Key Insights

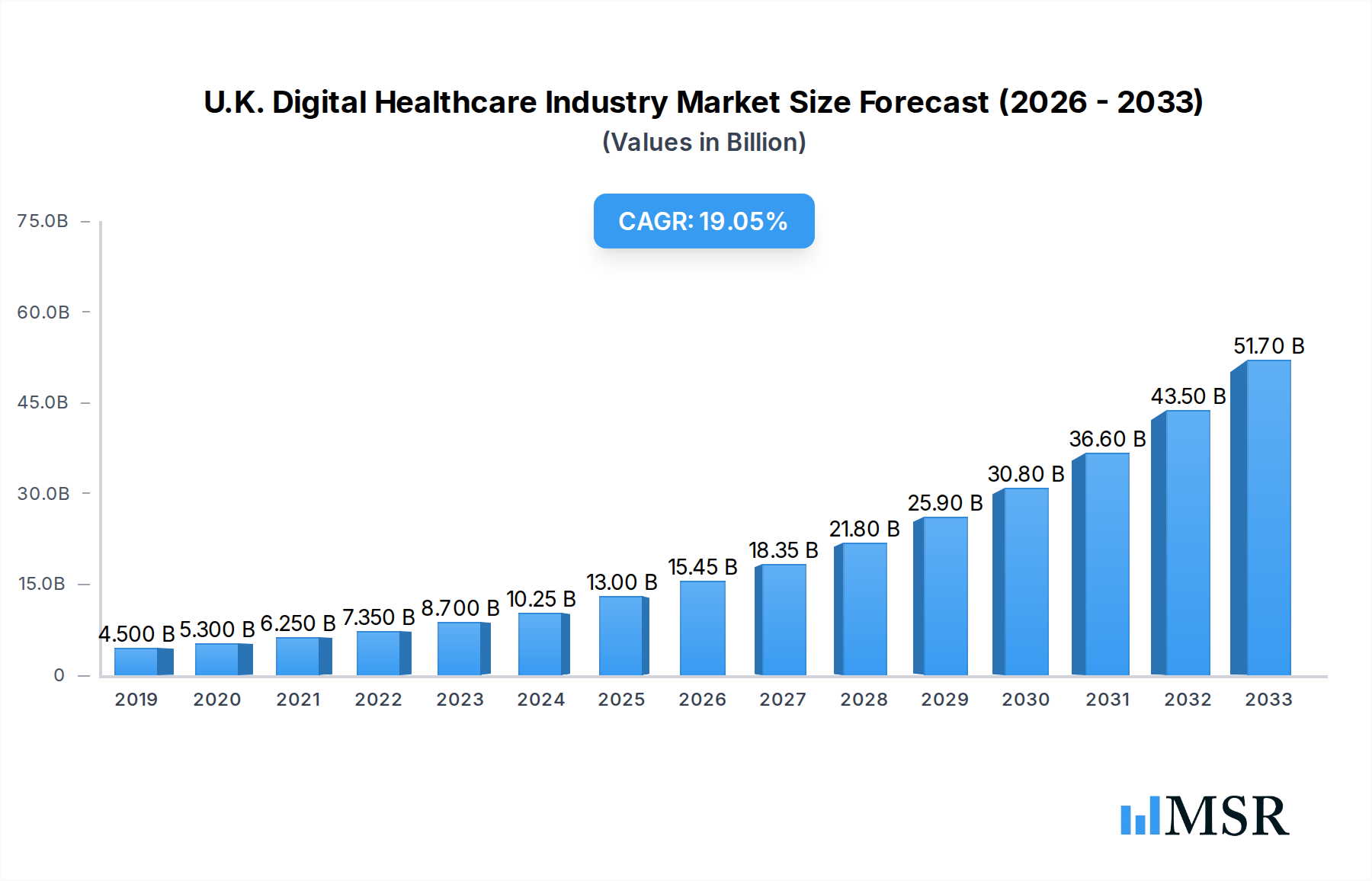

The U.K. digital healthcare industry is poised for substantial expansion, driven by an increasing adoption of advanced technologies and a growing demand for accessible, efficient healthcare solutions. With a projected CAGR of 18.96%, the market is set to reach an estimated £13,000 million by 2025. This robust growth is fueled by key drivers such as the escalating need for remote patient monitoring, the integration of telehealth services for chronic disease management, and the proactive government initiatives to digitize healthcare infrastructure. The mHealth segment, in particular, is experiencing a surge in demand for mobile applications that facilitate patient engagement, appointment scheduling, and access to health records. Furthermore, the burgeoning field of Healthcare Analytics is enabling providers to gain deeper insights into patient outcomes and operational efficiencies, thereby enhancing the overall quality of care. The U.K. is actively embracing digital transformation in its National Health Service (NHS), creating a fertile ground for innovations in digital health systems.

U.K. Digital Healthcare Industry Market Size (In Billion)

This dynamic market landscape is further characterized by significant trends including the widespread implementation of AI and machine learning for diagnostic support and personalized treatment plans, the increasing reliance on cloud-based solutions for data management and interoperability, and the growing emphasis on cybersecurity to protect sensitive patient information. While the market enjoys strong tailwinds, certain restraints such as data privacy concerns and the initial high cost of implementing advanced digital solutions need to be addressed. However, the long-term outlook remains exceptionally positive. The U.K. is investing heavily in digital health infrastructure, with a clear focus on improving patient outcomes, reducing healthcare costs, and enhancing the patient experience. The anticipated market size indicates a significant shift towards integrated digital healthcare ecosystems.

U.K. Digital Healthcare Industry Company Market Share

This in-depth report provides a critical analysis of the U.K. Digital Healthcare Industry, offering unparalleled insights into market dynamics, technological advancements, and growth trajectories. Spanning the Study Period 2019–2033, with a Base Year 2025, Estimated Year 2025, and Forecast Period 2025–2033, this report is an essential resource for stakeholders navigating the rapidly evolving landscape of digital health in the United Kingdom. With a focus on high-ranking keywords such as Telehealthcare, mHealth, Healthcare Analytics, Digital Health Systems, Software, Hardware, and Services, this report is meticulously crafted to maximize search visibility and attract key industry players.

U.K. Digital Healthcare Industry Market Concentration & Dynamics

The U.K. Digital Healthcare Industry is characterized by a dynamic interplay of established giants and agile startups. Market concentration is moderate, with a significant presence of major technology and healthcare providers alongside numerous specialized digital health companies. Innovation ecosystems are thriving, fueled by government initiatives and private investment, leading to a robust pipeline of new solutions. The regulatory framework, while evolving, is becoming more supportive of digital health adoption. Substitute products are emerging rapidly, primarily in the form of advanced wearable devices and AI-powered diagnostic tools, challenging traditional healthcare delivery models. End-user trends indicate a growing demand for convenient, personalized, and accessible healthcare, driving the adoption of digital solutions. Merger and acquisition (M&A) activities are a significant feature, with an estimated XX M&A deals occurring during the historical period. Key players like Cerner Corporation, McKesson Corporation, and Koninklijke Philips N.V. are actively involved in consolidating market share and acquiring innovative startups.

U.K. Digital Healthcare Industry Industry Insights & Trends

The U.K. Digital Healthcare Industry is experiencing robust growth, projected to reach a market size of over £XX Million by 2033, with a Compound Annual Growth Rate (CAGR) of approximately XX% from 2025 to 2033. This surge is primarily driven by increasing healthcare expenditure, a growing aging population with a higher prevalence of chronic diseases, and a widespread adoption of smartphones and internet connectivity, facilitating the reach of mHealth and Telehealthcare solutions. Technological disruptions are at the forefront, with advancements in Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), and Big Data analytics revolutionizing Healthcare Analytics and Digital Health Systems. AI is increasingly being deployed for predictive diagnostics, personalized treatment plans, and optimizing hospital operations, while IoT devices enable continuous remote patient monitoring. The evolving consumer behavior, influenced by the convenience and accessibility offered by digital platforms, is a powerful market driver. Patients are actively seeking digital alternatives for routine consultations, prescription refills, and access to health information, pushing healthcare providers to accelerate their digital transformation. The integration of Software, Hardware, and Services is crucial, creating seamless patient journeys and efficient healthcare workflows. The rise of personalized medicine, enabled by advanced analytics and genomics, further fuels the demand for sophisticated digital health solutions.

Key Markets & Segments Leading U.K. Digital Healthcare Industry

The Telehealthcare segment stands as a dominant force within the U.K. Digital Healthcare Industry, driven by its ability to overcome geographical barriers and improve access to medical professionals, especially in remote areas. The mHealth segment is also experiencing phenomenal growth, propelled by the ubiquity of smartphones and the increasing demand for health and fitness tracking applications. Healthcare Analytics is a crucial enabler, providing invaluable insights for better decision-making, operational efficiency, and personalized patient care. The Digital Health Systems segment underpins the entire ecosystem, integrating various digital tools and platforms.

Drivers for Telehealthcare Dominance:

- Government initiatives to reduce hospital waiting times.

- Increasing patient comfort and preference for remote consultations.

- Technological advancements in video conferencing and secure data transmission.

- Cost-effectiveness for both providers and patients.

Dominance Analysis of mHealth: The widespread adoption of smartphones across all age demographics makes mHealth solutions highly accessible. Applications ranging from chronic disease management and medication reminders to mental health support and fitness tracking are rapidly gaining traction. The integration of wearable devices further enhances the capabilities of mHealth, providing real-time physiological data that can be analyzed for early detection of health issues.

The Crucial Role of Healthcare Analytics: Big Data generated from various digital health touchpoints presents a treasure trove of information. Healthcare Analytics platforms are instrumental in processing this data to identify trends, predict disease outbreaks, optimize resource allocation, and personalize treatment pathways. This is essential for improving patient outcomes and driving down healthcare costs.

Integrated Digital Health Systems: The comprehensive integration of Software, Hardware, and Services forms the backbone of efficient Digital Health Systems. This includes electronic health records (EHRs), patient portals, remote monitoring platforms, and AI-powered diagnostic tools, all working in synergy to create a connected and intelligent healthcare ecosystem. The increasing investment in cloud-based solutions further enhances scalability and accessibility.

U.K. Digital Healthcare Industry Product Developments

The U.K. digital healthcare market is witnessing a wave of innovative product developments. Companies are focusing on enhancing user experience and clinical efficacy through advanced Software solutions, including AI-driven diagnostic tools and personalized patient engagement platforms. The proliferation of sophisticated Hardware, such as smart wearable devices and home-based medical equipment, is enabling remote patient monitoring and proactive health management. Integrated Services that combine these elements offer comprehensive solutions for chronic disease management, mental wellness, and specialized care. These advancements are creating significant competitive advantages for early adopters and driving higher standards of patient care and accessibility across the nation.

Challenges in the U.K. Digital Healthcare Industry Market

Despite its immense potential, the U.K. Digital Healthcare Industry faces several significant challenges. Regulatory hurdles, including data privacy concerns (GDPR compliance) and the need for robust cybersecurity measures, can slow down the adoption and deployment of new technologies. Interoperability issues between different digital health systems and legacy IT infrastructure present a substantial barrier, hindering seamless data exchange. Furthermore, the initial investment cost for implementing advanced digital solutions can be substantial, posing a challenge for smaller healthcare providers. Workforce training and digital literacy among healthcare professionals are also critical factors that require ongoing attention to ensure effective utilization of these new tools. Supply chain disruptions, particularly for specialized hardware components, can impact product availability and rollout timelines.

Forces Driving U.K. Digital Healthcare Industry Growth

The growth of the U.K. Digital Healthcare Industry is propelled by a confluence of powerful forces. Government support and funding initiatives aimed at modernizing the National Health Service (NHS) are significant catalysts. The increasing prevalence of chronic diseases and an aging population necessitate more efficient and accessible healthcare delivery models, which digital solutions are well-positioned to provide. Rapid technological advancements, including the expanding capabilities of AI, IoT, and Big Data analytics, are continuously creating new possibilities for improved patient care and operational efficiency. Furthermore, a growing consumer demand for personalized, convenient, and proactive healthcare experiences is actively shaping market trends and encouraging innovation.

Challenges in the U.K. Digital Healthcare Industry Market

Long-term growth in the U.K. Digital Healthcare Industry is underpinned by sustained innovation and strategic market expansion. Continued investment in research and development of cutting-edge technologies like personalized medicine, genomics integration, and advanced telehealth platforms is crucial. Fostering strategic partnerships between technology providers, healthcare institutions, and pharmaceutical companies will unlock new avenues for integrated care solutions. Expanding digital health services into underserved regions and to specific demographic groups, such as the elderly or those with limited digital literacy, will be key to achieving widespread impact and sustained growth.

Emerging Opportunities in U.K. Digital Healthcare Industry

The U.K. Digital Healthcare Industry is ripe with emerging opportunities. The continued expansion of Telehealthcare into specialized medical fields, such as mental health and chronic disease management, presents vast potential. The integration of AI-powered predictive analytics for early disease detection and prevention is a significant growth area. The burgeoning mHealth market, particularly in the realm of remote patient monitoring and personalized wellness, offers substantial opportunities for app developers and wearable technology manufacturers. Furthermore, the increasing focus on data-driven healthcare and the development of secure, interoperable Digital Health Systems will pave the way for innovative new services and business models, catering to the evolving needs of a digitally connected population. The growing emphasis on value-based healthcare models also creates opportunities for digital solutions that demonstrate improved patient outcomes and cost efficiencies.

Leading Players in the U.K. Digital Healthcare Industry Sector

- AMD Global Telemedicine Inc

- Cerner Corporation

- iHealth Lab Inc

- International Business Machines Corporation (IBM)

- Cisco Systems

- Allscripts Healthcare Solutions Inc

- Koninklijke Philips N.V.

- McKesson Corporation

- AT&T

- Athenahealth Inc

Key Milestones in U.K. Digital Healthcare Industry Industry

- July 2023: Plan Your Baby, a London-based startup, launched a new telehealth fertility clinic in the UK, providing accessible fertility support through digital channels.

- June 2023: The Government of England announced plans for a Digital NHS Health Check to be delivered to one million individuals across England, commencing from the following spring, aiming to proactively manage population health.

Strategic Outlook for U.K. Digital Healthcare Industry Market

The strategic outlook for the U.K. Digital Healthcare Industry market is exceptionally positive, driven by continuous innovation and a strong commitment to digital transformation within the healthcare sector. Future growth will be accelerated by the deeper integration of AI and ML across all segments, enabling more personalized and predictive healthcare. The expansion of cloud-based Digital Health Systems will enhance scalability and data accessibility. Strategic collaborations and investments in Telehealthcare and mHealth infrastructure will further solidify the market's growth trajectory. Opportunities abound for companies focusing on patient-centric solutions, preventative care, and data analytics, positioning the U.K. as a global leader in the digital health revolution.

U.K. Digital Healthcare Industry Segmentation

-

1. Technology

- 1.1. Telehealthcare

- 1.2. mHealth

- 1.3. Healthcare Analytics

- 1.4. Digital Health Systems

-

2. Component

- 2.1. Software

- 2.2. Hardware

- 2.3. Services

U.K. Digital Healthcare Industry Segmentation By Geography

- 1. U.K.

U.K. Digital Healthcare Industry Regional Market Share

Geographic Coverage of U.K. Digital Healthcare Industry

U.K. Digital Healthcare Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.96% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Telehealthcare

- 5.1.2. mHealth

- 5.1.3. Healthcare Analytics

- 5.1.4. Digital Health Systems

- 5.2. Market Analysis, Insights and Forecast - by Component

- 5.2.1. Software

- 5.2.2. Hardware

- 5.2.3. Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. U.K.

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. U.K. Digital Healthcare Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Telehealthcare

- 6.1.2. mHealth

- 6.1.3. Healthcare Analytics

- 6.1.4. Digital Health Systems

- 6.2. Market Analysis, Insights and Forecast - by Component

- 6.2.1. Software

- 6.2.2. Hardware

- 6.2.3. Services

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 AMD Global Telemedicine Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Cerner Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 iHealth Lab Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 International business Machinery Corporation (IBM)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Cisco Systems

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Allscripts Healthcare Solutions Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Koninklijke Philips N V

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 McKesson Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AT & T

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Athenahealth Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 AMD Global Telemedicine Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: U.K. Digital Healthcare Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: U.K. Digital Healthcare Industry Share (%) by Company 2025

List of Tables

- Table 1: U.K. Digital Healthcare Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 2: U.K. Digital Healthcare Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 3: U.K. Digital Healthcare Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 4: U.K. Digital Healthcare Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 5: U.K. Digital Healthcare Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: U.K. Digital Healthcare Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: U.K. Digital Healthcare Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 8: U.K. Digital Healthcare Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 9: U.K. Digital Healthcare Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 10: U.K. Digital Healthcare Industry Volume K Unit Forecast, by Component 2020 & 2033

- Table 11: U.K. Digital Healthcare Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: U.K. Digital Healthcare Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the U.K. Digital Healthcare Industry?

The projected CAGR is approximately 18.96%.

2. Which companies are prominent players in the U.K. Digital Healthcare Industry?

Key companies in the market include AMD Global Telemedicine Inc, Cerner Corporation, iHealth Lab Inc, International business Machinery Corporation (IBM), Cisco Systems, Allscripts Healthcare Solutions Inc, Koninklijke Philips N V, McKesson Corporation, AT & T, Athenahealth Inc.

3. What are the main segments of the U.K. Digital Healthcare Industry?

The market segments include Technology, Component.

4. Can you provide details about the market size?

The market size is estimated to be USD 13 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Digital Healthcare; Rise in Artificial Intelligence. IoT. and Big Data; Growing adoption of mobile health applications.

6. What are the notable trends driving market growth?

mHealth Segment is Expected to Hold a Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Cybersecurity And Privacy Concerns.

8. Can you provide examples of recent developments in the market?

July 2023: Plan Your Baby, a London-based startup launched new telehealth fertility clinic in the UK to provide fertility support.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "U.K. Digital Healthcare Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the U.K. Digital Healthcare Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the U.K. Digital Healthcare Industry?

To stay informed about further developments, trends, and reports in the U.K. Digital Healthcare Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence