Key Insights

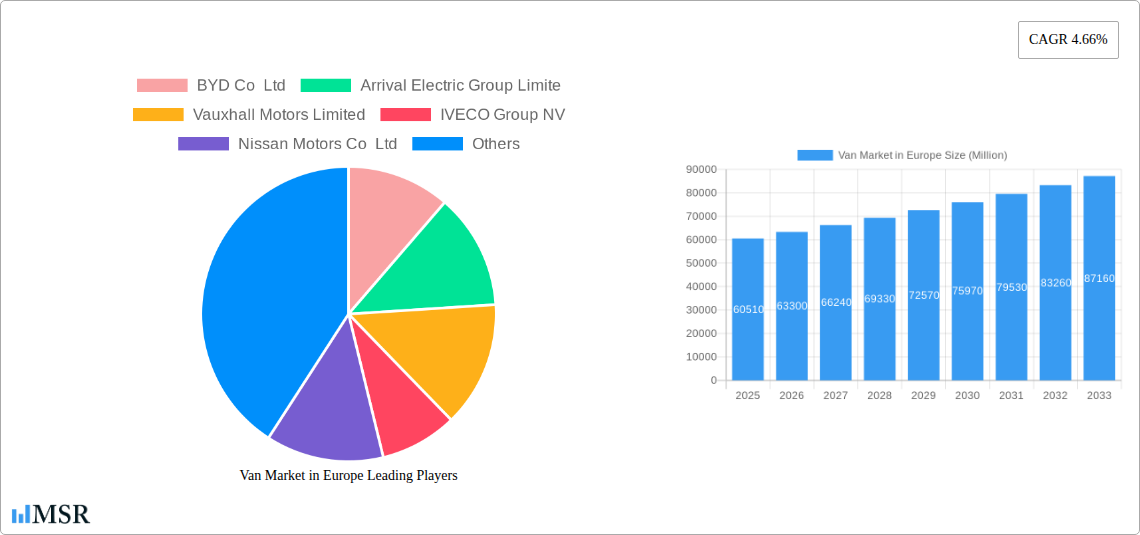

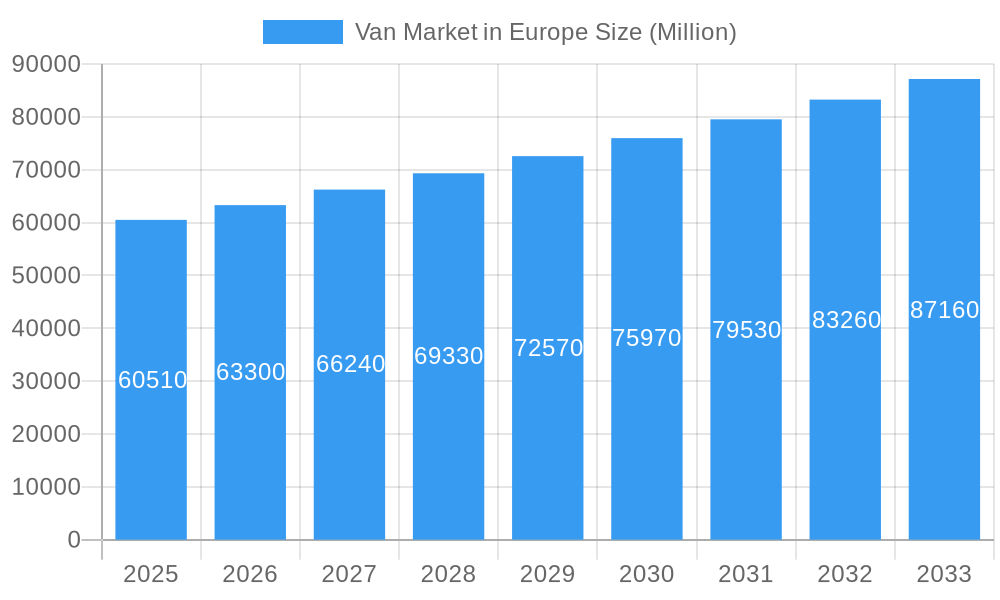

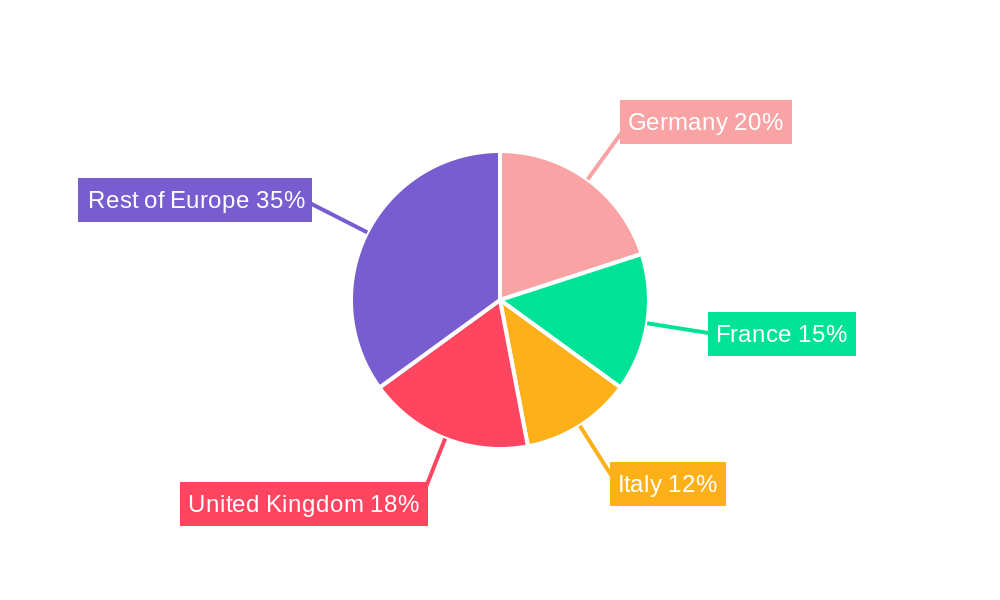

The European van market, valued at €60.51 billion in 2025, is projected to experience robust growth, driven by a compound annual growth rate (CAGR) of 4.66% from 2025 to 2033. This expansion is fueled by several key factors. The burgeoning e-commerce sector necessitates efficient last-mile delivery solutions, significantly boosting demand for vans across various sizes and drive types. Furthermore, government initiatives promoting sustainable transportation, including incentives for electric and alternative fuel vans, are accelerating market adoption of greener vehicles. The construction and logistics sectors, major end-users, also contribute significantly to market growth, with increasing investment in infrastructure and supply chain optimization. Segmentation analysis reveals a strong preference for vans with cargo space exceeding 5 cubic meters, particularly within the commercial sector. While Internal Combustion Engine (ICE) vans currently dominate the market, the adoption of electric and alternative fuel vans is gaining traction, driven by environmental concerns and government regulations. Competitive landscape analysis reveals a diverse range of established and emerging players such as BYD, Arrival, Vauxhall, IVECO, Nissan, Volkswagen, Stellantis, Daimler, Renault, Toyota, Hyundai, and Ford, each vying for market share through technological innovation and strategic partnerships. The market's growth is not uniform across all European nations; Germany, France, Italy, and the UK are expected to be leading contributors, due to robust economies and high demand across multiple sectors.

Van Market in Europe Market Size (In Billion)

The European van market's continued growth is contingent upon several factors. Overcoming challenges such as the rising cost of raw materials and supply chain disruptions will be crucial. Furthermore, manufacturers must continue to innovate, offering a broader range of electric and alternative fuel options to meet evolving environmental regulations and consumer preferences. Sustained economic growth across major European nations is also essential for maintaining the predicted CAGR. The ongoing development of charging infrastructure for electric vans will directly impact market penetration. Finally, effective marketing strategies targeting commercial and government clients will be vital to drive further adoption and increase market penetration. The projected growth reflects a positive outlook, but successful navigation of these challenges is crucial to realizing the market's full potential.

Van Market in Europe Company Market Share

Van Market in Europe: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the European van market, encompassing market dynamics, industry trends, key players, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an essential resource for industry stakeholders, investors, and strategists seeking to navigate the complexities of this dynamic market. The report leverages extensive data analysis to offer actionable insights and predictions, covering all major segments and key players. The European van market is projected to reach xx Million by 2033.

Van Market in Europe Market Concentration & Dynamics

The European van market exhibits a moderately concentrated landscape, with several major players holding significant market share. Volkswagen AG, Stellantis NV, Daimler AG, and Ford Motor Company collectively account for an estimated xx% of the market. However, the emergence of new electric vehicle (EV) manufacturers like BYD Co Ltd and Arrival Electric Group Limited is disrupting the traditional market structure, fostering increased competition and innovation.

Market Dynamics:

- Innovation Ecosystems: Significant investments in R&D are driving innovation in areas such as electrification, autonomous driving, and connectivity. Collaborations between established automakers and tech companies are further accelerating this trend.

- Regulatory Frameworks: Stringent emission regulations, such as Euro VI and upcoming stricter standards, are pushing manufacturers to adopt cleaner technologies, particularly electric and alternative fuel vehicles.

- Substitute Products: The rise of alternative transportation solutions, such as cargo bikes and delivery drones, is impacting the van market, particularly in urban areas.

- End-User Trends: The growing e-commerce sector is driving demand for delivery vans, while the increasing focus on sustainability is boosting the adoption of electric vans.

- M&A Activities: The number of M&A deals in the European van market has fluctuated in recent years, with xx deals recorded between 2019 and 2024. These activities often involve strategic acquisitions of smaller companies possessing specialized technologies or a strong presence in niche markets.

Van Market in Europe Industry Insights & Trends

The European van market experienced a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024). Market size in 2024 was estimated at xx Million. Growth is primarily driven by the flourishing e-commerce industry, expanding logistics networks, and increasing urbanization. The rising adoption of electric and alternative fuel vehicles is further shaping market trends, driven by government incentives, environmental concerns, and advancements in battery technology. Technological disruptions, including the integration of advanced driver-assistance systems (ADAS) and connected vehicle technologies, are transforming the van landscape. Shifting consumer preferences towards fuel efficiency, reduced emissions, and enhanced safety features are influencing vehicle purchasing decisions. The forecast period (2025-2033) is projected to witness a CAGR of xx%, reaching xx Million by 2033. This growth will be fueled by continued expansion of e-commerce and logistics, and broader adoption of electric and alternative fuel vehicles.

Key Markets & Segments Leading Van Market in Europe

Dominant Segments:

- By Cargo Space: The "More than 5 Cubic Meter" segment holds the largest market share due to its ability to accommodate larger volumes of goods.

- By End-User: The "Commercial" segment dominates, reflecting the significant demand from businesses involved in logistics, delivery, and other commercial activities.

- By Drive Type: While IC Engine vans still hold a larger market share, the "Electric" segment is experiencing the fastest growth due to environmental regulations and technological advancements.

Drivers by Segment:

- More than 5 Cubic Meter: Expansion of logistics and distribution networks, growth of e-commerce.

- Less than 5 Cubic Meter: Growth of last-mile delivery services, increasing demand for smaller, more maneuverable vans in urban areas.

- Commercial: Flourishing e-commerce and business activities, rising demand for efficient transportation solutions.

- Government: Government fleet modernization programs, increased focus on sustainable transportation options.

- IC Engine: Established infrastructure for fuel distribution, lower initial purchase price compared to electric vehicles.

- Electric: Government incentives and subsidies, growing environmental awareness, advancements in battery technology.

- Alternative Fuel: Focus on reducing carbon emissions, exploration of alternative fuel options like CNG and hydrogen.

Germany, France, and the UK are the leading national markets in Europe, driven by robust economic growth, well-developed infrastructure, and high demand for commercial vehicles.

Van Market in Europe Product Developments

Significant advancements are transforming the van market, with a growing focus on electric vehicles, alternative fuel options, and enhanced safety features. Manufacturers are integrating ADAS, telematics, and connectivity features to improve efficiency, safety, and fleet management. Lightweight materials and aerodynamic designs are being employed to enhance fuel economy and reduce emissions. The development of modular platforms allows for greater flexibility in customization and the ability to offer a wider range of vehicle configurations tailored to specific customer needs.

Challenges in the Van Market in Europe Market

Several challenges hinder the growth of the European van market. Stringent emission regulations impose significant costs on manufacturers to comply with increasingly stricter standards. Supply chain disruptions, particularly regarding battery components for electric vans, create production bottlenecks and affect vehicle availability. Intense competition from established and emerging players requires continuous innovation and cost optimization to maintain market share. These factors collectively impact overall market growth and profitability. The total quantifiable impact of these challenges is estimated to result in a xx Million loss annually in the European Van Market.

Forces Driving Van Market in Europe Growth

Key growth drivers include the expansion of e-commerce, the increasing demand for last-mile delivery services, and the growing adoption of electric and alternative fuel vehicles, driven by government incentives and environmental concerns. Advances in battery technology and charging infrastructure are also pivotal in driving the electric van market. The continuous improvement of autonomous driving technologies holds great potential for enhancing efficiency and safety in the future.

Long-Term Growth Catalysts in the Van Market in Europe

Long-term growth will be fueled by the continued expansion of the e-commerce sector, increasing investment in infrastructure, and further advancements in battery technology and autonomous driving capabilities. Strategic partnerships between traditional automakers and technology companies will drive innovation and product development. The exploration of new markets and segments, such as specialized vans for specific industries, presents significant growth potential. Expansion into new geographical regions will also contribute to long-term growth.

Emerging Opportunities in Van Market in Europe

Emerging opportunities include the growth of the electric van market, the development of autonomous delivery systems, and the rise of subscription-based van services. The integration of smart technologies, such as connected fleet management systems, creates opportunities to enhance efficiency and operational effectiveness. The expanding sharing economy and the increasing adoption of van-pooling services offer further avenues for growth. Focus on sustainable materials and environmentally friendly manufacturing processes will gain market traction.

Leading Players in the Van Market in Europe Sector

Key Milestones in Van Market in Europe Industry

- June 2023: TÜV Rheinland and Centro Tecnológico Randon (CTR) collaborate on automotive vehicle and component certification, boosting industry standardization.

- May 2023: Arrival builds 3 L Vans, accumulating over 90,000 km of road testing, demonstrating progress in electric van production.

- May 2023: AvtoVAZ showcases diverse LADA van models, highlighting expansion in commercial vehicle offerings.

- January 2022: Volkswagen unveils a new electric van with an extended range (up to 342 miles), signaling advancements in electric vehicle technology.

Strategic Outlook for Van Market in Europe Market

The European van market holds significant future potential, driven by the continued growth of e-commerce, the increasing adoption of electric and alternative fuel vehicles, and the ongoing development of autonomous driving technologies. Strategic opportunities lie in capitalizing on the shift towards sustainable transportation, developing innovative vehicle designs and features, and fostering strategic partnerships to accelerate technological advancements. The market presents lucrative prospects for companies capable of adapting to evolving consumer preferences, embracing technological innovation, and efficiently navigating the challenges of a dynamic regulatory landscape.

Van Market in Europe Segmentation

-

1. Cargo Space

- 1.1. More than 5 Cubic Meter

- 1.2. Less than 5 Cubic Meter

-

2. End User

- 2.1. Commercial

- 2.2. Government

-

3. Drive Type

- 3.1. IC Engine

- 3.2. Electric

- 3.3. Alternative Fuel

Van Market in Europe Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. France

- 5. Spain

- 6. Rest of Europe

Van Market in Europe Regional Market Share

Geographic Coverage of Van Market in Europe

Van Market in Europe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.66% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Cargo Space

- 5.1.1. More than 5 Cubic Meter

- 5.1.2. Less than 5 Cubic Meter

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Commercial

- 5.2.2. Government

- 5.3. Market Analysis, Insights and Forecast - by Drive Type

- 5.3.1. IC Engine

- 5.3.2. Electric

- 5.3.3. Alternative Fuel

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. Italy

- 5.4.4. France

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Cargo Space

- 6. Van Market in Europe Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Cargo Space

- 6.1.1. More than 5 Cubic Meter

- 6.1.2. Less than 5 Cubic Meter

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Commercial

- 6.2.2. Government

- 6.3. Market Analysis, Insights and Forecast - by Drive Type

- 6.3.1. IC Engine

- 6.3.2. Electric

- 6.3.3. Alternative Fuel

- 6.1. Market Analysis, Insights and Forecast - by Cargo Space

- 7. Germany Van Market in Europe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Cargo Space

- 7.1.1. More than 5 Cubic Meter

- 7.1.2. Less than 5 Cubic Meter

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Commercial

- 7.2.2. Government

- 7.3. Market Analysis, Insights and Forecast - by Drive Type

- 7.3.1. IC Engine

- 7.3.2. Electric

- 7.3.3. Alternative Fuel

- 7.1. Market Analysis, Insights and Forecast - by Cargo Space

- 8. United Kingdom Van Market in Europe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Cargo Space

- 8.1.1. More than 5 Cubic Meter

- 8.1.2. Less than 5 Cubic Meter

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Commercial

- 8.2.2. Government

- 8.3. Market Analysis, Insights and Forecast - by Drive Type

- 8.3.1. IC Engine

- 8.3.2. Electric

- 8.3.3. Alternative Fuel

- 8.1. Market Analysis, Insights and Forecast - by Cargo Space

- 9. Italy Van Market in Europe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Cargo Space

- 9.1.1. More than 5 Cubic Meter

- 9.1.2. Less than 5 Cubic Meter

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Commercial

- 9.2.2. Government

- 9.3. Market Analysis, Insights and Forecast - by Drive Type

- 9.3.1. IC Engine

- 9.3.2. Electric

- 9.3.3. Alternative Fuel

- 9.1. Market Analysis, Insights and Forecast - by Cargo Space

- 10. France Van Market in Europe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Cargo Space

- 10.1.1. More than 5 Cubic Meter

- 10.1.2. Less than 5 Cubic Meter

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Commercial

- 10.2.2. Government

- 10.3. Market Analysis, Insights and Forecast - by Drive Type

- 10.3.1. IC Engine

- 10.3.2. Electric

- 10.3.3. Alternative Fuel

- 10.1. Market Analysis, Insights and Forecast - by Cargo Space

- 11. Spain Van Market in Europe Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Cargo Space

- 11.1.1. More than 5 Cubic Meter

- 11.1.2. Less than 5 Cubic Meter

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Commercial

- 11.2.2. Government

- 11.3. Market Analysis, Insights and Forecast - by Drive Type

- 11.3.1. IC Engine

- 11.3.2. Electric

- 11.3.3. Alternative Fuel

- 11.1. Market Analysis, Insights and Forecast - by Cargo Space

- 12. Rest of Europe Van Market in Europe Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Cargo Space

- 12.1.1. More than 5 Cubic Meter

- 12.1.2. Less than 5 Cubic Meter

- 12.2. Market Analysis, Insights and Forecast - by End User

- 12.2.1. Commercial

- 12.2.2. Government

- 12.3. Market Analysis, Insights and Forecast - by Drive Type

- 12.3.1. IC Engine

- 12.3.2. Electric

- 12.3.3. Alternative Fuel

- 12.1. Market Analysis, Insights and Forecast - by Cargo Space

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 BYD Co Ltd

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Arrival Electric Group Limite

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Vauxhall Motors Limited

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 IVECO Group NV

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Nissan Motors Co Ltd

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Volkswagen AG

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Stellantis NV

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Daimler AG

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Groupe Renault

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Toyota Motor Corporation

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Hyundai Motors

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Ford Motor Company

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.1 BYD Co Ltd

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Van Market in Europe Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Van Market in Europe Share (%) by Company 2025

List of Tables

- Table 1: Van Market in Europe Revenue Million Forecast, by Cargo Space 2020 & 2033

- Table 2: Van Market in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Van Market in Europe Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 4: Van Market in Europe Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Van Market in Europe Revenue Million Forecast, by Cargo Space 2020 & 2033

- Table 6: Van Market in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 7: Van Market in Europe Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 8: Van Market in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Van Market in Europe Revenue Million Forecast, by Cargo Space 2020 & 2033

- Table 10: Van Market in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 11: Van Market in Europe Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 12: Van Market in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Van Market in Europe Revenue Million Forecast, by Cargo Space 2020 & 2033

- Table 14: Van Market in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 15: Van Market in Europe Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 16: Van Market in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Van Market in Europe Revenue Million Forecast, by Cargo Space 2020 & 2033

- Table 18: Van Market in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 19: Van Market in Europe Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 20: Van Market in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Van Market in Europe Revenue Million Forecast, by Cargo Space 2020 & 2033

- Table 22: Van Market in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 23: Van Market in Europe Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 24: Van Market in Europe Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Van Market in Europe Revenue Million Forecast, by Cargo Space 2020 & 2033

- Table 26: Van Market in Europe Revenue Million Forecast, by End User 2020 & 2033

- Table 27: Van Market in Europe Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 28: Van Market in Europe Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Van Market in Europe?

The projected CAGR is approximately 4.66%.

2. Which companies are prominent players in the Van Market in Europe?

Key companies in the market include BYD Co Ltd, Arrival Electric Group Limite, Vauxhall Motors Limited, IVECO Group NV, Nissan Motors Co Ltd, Volkswagen AG, Stellantis NV, Daimler AG, Groupe Renault, Toyota Motor Corporation, Hyundai Motors, Ford Motor Company.

3. What are the main segments of the Van Market in Europe?

The market segments include Cargo Space, End User, Drive Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 60.51 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in Sale of Electric Vans.

6. What are the notable trends driving market growth?

Rise in Sale of Electric Vans.

7. Are there any restraints impacting market growth?

High Cost of Electric Vehicle Battery.

8. Can you provide examples of recent developments in the market?

June 2023: TÜV Rheinland and Centro Tecnológico Randon (CTR) have announced a collaboration for automotive vehicle and component homologation, testing, and type certification. The collaboration aims to provide an extensive range of certification services for commercial vehicles, light cars, vehicle systems, and components while maintaining the security and flexibility that clients expect.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Van Market in Europe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Van Market in Europe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Van Market in Europe?

To stay informed about further developments, trends, and reports in the Van Market in Europe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence