Key Insights

The global veterinary vaccines market is poised for significant expansion, driven by increasing zoonotic disease prevalence, a surge in pet ownership, and a growing imperative for enhanced animal health and productivity. Advances in vaccine development, including novel adjuvants like liposomes and nanoparticles, are yielding more effective and safer immunizations. This innovation is supported by a deeper understanding of animal immunology and the creation of targeted vaccines for specific pathogens. Stringent animal health regulations further promote vaccination programs, especially in livestock, to mitigate disease outbreaks and economic losses. The market is segmented by vaccine type (including traditional and novel formulations), administration route, and animal type (livestock and companion animals), catering to diverse species and disease needs.

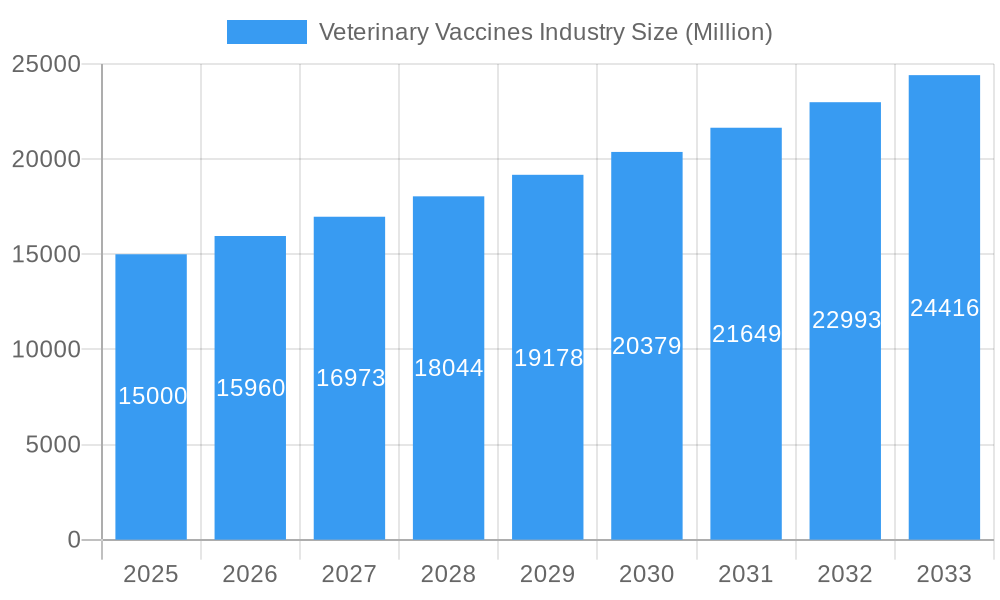

Veterinary Vaccines Industry Market Size (In Billion)

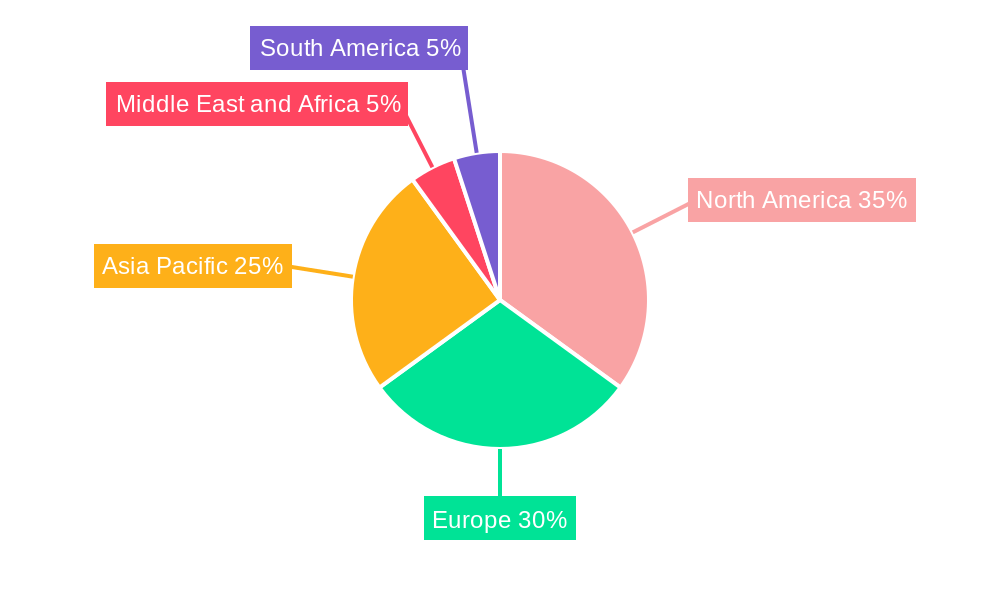

North America and Europe currently lead the market due to high pet ownership, robust regulatory frameworks, and developed veterinary infrastructure. However, the Asia-Pacific region presents substantial growth opportunities, fueled by expanding livestock populations and heightened awareness of animal health. The competitive landscape features major multinational pharmaceutical firms and specialized manufacturers, fostering innovation and cost-effectiveness. Strategic collaborations, mergers, and acquisitions are key to market expansion and portfolio growth. Key market indicators project a 7.2% CAGR, reaching a market size of $12.19 billion by 2025.

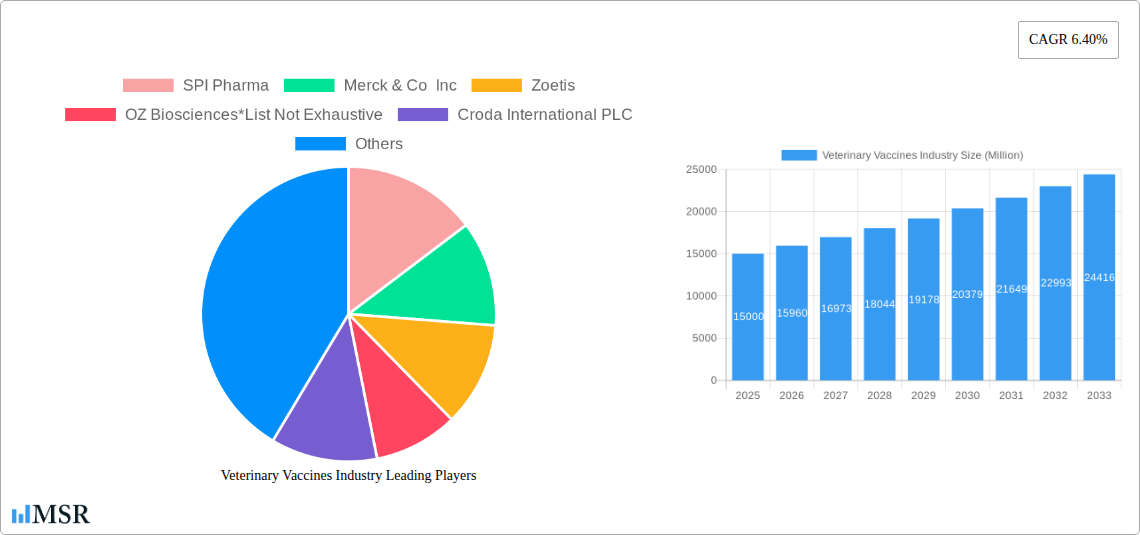

Veterinary Vaccines Industry Company Market Share

Challenges include high development and distribution costs, potential adverse reactions, and the emergence of antibiotic-resistant pathogens. Addressing these requires sustained R&D investment, improved vaccine accessibility in underserved regions, and cross-sector collaboration. The veterinary vaccines market outlook remains optimistic, with continued growth anticipated due to ongoing technological advancements and a global focus on animal well-being.

Veterinary Vaccines Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of the Veterinary Vaccines Industry, offering invaluable insights for stakeholders, investors, and industry professionals. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. The report covers a market valued at $XX Million in 2025, experiencing a Compound Annual Growth Rate (CAGR) of XX% during the forecast period.

Veterinary Vaccines Industry Market Concentration & Dynamics

The veterinary vaccines market is characterized by a moderately concentrated landscape, with key players like Zoetis, Merck & Co Inc, and Phibro Animal Health Corporation holding significant market share. However, the presence of numerous smaller companies and emerging players indicates a dynamic competitive environment. Innovation in adjuvant technology and vaccine delivery systems is a major driver, with companies investing heavily in R&D to develop next-generation vaccines. Regulatory frameworks, varying by region, play a crucial role, influencing product approvals and market access. Substitute products, such as alternative disease prevention strategies, pose a competitive threat, albeit limited due to the effectiveness and widespread acceptance of vaccines. End-user trends, such as increasing pet ownership and growing awareness of animal health, are boosting market demand, particularly in the companion animal segment. Significant M&A activity has been observed in recent years, with xx deals recorded between 2019 and 2024, further shaping market consolidation and technological advancement.

- Market Share: Zoetis: XX%, Merck & Co Inc: XX%, Phibro Animal Health: XX%, Others: XX%

- M&A Deal Count (2019-2024): XX

- Key Regulatory Bodies: (List relevant regulatory bodies by region)

Veterinary Vaccines Industry Industry Insights & Trends

The veterinary vaccines market is experiencing robust growth, driven primarily by the rising prevalence of animal diseases, increasing pet ownership globally, and government initiatives promoting animal health. Technological advancements, such as the development of novel adjuvants and improved vaccine delivery systems (e.g., intranasal vaccines), are further stimulating market expansion. Evolving consumer behaviors, including increased willingness to spend on pet healthcare and a preference for preventative healthcare, are creating opportunities for premium vaccines and innovative solutions. The market size reached an estimated $XX Million in 2025 and is projected to expand to $XX Million by 2033, indicating significant potential for growth. This expansion is fueled by the growing demand for effective and safe vaccines across livestock and companion animals.

Key Markets & Segments Leading Veterinary Vaccines Industry

The global veterinary vaccines market is dominated by the companion animal segment, driven by increasing pet ownership and higher per-animal spending on healthcare in developed regions such as North America and Europe. Within the "By Type" segment, Alum and Calcium Salts adjuvants currently hold the largest market share, but the demand for advanced adjuvants like liposomes and nanoparticles is increasing, reflecting a shift towards more effective and targeted vaccine formulations. The Intramuscular route of administration remains dominant, though there is increasing research and development of oral vaccines for enhanced convenience.

- Dominant Region: North America

- Dominant Segment (By Animal Type): Companion Animals

- Dominant Segment (By Type): Alum and Calcium Salts

- Dominant Segment (By Route of Administration): Intramuscular

- Drivers:

- Increasing pet ownership and humanization of pets

- Rising awareness of zoonotic diseases

- Government initiatives promoting animal welfare and disease control

- Economic growth and increased disposable income in emerging markets

- Advancements in vaccine technology

Veterinary Vaccines Industry Product Developments

Recent product innovations focus on developing safer, more effective, and convenient vaccines. This includes the use of novel adjuvants, such as those derived from amaranth oil (PhytoSquene), to enhance vaccine efficacy and reduce reliance on animal-derived components. The development of vaccines against emerging diseases, along with improved delivery methods and formulations, are also key areas of focus. These advancements provide companies with a significant competitive edge in the market, allowing them to cater to evolving consumer demands and regulatory requirements.

Challenges in the Veterinary Vaccines Industry Market

The veterinary vaccines market faces challenges such as stringent regulatory approvals, which can increase time-to-market and development costs. Supply chain disruptions, particularly concerning raw materials and manufacturing capabilities, can affect production and availability. Intense competition among established and emerging players requires continuous innovation and adaptation. These factors collectively impact the market's overall growth trajectory, requiring companies to implement robust strategies to navigate these hurdles. For example, regulatory delays for novel vaccines can delay market entry by XX months, impacting revenue by $XX Million.

Forces Driving Veterinary Vaccines Industry Growth

Technological advancements, such as the development of novel adjuvants and mRNA vaccines, are significantly contributing to market growth. Favorable economic conditions in many regions are increasing per capita spending on animal healthcare. Government regulations and policies promoting animal welfare and disease control further stimulate market expansion. The increasing prevalence of zoonotic diseases (diseases transmitted from animals to humans) also strengthens demand for effective vaccines.

Long-Term Growth Catalysts in the Veterinary Vaccines Industry

The long-term growth of the veterinary vaccines market will be fueled by continued innovation in vaccine technology, including personalized and targeted vaccines. Strategic partnerships and collaborations among companies, research institutions, and governments will accelerate the development and deployment of new vaccines. Expansion into emerging markets with rising animal populations and increased awareness of animal health will unlock significant growth opportunities.

Emerging Opportunities in Veterinary Vaccines Industry

Emerging opportunities exist in the development of vaccines for newly emerging animal diseases, as well as vaccines targeting specific animal populations or breeds. The increasing use of digital technologies, such as telemedicine and data analytics, offers the potential for improved vaccine distribution and disease surveillance. Furthermore, a growing demand for personalized medicine in veterinary care could lead to the development of tailored vaccines for individual animals based on their genetic makeup and health status.

Leading Players in the Veterinary Vaccines Industry Sector

- SPI Pharma

- Merck & Co Inc

- Zoetis

- OZ Biosciences

- Croda International PLC

- SEPPIC

- Invivogen

- Phibro Animal Health Corporation

- Bioveta AS

Key Milestones in Veterinary Vaccines Industry Industry

- December 2022: Evonik launched PhytoSquene, a non-animal-derived squalene for use in vaccine adjuvants. This significantly reduces reliance on animal-sourced materials and addresses ethical concerns.

- June 2022: ICAR-NRC launched animal vaccines containing inactivated SARS-CoV-2 (Delta) antigen, demonstrating a rapid response to emerging zoonotic disease threats.

Strategic Outlook for Veterinary Vaccines Industry Market

The veterinary vaccines market presents a compelling growth trajectory, driven by strong underlying factors such as increasing pet ownership, heightened awareness of animal health, and continuous technological advancements. Strategic opportunities for companies include investing in R&D to develop next-generation vaccines, exploring new markets, and forming strategic partnerships to expand their reach and market share. The future growth of this market hinges on successfully navigating regulatory hurdles and effectively addressing supply chain challenges while maintaining a keen focus on delivering innovative and effective vaccines.

Veterinary Vaccines Industry Segmentation

-

1. Type

- 1.1. Alum and Calcium Salts

- 1.2. Oil Emulsion Adjuvants

- 1.3. Liposomes and Archaeosomes

- 1.4. Nanoparticles and Microparticles

- 1.5. Other Types

-

2. Route of Administration

- 2.1. Oral

- 2.2. Intramuscular

- 2.3. Other Routes of Administration

-

3. Animal Type

- 3.1. Livestock

- 3.2. Companion Animal

Veterinary Vaccines Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Veterinary Vaccines Industry Regional Market Share

Geographic Coverage of Veterinary Vaccines Industry

Veterinary Vaccines Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Alum and Calcium Salts

- 5.1.2. Oil Emulsion Adjuvants

- 5.1.3. Liposomes and Archaeosomes

- 5.1.4. Nanoparticles and Microparticles

- 5.1.5. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Route of Administration

- 5.2.1. Oral

- 5.2.2. Intramuscular

- 5.2.3. Other Routes of Administration

- 5.3. Market Analysis, Insights and Forecast - by Animal Type

- 5.3.1. Livestock

- 5.3.2. Companion Animal

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Veterinary Vaccines Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Alum and Calcium Salts

- 6.1.2. Oil Emulsion Adjuvants

- 6.1.3. Liposomes and Archaeosomes

- 6.1.4. Nanoparticles and Microparticles

- 6.1.5. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Route of Administration

- 6.2.1. Oral

- 6.2.2. Intramuscular

- 6.2.3. Other Routes of Administration

- 6.3. Market Analysis, Insights and Forecast - by Animal Type

- 6.3.1. Livestock

- 6.3.2. Companion Animal

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Veterinary Vaccines Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Alum and Calcium Salts

- 7.1.2. Oil Emulsion Adjuvants

- 7.1.3. Liposomes and Archaeosomes

- 7.1.4. Nanoparticles and Microparticles

- 7.1.5. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Route of Administration

- 7.2.1. Oral

- 7.2.2. Intramuscular

- 7.2.3. Other Routes of Administration

- 7.3. Market Analysis, Insights and Forecast - by Animal Type

- 7.3.1. Livestock

- 7.3.2. Companion Animal

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Veterinary Vaccines Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Alum and Calcium Salts

- 8.1.2. Oil Emulsion Adjuvants

- 8.1.3. Liposomes and Archaeosomes

- 8.1.4. Nanoparticles and Microparticles

- 8.1.5. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Route of Administration

- 8.2.1. Oral

- 8.2.2. Intramuscular

- 8.2.3. Other Routes of Administration

- 8.3. Market Analysis, Insights and Forecast - by Animal Type

- 8.3.1. Livestock

- 8.3.2. Companion Animal

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Veterinary Vaccines Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Alum and Calcium Salts

- 9.1.2. Oil Emulsion Adjuvants

- 9.1.3. Liposomes and Archaeosomes

- 9.1.4. Nanoparticles and Microparticles

- 9.1.5. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Route of Administration

- 9.2.1. Oral

- 9.2.2. Intramuscular

- 9.2.3. Other Routes of Administration

- 9.3. Market Analysis, Insights and Forecast - by Animal Type

- 9.3.1. Livestock

- 9.3.2. Companion Animal

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Veterinary Vaccines Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Alum and Calcium Salts

- 10.1.2. Oil Emulsion Adjuvants

- 10.1.3. Liposomes and Archaeosomes

- 10.1.4. Nanoparticles and Microparticles

- 10.1.5. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Route of Administration

- 10.2.1. Oral

- 10.2.2. Intramuscular

- 10.2.3. Other Routes of Administration

- 10.3. Market Analysis, Insights and Forecast - by Animal Type

- 10.3.1. Livestock

- 10.3.2. Companion Animal

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South America Veterinary Vaccines Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Alum and Calcium Salts

- 11.1.2. Oil Emulsion Adjuvants

- 11.1.3. Liposomes and Archaeosomes

- 11.1.4. Nanoparticles and Microparticles

- 11.1.5. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Route of Administration

- 11.2.1. Oral

- 11.2.2. Intramuscular

- 11.2.3. Other Routes of Administration

- 11.3. Market Analysis, Insights and Forecast - by Animal Type

- 11.3.1. Livestock

- 11.3.2. Companion Animal

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SPI Pharma

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck & Co Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Zoetis

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 OZ Biosciences*List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Croda International PLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SEPPIC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Invivogen

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Phibro Animal Health Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bioveta AS

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 SPI Pharma

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Veterinary Vaccines Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Veterinary Vaccines Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Veterinary Vaccines Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Veterinary Vaccines Industry Revenue (billion), by Route of Administration 2025 & 2033

- Figure 5: North America Veterinary Vaccines Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 6: North America Veterinary Vaccines Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 7: North America Veterinary Vaccines Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 8: North America Veterinary Vaccines Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Veterinary Vaccines Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Veterinary Vaccines Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: Europe Veterinary Vaccines Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Veterinary Vaccines Industry Revenue (billion), by Route of Administration 2025 & 2033

- Figure 13: Europe Veterinary Vaccines Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 14: Europe Veterinary Vaccines Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 15: Europe Veterinary Vaccines Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 16: Europe Veterinary Vaccines Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Veterinary Vaccines Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Veterinary Vaccines Industry Revenue (billion), by Type 2025 & 2033

- Figure 19: Asia Pacific Veterinary Vaccines Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Veterinary Vaccines Industry Revenue (billion), by Route of Administration 2025 & 2033

- Figure 21: Asia Pacific Veterinary Vaccines Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 22: Asia Pacific Veterinary Vaccines Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 23: Asia Pacific Veterinary Vaccines Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 24: Asia Pacific Veterinary Vaccines Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Veterinary Vaccines Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Veterinary Vaccines Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Veterinary Vaccines Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Veterinary Vaccines Industry Revenue (billion), by Route of Administration 2025 & 2033

- Figure 29: Middle East and Africa Veterinary Vaccines Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 30: Middle East and Africa Veterinary Vaccines Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 31: Middle East and Africa Veterinary Vaccines Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 32: Middle East and Africa Veterinary Vaccines Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: Middle East and Africa Veterinary Vaccines Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Veterinary Vaccines Industry Revenue (billion), by Type 2025 & 2033

- Figure 35: South America Veterinary Vaccines Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: South America Veterinary Vaccines Industry Revenue (billion), by Route of Administration 2025 & 2033

- Figure 37: South America Veterinary Vaccines Industry Revenue Share (%), by Route of Administration 2025 & 2033

- Figure 38: South America Veterinary Vaccines Industry Revenue (billion), by Animal Type 2025 & 2033

- Figure 39: South America Veterinary Vaccines Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 40: South America Veterinary Vaccines Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America Veterinary Vaccines Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Veterinary Vaccines Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Veterinary Vaccines Industry Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 3: Global Veterinary Vaccines Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 4: Global Veterinary Vaccines Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Veterinary Vaccines Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Veterinary Vaccines Industry Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 7: Global Veterinary Vaccines Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 8: Global Veterinary Vaccines Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Mexico Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Veterinary Vaccines Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: Global Veterinary Vaccines Industry Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 14: Global Veterinary Vaccines Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 15: Global Veterinary Vaccines Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Germany Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: France Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Italy Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Spain Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Veterinary Vaccines Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Global Veterinary Vaccines Industry Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 24: Global Veterinary Vaccines Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 25: Global Veterinary Vaccines Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: China Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: India Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Australia Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Korea Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Veterinary Vaccines Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 33: Global Veterinary Vaccines Industry Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 34: Global Veterinary Vaccines Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 35: Global Veterinary Vaccines Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: GCC Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Africa Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Global Veterinary Vaccines Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 40: Global Veterinary Vaccines Industry Revenue billion Forecast, by Route of Administration 2020 & 2033

- Table 41: Global Veterinary Vaccines Industry Revenue billion Forecast, by Animal Type 2020 & 2033

- Table 42: Global Veterinary Vaccines Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 43: Brazil Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Argentina Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Veterinary Vaccines Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Vaccines Industry?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the Veterinary Vaccines Industry?

Key companies in the market include SPI Pharma, Merck & Co Inc, Zoetis, OZ Biosciences*List Not Exhaustive, Croda International PLC, SEPPIC, Invivogen, Phibro Animal Health Corporation, Bioveta AS.

3. What are the main segments of the Veterinary Vaccines Industry?

The market segments include Type, Route of Administration, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.19 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Use of Adjuvants in Vaccines; Increasing Livestock Population and Associated Diseases; High Incidence of Diseases.

6. What are the notable trends driving market growth?

Companion Animal Segment is Expected to Witness Considerable Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

High Toxicity and Side Effects of Adjuvants.

8. Can you provide examples of recent developments in the market?

In December 2022, Evonik launched non-animal-derived squalene suitable for vaccines and other pharmaceutical applications. PhytoSquene is the first known amaranth oil-derived squalene for use in adjuvants in parenteral dosage forms.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Vaccines Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Vaccines Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Vaccines Industry?

To stay informed about further developments, trends, and reports in the Veterinary Vaccines Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence