Key Insights

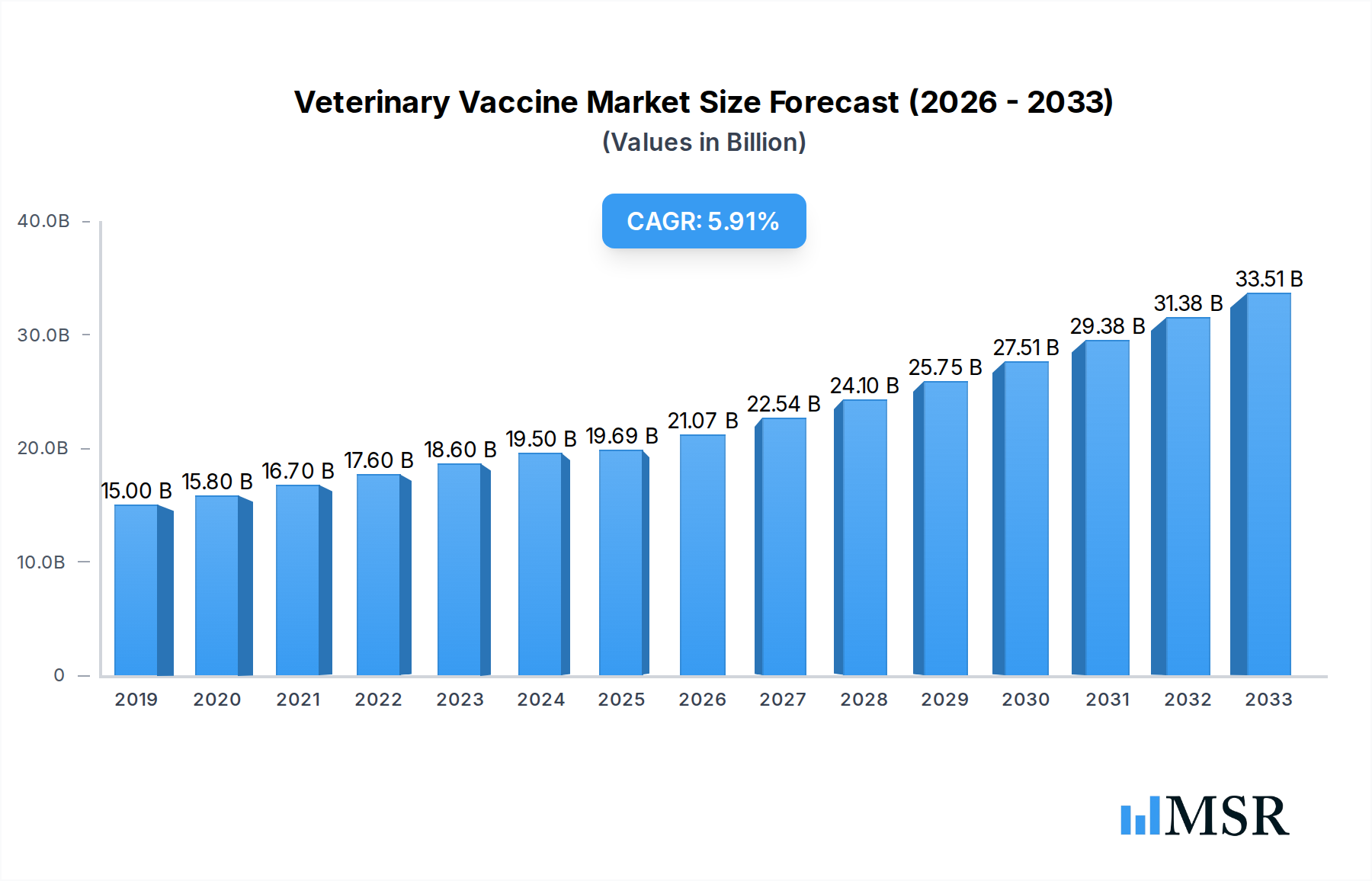

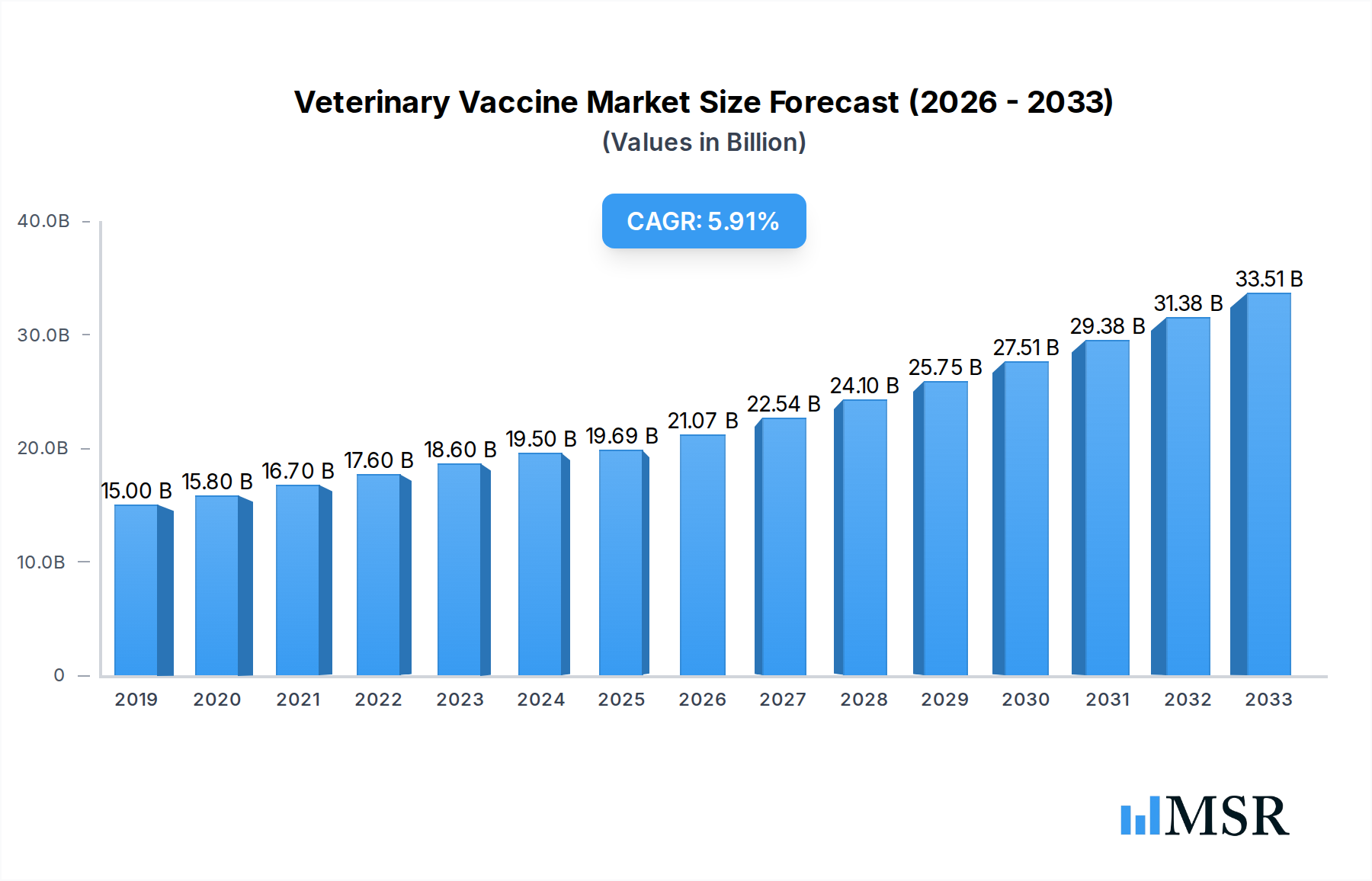

The global veterinary vaccine market is poised for robust expansion, with a market size of $19,690 million in 2025 and a projected CAGR of 6.9% through 2033. This significant growth is underpinned by a confluence of factors including the increasing demand for animal protein, a rising prevalence of zoonotic diseases that necessitate vaccination for both animal and human health, and a growing pet ownership trend globally. The companion animal segment, in particular, is a strong contributor, driven by pet humanization and increased expenditure on pet healthcare. Farm animals, essential for global food security, also represent a substantial and growing market for vaccines as livestock producers prioritize disease prevention to enhance productivity and ensure animal welfare. Key market drivers include advancements in vaccine technology, leading to more effective and safer products, and supportive government initiatives aimed at controlling animal diseases and improving public health. The market is characterized by a dynamic competitive landscape featuring major global players and emerging regional manufacturers, all contributing to innovation and market penetration.

Veterinary Vaccine Market Size (In Billion)

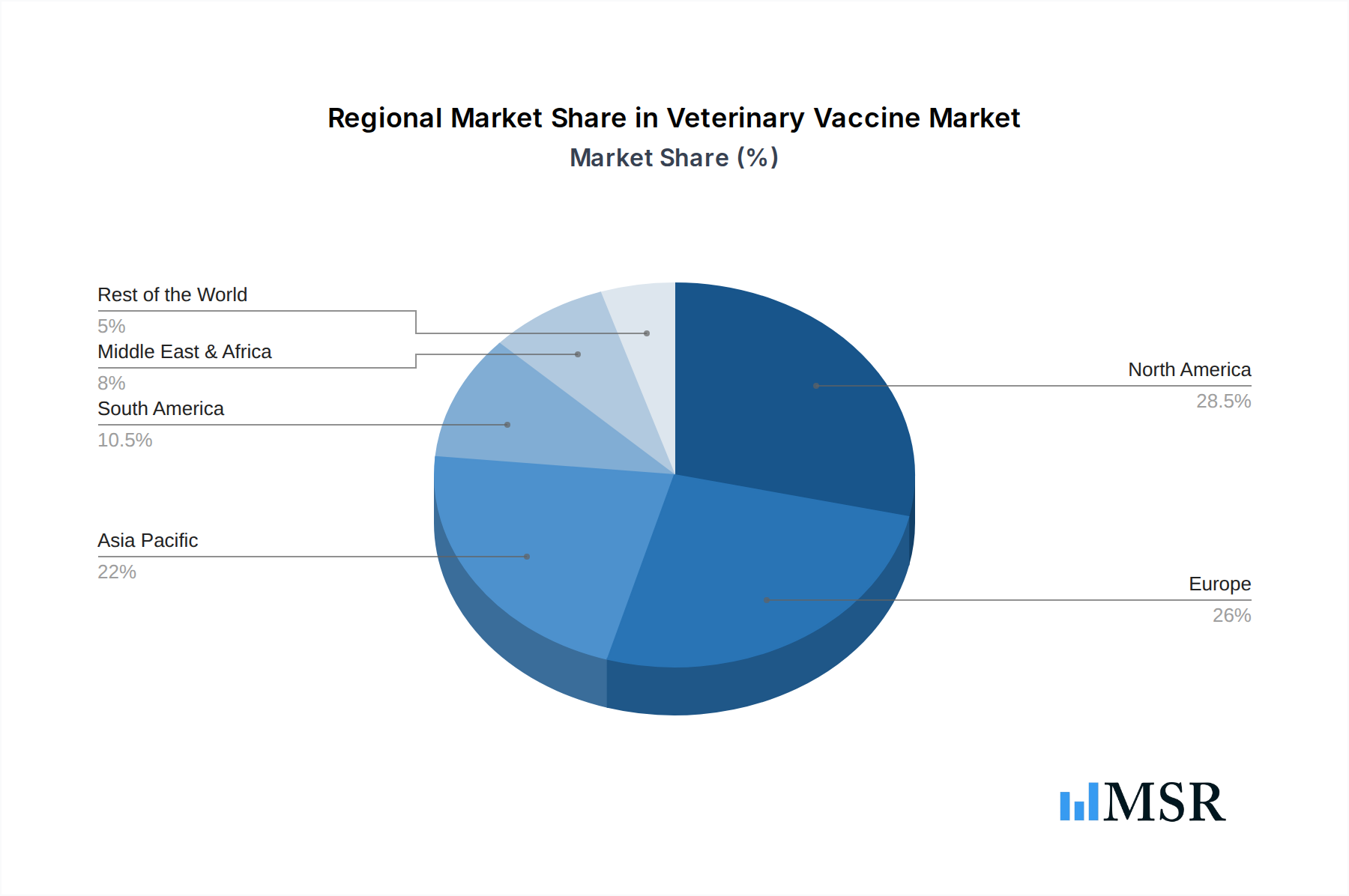

The veterinary vaccine market is segmented by application into Farm Animal and Companion Animal categories, and by type into Live Attenuated Vaccines, Inactivated Vaccines, and Other. Live attenuated vaccines offer strong immunity with fewer doses, while inactivated vaccines provide good safety profiles. The "Other" category likely encompasses newer vaccine technologies such as subunit and DNA vaccines, which are gaining traction due to their enhanced specificity and safety. Geographically, Asia Pacific, particularly China, is expected to witness the fastest growth, fueled by a large animal population and increasing investment in animal health infrastructure. North America and Europe remain significant markets due to well-established veterinary healthcare systems and high pet ownership rates. Restraints such as stringent regulatory approval processes and the high cost of vaccine development and manufacturing are present, but the overwhelming benefits of disease prevention and improved animal health are expected to outweigh these challenges, ensuring sustained market growth.

Veterinary Vaccine Company Market Share

Veterinary Vaccine Market Report: Growth, Innovation, and Competitive Landscape (2019-2033)

This comprehensive report delves into the dynamic global veterinary vaccine market, a critical sector supporting animal health and food security worldwide. Analyzing historical data from 2019–2024 and projecting future growth through 2033, with a base and estimated year of 2025, this study provides actionable insights for industry stakeholders. The market is characterized by significant innovation, evolving regulatory landscapes, and increasing demand for both farm animal and companion animal health solutions. The report identifies key growth drivers, emerging opportunities, and competitive strategies of leading global players, offering a strategic outlook for sustainable market expansion. The estimated market size is in the hundreds of millions, with projected growth exceeding billions over the forecast period.

Veterinary Vaccine Market Concentration & Dynamics

The global veterinary vaccine market exhibits a moderate to high concentration, with a few dominant players holding significant market share. In 2025, the estimated market share of the top five companies is projected to be over 60%, reflecting substantial R&D investments and established distribution networks. Innovation ecosystems are thriving, driven by advancements in biotechnology, including the development of novel delivery systems and combination vaccines. Regulatory frameworks, while varying by region, are becoming more stringent, emphasizing efficacy, safety, and environmental impact. Substitute products, such as antibiotics and alternative therapies, pose a competitive challenge, though the inherent preventative benefits of vaccines maintain their market dominance. End-user trends are shifting towards increased demand for preventative healthcare in companion animals and a growing focus on herd immunity and disease eradication in farm animals. Mergers and acquisitions (M&A) activities have been a notable feature, with an estimated XX M&A deals in the historical period (2019-2024) and a projected XX deals during the forecast period (2025-2033), consolidating market power and expanding product portfolios.

- Market Concentration: Dominated by key global players with substantial market share.

- Innovation Ecosystems: Driven by advancements in biotechnology, novel vaccine platforms, and combination therapies.

- Regulatory Frameworks: Increasingly stringent, focusing on safety, efficacy, and environmental considerations.

- Substitute Products: Antibiotics and alternative therapies present competition, but preventative benefits of vaccines are paramount.

- End-User Trends: Growing demand for companion animal preventative care and farm animal herd health.

- M&A Activities: Strategic consolidations and portfolio expansions are ongoing.

Veterinary Vaccine Industry Insights & Trends

The veterinary vaccine industry is poised for robust growth, driven by several interconnected factors. The estimated market size in 2025 is valued at approximately $7,500 million, with a projected Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period (2025–2033), reaching an estimated $12,800 million by 2033. This expansion is fueled by a confluence of increasing global demand for animal protein, rising pet ownership and expenditure on companion animal healthcare, and a heightened awareness of zoonotic disease prevention. Technological disruptions are a significant catalyst, with ongoing research and development in areas such as mRNA vaccine technology, subunit vaccines, and DNA vaccines promising enhanced efficacy, safety, and reduced side effects. The application of artificial intelligence (AI) in vaccine design and development is also accelerating the discovery of novel antigens and optimizing formulation. Evolving consumer behaviors play a crucial role, with pet owners increasingly prioritizing preventative care, akin to human healthcare, and livestock producers recognizing the economic imperative of disease prevention to ensure herd health and productivity. The growing global population and the subsequent demand for food security further underscore the importance of a healthy livestock population, directly impacting the demand for veterinary vaccines. Furthermore, government initiatives and favorable reimbursement policies in various regions are supporting the uptake of vaccination programs, thereby contributing to market expansion. The emergence of novel infectious diseases and the constant threat of pathogen evolution necessitate continuous innovation and the development of new and improved vaccine solutions, creating a sustained demand for the veterinary vaccine market.

Key Markets & Segments Leading Veterinary Vaccine

The global veterinary vaccine market is segmented by application into Farm Animal and Companion Animal, and by type into Live Attenuated Vaccines, Inactivated Vaccines, and Other. The Farm Animal segment currently dominates the market, driven by the escalating global demand for animal protein and the critical need for disease prevention in commercial livestock operations. Economic growth in developing nations significantly fuels this dominance, as increased disposable incomes lead to higher consumption of meat, dairy, and eggs, necessitating larger and healthier livestock populations. The growing emphasis on food security and the economic losses associated with animal diseases further bolster the demand for vaccines in this segment.

- Farm Animal Application Dominance Drivers:

- Rising Global Protein Demand: Increased consumption of meat, dairy, and eggs worldwide.

- Economic Growth in Emerging Markets: Higher disposable incomes leading to greater animal product consumption.

- Food Security Imperative: National and global efforts to ensure a stable food supply.

- Economic Losses from Disease: High costs associated with outbreaks in livestock.

- Government Support & Subsidies: Initiatives promoting livestock health and productivity.

The Companion Animal segment is experiencing rapid growth, driven by increasing pet ownership, humanization of pets, and a greater willingness among owners to invest in their pets' health. This trend is particularly pronounced in developed economies, where pet care is viewed as an integral part of family well-being.

- Companion Animal Growth Drivers:

- Increasing Pet Ownership: A global rise in households owning pets.

- Humanization of Pets: Pets treated as family members, leading to increased healthcare spending.

- Owner Willingness to Spend: Higher disposable incomes allocated to pet healthcare.

- Focus on Preventative Care: Owners prioritizing vaccinations to prevent illness.

In terms of vaccine types, Live Attenuated Vaccines and Inactivated Vaccines are the most prevalent. Live attenuated vaccines offer strong and long-lasting immunity but can carry a risk of reversion to virulence. Inactivated vaccines are generally safer but may require adjuvants and multiple doses for optimal immunity. The "Other" category, encompassing subunit, recombinant, and DNA vaccines, is rapidly gaining traction due to their enhanced safety profiles and targeted immunogenicity. Technological advancements are driving innovation in this category, leading to more effective and versatile vaccine solutions.

Veterinary Vaccine Product Developments

The veterinary vaccine market is witnessing a surge in product developments, primarily focusing on enhanced efficacy, extended shelf life, and improved safety profiles. Innovations include the development of multi-valent vaccines, capable of protecting against multiple diseases with a single administration, thereby reducing animal stress and labor costs. Advancements in recombinant DNA technology and viral vector platforms are enabling the creation of highly specific vaccines that elicit targeted immune responses. The application of novel adjuvants and delivery systems, such as nanoparticles, is also improving vaccine potency and duration of immunity. These product innovations are crucial in addressing emerging infectious diseases and evolving pathogen resistance, providing veterinarians and animal owners with more effective tools for disease prevention and control.

Challenges in the Veterinary Vaccine Market

The veterinary vaccine market faces several significant challenges that can impede its growth and market penetration. Regulatory hurdles, including lengthy and complex approval processes for new vaccines in different geographical regions, can delay market entry and increase R&D costs. Supply chain disruptions, exacerbated by global events, can impact the availability of raw materials and the timely distribution of finished products, leading to stockouts and unmet demand. Intense competitive pressures from established players and emerging companies, coupled with pricing sensitivities in certain market segments, can squeeze profit margins. Furthermore, the economic vulnerability of some end-users, particularly small-scale farmers, can limit their ability to invest in comprehensive vaccination programs.

- Regulatory Hurdles: Complex and time-consuming approval processes.

- Supply Chain Vulnerabilities: Disruptions impacting raw materials and distribution.

- Competitive Pressures: Intense market competition and pricing challenges.

- Economic Sensitivity: Affordability constraints for certain user segments.

Forces Driving Veterinary Vaccine Growth

Several powerful forces are propelling the growth of the veterinary vaccine market. Technological advancements, particularly in biotechnology and immunology, are enabling the development of more effective, safer, and targeted vaccines. The increasing global demand for animal protein, driven by a rising human population, necessitates healthier and more productive livestock, thereby boosting vaccine demand. The growing trend of pet humanization and increased pet ownership worldwide is driving significant investment in companion animal healthcare, including preventative vaccinations. Favorable government policies, including subsidies for animal health programs and mandates for disease control, also play a crucial role. Moreover, the continuous threat of emerging and re-emerging infectious diseases, including zoonotic diseases, creates a constant need for novel and updated vaccine solutions.

Challenges in the Veterinary Vaccine Market

While significant growth is anticipated, the veterinary vaccine market also faces long-term growth catalysts that require strategic navigation. The ongoing evolution of pathogens necessitates continuous research and development to create vaccines that can effectively combat new strains and resistant variants. Strategic partnerships and collaborations between pharmaceutical companies, academic institutions, and research organizations are vital for accelerating innovation and knowledge sharing. Market expansion into underserved regions and the development of cost-effective vaccine solutions tailored to the needs of these markets represent significant opportunities. Furthermore, the increasing adoption of digital technologies, such as data analytics and AI in vaccine development and deployment, will streamline processes and enhance market reach.

Emerging Opportunities in Veterinary Vaccine

Emerging opportunities in the veterinary vaccine market are abundant, driven by evolving scientific understanding and shifting consumer preferences. The development of thermostable vaccines that do not require cold chain storage presents a significant opportunity to expand access in remote or resource-limited regions. The application of novel vaccine platforms, such as self-amplifying RNA (saRNA) and bacteriophage display, offers potential for faster development and improved immunogenicity. There is a growing demand for vaccines targeting non-infectious conditions, such as allergies and cancer, in companion animals. Furthermore, the integration of vaccination data with other animal health monitoring systems can create comprehensive disease management solutions, opening new avenues for service-based revenue streams. The focus on antimicrobial stewardship also indirectly drives vaccine demand, as effective vaccination reduces the reliance on antibiotics.

Leading Players in the Veterinary Vaccine Sector

- Merck

- Zoetis

- Boehringer Ingelheim

- Ceva

- CAHIC

- HVRI

- Ringpu Biology

- Yebio

- DHN

- WINSUN

- Elanco

- Virbac

- Jinyu Bio-Technology

- Medion

- CAVAC

- Kyoto Biken Laboratories

- FATRO

- Vaksindo

- Bio-Labs

- Avimex Animal Health

- MEVAC

- Biovac

- Atafen

- Dyntec

- RVSRI

Key Milestones in Veterinary Vaccine Industry

- 2019: Launch of novel combination vaccine for poultry, offering protection against multiple viral diseases.

- 2020: Significant investment in mRNA vaccine research for veterinary applications, showing promising preclinical results.

- 2021: Acquisition of a key biotechnology firm by a major player, expanding its portfolio in subunit vaccine technology.

- 2022: Approval of the first DNA vaccine for a specific canine disease in a major market.

- 2023: Increased focus on developing thermostable vaccines to improve accessibility in developing countries.

- 2024: Introduction of AI-driven platforms for accelerated vaccine antigen discovery.

Strategic Outlook for Veterinary Vaccine Market

The strategic outlook for the veterinary vaccine market remains exceptionally positive, driven by sustained demand and continuous innovation. Growth accelerators include the ongoing development of advanced vaccine technologies, such as subunit and mRNA vaccines, which offer enhanced safety and efficacy. Strategic partnerships and collaborations will be crucial for expanding market reach and accelerating product development. The increasing adoption of digital tools for disease surveillance and personalized vaccination strategies presents significant opportunities. Furthermore, the growing awareness of the link between animal and human health (One Health initiative) will continue to elevate the importance of veterinary vaccines in public health strategies. Companies that can effectively navigate regulatory landscapes, build robust supply chains, and cater to the evolving needs of both farm animal and companion animal sectors will be well-positioned for sustained growth and profitability in this vital market.

Veterinary Vaccine Segmentation

-

1. Application

- 1.1. Farm Animal

- 1.2. Companion Animal

-

2. Type

- 2.1. Live Attenuated Vaccines

- 2.2. Inactivated Vaccines

- 2.3. Other

Veterinary Vaccine Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Veterinary Vaccine Regional Market Share

Geographic Coverage of Veterinary Vaccine

Veterinary Vaccine REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Veterinary Vaccine Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Farm Animal

- 5.1.2. Companion Animal

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Live Attenuated Vaccines

- 5.2.2. Inactivated Vaccines

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Veterinary Vaccine Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Farm Animal

- 6.1.2. Companion Animal

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Live Attenuated Vaccines

- 6.2.2. Inactivated Vaccines

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Veterinary Vaccine Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Farm Animal

- 7.1.2. Companion Animal

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Live Attenuated Vaccines

- 7.2.2. Inactivated Vaccines

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Veterinary Vaccine Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Farm Animal

- 8.1.2. Companion Animal

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Live Attenuated Vaccines

- 8.2.2. Inactivated Vaccines

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Veterinary Vaccine Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Farm Animal

- 9.1.2. Companion Animal

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Live Attenuated Vaccines

- 9.2.2. Inactivated Vaccines

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Veterinary Vaccine Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Farm Animal

- 10.1.2. Companion Animal

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Live Attenuated Vaccines

- 10.2.2. Inactivated Vaccines

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Merck

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Zoetis

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Boehringer Ingelheim

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Ceva

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 CAHIC

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 HVRI

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ringpu Biology

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Yebio

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DHN

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 WINSUN

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Elanco

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Virbac

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Jinyu Bio-Technology

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Medion

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 CAVAC

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Kyoto Biken Laboratories

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 FATRO

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Vaksindo

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Bio-Labs

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Avimex Animal Health

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 MEVAC

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Biovac

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Atafen

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Dyntec

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 RVSRI

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.1 Merck

List of Figures

- Figure 1: Global Veterinary Vaccine Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Veterinary Vaccine Revenue (million), by Application 2025 & 2033

- Figure 3: North America Veterinary Vaccine Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Veterinary Vaccine Revenue (million), by Type 2025 & 2033

- Figure 5: North America Veterinary Vaccine Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Veterinary Vaccine Revenue (million), by Country 2025 & 2033

- Figure 7: North America Veterinary Vaccine Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Veterinary Vaccine Revenue (million), by Application 2025 & 2033

- Figure 9: South America Veterinary Vaccine Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Veterinary Vaccine Revenue (million), by Type 2025 & 2033

- Figure 11: South America Veterinary Vaccine Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Veterinary Vaccine Revenue (million), by Country 2025 & 2033

- Figure 13: South America Veterinary Vaccine Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Veterinary Vaccine Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Veterinary Vaccine Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Veterinary Vaccine Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Veterinary Vaccine Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Veterinary Vaccine Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Veterinary Vaccine Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Veterinary Vaccine Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Veterinary Vaccine Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Veterinary Vaccine Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Veterinary Vaccine Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Veterinary Vaccine Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Veterinary Vaccine Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Veterinary Vaccine Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Veterinary Vaccine Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Veterinary Vaccine Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Veterinary Vaccine Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Veterinary Vaccine Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Veterinary Vaccine Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Veterinary Vaccine Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Veterinary Vaccine Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Veterinary Vaccine Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Veterinary Vaccine Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Veterinary Vaccine Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Veterinary Vaccine Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Veterinary Vaccine Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Veterinary Vaccine Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Veterinary Vaccine Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Veterinary Vaccine Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Veterinary Vaccine Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Veterinary Vaccine Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Veterinary Vaccine Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Veterinary Vaccine Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Veterinary Vaccine Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Veterinary Vaccine Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Veterinary Vaccine Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Veterinary Vaccine Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Veterinary Vaccine Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Vaccine?

The projected CAGR is approximately 6.9%.

2. Which companies are prominent players in the Veterinary Vaccine?

Key companies in the market include Merck, Zoetis, Boehringer Ingelheim, Ceva, CAHIC, HVRI, Ringpu Biology, Yebio, DHN, WINSUN, Elanco, Virbac, Jinyu Bio-Technology, Medion, CAVAC, Kyoto Biken Laboratories, FATRO, Vaksindo, Bio-Labs, Avimex Animal Health, MEVAC, Biovac, Atafen, Dyntec, RVSRI.

3. What are the main segments of the Veterinary Vaccine?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 19690 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Vaccine," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Vaccine report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Vaccine?

To stay informed about further developments, trends, and reports in the Veterinary Vaccine, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence