Key Insights

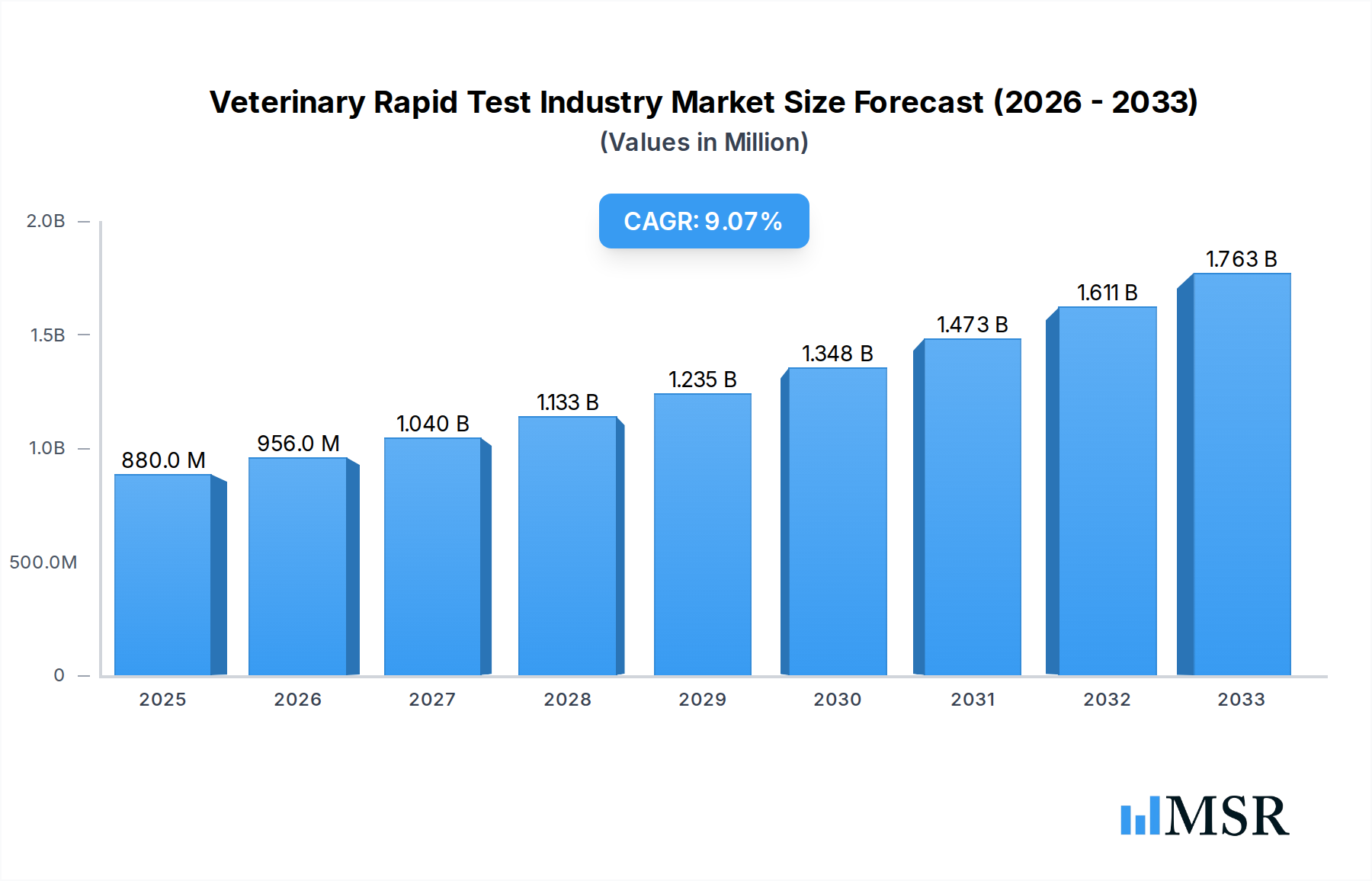

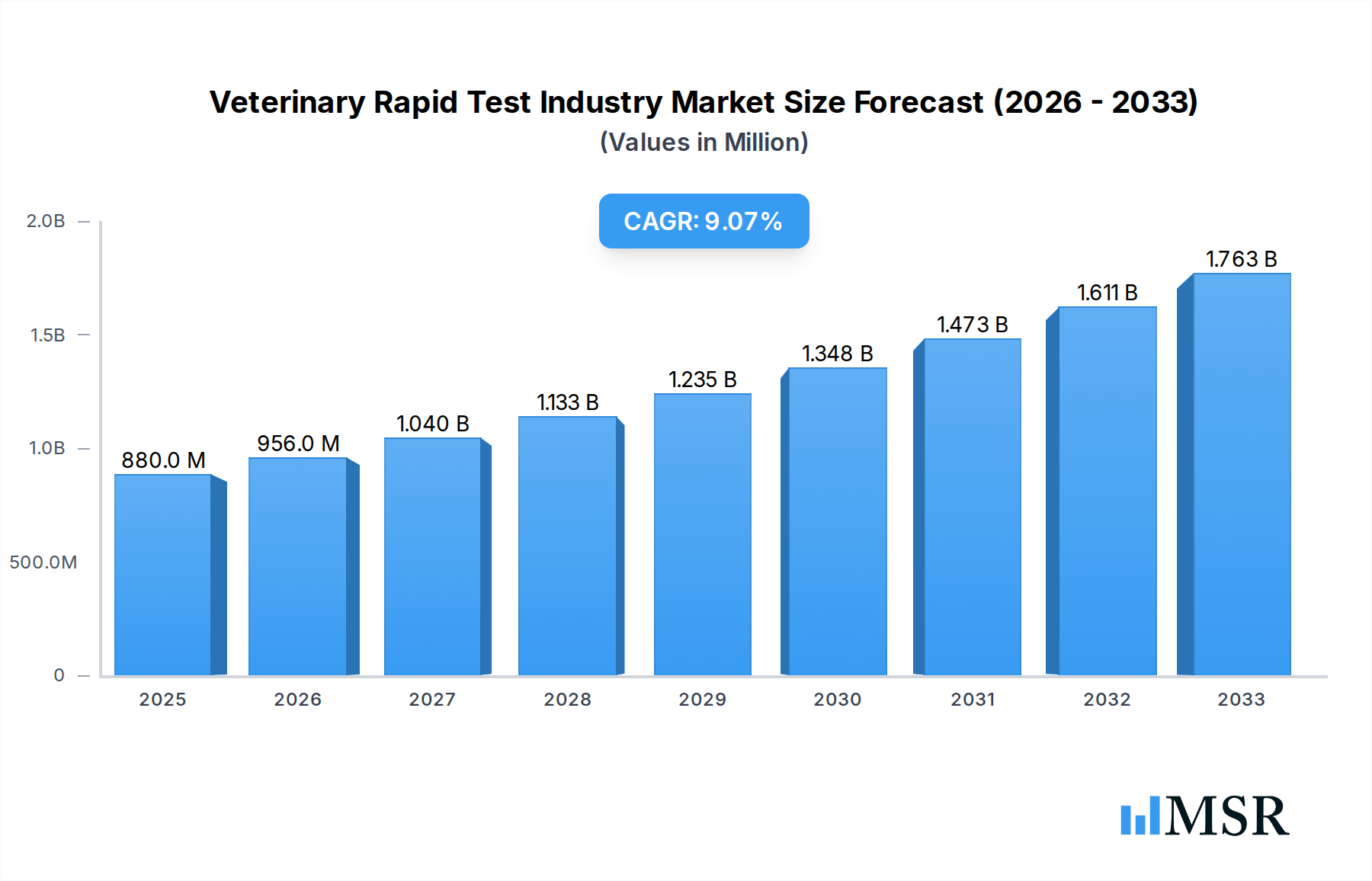

The global Veterinary Rapid Test Industry is poised for significant expansion, driven by an increasing emphasis on animal health and welfare, alongside advancements in diagnostic technologies. The market is valued at an estimated $880 million in the base year of 2025, and is projected to experience a robust Compound Annual Growth Rate (CAGR) of 8.70% throughout the forecast period of 2025-2033. This growth is largely fueled by the rising incidence of viral, bacterial, and parasitic diseases in both companion and livestock animals, necessitating swift and accurate on-site diagnostics. The growing pet humanization trend, leading to increased spending on pet healthcare, coupled with the economic importance of livestock health for food security, are critical market accelerators. Furthermore, the convenience and cost-effectiveness of rapid test kits and readers are making them indispensable tools for veterinarians, enabling quicker treatment decisions and improved patient outcomes.

Veterinary Rapid Test Industry Market Size (In Million)

The market's trajectory is also shaped by evolving trends such as the development of multiplex diagnostic tests capable of detecting multiple pathogens simultaneously, and the integration of digital technologies for data management and analysis. While the market demonstrates strong growth potential, certain restraints may influence its pace. These include the initial cost of advanced diagnostic readers, potential regulatory hurdles in specific regions, and the need for continuous training and education for veterinary professionals on utilizing these technologies effectively. Key segments contributing to this market include viral and bacterial disease applications, with rapid test kits representing the dominant product type. Geographically, North America and Europe are expected to lead market share due to high veterinary expenditure and advanced healthcare infrastructure, while the Asia Pacific region is anticipated to witness the fastest growth owing to increasing disposable incomes and a growing awareness of animal health issues. Leading companies such as IDEXX Laboratories Inc. and Zoetis Inc. are actively innovating and expanding their product portfolios to capitalize on these burgeoning market dynamics.

Veterinary Rapid Test Industry Company Market Share

Here's the SEO-optimized and engaging report description for the Veterinary Rapid Test Industry, meticulously crafted for search visibility and stakeholder attraction:

Unlock the Future of Animal Health Diagnostics: Comprehensive Veterinary Rapid Test Industry Report 2024-2033

Dive deep into the burgeoning veterinary rapid test market with our unparalleled industry analysis, covering the pivotal period from 2019–2033, with a robust focus on the base and estimated year of 2025. This definitive report provides critical insights into the global veterinary diagnostics landscape, equipping industry stakeholders with the strategic intelligence needed to navigate veterinary point-of-care testing and capitalize on future growth. Explore market dynamics, innovation trends, and key players shaping the veterinary rapid diagnostic kits sector. This report is essential for veterinary diagnostic companies, veterinary practitioners, animal health investors, and pet owners seeking to understand the trajectory of veterinary disease detection and management.

Veterinary Rapid Test Industry Market Concentration & Dynamics

The veterinary rapid test industry exhibits a moderate to high level of market concentration, with a few key players dominating a significant portion of the market share. This concentration is driven by substantial R&D investments, established distribution networks, and stringent regulatory approvals for veterinary diagnostic solutions. Innovation ecosystems are flourishing, fueled by advancements in biomarker discovery and assay development, particularly for rapid veterinary diagnostics. Regulatory frameworks, while crucial for ensuring product safety and efficacy, can also act as a barrier to entry for new competitors, particularly in regions with rigorous approval processes. Substitute products, such as traditional laboratory-based diagnostic methods, are gradually being displaced by the speed, convenience, and cost-effectiveness of rapid tests. End-user trends are strongly leaning towards point-of-care diagnostics within veterinary clinics, driven by the desire for immediate results and improved patient outcomes. Mergers and acquisitions (M&A) activities are a significant indicator of market consolidation and strategic expansion, with companies seeking to broaden their product portfolios and geographic reach. The market has witnessed several strategic acquisitions aimed at integrating complementary technologies and market access, further solidifying the positions of leading veterinary rapid test manufacturers. The current market share distribution suggests a dynamic competitive landscape where strategic partnerships and technological innovation are paramount.

Veterinary Rapid Test Industry Industry Insights & Trends

The veterinary rapid test industry is poised for significant expansion, projected to reach a market size of $5,200 Million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 12.5% expected throughout the forecast period of 2025–2033. This robust growth is underpinned by several key drivers, including the escalating pet population worldwide and the increasing demand for advanced veterinary healthcare services. Owners are increasingly investing in their pets' well-being, leading to a greater adoption of preventative care and diagnostic testing, which directly fuels the demand for veterinary rapid diagnostic kits. Technological disruptions are at the forefront of this growth, with continuous innovation in assay sensitivity, specificity, and multiplexing capabilities. The development of rapid test readers that offer enhanced data management and connectivity is also transforming the veterinary point-of-care testing landscape. Furthermore, the rising prevalence of zoonotic diseases and the growing awareness of animal welfare are creating a critical need for rapid and reliable diagnostic tools, particularly for viral diseases, bacterial diseases, and parasitic diseases. Evolving consumer behaviors, characterized by a demand for faster diagnoses, reduced wait times, and more accessible veterinary care, are aligning perfectly with the advantages offered by rapid diagnostic solutions. The integration of artificial intelligence and machine learning in diagnostic platforms is also emerging as a significant trend, promising to further enhance the accuracy and efficiency of veterinary disease detection. The increasing focus on companion animals, alongside the critical needs of livestock health, provides a broad spectrum for market penetration and innovation in veterinary diagnostics.

Key Markets & Segments Leading Veterinary Rapid Test Industry

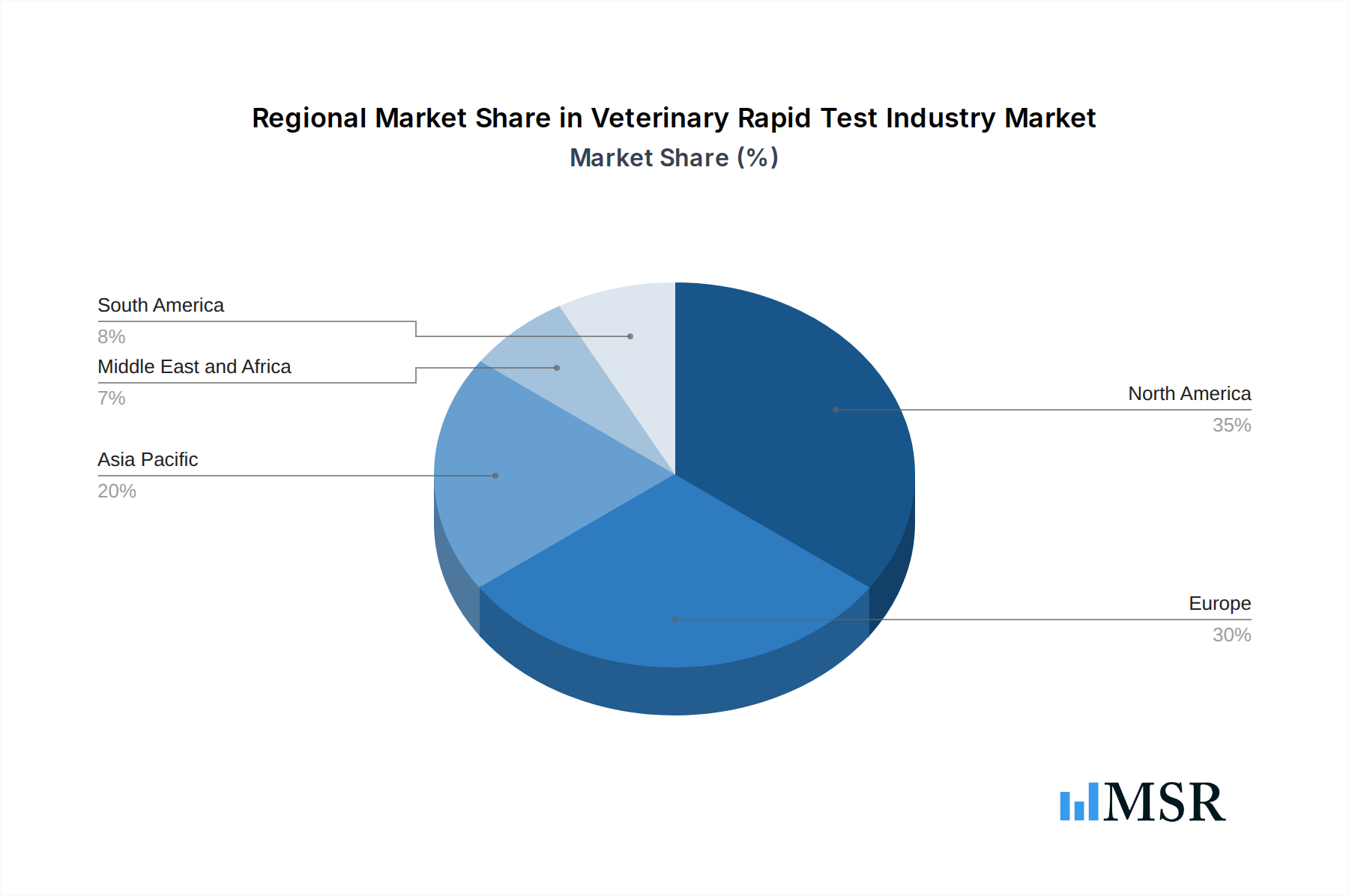

The veterinary rapid test industry is experiencing significant traction globally, with North America currently leading the market due to a high pet ownership rate, advanced veterinary infrastructure, and a strong willingness to invest in animal healthcare. The United States, in particular, represents a dominant market due to its large companion animal population and widespread adoption of advanced veterinary diagnostics. In terms of Product Type, Rapid Test Kits are the undisputed leader, accounting for the vast majority of the market revenue, driven by their ease of use and cost-effectiveness for routine diagnostics. The growth of Rapid Test Readers is also accelerating, as they enhance the utility and data output of the kits, offering integrated solutions for veterinary clinics.

Dominance Drivers for Rapid Test Kits:

- High demand for infectious disease screening: Rapid tests are crucial for quick diagnosis of common viral diseases, bacterial diseases, and parasitic diseases in both companion animals and livestock animals.

- Cost-effectiveness: Compared to traditional lab tests, rapid kits offer a more economical solution for veterinarians.

- Point-of-care convenience: Enables immediate diagnosis and treatment initiation within the clinic.

Dominance Drivers for Companion Animals:

- Increasing pet humanization: Owners view pets as family members, leading to higher spending on their health.

- Growth in specialized veterinary services: The demand for diagnostics for allergies, cardiac issues, and cancer screening is rising.

- Technological adoption by veterinarians: Clinics are readily embracing new diagnostic tools to improve patient care.

Dominance Drivers for Viral Diseases:

- Prevalence of common viral infections: Diseases like parvovirus, distemper, and influenza require rapid identification.

- Importance in vaccination programs: Rapid tests are used to assess immunity and diagnose potential vaccine failures.

- Pandemic preparedness: Increased focus on infectious disease control due to past global health events.

The Asia-Pacific region is projected to exhibit the highest growth rate, fueled by a rapidly expanding middle class, increasing pet ownership, and a growing awareness of animal health, particularly in countries like China and India.

Veterinary Rapid Test Industry Product Developments

Product developments in the veterinary rapid test industry are focused on enhancing speed, accuracy, and multiplexing capabilities. Innovations include novel immunoassay technologies and molecular diagnostic approaches for faster and more precise veterinary disease detection. The integration of digital technologies, leading to smart rapid test readers that offer data connectivity and analysis, is transforming the diagnostic workflow in veterinary practices. These advancements are crucial for timely diagnosis of viral diseases, bacterial diseases, and parasitic diseases in companion animals and livestock animals. For instance, the April 2024 launch of Antech's Nu.Q Vet Cancer Test exemplifies a significant leap in rapid oncology diagnostics for dogs.

Challenges in the Veterinary Rapid Test Industry Market

Despite robust growth, the veterinary rapid test industry faces several challenges. Stringent regulatory hurdles in various international markets can delay product approvals and market entry, estimated to cost millions in development and launch phases. Supply chain disruptions, exacerbated by global events, can impact the availability of raw materials and finished products, leading to an estimated 5-10% fluctuation in supply. Competitive pressures from established players and new entrants, coupled with pricing sensitivities in some market segments, also present significant barriers. The need for continuous R&D investment to keep pace with technological advancements can be financially demanding, with estimated annual R&D expenditures ranging from $50 Million to $200 Million for leading companies.

Forces Driving Veterinary Rapid Test Industry Growth

Several forces are propelling the veterinary rapid test industry forward. Technological advancements in assay design and reader technology are creating more sensitive and specific veterinary diagnostics. The increasing pet humanization trend translates to higher spending on animal healthcare, driving demand for veterinary point-of-care testing. Furthermore, growing awareness of zoonotic diseases and the importance of animal welfare are boosting the adoption of rapid diagnostic tools for early veterinary disease detection. Government initiatives promoting animal health and biosecurity, coupled with economic growth in emerging markets, also contribute significantly to market expansion, with estimated government spending on animal health reaching $30 Billion globally.

Challenges in the Veterinary Rapid Test Industry Market

Long-term growth catalysts for the veterinary rapid test industry are multifaceted. Continued innovation in multiplexing tests, allowing for the simultaneous detection of multiple pathogens or biomarkers, will be crucial. Strategic partnerships between diagnostic companies and veterinary clinics or pharmaceutical firms will expand market reach and product adoption. Furthermore, expanding into emerging markets with growing pet populations and increasing veterinary infrastructure will unlock significant new revenue streams. The development of more affordable and user-friendly veterinary rapid diagnostic kits will also be key to widespread adoption, particularly in price-sensitive regions.

Emerging Opportunities in Veterinary Rapid Test Industry

Emerging opportunities in the veterinary rapid test industry lie in the development of rapid tests for chronic diseases, such as diabetes and kidney disease, beyond infectious agents. The integration of AI and machine learning with rapid test readers offers potential for predictive diagnostics and personalized treatment plans. Expansion into point-of-care diagnostics for exotic pets and specialized animal populations presents a niche but growing market. Furthermore, the increasing demand for at-home veterinary testing solutions, driven by convenience and owner preferences, opens new avenues for direct-to-consumer veterinary diagnostics.

Leading Players in the Veterinary Rapid Test Industry Sector

- Heska Corporation

- IDEXX Laboratories Inc

- DiaSys Diagnostic Systems GmbH

- BioNote Inc

- Antech Diagnostics

- MEGACOR Veterinary Diagnostics

- Fassisi GmbH

- Biopanda Reagents Ltd

- Ring Biotechnology Co Ltd

- CorisBioConcept SPRL

- Biosynex Group

- Zoetis Inc

Key Milestones in Veterinary Rapid Test Industry Industry

- April 2024: VolitionRx Limited launched Antech's Nu.Q Vet Cancer Test in Europe and the United States, offering rapid, accurate, and economical cancer screening for dogs on the Element i+ Analyzer, with results in approximately six minutes.

- November 2023: Antech expanded its UK lab network by opening a new veterinary diagnostics laboratory in Warwick, United Kingdom, complementing its existing facilities.

Strategic Outlook for Veterinary Rapid Test Industry Market

The strategic outlook for the veterinary rapid test industry is exceptionally bright, characterized by continuous innovation and market expansion. Growth accelerators include the increasing demand for comprehensive veterinary diagnostics, the ongoing development of advanced rapid test readers, and the growing emphasis on preventative care for companion animals and livestock animals. Companies that can effectively leverage technological advancements, forge strategic partnerships, and address the evolving needs of veterinarians and pet owners will be well-positioned for sustained success. The market's trajectory indicates a substantial increase in the adoption of veterinary point-of-care testing, making it a cornerstone of modern animal healthcare.

Veterinary Rapid Test Industry Segmentation

-

1. Product Type

- 1.1. Rapid Test Kits

- 1.2. Rapid Test Readers

-

2. Application

- 2.1. Viral Diseases

- 2.2. Bacterial Diseases

- 2.3. Parasitic Diseases

- 2.4. Allergies

-

3. Animal Type

- 3.1. Companion Animals

- 3.2. Livestock Animals

Veterinary Rapid Test Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Veterinary Rapid Test Industry Regional Market Share

Geographic Coverage of Veterinary Rapid Test Industry

Veterinary Rapid Test Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Rapid Test Kits

- 5.1.2. Rapid Test Readers

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Viral Diseases

- 5.2.2. Bacterial Diseases

- 5.2.3. Parasitic Diseases

- 5.2.4. Allergies

- 5.3. Market Analysis, Insights and Forecast - by Animal Type

- 5.3.1. Companion Animals

- 5.3.2. Livestock Animals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Veterinary Rapid Test Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Rapid Test Kits

- 6.1.2. Rapid Test Readers

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Viral Diseases

- 6.2.2. Bacterial Diseases

- 6.2.3. Parasitic Diseases

- 6.2.4. Allergies

- 6.3. Market Analysis, Insights and Forecast - by Animal Type

- 6.3.1. Companion Animals

- 6.3.2. Livestock Animals

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Veterinary Rapid Test Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Rapid Test Kits

- 7.1.2. Rapid Test Readers

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Viral Diseases

- 7.2.2. Bacterial Diseases

- 7.2.3. Parasitic Diseases

- 7.2.4. Allergies

- 7.3. Market Analysis, Insights and Forecast - by Animal Type

- 7.3.1. Companion Animals

- 7.3.2. Livestock Animals

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Veterinary Rapid Test Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Rapid Test Kits

- 8.1.2. Rapid Test Readers

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Viral Diseases

- 8.2.2. Bacterial Diseases

- 8.2.3. Parasitic Diseases

- 8.2.4. Allergies

- 8.3. Market Analysis, Insights and Forecast - by Animal Type

- 8.3.1. Companion Animals

- 8.3.2. Livestock Animals

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Veterinary Rapid Test Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Rapid Test Kits

- 9.1.2. Rapid Test Readers

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Viral Diseases

- 9.2.2. Bacterial Diseases

- 9.2.3. Parasitic Diseases

- 9.2.4. Allergies

- 9.3. Market Analysis, Insights and Forecast - by Animal Type

- 9.3.1. Companion Animals

- 9.3.2. Livestock Animals

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Veterinary Rapid Test Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Rapid Test Kits

- 10.1.2. Rapid Test Readers

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Viral Diseases

- 10.2.2. Bacterial Diseases

- 10.2.3. Parasitic Diseases

- 10.2.4. Allergies

- 10.3. Market Analysis, Insights and Forecast - by Animal Type

- 10.3.1. Companion Animals

- 10.3.2. Livestock Animals

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. South America Veterinary Rapid Test Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Rapid Test Kits

- 11.1.2. Rapid Test Readers

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Viral Diseases

- 11.2.2. Bacterial Diseases

- 11.2.3. Parasitic Diseases

- 11.2.4. Allergies

- 11.3. Market Analysis, Insights and Forecast - by Animal Type

- 11.3.1. Companion Animals

- 11.3.2. Livestock Animals

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Heska Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 IDEXX Laboratories Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DiaSys Diagnostic Systems GmbH

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BioNote Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Antech Diagnostics*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 MEGACOR Veterinary Diagnostics

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Fassisi GmbH

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Biopanda Reagents Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Ring Biotechnology Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 CorisBioConcept SPRL

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Biosynex Group

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Zoetis Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Heska Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Veterinary Rapid Test Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Veterinary Rapid Test Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 3: North America Veterinary Rapid Test Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Veterinary Rapid Test Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Veterinary Rapid Test Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Veterinary Rapid Test Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 7: North America Veterinary Rapid Test Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 8: North America Veterinary Rapid Test Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Veterinary Rapid Test Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Veterinary Rapid Test Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 11: Europe Veterinary Rapid Test Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 12: Europe Veterinary Rapid Test Industry Revenue (Million), by Application 2025 & 2033

- Figure 13: Europe Veterinary Rapid Test Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe Veterinary Rapid Test Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 15: Europe Veterinary Rapid Test Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 16: Europe Veterinary Rapid Test Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Veterinary Rapid Test Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Veterinary Rapid Test Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 19: Asia Pacific Veterinary Rapid Test Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 20: Asia Pacific Veterinary Rapid Test Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Asia Pacific Veterinary Rapid Test Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific Veterinary Rapid Test Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 23: Asia Pacific Veterinary Rapid Test Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 24: Asia Pacific Veterinary Rapid Test Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Veterinary Rapid Test Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Veterinary Rapid Test Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 27: Middle East and Africa Veterinary Rapid Test Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Middle East and Africa Veterinary Rapid Test Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Middle East and Africa Veterinary Rapid Test Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Veterinary Rapid Test Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 31: Middle East and Africa Veterinary Rapid Test Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 32: Middle East and Africa Veterinary Rapid Test Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Middle East and Africa Veterinary Rapid Test Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Veterinary Rapid Test Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 35: South America Veterinary Rapid Test Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 36: South America Veterinary Rapid Test Industry Revenue (Million), by Application 2025 & 2033

- Figure 37: South America Veterinary Rapid Test Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: South America Veterinary Rapid Test Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 39: South America Veterinary Rapid Test Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 40: South America Veterinary Rapid Test Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: South America Veterinary Rapid Test Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 4: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 6: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 7: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 8: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 13: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 15: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Italy Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Spain Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 23: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 25: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: China Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Japan Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: India Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Australia Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Korea Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 33: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 35: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: GCC Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Africa Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 40: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 41: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 42: Global Veterinary Rapid Test Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 43: Brazil Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Argentina Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Veterinary Rapid Test Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Rapid Test Industry?

The projected CAGR is approximately 8.70%.

2. Which companies are prominent players in the Veterinary Rapid Test Industry?

Key companies in the market include Heska Corporation, IDEXX Laboratories Inc, DiaSys Diagnostic Systems GmbH, BioNote Inc, Antech Diagnostics*List Not Exhaustive, MEGACOR Veterinary Diagnostics, Fassisi GmbH, Biopanda Reagents Ltd, Ring Biotechnology Co Ltd, CorisBioConcept SPRL, Biosynex Group, Zoetis Inc.

3. What are the main segments of the Veterinary Rapid Test Industry?

The market segments include Product Type, Application, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.88 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidences and Prevalence of Zoonotic Diseases; Increasing Awareness About Animal Health and Pet Ownership.

6. What are the notable trends driving market growth?

Rapid Test Kits Segment is Expected to Hold a Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Proper Infrastructure for Animal Healthcare Management; Concers Related to High Cost of Manufacturing.

8. Can you provide examples of recent developments in the market?

April 2024: VolitionRx Limited launched Antech's Nu.Q Vet Cancer Test in Europe and the United States. This Nu.Q Canine Cancer Test operates on the Element i+ Analyzer. It provides veterinarians with a rapid, accurate, and economical cancer screening tool for high-risk breeds and older dogs, with results in about six minutes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Rapid Test Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Rapid Test Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Rapid Test Industry?

To stay informed about further developments, trends, and reports in the Veterinary Rapid Test Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence