Key Insights into the Oral Drug Delivery Market

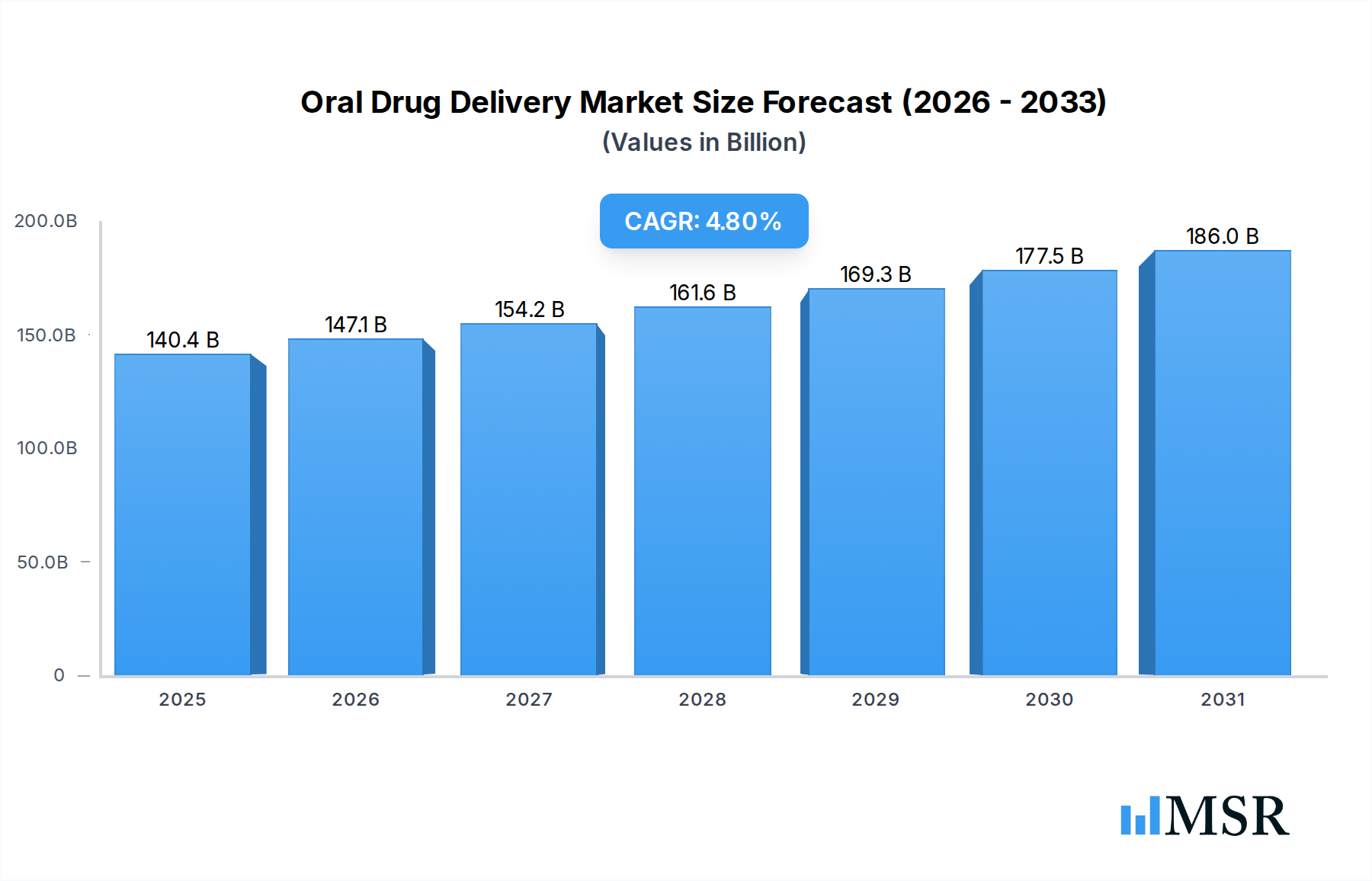

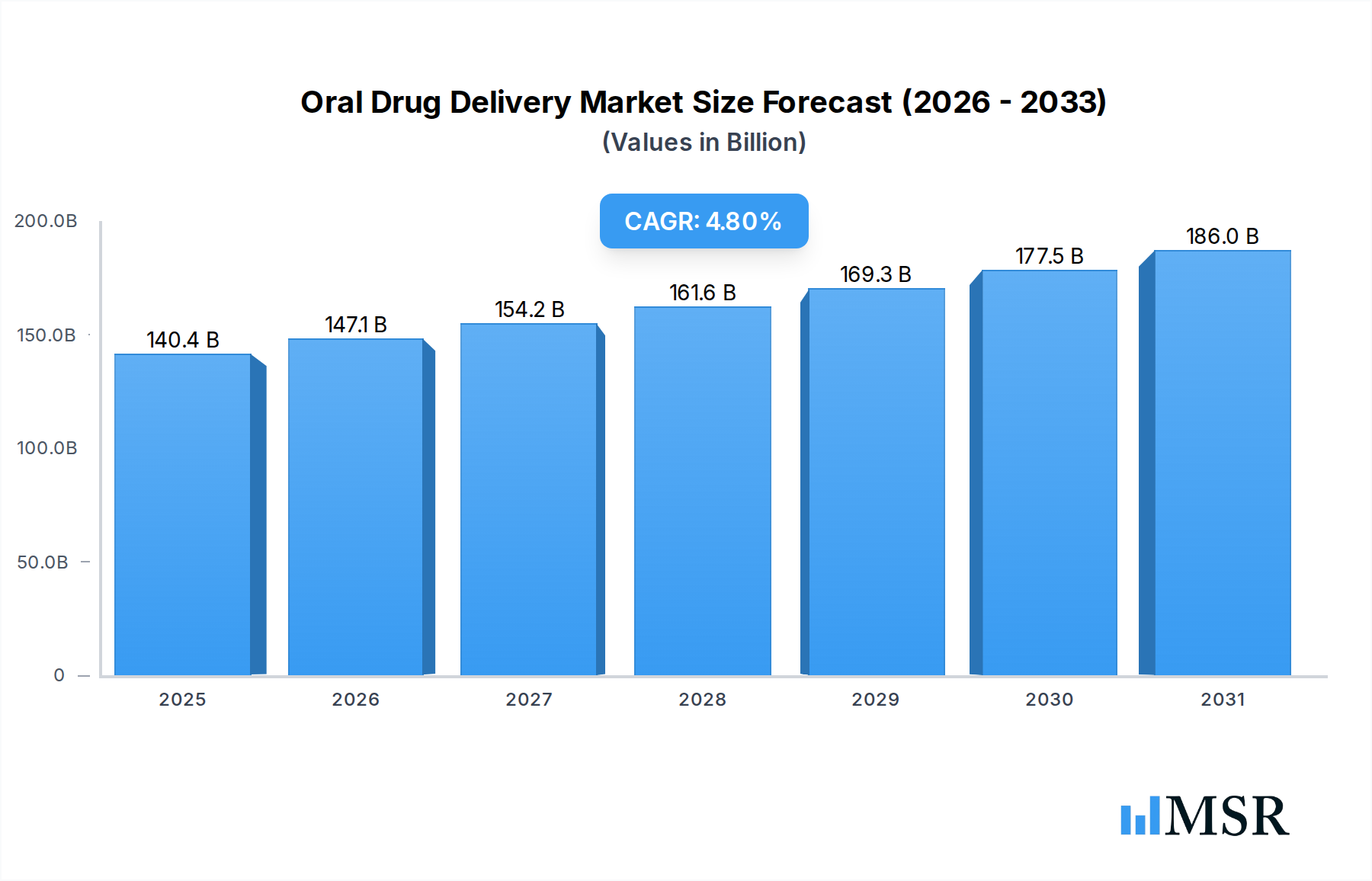

The global Oral Drug Delivery Market, valued at $133.94 billion in 2025, is poised for robust expansion, projected to reach approximately $204.1 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 4.8% over the forecast period. This significant growth trajectory is primarily propelled by a confluence of factors, including the escalating prevalence of chronic diseases globally, increasing patient preference for non-invasive drug administration routes, and continuous advancements in drug formulation technologies. Oral drug delivery systems offer unparalleled convenience, cost-effectiveness, and enhanced patient compliance compared to parenteral alternatives, making them the preferred choice for a vast array of therapeutic indications.

Oral Drug Delivery Market Size (In Billion)

Key demand drivers for the Oral Drug Delivery Market encompass the rising geriatric population, which inherently necessitates long-term medication regimens, and the burgeoning pipeline of small molecule drugs. Macro tailwinds such as increasing healthcare expenditure in emerging economies, government initiatives promoting affordable healthcare, and substantial research and development investments by pharmaceutical companies further bolster market expansion. Innovations in excipient technologies, enabling improved drug solubility, bioavailability, and targeted release, are pivotal. The shift towards personalized medicine and the growing demand for orally administered biologics via advanced encapsulation techniques are also shaping the market's future. The increasing prevalence of cardiovascular diseases, diabetes, and infectious diseases, for which oral medications are often the first line of treatment, underpins a consistent and growing demand across regional markets.

Oral Drug Delivery Company Market Share

The forward-looking outlook indicates a sustained focus on developing novel oral formulations that overcome challenges such as poor aqueous solubility, gastric degradation, and low permeability. The development of advanced systems like sustained-release tablets, orally disintegrating tablets (ODTs), and gastro-retentive systems is expected to unlock new therapeutic possibilities and expand the application scope of oral delivery. Strategic collaborations between drug developers and contract manufacturing organizations (CMOs) are becoming increasingly common to optimize manufacturing processes and accelerate market entry for new oral drug products. Furthermore, the expansion of healthcare infrastructure and accessibility in developing regions presents substantial untapped opportunities, reinforcing the Oral Drug Delivery Market's position as a cornerstone of modern pharmacotherapy.

Dominant Dosage Form Segment in Oral Drug Delivery Market

Within the broader Oral Drug Delivery Market, the Tablets sub-segment, under the Dosage Form category, currently holds the most substantial revenue share and is anticipated to maintain its dominance throughout the forecast period. This leadership is attributed to several intrinsic advantages that tablets offer, making them the most widely accepted and utilized solid oral dosage form. These advantages include superior manufacturing simplicity and scalability, which translates into lower production costs compared to more complex formulations. The inherent stability of tablets, especially in various environmental conditions, contributes to longer shelf lives and easier storage and distribution. From a patient perspective, tablets are generally easy to administer, can be formulated for various release profiles (immediate, sustained, delayed), and allow for precise dose accuracy.

The robust position of the Tablets sub-segment is further reinforced by continuous innovation in tablet technologies. For instance, the advancement in the Pharmaceutical Excipients Market has enabled the development of tablets with enhanced bioavailability for poorly soluble drugs, improved taste masking, and novel disintegration properties like orally disintegrating tablets (ODTs). These innovations expand the therapeutic applicability of tablets, making them suitable for pediatric and geriatric populations who might have difficulty swallowing conventional pills. Major pharmaceutical players and contract development and manufacturing organizations (CDMOs) heavily invest in optimizing tablet compression techniques, coating technologies, and material science to meet evolving therapeutic demands. The widespread use of tablets across a spectrum of therapeutic indications, from over-the-counter pain relief to complex treatments for chronic diseases, solidifies its market lead.

While capsules, powders, syrups, and gels also represent significant portions of the Oral Drug Delivery Market, tablets consistently outperform them in terms of overall volume and revenue. The Solid Dosage Forms Market, which encompasses tablets and capsules, generally represents the largest portion of all drug delivery methods due to patient compliance and manufacturing efficiencies. The global shift towards generic drug manufacturing, where tablets often represent the most straightforward and cost-effective pathway for bioequivalence, further bolsters this segment's growth. The continued focus on developing fixed-dose combination tablets, which improve patient adherence by reducing pill burden, is another key driver for sustained dominance. The dominance of tablets is not merely a historical artifact but a reflection of ongoing innovation and a highly optimized manufacturing ecosystem geared towards efficient and effective oral drug delivery.

Key Market Drivers & Constraints in Oral Drug Delivery Market

The Oral Drug Delivery Market's trajectory is primarily shaped by a dynamic interplay of potent drivers and persistent constraints. One of the foremost drivers is the escalating global burden of chronic diseases. For instance, the World Health Organization estimates that non-communicable diseases (NCDs), including cardiovascular diseases, cancer, diabetes, and chronic respiratory diseases, are responsible for 74% of all deaths globally, necessitating long-term, often daily, medication. Oral formulations are preferred for their convenience and ease of self-administration, directly enhancing patient adherence to these protracted treatment regimens. The increasing prevalence of diabetes, affecting over 537 million adults globally in 2021, fuels demand for advanced oral insulin delivery systems and other oral hypoglycemic agents, driving innovation in Controlled Release Drug Delivery Market solutions.

A second significant driver is the strong patient preference for non-invasive drug administration. This preference directly translates into higher patient compliance rates for oral medications, which is a critical factor in treatment efficacy, especially for conditions requiring chronic therapy. The convenience of taking medication at home, without the need for medical supervision or specialized equipment often associated with Parenteral Drug Delivery Market options, significantly contributes to this demand. Furthermore, the cost-effectiveness of oral drug manufacturing, compared to sterile injectable formulations, makes oral drugs more accessible and affordable, particularly in price-sensitive markets.

However, the Oral Drug Delivery Market faces notable constraints, primarily concerning the physicochemical properties of drug molecules and the complex gastrointestinal environment. A major challenge is the poor bioavailability of many new chemical entities (NCEs), with an estimated 70-80% of drug candidates exhibiting low solubility or permeability. This necessitates advanced formulation strategies to enhance absorption, often adding complexity and cost. First-pass metabolism in the liver can significantly reduce the concentration of active drug reaching systemic circulation, posing a barrier for certain therapeutic agents. Regulatory hurdles for novel oral delivery systems, particularly those involving advanced materials or complex release mechanisms, can also prolong development timelines and increase R&D costs. The challenges associated with developing effective oral formulations for large molecule biologics also represent a significant constraint, pushing the boundaries of current drug delivery science.

Competitive Ecosystem of Oral Drug Delivery Market

The Oral Drug Delivery Market is characterized by a diverse competitive landscape comprising pharmaceutical giants, specialized drug delivery companies, and contract development and manufacturing organizations (CDMOs). These entities continually innovate to enhance drug solubility, bioavailability, and patient compliance through advanced oral formulations.

- Catalent: A leading global provider of advanced delivery technologies and development solutions for drugs, biologics, gene therapies, and consumer health products, playing a critical role in oral dose formulation and manufacturing for numerous clients.

- Lonza: A key partner to the pharmaceutical, biotech, and nutrition industries, offering comprehensive services from discovery to commercial manufacturing, with a strong focus on advanced oral dosage forms and bioavailability enhancement technologies.

- Evonik Industries: A prominent specialty chemicals company, providing high-quality excipients and functional polymers crucial for the development of innovative oral drug delivery systems, particularly in controlled and targeted release formulations.

- Colorcon: A world leader in the development and supply of film coatings, excipients, and functional packaging for the pharmaceutical industry, directly contributing to the aesthetic, stability, and release characteristics of oral solid dosage forms.

- Roquette: A global leader in plant-based ingredients, offering a wide range of pharmaceutical excipients derived from starch and polyols, which are vital for tablet binding, disintegration, and solubility enhancement in oral drug products.

- Pfizer: One of the world's largest pharmaceutical companies, with an extensive portfolio of orally administered drugs across various therapeutic areas, and ongoing investments in R&D for new oral formulations.

- Novartis: A global healthcare company with a strong presence in the Oral Drug Delivery Market, developing and manufacturing a broad range of oral medications for chronic diseases and specialized treatments.

- AstraZeneca: A multinational pharmaceutical and biotechnology company focused on the discovery, development, and commercialization of prescription medicines, many of which are delivered orally for conditions like cardiovascular diseases and oncology.

- Merck & Co.: A leading global biopharmaceutical company, known for its significant contributions to developing innovative oral therapies across a wide range of diseases, including diabetes and infectious diseases.

- AbbVie: A research-based global biopharmaceutical company that leverages its expertise to develop and commercialize advanced oral treatments, particularly in immunology, oncology, and neuroscience.

- Johnson & Johnson: A diversified healthcare conglomerate with a significant pharmaceutical segment that develops and markets numerous oral medications, focusing on areas with high unmet medical needs.

- Boehringer Ingelheim: A research-driven pharmaceutical company specializing in innovative therapies, including a substantial portfolio of orally administered drugs for respiratory, cardiometabolic, and oncology indications.

- Teva Pharmaceutical Industries: A global leader in generic medicines and specialty pharmaceuticals, with a vast array of oral drug products and a focus on expanding access to essential medications worldwide.

- Abbott Laboratories: A diversified healthcare company involved in pharmaceuticals, medical devices, and diagnostics, offering a range of oral medications and nutritional products that utilize advanced delivery technologies.

Recent Developments & Milestones in Oral Drug Delivery Market

The Oral Drug Delivery Market is a hotbed of innovation, driven by continuous research into advanced formulations and strategic collaborations. Recent developments highlight a trend towards improving bioavailability, patient compliance, and targeted delivery.

- January 2023: A leading CDMO announced the successful completion of a Phase I clinical trial for a novel oral formulation of a poorly soluble anti-inflammatory drug, utilizing a proprietary amorphous solid dispersion (ASD) technology to enhance absorption.

- March 2023: A major pharmaceutical company entered a strategic partnership with a biotech firm specializing in peptide delivery, aiming to develop orally administered versions of previously injectable peptide-based therapies, signaling a significant step towards expanding the Biopharmaceutical Manufacturing Market into oral routes.

- May 2023: Regulatory authorities in Europe approved a new orally disintegrating tablet (ODT) for pediatric use, addressing challenges in medication administration for children and expanding the market for convenient dosage forms.

- July 2023: Researchers unveiled a breakthrough in gastro-retentive oral drug delivery systems, demonstrating extended drug release for up to 24 hours, promising improved therapeutic outcomes for chronic conditions requiring sustained drug levels.

- September 2023: A technology licensing agreement was signed between a drug delivery specialist and a generic pharmaceutical manufacturer for a proprietary controlled-release technology, enabling the development of next-generation generic oral drugs.

- November 2023: A significant investment was announced for expanding manufacturing capabilities for oral solid dosage forms, including high-potency active pharmaceutical ingredients (APIs), to meet the rising demand in the Oncology Drug Delivery Market.

- February 2024: A new study published demonstrated the efficacy of an oral nanocarrier system for delivering gene therapy agents, opening new avenues for complex therapies through the oral route, which could impact the Drug Compounding Market by offering more sophisticated preparations.

- April 2024: A key industry player launched a new line of taste-masked granules for pediatric medications, specifically designed to improve compliance for oral liquid formulations, further enhancing patient acceptance.

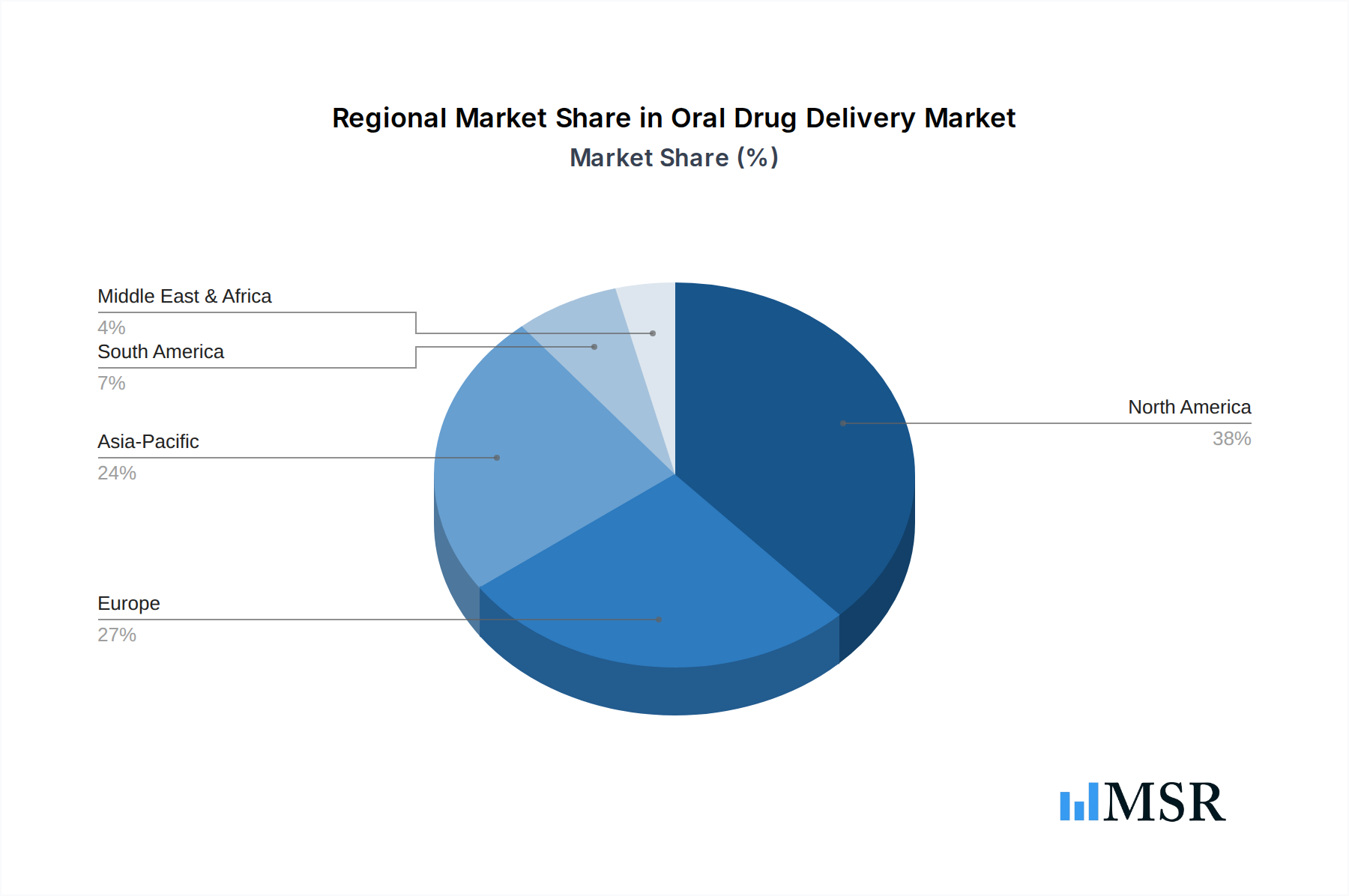

Regional Market Breakdown for Oral Drug Delivery Market

The Oral Drug Delivery Market exhibits distinct regional dynamics driven by varying healthcare infrastructures, disease prevalences, and regulatory landscapes. Globally, North America and Europe represent the most mature markets, while Asia Pacific is emerging as the fastest-growing region.

North America, encompassing the United States, Canada, and Mexico, holds the largest revenue share in the Oral Drug Delivery Market. This dominance is attributable to high healthcare expenditure, significant R&D investments by pharmaceutical companies, the presence of major industry players, and a well-established regulatory framework that supports the introduction of innovative oral formulations. The region also benefits from a high prevalence of chronic diseases and a strong patient preference for convenient, non-invasive treatments, leading to substantial adoption of oral medications. The sophisticated distribution networks including Retail Pharmacies and Hospital Pharmacies, further facilitate market growth.

Europe, including countries like the United Kingdom, Germany, and France, also accounts for a substantial share of the market. Similar to North America, Europe boasts a developed healthcare system, a rapidly aging population, and robust R&D activities focused on drug formulation advancements. Stringent quality standards and a high demand for specialty drugs, often administered orally, further drive this market segment. The region is a hub for pharmaceutical manufacturing and clinical trials, supporting continuous innovation in oral drug delivery technologies. The presence of numerous Specialty Clinics Market segments also contributes to the regional demand.

Asia Pacific, driven by countries such as China, India, and Japan, is projected to be the fastest-growing region in the Oral Drug Delivery Market. This growth is fueled by a massive patient pool, improving healthcare infrastructure, increasing disposable incomes, and rising awareness about modern medication. The region is witnessing a rapid expansion of local pharmaceutical manufacturing capabilities and a growing emphasis on affordable generic oral drugs. Furthermore, the rising prevalence of lifestyle diseases and infectious diseases in densely populated countries like India and China significantly contributes to the demand for oral drug delivery systems. Government initiatives to enhance healthcare access and the expanding network of Online Pharmacies are also key growth catalysts.

The Middle East & Africa (MEA) and South America represent emerging markets with considerable growth potential. In MEA, increasing healthcare investments, a growing pharmaceutical sector, and efforts to diversify economies away from oil are stimulating market expansion. Countries in the GCC (Gulf Cooperation Council) are actively upgrading their healthcare facilities and pharmaceutical production. In South America, particularly Brazil and Argentina, the expansion of healthcare access, coupled with a rising demand for affordable generic drugs, is driving the adoption of oral drug delivery solutions. While these regions currently hold smaller market shares, their substantial unmet medical needs and developing healthcare landscapes position them for accelerated growth in the coming decade.

Oral Drug Delivery Regional Market Share

Pricing Dynamics & Margin Pressure in Oral Drug Delivery Market

The pricing dynamics within the Oral Drug Delivery Market are intricate, influenced by a multitude of factors ranging from R&D costs and manufacturing complexities to regulatory environments and competitive intensity. Average selling prices (ASPs) for oral drugs vary significantly depending on whether they are branded, generic, or specialty formulations utilizing advanced delivery technologies. Branded drugs, especially those incorporating novel excipients or Controlled Release Drug Delivery Market systems, typically command premium prices due to the extensive R&D investments, patent protection, and clinical validation required. Generic oral drugs, by contrast, operate on much thinner margins, with pricing driven primarily by volume and intense competition once patents expire. The Pharmaceutical Excipients Market costs can also impact the final drug price, as specialized excipients needed for complex formulations are often more expensive.

Margin structures across the value chain are under constant pressure. Pharmaceutical companies developing innovative oral drugs face high upfront R&D costs, and clinical trial failures can significantly erode potential margins. Manufacturing costs, particularly for complex oral solid dosage forms that require specialized equipment or controlled environments, also contribute to margin pressure. For generic manufacturers, the 'race to the bottom' in pricing, coupled with increasing raw material costs and stringent quality control requirements, often squeezes profitability. Contract manufacturing organizations (CMOs) operating in the Biopharmaceutical Manufacturing Market and oral drug delivery space face pressure from clients to offer competitive pricing while maintaining high quality and regulatory compliance.

Key cost levers include the cost of active pharmaceutical ingredients (APIs), the price of excipients, labor costs for manufacturing, and regulatory compliance expenses. Commodity cycles, especially those impacting raw materials used in API synthesis or excipient production, can directly affect manufacturing costs and, subsequently, the ASPs. Intense competitive intensity, particularly in mature generic drug markets, forces companies to continually optimize their production processes and supply chains to maintain profitability. Furthermore, the increasing demand for affordability from payers and governments worldwide exerts downward pressure on drug prices, compelling manufacturers to seek efficiencies throughout the entire production lifecycle to sustain margins in the Oral Drug Delivery Market." } ``````json { "reportId": 136497, "keywords": [ "Solid Dosage Forms Market", "Controlled Release Drug Delivery Market", "Pharmaceutical Excipients Market", "Oncology Drug Delivery Market", "Biopharmaceutical Manufacturing Market", "Parenteral Drug Delivery Market", "Specialty Clinics Market", "Drug Compounding Market" ], "reportContent": "## Key Insights into the Oral Drug Delivery Market

The global Oral Drug Delivery Market, valued at $133.94 billion in 2025, is poised for robust expansion, projected to reach approximately $204.1 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 4.8% over the forecast period. This significant growth trajectory is primarily propelled by a confluence of factors, including the escalating prevalence of chronic diseases globally, increasing patient preference for non-invasive drug administration routes, and continuous advancements in drug formulation technologies. Oral drug delivery systems offer unparalleled convenience, cost-effectiveness, and enhanced patient compliance compared to parenteral alternatives, making them the preferred choice for a vast array of therapeutic indications.

Key demand drivers for the Oral Drug Delivery Market encompass the rising geriatric population, which inherently necessitates long-term medication regimens, and the burgeoning pipeline of small molecule drugs. Macro tailwinds such as increasing healthcare expenditure in emerging economies, government initiatives promoting affordable healthcare, and substantial research and development investments by pharmaceutical companies further bolster market expansion. Innovations in excipient technologies, enabling improved drug solubility, bioavailability, and targeted release, are pivotal. The shift towards personalized medicine and the growing demand for orally administered biologics via advanced encapsulation techniques are also shaping the market's future. The increasing prevalence of cardiovascular diseases, diabetes, and infectious diseases, for which oral medications are often the first line of treatment, underpins a consistent and growing demand across regional markets.

The forward-looking outlook indicates a sustained focus on developing novel oral formulations that overcome challenges such as poor aqueous solubility, gastric degradation, and low permeability. The development of advanced systems like sustained-release tablets, orally disintegrating tablets (ODTs), and gastro-retentive systems is expected to unlock new therapeutic possibilities and expand the application scope of oral delivery. Strategic collaborations between drug developers and contract manufacturing organizations (CMOs) are becoming increasingly common to optimize manufacturing processes and accelerate market entry for new oral drug products. Furthermore, the expansion of healthcare infrastructure and accessibility in developing regions presents substantial untapped opportunities, reinforcing the Oral Drug Delivery Market's position as a cornerstone of modern pharmacotherapy.

Dominant Dosage Form Segment in Oral Drug Delivery Market

Within the broader Oral Drug Delivery Market, the Tablets sub-segment, under the Dosage Form category, currently holds the most substantial revenue share and is anticipated to maintain its dominance throughout the forecast period. This leadership is attributed to several intrinsic advantages that tablets offer, making them the most widely accepted and utilized solid oral dosage form. These advantages include superior manufacturing simplicity and scalability, which translates into lower production costs compared to more complex formulations. The inherent stability of tablets, especially in various environmental conditions, contributes to longer shelf lives and easier storage and distribution. From a patient perspective, tablets are generally easy to administer, can be formulated for various release profiles (immediate, sustained, delayed), and allow for precise dose accuracy.

The robust position of the Tablets sub-segment is further reinforced by continuous innovation in tablet technologies. For instance, the advancement in the Pharmaceutical Excipients Market has enabled the development of tablets with enhanced bioavailability for poorly soluble drugs, improved taste masking, and novel disintegration properties like orally disintegrating tablets (ODTs). These innovations expand the therapeutic applicability of tablets, making them suitable for pediatric and geriatric populations who might have difficulty swallowing conventional pills. Major pharmaceutical players and contract development and manufacturing organizations (CDMOs) heavily invest in optimizing tablet compression techniques, coating technologies, and material science to meet evolving therapeutic demands. The widespread use of tablets across a spectrum of therapeutic indications, from over-the-counter pain relief to complex treatments for chronic diseases, solidifies its market lead.

While capsules, powders, syrups, and gels also represent significant portions of the Oral Drug Delivery Market, tablets consistently outperform them in terms of overall volume and revenue. The Solid Dosage Forms Market, which encompasses tablets and capsules, generally represents the largest portion of all drug delivery methods due to patient compliance and manufacturing efficiencies. The global shift towards generic drug manufacturing, where tablets often represent the most straightforward and cost-effective pathway for bioequivalence, further bolsters this segment's growth. The continued focus on developing fixed-dose combination tablets, which improve patient adherence by reducing pill burden, is another key driver for sustained dominance. The dominance of tablets is not merely a historical artifact but a reflection of ongoing innovation and a highly optimized manufacturing ecosystem geared towards efficient and effective oral drug delivery.

Key Market Drivers & Constraints in Oral Drug Delivery Market

The Oral Drug Delivery Market's trajectory is primarily shaped by a dynamic interplay of potent drivers and persistent constraints. One of the foremost drivers is the escalating global burden of chronic diseases. For instance, the World Health Organization estimates that non-communicable diseases (NCDs), including cardiovascular diseases, cancer, diabetes, and chronic respiratory diseases, are responsible for 74% of all deaths globally, necessitating long-term, often daily, medication. Oral formulations are preferred for their convenience and ease of self-administration, directly enhancing patient adherence to these protracted treatment regimens. The increasing prevalence of diabetes, affecting over 537 million adults globally in 2021, fuels demand for advanced oral insulin delivery systems and other oral hypoglycemic agents, driving innovation in Controlled Release Drug Delivery Market solutions.

A second significant driver is the strong patient preference for non-invasive drug administration. This preference directly translates into higher patient compliance rates for oral medications, which is a critical factor in treatment efficacy, especially for conditions requiring chronic therapy. The convenience of taking medication at home, without the need for medical supervision or specialized equipment often associated with Parenteral Drug Delivery Market options, significantly contributes to this demand. Furthermore, the cost-effectiveness of oral drug manufacturing, compared to sterile injectable formulations, makes oral drugs more accessible and affordable, particularly in price-sensitive markets.

However, the Oral Drug Delivery Market faces notable constraints, primarily concerning the physicochemical properties of drug molecules and the complex gastrointestinal environment. A major challenge is the poor bioavailability of many new chemical entities (NCEs), with an estimated 70-80% of drug candidates exhibiting low solubility or permeability. This necessitates advanced formulation strategies to enhance absorption, often adding complexity and cost. First-pass metabolism in the liver can significantly reduce the concentration of active drug reaching systemic circulation, posing a barrier for certain therapeutic agents. Regulatory hurdles for novel oral delivery systems, particularly those involving advanced materials or complex release mechanisms, can also prolong development timelines and increase R&D costs. The challenges associated with developing effective oral formulations for large molecule biologics also represent a significant constraint, pushing the boundaries of current drug delivery science.

Competitive Ecosystem of Oral Drug Delivery Market

The Oral Drug Delivery Market is characterized by a diverse competitive landscape comprising pharmaceutical giants, specialized drug delivery companies, and contract development and manufacturing organizations (CDMOs). These entities continually innovate to enhance drug solubility, bioavailability, and patient compliance through advanced oral formulations.

- Catalent: A leading global provider of advanced delivery technologies and development solutions for drugs, biologics, gene therapies, and consumer health products, playing a critical role in oral dose formulation and manufacturing for numerous clients.

- Lonza: A key partner to the pharmaceutical, biotech, and nutrition industries, offering comprehensive services from discovery to commercial manufacturing, with a strong focus on advanced oral dosage forms and bioavailability enhancement technologies.

- Evonik Industries: A prominent specialty chemicals company, providing high-quality excipients and functional polymers crucial for the development of innovative oral drug delivery systems, particularly in controlled and targeted release formulations.

- Colorcon: A world leader in the development and supply of film coatings, excipients, and functional packaging for the pharmaceutical industry, directly contributing to the aesthetic, stability, and release characteristics of oral solid dosage forms.

- Roquette: A global leader in plant-based ingredients, offering a wide range of pharmaceutical excipients derived from starch and polyols, which are vital for tablet binding, disintegration, and solubility enhancement in oral drug products.

- Pfizer: One of the world's largest pharmaceutical companies, with an extensive portfolio of orally administered drugs across various therapeutic areas, and ongoing investments in R&D for new oral formulations.

- Novartis: A global healthcare company with a strong presence in the Oral Drug Delivery Market, developing and manufacturing a broad range of oral medications for chronic diseases and specialized treatments.

- AstraZeneca: A multinational pharmaceutical and biotechnology company focused on the discovery, development, and commercialization of prescription medicines, many of which are delivered orally for conditions like cardiovascular diseases and oncology.

- Merck & Co.: A leading global biopharmaceutical company, known for its significant contributions to developing innovative oral therapies across a wide range of diseases, including diabetes and infectious diseases.

- AbbVie: A research-based global biopharmaceutical company that leverages its expertise to develop and commercialize advanced oral treatments, particularly in immunology, oncology, and neuroscience.

- Johnson & Johnson: A diversified healthcare conglomerate with a significant pharmaceutical segment that develops and markets numerous oral medications, focusing on areas with high unmet medical needs.

- Boehringer Ingelheim: A research-driven pharmaceutical company specializing in innovative therapies, including a substantial portfolio of orally administered drugs for respiratory, cardiometabolic, and oncology indications.

- Teva Pharmaceutical Industries: A global leader in generic medicines and specialty pharmaceuticals, with a vast array of oral drug products and a focus on expanding access to essential medications worldwide.

- Abbott Laboratories: A diversified healthcare company involved in pharmaceuticals, medical devices, and diagnostics, offering a range of oral medications and nutritional products that utilize advanced delivery technologies.

Recent Developments & Milestones in Oral Drug Delivery Market

The Oral Drug Delivery Market is a hotbed of innovation, driven by continuous research into advanced formulations and strategic collaborations. Recent developments highlight a trend towards improving bioavailability, patient compliance, and targeted delivery.

- January 2023: A leading CDMO announced the successful completion of a Phase I clinical trial for a novel oral formulation of a poorly soluble anti-inflammatory drug, utilizing a proprietary amorphous solid dispersion (ASD) technology to enhance absorption.

- March 2023: A major pharmaceutical company entered a strategic partnership with a biotech firm specializing in peptide delivery, aiming to develop orally administered versions of previously injectable peptide-based therapies, signaling a significant step towards expanding the Biopharmaceutical Manufacturing Market into oral routes.

- May 2023: Regulatory authorities in Europe approved a new orally disintegrating tablet (ODT) for pediatric use, addressing challenges in medication administration for children and expanding the market for convenient dosage forms.

- July 2023: Researchers unveiled a breakthrough in gastro-retentive oral drug delivery systems, demonstrating extended drug release for up to 24 hours, promising improved therapeutic outcomes for chronic conditions requiring sustained drug levels.

- September 2023: A technology licensing agreement was signed between a drug delivery specialist and a generic pharmaceutical manufacturer for a proprietary controlled-release technology, enabling the development of next-generation generic oral drugs.

- November 2023: A significant investment was announced for expanding manufacturing capabilities for oral solid dosage forms, including high-potency active pharmaceutical ingredients (APIs), to meet the rising demand in the Oncology Drug Delivery Market.

- February 2024: A new study published demonstrated the efficacy of an oral nanocarrier system for delivering gene therapy agents, opening new avenues for complex therapies through the oral route, which could impact the Drug Compounding Market by offering more sophisticated preparations.

- April 2024: A key industry player launched a new line of taste-masked granules for pediatric medications, specifically designed to improve compliance for oral liquid formulations, further enhancing patient acceptance.

Regional Market Breakdown for Oral Drug Delivery Market

The Oral Drug Delivery Market exhibits distinct regional dynamics driven by varying healthcare infrastructures, disease prevalences, and regulatory landscapes. Globally, North America and Europe represent the most mature markets, while Asia Pacific is emerging as the fastest-growing region.

North America, encompassing the United States, Canada, and Mexico, holds the largest revenue share in the Oral Drug Delivery Market. This dominance is attributable to high healthcare expenditure, significant R&D investments by pharmaceutical companies, the presence of major industry players, and a well-established regulatory framework that supports the introduction of innovative oral formulations. The region also benefits from a high prevalence of chronic diseases and a strong patient preference for convenient, non-invasive treatments, leading to substantial adoption of oral medications. The sophisticated distribution networks including Retail Pharmacies and Hospital Pharmacies, further facilitate market growth.

Europe, including countries like the United Kingdom, Germany, and France, also accounts for a substantial share of the market. Similar to North America, Europe boasts a developed healthcare system, a rapidly aging population, and robust R&D activities focused on drug formulation advancements. Stringent quality standards and a high demand for specialty drugs, often administered orally, further drive this market segment. The region is a hub for pharmaceutical manufacturing and clinical trials, supporting continuous innovation in oral drug delivery technologies. The presence of numerous Specialty Clinics Market segments also contributes to the regional demand.

Asia Pacific, driven by countries such as China, India, and Japan, is projected to be the fastest-growing region in the Oral Drug Delivery Market. This growth is fueled by a massive patient pool, improving healthcare infrastructure, increasing disposable incomes, and rising awareness about modern medication. The region is witnessing a rapid expansion of local pharmaceutical manufacturing capabilities and a growing emphasis on affordable generic oral drugs. Furthermore, the rising prevalence of lifestyle diseases and infectious diseases in densely populated countries like India and China significantly contributes to the demand for oral drug delivery systems. Government initiatives to enhance healthcare access and the expanding network of Online Pharmacies are also key growth catalysts.

The Middle East & Africa (MEA) and South America represent emerging markets with considerable growth potential. In MEA, increasing healthcare investments, a growing pharmaceutical sector, and efforts to diversify economies away from oil are stimulating market expansion. Countries in the GCC (Gulf Cooperation Council) are actively upgrading their healthcare facilities and pharmaceutical production. In South America, particularly Brazil and Argentina, the expansion of healthcare access, coupled with a rising demand for affordable generic drugs, is driving the adoption of oral drug delivery solutions. While these regions currently hold smaller market shares, their substantial unmet medical needs and developing healthcare landscapes position them for accelerated growth in the coming decade.

Oral Drug Delivery Regional Market Share

Pricing Dynamics & Margin Pressure in Oral Drug Delivery Market

The pricing dynamics within the Oral Drug Delivery Market are intricate, influenced by a multitude of factors ranging from R&D costs and manufacturing complexities to regulatory environments and competitive intensity. Average selling prices (ASPs) for oral drugs vary significantly depending on whether they are branded, generic, or specialty formulations utilizing advanced delivery technologies. Branded drugs, especially those incorporating novel excipients or Controlled Release Drug Delivery Market systems, typically command premium prices due to the extensive R&D investments, patent protection, and clinical validation required. Generic oral drugs, by contrast, operate on much thinner margins, with pricing driven primarily by volume and intense competition once patents expire. The Pharmaceutical Excipients Market costs can also impact the final drug price, as specialized excipients needed for complex formulations are often more expensive.

Margin structures across the value chain are under constant pressure. Pharmaceutical companies developing innovative oral drugs face high upfront R&D costs, and clinical trial failures can significantly erode potential margins. Manufacturing costs, particularly for complex oral solid dosage forms that require specialized equipment or controlled environments, also contribute to margin pressure. For generic manufacturers, the 'race to the bottom' in pricing, coupled with increasing raw material costs and stringent quality control requirements, often squeezes profitability. Contract manufacturing organizations (CMOs) operating in the Biopharmaceutical Manufacturing Market and oral drug delivery space face pressure from clients to offer competitive pricing while maintaining high quality and regulatory compliance.

Key cost levers include the cost of active pharmaceutical ingredients (APIs), the price of excipients, labor costs for manufacturing, and regulatory compliance expenses. Commodity cycles, especially those impacting raw materials used in API synthesis or excipient production, can directly affect manufacturing costs and, subsequently, the ASPs. Intense competitive intensity, particularly in mature generic drug markets, forces companies to continually optimize their production processes and supply chains to maintain profitability. Furthermore, the increasing demand for affordability from payers and governments worldwide exerts downward pressure on drug prices, compelling manufacturers to seek efficiencies throughout the entire production lifecycle to sustain margins in the Oral Drug Delivery Market.

Export, Trade Flow & Tariff Impact on Oral Drug Delivery Market

Global trade flows for products within the Oral Drug Delivery Market are substantial, driven by the internationalization of pharmaceutical manufacturing and distribution. Major trade corridors often connect key API and excipient manufacturing hubs in Asia (e.g., China, India) with drug formulation and packaging centers in North America and Europe. Leading exporting nations for finished oral pharmaceutical products include Germany, Switzerland, Ireland, the United States, and India, leveraging advanced manufacturing capabilities and competitive production costs respectively. Conversely, leading importing nations are typically those with large patient populations, significant healthcare spending, and sometimes limited domestic manufacturing capacity, such as the United States, Japan, and various European countries.

Tariff and non-tariff barriers play a crucial role in shaping these trade dynamics. While tariffs on finished pharmaceutical products are generally low or non-existent in many regions due to their essential nature, tariffs on raw materials and intermediate goods can impact the final cost of oral drugs. Non-tariff barriers, such as complex regulatory approval processes, variations in pharmacopeial standards, and intellectual property protection laws, often pose more significant challenges to cross-border trade than direct tariffs. For instance, obtaining market authorization from agencies like the FDA (U.S.) or EMA (Europe) requires extensive documentation and adherence to Good Manufacturing Practices (GMP), which can be resource-intensive for exporters.

Recent trade policy impacts, such as the U.S.-China trade tensions, have led to some shifts in supply chain strategies within the Oral Drug Delivery Market. Companies have explored diversifying their API and excipient sourcing to mitigate risks associated with tariffs or potential supply disruptions, contributing to the growth of alternative manufacturing hubs. The COVID-19 pandemic also highlighted vulnerabilities in global supply chains, prompting many nations to consider reshoring or nearshoring pharmaceutical production to ensure essential drug availability. While direct quantification of tariff impacts on cross-border volume is complex due to various mitigating strategies, policy changes can lead to increased operational costs for manufacturers, potentially influencing drug pricing and market accessibility in specific regions. The ongoing efforts for harmonization of regulatory standards across international bodies aim to reduce non-tariff barriers and streamline trade flows for oral drug products, thereby fostering a more efficient global Oral Drug Delivery Market.

Oral Drug Delivery Segmentation

-

1. Dosage Form

- 1.1. Tablets

- 1.2. Capsules

- 1.3. Powders

- 1.4. Syrups

- 1.5. Gels

-

2. Release Mechanism

- 2.1. Immediate Release

- 2.2. Controlled/Sustained Release

- 2.3. Delayed Release

- 2.4. Targeted Release

-

3. Therapeutic Indication

- 3.1. Cardiovascular Diseases

- 3.2. Oncology

- 3.3. Infectious Diseases

- 3.4. Diabetes

- 3.5. Gastrointestinal Disorders

- 3.6. Central Nervous System (CNS)

- 3.7. Others

-

4. Distribution Channel

- 4.1. Hospital Pharmacies

- 4.2. Retail Pharmacies

- 4.3. Online Pharmacies

-

5. End User

- 5.1. Hospitals

- 5.2. Specialty Clinics

- 5.3. Ambulatory Care Centers

- 5.4. Homecare

- 5.5. Others

Oral Drug Delivery Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Oral Drug Delivery Regional Market Share

Geographic Coverage of Oral Drug Delivery

Oral Drug Delivery REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Dosage Form

- 5.1.1. Tablets

- 5.1.2. Capsules

- 5.1.3. Powders

- 5.1.4. Syrups

- 5.1.5. Gels

- 5.2. Market Analysis, Insights and Forecast - by Release Mechanism

- 5.2.1. Immediate Release

- 5.2.2. Controlled/Sustained Release

- 5.2.3. Delayed Release

- 5.2.4. Targeted Release

- 5.3. Market Analysis, Insights and Forecast - by Therapeutic Indication

- 5.3.1. Cardiovascular Diseases

- 5.3.2. Oncology

- 5.3.3. Infectious Diseases

- 5.3.4. Diabetes

- 5.3.5. Gastrointestinal Disorders

- 5.3.6. Central Nervous System (CNS)

- 5.3.7. Others

- 5.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.4.1. Hospital Pharmacies

- 5.4.2. Retail Pharmacies

- 5.4.3. Online Pharmacies

- 5.5. Market Analysis, Insights and Forecast - by End User

- 5.5.1. Hospitals

- 5.5.2. Specialty Clinics

- 5.5.3. Ambulatory Care Centers

- 5.5.4. Homecare

- 5.5.5. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. South America

- 5.6.3. Europe

- 5.6.4. Middle East & Africa

- 5.6.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Dosage Form

- 6. Global Oral Drug Delivery Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Dosage Form

- 6.1.1. Tablets

- 6.1.2. Capsules

- 6.1.3. Powders

- 6.1.4. Syrups

- 6.1.5. Gels

- 6.2. Market Analysis, Insights and Forecast - by Release Mechanism

- 6.2.1. Immediate Release

- 6.2.2. Controlled/Sustained Release

- 6.2.3. Delayed Release

- 6.2.4. Targeted Release

- 6.3. Market Analysis, Insights and Forecast - by Therapeutic Indication

- 6.3.1. Cardiovascular Diseases

- 6.3.2. Oncology

- 6.3.3. Infectious Diseases

- 6.3.4. Diabetes

- 6.3.5. Gastrointestinal Disorders

- 6.3.6. Central Nervous System (CNS)

- 6.3.7. Others

- 6.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.4.1. Hospital Pharmacies

- 6.4.2. Retail Pharmacies

- 6.4.3. Online Pharmacies

- 6.5. Market Analysis, Insights and Forecast - by End User

- 6.5.1. Hospitals

- 6.5.2. Specialty Clinics

- 6.5.3. Ambulatory Care Centers

- 6.5.4. Homecare

- 6.5.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Dosage Form

- 7. North America Oral Drug Delivery Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Dosage Form

- 7.1.1. Tablets

- 7.1.2. Capsules

- 7.1.3. Powders

- 7.1.4. Syrups

- 7.1.5. Gels

- 7.2. Market Analysis, Insights and Forecast - by Release Mechanism

- 7.2.1. Immediate Release

- 7.2.2. Controlled/Sustained Release

- 7.2.3. Delayed Release

- 7.2.4. Targeted Release

- 7.3. Market Analysis, Insights and Forecast - by Therapeutic Indication

- 7.3.1. Cardiovascular Diseases

- 7.3.2. Oncology

- 7.3.3. Infectious Diseases

- 7.3.4. Diabetes

- 7.3.5. Gastrointestinal Disorders

- 7.3.6. Central Nervous System (CNS)

- 7.3.7. Others

- 7.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.4.1. Hospital Pharmacies

- 7.4.2. Retail Pharmacies

- 7.4.3. Online Pharmacies

- 7.5. Market Analysis, Insights and Forecast - by End User

- 7.5.1. Hospitals

- 7.5.2. Specialty Clinics

- 7.5.3. Ambulatory Care Centers

- 7.5.4. Homecare

- 7.5.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Dosage Form

- 8. South America Oral Drug Delivery Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Dosage Form

- 8.1.1. Tablets

- 8.1.2. Capsules

- 8.1.3. Powders

- 8.1.4. Syrups

- 8.1.5. Gels

- 8.2. Market Analysis, Insights and Forecast - by Release Mechanism

- 8.2.1. Immediate Release

- 8.2.2. Controlled/Sustained Release

- 8.2.3. Delayed Release

- 8.2.4. Targeted Release

- 8.3. Market Analysis, Insights and Forecast - by Therapeutic Indication

- 8.3.1. Cardiovascular Diseases

- 8.3.2. Oncology

- 8.3.3. Infectious Diseases

- 8.3.4. Diabetes

- 8.3.5. Gastrointestinal Disorders

- 8.3.6. Central Nervous System (CNS)

- 8.3.7. Others

- 8.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.4.1. Hospital Pharmacies

- 8.4.2. Retail Pharmacies

- 8.4.3. Online Pharmacies

- 8.5. Market Analysis, Insights and Forecast - by End User

- 8.5.1. Hospitals

- 8.5.2. Specialty Clinics

- 8.5.3. Ambulatory Care Centers

- 8.5.4. Homecare

- 8.5.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Dosage Form

- 9. Europe Oral Drug Delivery Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Dosage Form

- 9.1.1. Tablets

- 9.1.2. Capsules

- 9.1.3. Powders

- 9.1.4. Syrups

- 9.1.5. Gels

- 9.2. Market Analysis, Insights and Forecast - by Release Mechanism

- 9.2.1. Immediate Release

- 9.2.2. Controlled/Sustained Release

- 9.2.3. Delayed Release

- 9.2.4. Targeted Release

- 9.3. Market Analysis, Insights and Forecast - by Therapeutic Indication

- 9.3.1. Cardiovascular Diseases

- 9.3.2. Oncology

- 9.3.3. Infectious Diseases

- 9.3.4. Diabetes

- 9.3.5. Gastrointestinal Disorders

- 9.3.6. Central Nervous System (CNS)

- 9.3.7. Others

- 9.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.4.1. Hospital Pharmacies

- 9.4.2. Retail Pharmacies

- 9.4.3. Online Pharmacies

- 9.5. Market Analysis, Insights and Forecast - by End User

- 9.5.1. Hospitals

- 9.5.2. Specialty Clinics

- 9.5.3. Ambulatory Care Centers

- 9.5.4. Homecare

- 9.5.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Dosage Form

- 10. Middle East & Africa Oral Drug Delivery Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Dosage Form

- 10.1.1. Tablets

- 10.1.2. Capsules

- 10.1.3. Powders

- 10.1.4. Syrups

- 10.1.5. Gels

- 10.2. Market Analysis, Insights and Forecast - by Release Mechanism

- 10.2.1. Immediate Release

- 10.2.2. Controlled/Sustained Release

- 10.2.3. Delayed Release

- 10.2.4. Targeted Release

- 10.3. Market Analysis, Insights and Forecast - by Therapeutic Indication

- 10.3.1. Cardiovascular Diseases

- 10.3.2. Oncology

- 10.3.3. Infectious Diseases

- 10.3.4. Diabetes

- 10.3.5. Gastrointestinal Disorders

- 10.3.6. Central Nervous System (CNS)

- 10.3.7. Others

- 10.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.4.1. Hospital Pharmacies

- 10.4.2. Retail Pharmacies

- 10.4.3. Online Pharmacies

- 10.5. Market Analysis, Insights and Forecast - by End User

- 10.5.1. Hospitals

- 10.5.2. Specialty Clinics

- 10.5.3. Ambulatory Care Centers

- 10.5.4. Homecare

- 10.5.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Dosage Form

- 11. Asia Pacific Oral Drug Delivery Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Dosage Form

- 11.1.1. Tablets

- 11.1.2. Capsules

- 11.1.3. Powders

- 11.1.4. Syrups

- 11.1.5. Gels

- 11.2. Market Analysis, Insights and Forecast - by Release Mechanism

- 11.2.1. Immediate Release

- 11.2.2. Controlled/Sustained Release

- 11.2.3. Delayed Release

- 11.2.4. Targeted Release

- 11.3. Market Analysis, Insights and Forecast - by Therapeutic Indication

- 11.3.1. Cardiovascular Diseases

- 11.3.2. Oncology

- 11.3.3. Infectious Diseases

- 11.3.4. Diabetes

- 11.3.5. Gastrointestinal Disorders

- 11.3.6. Central Nervous System (CNS)

- 11.3.7. Others

- 11.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.4.1. Hospital Pharmacies

- 11.4.2. Retail Pharmacies

- 11.4.3. Online Pharmacies

- 11.5. Market Analysis, Insights and Forecast - by End User

- 11.5.1. Hospitals

- 11.5.2. Specialty Clinics

- 11.5.3. Ambulatory Care Centers

- 11.5.4. Homecare

- 11.5.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Dosage Form

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Catalent

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Lonza

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Evonik Industries

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Colorcon

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Roquette

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pfizer

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Novartis

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 AstraZeneca

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Merck & Co.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 AbbVie

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Johnson & Johnson

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Boehringer Ingelheim

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Teva Pharmaceutical Industries

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Abbott Laboratories

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Others

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Catalent

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Oral Drug Delivery Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Oral Drug Delivery Revenue (billion), by Dosage Form 2025 & 2033

- Figure 3: North America Oral Drug Delivery Revenue Share (%), by Dosage Form 2025 & 2033

- Figure 4: North America Oral Drug Delivery Revenue (billion), by Release Mechanism 2025 & 2033

- Figure 5: North America Oral Drug Delivery Revenue Share (%), by Release Mechanism 2025 & 2033

- Figure 6: North America Oral Drug Delivery Revenue (billion), by Therapeutic Indication 2025 & 2033

- Figure 7: North America Oral Drug Delivery Revenue Share (%), by Therapeutic Indication 2025 & 2033

- Figure 8: North America Oral Drug Delivery Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 9: North America Oral Drug Delivery Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Oral Drug Delivery Revenue (billion), by End User 2025 & 2033

- Figure 11: North America Oral Drug Delivery Revenue Share (%), by End User 2025 & 2033

- Figure 12: North America Oral Drug Delivery Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Oral Drug Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Oral Drug Delivery Revenue (billion), by Dosage Form 2025 & 2033

- Figure 15: South America Oral Drug Delivery Revenue Share (%), by Dosage Form 2025 & 2033

- Figure 16: South America Oral Drug Delivery Revenue (billion), by Release Mechanism 2025 & 2033

- Figure 17: South America Oral Drug Delivery Revenue Share (%), by Release Mechanism 2025 & 2033

- Figure 18: South America Oral Drug Delivery Revenue (billion), by Therapeutic Indication 2025 & 2033

- Figure 19: South America Oral Drug Delivery Revenue Share (%), by Therapeutic Indication 2025 & 2033

- Figure 20: South America Oral Drug Delivery Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 21: South America Oral Drug Delivery Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: South America Oral Drug Delivery Revenue (billion), by End User 2025 & 2033

- Figure 23: South America Oral Drug Delivery Revenue Share (%), by End User 2025 & 2033

- Figure 24: South America Oral Drug Delivery Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Oral Drug Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Oral Drug Delivery Revenue (billion), by Dosage Form 2025 & 2033

- Figure 27: Europe Oral Drug Delivery Revenue Share (%), by Dosage Form 2025 & 2033

- Figure 28: Europe Oral Drug Delivery Revenue (billion), by Release Mechanism 2025 & 2033

- Figure 29: Europe Oral Drug Delivery Revenue Share (%), by Release Mechanism 2025 & 2033

- Figure 30: Europe Oral Drug Delivery Revenue (billion), by Therapeutic Indication 2025 & 2033

- Figure 31: Europe Oral Drug Delivery Revenue Share (%), by Therapeutic Indication 2025 & 2033

- Figure 32: Europe Oral Drug Delivery Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 33: Europe Oral Drug Delivery Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Europe Oral Drug Delivery Revenue (billion), by End User 2025 & 2033

- Figure 35: Europe Oral Drug Delivery Revenue Share (%), by End User 2025 & 2033

- Figure 36: Europe Oral Drug Delivery Revenue (billion), by Country 2025 & 2033

- Figure 37: Europe Oral Drug Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 38: Middle East & Africa Oral Drug Delivery Revenue (billion), by Dosage Form 2025 & 2033

- Figure 39: Middle East & Africa Oral Drug Delivery Revenue Share (%), by Dosage Form 2025 & 2033

- Figure 40: Middle East & Africa Oral Drug Delivery Revenue (billion), by Release Mechanism 2025 & 2033

- Figure 41: Middle East & Africa Oral Drug Delivery Revenue Share (%), by Release Mechanism 2025 & 2033

- Figure 42: Middle East & Africa Oral Drug Delivery Revenue (billion), by Therapeutic Indication 2025 & 2033

- Figure 43: Middle East & Africa Oral Drug Delivery Revenue Share (%), by Therapeutic Indication 2025 & 2033

- Figure 44: Middle East & Africa Oral Drug Delivery Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 45: Middle East & Africa Oral Drug Delivery Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Middle East & Africa Oral Drug Delivery Revenue (billion), by End User 2025 & 2033

- Figure 47: Middle East & Africa Oral Drug Delivery Revenue Share (%), by End User 2025 & 2033

- Figure 48: Middle East & Africa Oral Drug Delivery Revenue (billion), by Country 2025 & 2033

- Figure 49: Middle East & Africa Oral Drug Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Oral Drug Delivery Revenue (billion), by Dosage Form 2025 & 2033

- Figure 51: Asia Pacific Oral Drug Delivery Revenue Share (%), by Dosage Form 2025 & 2033

- Figure 52: Asia Pacific Oral Drug Delivery Revenue (billion), by Release Mechanism 2025 & 2033

- Figure 53: Asia Pacific Oral Drug Delivery Revenue Share (%), by Release Mechanism 2025 & 2033

- Figure 54: Asia Pacific Oral Drug Delivery Revenue (billion), by Therapeutic Indication 2025 & 2033

- Figure 55: Asia Pacific Oral Drug Delivery Revenue Share (%), by Therapeutic Indication 2025 & 2033

- Figure 56: Asia Pacific Oral Drug Delivery Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 57: Asia Pacific Oral Drug Delivery Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Asia Pacific Oral Drug Delivery Revenue (billion), by End User 2025 & 2033

- Figure 59: Asia Pacific Oral Drug Delivery Revenue Share (%), by End User 2025 & 2033

- Figure 60: Asia Pacific Oral Drug Delivery Revenue (billion), by Country 2025 & 2033

- Figure 61: Asia Pacific Oral Drug Delivery Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Oral Drug Delivery Revenue billion Forecast, by Dosage Form 2020 & 2033

- Table 2: Global Oral Drug Delivery Revenue billion Forecast, by Release Mechanism 2020 & 2033

- Table 3: Global Oral Drug Delivery Revenue billion Forecast, by Therapeutic Indication 2020 & 2033

- Table 4: Global Oral Drug Delivery Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Oral Drug Delivery Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Oral Drug Delivery Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Global Oral Drug Delivery Revenue billion Forecast, by Dosage Form 2020 & 2033

- Table 8: Global Oral Drug Delivery Revenue billion Forecast, by Release Mechanism 2020 & 2033

- Table 9: Global Oral Drug Delivery Revenue billion Forecast, by Therapeutic Indication 2020 & 2033

- Table 10: Global Oral Drug Delivery Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global Oral Drug Delivery Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Oral Drug Delivery Revenue billion Forecast, by Country 2020 & 2033

- Table 13: United States Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Canada Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Mexico Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Oral Drug Delivery Revenue billion Forecast, by Dosage Form 2020 & 2033

- Table 17: Global Oral Drug Delivery Revenue billion Forecast, by Release Mechanism 2020 & 2033

- Table 18: Global Oral Drug Delivery Revenue billion Forecast, by Therapeutic Indication 2020 & 2033

- Table 19: Global Oral Drug Delivery Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 20: Global Oral Drug Delivery Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Oral Drug Delivery Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Brazil Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Argentina Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Rest of South America Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Global Oral Drug Delivery Revenue billion Forecast, by Dosage Form 2020 & 2033

- Table 26: Global Oral Drug Delivery Revenue billion Forecast, by Release Mechanism 2020 & 2033

- Table 27: Global Oral Drug Delivery Revenue billion Forecast, by Therapeutic Indication 2020 & 2033

- Table 28: Global Oral Drug Delivery Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 29: Global Oral Drug Delivery Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Oral Drug Delivery Revenue billion Forecast, by Country 2020 & 2033

- Table 31: United Kingdom Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: France Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Italy Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Spain Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Russia Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Benelux Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Nordics Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Global Oral Drug Delivery Revenue billion Forecast, by Dosage Form 2020 & 2033

- Table 41: Global Oral Drug Delivery Revenue billion Forecast, by Release Mechanism 2020 & 2033

- Table 42: Global Oral Drug Delivery Revenue billion Forecast, by Therapeutic Indication 2020 & 2033

- Table 43: Global Oral Drug Delivery Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 44: Global Oral Drug Delivery Revenue billion Forecast, by End User 2020 & 2033

- Table 45: Global Oral Drug Delivery Revenue billion Forecast, by Country 2020 & 2033

- Table 46: Turkey Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Israel Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: GCC Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 49: North Africa Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: South Africa Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: Rest of Middle East & Africa Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Global Oral Drug Delivery Revenue billion Forecast, by Dosage Form 2020 & 2033

- Table 53: Global Oral Drug Delivery Revenue billion Forecast, by Release Mechanism 2020 & 2033

- Table 54: Global Oral Drug Delivery Revenue billion Forecast, by Therapeutic Indication 2020 & 2033

- Table 55: Global Oral Drug Delivery Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 56: Global Oral Drug Delivery Revenue billion Forecast, by End User 2020 & 2033

- Table 57: Global Oral Drug Delivery Revenue billion Forecast, by Country 2020 & 2033

- Table 58: China Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 59: India Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Japan Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 61: South Korea Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: ASEAN Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 63: Oceania Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Rest of Asia Pacific Oral Drug Delivery Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oral Drug Delivery?

The projected CAGR is approximately 4.8%.

2. Which companies are prominent players in the Oral Drug Delivery?

Key companies in the market include Catalent, Lonza, Evonik Industries, Colorcon, Roquette, Pfizer, Novartis, AstraZeneca, Merck & Co., AbbVie, Johnson & Johnson, Boehringer Ingelheim, Teva Pharmaceutical Industries, Abbott Laboratories, Others.

3. What are the main segments of the Oral Drug Delivery?

The market segments include Dosage Form, Release Mechanism, Therapeutic Indication, Distribution Channel, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 133.94 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oral Drug Delivery," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oral Drug Delivery report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oral Drug Delivery?

To stay informed about further developments, trends, and reports in the Oral Drug Delivery, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence