasing demand for enhanced vehicle safety features, and the growing consumer interest in autonomous driving experiences. The development of sophisticated sensors, high-performance computing, and precise navigation systems are critical enablers for this market. Furthermore, the supportive regulatory frameworks being established by governments worldwide, alongside significant investments from both established automotive giants and innovative tech companies, are accelerating the adoption of autonomous driving technologies. The market is witnessing a dual-pronged evolution, with applications spanning both commercial vehicles, promising greater efficiency in logistics and transportation, and passenger cars, aiming to revolutionize personal mobility and urban commuting.

Computer Driving Car Market Size (In Billion)

The market's trajectory is further shaped by evolving consumer preferences and technological integration. While the semi-autonomous segment continues to offer advanced driver-assistance systems (ADAS) that enhance safety and convenience, the fully autonomous segment represents the future, promising to free up driver time and redefine transportation. Key players like Daimler, Toyota Motor, BMW, and Volkswagen, alongside tech innovators such as Apple, are heavily investing in research and development, forming strategic alliances, and actively working towards commercializing these advanced systems. However, challenges such as high development costs, cybersecurity concerns, ethical dilemmas surrounding accident scenarios, and public acceptance hurdles need to be addressed to ensure widespread and seamless integration. Despite these restraints, the overarching trend towards smarter, safer, and more connected vehicles, coupled with the potential for improved traffic flow and reduced emissions, paints a promising picture for the future of computer driving cars.

Computer Driving Car Company Market Share

Computer Driving Car Market Report Description

This comprehensive report, "Computer Driving Car Market: Global Analysis and Forecast 2019–2033," offers an in-depth exploration of the rapidly evolving landscape of autonomous vehicle technology. Spanning a study period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this analysis provides critical insights for industry stakeholders, investors, and strategists. Discover the market concentration, key trends, dominant segments, product innovations, challenges, growth drivers, emerging opportunities, leading players, and pivotal milestones that are shaping the future of computer driving cars, autonomous driving technology, self-driving cars, and advanced driver-assistance systems (ADAS). This report is essential for understanding the trajectory of commercial vehicle and passenger car autonomy, encompassing both semi-autonomous and fully autonomous vehicle segments.

Computer Driving Car Market Concentration & Dynamics

The computer driving car market is characterized by dynamic shifts, with significant investment in innovation ecosystems and evolving regulatory frameworks playing pivotal roles. Market concentration is influenced by a handful of major automotive manufacturers and burgeoning tech companies. Key players like Daimler, Ford Motor, Toyota Motor, BMW, Audi, Volvo, Volkswagen, and Apple are investing billions in research and development, aiming to capture substantial market share. The autonomous driving technology sector sees a mix of in-house development and strategic partnerships. Competition is intensifying, driven by technological advancements and the pursuit of market leadership. The regulatory landscape is a critical factor, with governments worldwide developing guidelines and standards for the safe deployment of self-driving cars. Substitute products, such as advanced driver-assistance systems (ADAS) that enhance human driving capabilities rather than fully replacing the driver, continue to hold a significant presence, though their long-term relevance is challenged by the rapid progress in fully autonomous systems. End-user trends are increasingly favoring enhanced safety, convenience, and efficiency, particularly in commercial vehicle applications like logistics and ride-sharing. Mergers and acquisitions (M&A) activity is a key indicator of market consolidation and strategic positioning. Recent M&A deals, totaling an estimated billion dollar value, reflect companies consolidating capabilities and acquiring crucial technologies. The Dutch Automated Vehicle Initiative (DAVI) and AutoNOMOS Labs exemplify research and development hubs driving innovation. The market share of leading entities is projected to see significant shifts over the forecast period as deployment scales.

Computer Driving Car Industry Insights & Trends

The computer driving car industry is poised for unprecedented growth, driven by a confluence of technological advancements, shifting consumer behaviors, and supportive economic factors. The global market size is projected to reach trillions of dollars by 2033, with a compound annual growth rate (CAGR) exceeding xx% during the forecast period. The primary growth drivers include the relentless pursuit of enhanced road safety, aiming to drastically reduce accidents caused by human error, which accounts for billions of dollars in economic losses annually. The increasing demand for convenience and efficiency, particularly in urban environments and for commercial vehicle fleets, is another significant catalyst. Technological disruptions, including rapid advancements in Artificial Intelligence (AI), machine learning, sensor technology (LiDAR, radar, cameras), and high-definition mapping, are making fully autonomous driving increasingly feasible and reliable. The development of robust V2X (Vehicle-to-Everything) communication infrastructure is crucial for seamless integration of self-driving cars into existing traffic systems. Consumer adoption is gradually increasing as awareness grows and the benefits of autonomous driving technology become more apparent. Early adopters and fleet operators are paving the way for broader market acceptance. The evolution of semi-autonomous features, such as advanced adaptive cruise control and lane-keeping assist, serves as a stepping stone towards full autonomy, familiarizing consumers with automated driving capabilities. The economic impact of this sector is multifaceted, encompassing job creation in new technology fields, reduced transportation costs for businesses, and the potential for new mobility-as-a-service (MaaS) models. The integration of computer driving car technology into various platforms, from personal passenger cars to heavy-duty trucks, signifies a transformative shift in the automotive industry, with billions being invested by major players like Tesela and Volkswagen.

Key Markets & Segments Leading Computer Driving Car

The computer driving car market is experiencing significant regional and segmental dominance, with specific applications and vehicle types leading the charge.

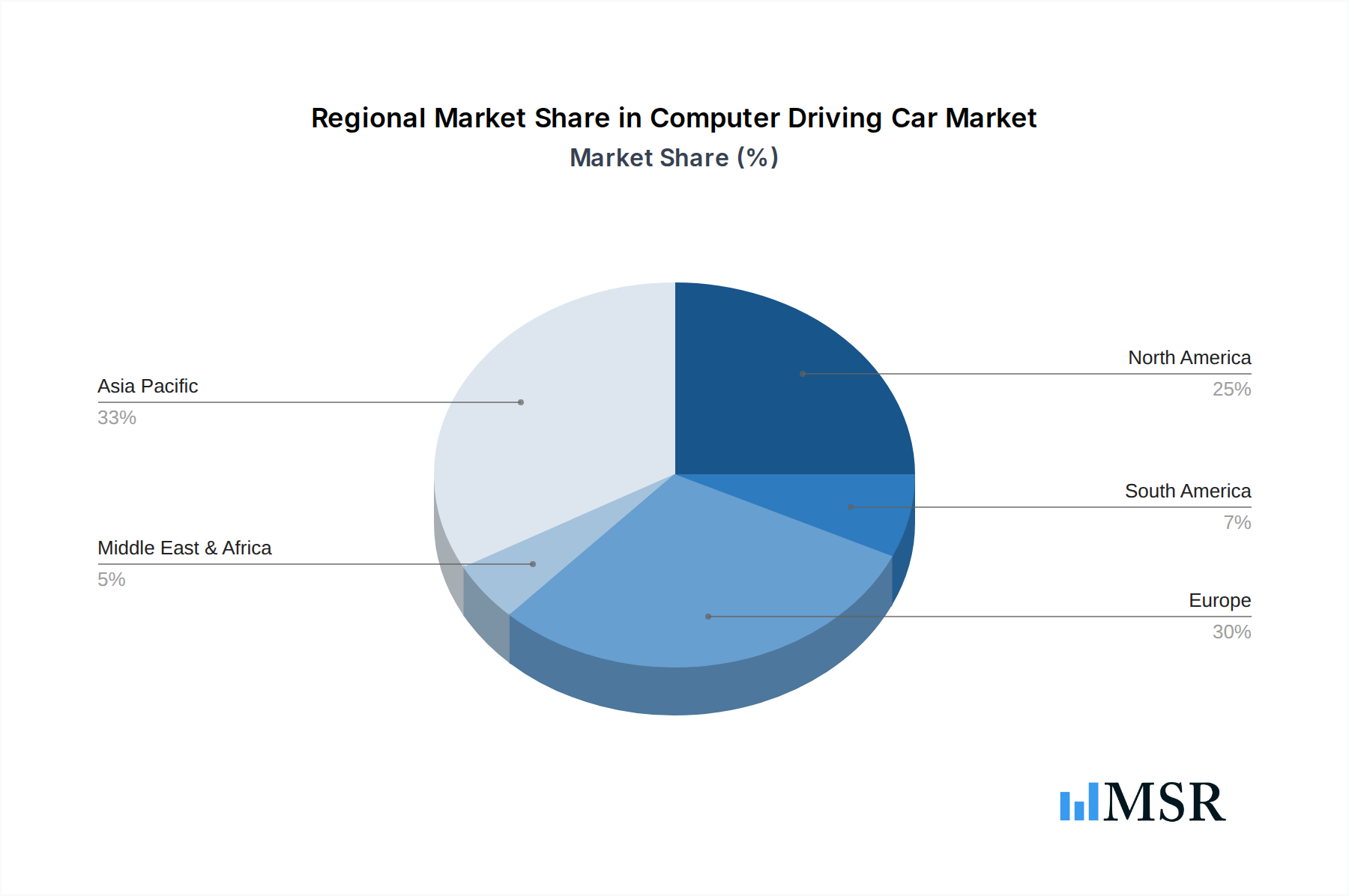

Dominant Region: North America and Europe are currently leading the adoption and development of autonomous driving technology, driven by robust R&D investments, favorable regulatory environments in select regions, and a strong consumer appetite for advanced vehicle features. Asian markets, particularly China, are rapidly catching up, fueled by government initiatives and massive domestic automotive industries.

Dominant Application Segments:

- Commercial Vehicle: This segment is expected to be a major driver of early autonomous driving adoption due to the potential for significant cost savings in logistics, trucking, and delivery services. The pursuit of increased operational efficiency, reduced labor costs, and enhanced fleet management is propelling investment. Companies are exploring fully autonomous solutions for long-haul trucking and last-mile delivery, with projected efficiency gains translating into billions in savings.

- Passenger Car: While adoption might be slower due to consumer trust and regulatory complexities, the passenger car segment is a significant long-term market. The convenience, safety, and accessibility benefits are compelling, especially for urban commuting and for individuals with mobility challenges. The ongoing development of semi-autonomous features in mainstream vehicles is preparing consumers for more advanced capabilities.

Dominant Vehicle Types:

- Semi-Autonomous: Currently, semi-autonomous systems represent the largest segment of the market. Features like adaptive cruise control, lane centering, and automatic parking are becoming increasingly common, offering tangible benefits to drivers without requiring complete relinquishment of control. These systems are crucial for building consumer confidence.

- Fully Autonomous: While still in its nascent stages for widespread public deployment, fully autonomous vehicles (Level 4 and Level 5) are the ultimate goal. Early deployments are being seen in controlled environments and specific use cases, such as robotaxis and autonomous shuttles in designated zones. The potential to revolutionize personal mobility and logistics is immense, with billions in future market value tied to this segment.

Drivers of Dominance:

- Economic Growth: Strong economies support higher consumer spending on advanced vehicle technologies and provide the capital for extensive R&D and infrastructure development.

- Technological Advancement: Breakthroughs in AI, sensor technology, and connectivity are critical enablers for sophisticated autonomous systems.

- Regulatory Support: Proactive and clear regulatory frameworks are essential for testing, validation, and widespread deployment of self-driving cars.

- Infrastructure Development: Investment in smart city initiatives and advanced road infrastructure capable of supporting autonomous vehicles is crucial.

- Consumer Demand: Growing awareness and acceptance of the benefits of autonomous driving are fostering market demand.

Computer Driving Car Product Developments

Product innovation in the computer driving car market is rapidly advancing, with a focus on enhancing safety, efficiency, and user experience. Leading companies are continuously refining sensor suites, AI algorithms, and connectivity solutions. Key developments include more sophisticated object detection and prediction systems, improved decision-making capabilities for complex traffic scenarios, and seamless integration of semi-autonomous and fully autonomous driving modes. The market relevance is growing as these technologies move from research labs to real-world testing and early commercial deployments. Competitive edges are being gained through superior processing power, advanced mapping capabilities, and robust cybersecurity measures. The application of computer driving car technology extends beyond personal vehicles, with significant progress in autonomous solutions for public transportation and logistics, promising billions in operational savings and new service models.

Challenges in the Computer Driving Car Market

The computer driving car market faces significant challenges that need to be overcome for widespread adoption. These include:

- Regulatory Hurdles: The lack of standardized global regulations and the complexities of liability frameworks create uncertainty and slow down deployment. Billions in potential market growth are contingent on clear legal guidelines.

- Public Trust and Acceptance: Building consumer confidence in the safety and reliability of self-driving cars remains a critical barrier. Accidents, even rare ones, can significantly impact public perception.

- High Development and Implementation Costs: The research, development, testing, and deployment of autonomous driving technology require substantial capital investment, running into billions.

- Cybersecurity Threats: Ensuring the security of autonomous vehicle systems against hacking and malicious attacks is paramount.

- Infrastructure Readiness: The existing road infrastructure in many regions is not yet optimized for fully autonomous vehicles, requiring significant upgrades.

Forces Driving Computer Driving Car Growth

Several powerful forces are propelling the growth of the computer driving car market. Technological advancements, particularly in artificial intelligence, machine learning, and sensor technology, are making autonomous driving more sophisticated and reliable. The economic imperative to improve safety and reduce the billions lost annually due to traffic accidents is a major driver. Furthermore, the increasing demand for convenience, efficiency, and new mobility services is shaping consumer preferences. Supportive government initiatives and the development of clear regulatory frameworks in key markets are also crucial catalysts. The successful integration of semi-autonomous features is building consumer familiarity and trust, paving the way for fully autonomous solutions.

Challenges in the Computer Driving Car Market

Long-term growth catalysts for the computer driving car market are rooted in continued technological innovation and strategic market expansions. Breakthroughs in areas like sensor fusion, predictive analytics, and vehicle-to-everything (V2X) communication will be instrumental in achieving higher levels of autonomy and safety. The establishment of robust data-sharing protocols and collaborative partnerships between automakers, tech companies, and infrastructure providers will accelerate development. As fully autonomous systems become more prevalent, new business models like autonomous ride-hailing services and integrated logistics solutions will emerge, unlocking significant market potential, estimated in the trillions.

Emerging Opportunities in Computer Driving Car

Emerging opportunities in the computer driving car market are vast and transformative. The development of specialized autonomous vehicles for niche applications, such as autonomous agricultural machinery and construction equipment, presents significant untapped markets. The integration of computer driving car technology into smart city initiatives, creating seamless urban mobility ecosystems, is another major opportunity. The growing demand for accessibility solutions for the elderly and individuals with disabilities will drive innovation in specialized autonomous transport. Furthermore, the potential for autonomous vehicles to revolutionize freight transportation and logistics, creating more efficient and cost-effective supply chains, offers substantial growth prospects, with billions in annual savings projected.

Leading Players in the Computer Driving Car Sector

- Daimler

- Ford Motor

- Toyota Motor

- BMW

- Audi

- Volvo

- Volkswagen

- Apple

- Tesela

Key Milestones in Computer Driving Car Industry

- 2019: Initial deployments of advanced Level 2 semi-autonomous features in mass-market passenger cars.

- 2020: Significant advancements in AI and sensor technology, enabling more complex autonomous driving simulations and testing.

- 2021: Increased regulatory discussions and initial frameworks for autonomous vehicle testing in several key regions.

- 2022: Pilot programs for autonomous ride-hailing services in select cities demonstrating the viability of Level 4 autonomy.

- 2023: Major automotive and technology companies announcing billions in investment for autonomous driving R&D and partnerships.

- 2024: Expansion of autonomous trucking pilot programs on highways, highlighting efficiency gains.

- 2025: Projected wider availability of advanced semi-autonomous features and increased regulatory clarity for certain autonomous applications.

Strategic Outlook for Computer Driving Car Market

The strategic outlook for the computer driving car market is one of rapid expansion and technological convergence. Growth accelerators will be driven by strategic partnerships between traditional automotive manufacturers and technology giants, fostering innovation and accelerating product development. The increasing focus on fully autonomous solutions for commercial applications, such as logistics and ride-sharing, will unlock substantial revenue streams, estimated in the trillions. Investment in robust cybersecurity measures and the development of standardized safety protocols will be crucial for widespread adoption and public trust. The market's trajectory suggests a future where computer driving cars redefine mobility, transport, and urban planning, creating new economic opportunities and societal benefits.

Computer Driving Car Segmentation

-

1. Application

- 1.1. Commercial Vehicle

- 1.2. Passenger Car

-

2. Types

- 2.1. Semi-Autonomous

- 2.2. Fully Autonomous

Computer Driving Car Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Computer Driving Car Regional Market Share

Geographic Coverage of Computer Driving Car

Computer Driving Car REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Computer Driving Car Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicle

- 5.1.2. Passenger Car

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Semi-Autonomous

- 5.2.2. Fully Autonomous

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Computer Driving Car Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicle

- 6.1.2. Passenger Car

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Semi-Autonomous

- 6.2.2. Fully Autonomous

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Computer Driving Car Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicle

- 7.1.2. Passenger Car

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Semi-Autonomous

- 7.2.2. Fully Autonomous

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Computer Driving Car Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicle

- 8.1.2. Passenger Car

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Semi-Autonomous

- 8.2.2. Fully Autonomous

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Computer Driving Car Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicle

- 9.1.2. Passenger Car

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Semi-Autonomous

- 9.2.2. Fully Autonomous

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Computer Driving Car Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicle

- 10.1.2. Passenger Car

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Semi-Autonomous

- 10.2.2. Fully Autonomous

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Daimler

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ford Motor

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Toyota Motor

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BMW

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Audi

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Volvo

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Dutch Automated Vehicle Initiative (DAVI)

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AutoNOMOS Labs

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Volkswagen

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tesela

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Apple

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Daimler

List of Figures

- Figure 1: Global Computer Driving Car Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Computer Driving Car Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Computer Driving Car Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Computer Driving Car Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Computer Driving Car Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Computer Driving Car Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Computer Driving Car Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Computer Driving Car Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Computer Driving Car Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Computer Driving Car Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Computer Driving Car Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Computer Driving Car Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Computer Driving Car Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Computer Driving Car Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Computer Driving Car Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Computer Driving Car Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Computer Driving Car Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Computer Driving Car Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Computer Driving Car Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Computer Driving Car Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Computer Driving Car Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Computer Driving Car Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Computer Driving Car Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Computer Driving Car Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Computer Driving Car Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Computer Driving Car Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Computer Driving Car Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Computer Driving Car Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Computer Driving Car Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Computer Driving Car Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Computer Driving Car Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Computer Driving Car Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Computer Driving Car Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Computer Driving Car Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Computer Driving Car Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Computer Driving Car Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Computer Driving Car Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Computer Driving Car Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Computer Driving Car Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Computer Driving Car Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Computer Driving Car Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Computer Driving Car Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Computer Driving Car Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Computer Driving Car Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Computer Driving Car Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Computer Driving Car Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Computer Driving Car Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Computer Driving Car Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Computer Driving Car Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Computer Driving Car Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Computer Driving Car?

The projected CAGR is approximately 5.4%.

2. Which companies are prominent players in the Computer Driving Car?

Key companies in the market include Daimler, Ford Motor, Toyota Motor, BMW, Audi, Volvo, Dutch Automated Vehicle Initiative (DAVI), AutoNOMOS Labs, Volkswagen, Tesela, Apple.

3. What are the main segments of the Computer Driving Car?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 202.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Computer Driving Car," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Computer Driving Car report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Computer Driving Car?

To stay informed about further developments, trends, and reports in the Computer Driving Car, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence