Key Insights

The Australian plant-based protein market is set for substantial growth, forecasted to reach AUD 149.52 million by 2025, with a CAGR of 5.39%. This expansion is fueled by shifting consumer demands for healthier and sustainable dietary options, driven by increased health consciousness and environmental awareness regarding traditional animal agriculture. The "Food and Beverages" segment, including plant-based dairy and meat alternatives, is a key driver, alongside the growing "Supplements" sector for sports nutrition and specialized diets. Technological advancements in ingredient formulation are improving the taste, texture, and nutritional value of plant-based protein products, further stimulating demand.

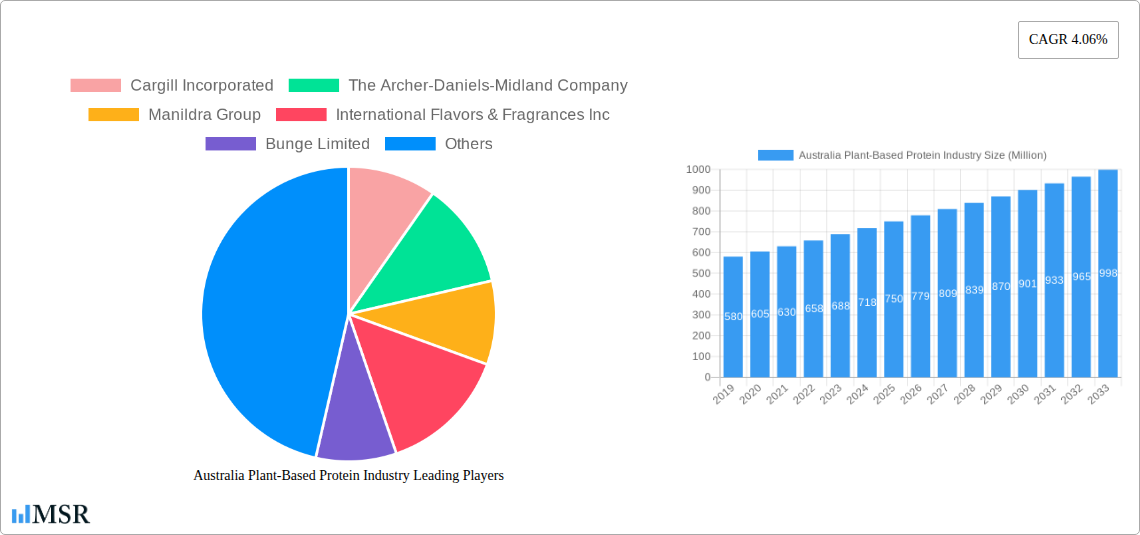

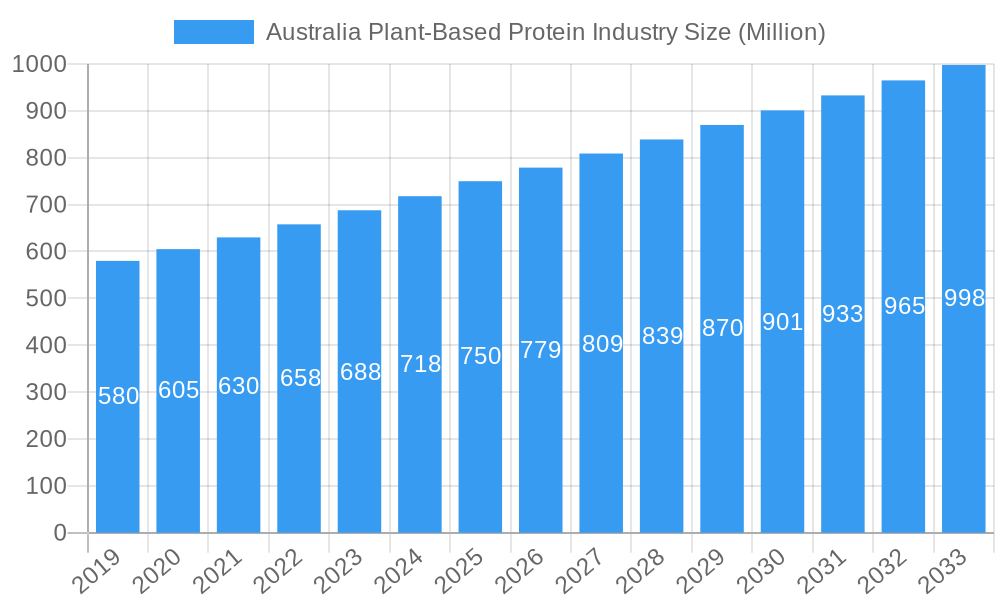

Australia Plant-Based Protein Industry Market Size (In Million)

Key trends influencing market dynamics include the adoption of novel protein sources such as pea and hemp, valued for their nutritional and functional benefits. Product innovation, from plant-based meats and cheeses to fortified beverages, is enhancing consumer choice and availability. Potential market restraints include the perception of higher pricing compared to conventional protein sources and challenges in replicating sensory experiences across all product types. Nevertheless, the Australian plant-based protein industry is on a robust growth path, propelled by the increasing prevalence of flexitarian, vegetarian, and vegan diets, supported by a wide array of protein types and diverse end-user applications.

Australia Plant-Based Protein Industry Company Market Share

Unveiling the Australia Plant-Based Protein Industry: A Comprehensive Market Analysis (2019-2033)

Report Description:

Dive deep into the booming Australia plant-based protein market with this definitive industry report. Spanning the historical period of 2019-2024 and forecasting through 2033, this analysis provides unparalleled insights into the dynamics, trends, and future potential of Australia's rapidly expanding plant-based protein industry. With a base year of 2025 and an estimated year also of 2025, this report offers timely and actionable intelligence for food and beverage manufacturers, supplement producers, animal feed companies, cosmetic brands, investors, and industry stakeholders seeking to capitalize on the surging demand for sustainable and healthy protein alternatives. Discover the key protein types like hemp protein, pea protein, soy protein, and rice protein, analyze their application across diverse end-users including meat alternatives, dairy alternatives, sports nutrition, and animal feed, and understand the impact of pivotal industry developments such as strategic investments and R&D center launches. This report is your essential guide to navigating and thriving in the Australian plant-based protein sector.

Australia Plant-Based Protein Industry Market Concentration & Dynamics

The Australia plant-based protein market is characterized by a moderate to high level of concentration, with a few key players dominating significant market share. Innovation is a critical driver, fueled by extensive research and development within both established multinational corporations and emerging Australian companies. Regulatory frameworks are evolving, generally supportive of the growing health and sustainability trends associated with plant-based diets. Substitute products, primarily traditional animal-based proteins, still hold a substantial market presence, but the gap is rapidly narrowing. End-user trends are overwhelmingly positive, with increasing consumer preference for plant-derived ingredients across all sectors. Mergers and acquisitions (M&A) activity is a notable dynamic, indicating a consolidation phase and strategic expansion by leading companies.

- Market Share: Leading players hold an estimated 60-70% of the market share, with significant growth potential for smaller, specialized companies.

- M&A Deal Counts: The historical period (2019-2024) has seen an average of 3-5 significant M&A deals annually, signaling increasing industry consolidation and investment.

- Innovation Ecosystems: Strong collaboration between research institutions and industry players is fostering rapid product development and technological advancements.

Australia Plant-Based Protein Industry Industry Insights & Trends

The Australia plant-based protein market is experiencing robust growth, driven by a confluence of factors including heightened consumer awareness of health and wellness, environmental sustainability concerns, and ethical considerations surrounding animal welfare. The projected market size for 2025 is estimated at approximately $1.5 Billion AUD, with an impressive Compound Annual Growth Rate (CAGR) of 12.5% anticipated from 2025 to 2033. Technological disruptions, such as advancements in protein extraction and processing, are enabling the creation of more palatable and functional plant-based ingredients, addressing historical taste and texture challenges. Evolving consumer behaviors are central to this expansion, with a significant shift towards flexitarianism, vegetarianism, and veganism across all age demographics. The demand for clean-label products and transparency in sourcing further influences market trends, pushing manufacturers to prioritize high-quality, recognizable ingredients. This sustained growth trajectory is underpinned by government initiatives promoting sustainable agriculture and food innovation, as well as a growing understanding of the nutritional benefits of plant-derived proteins, particularly for specific dietary needs such as sports nutrition and infant formula. The increasing availability and variety of plant-based protein sources are making them more accessible and appealing to a broader consumer base, further solidifying their position as a mainstream dietary choice.

Key Markets & Segments Leading Australia Plant-Based Protein Industry

The Australia plant-based protein industry is witnessing dominant growth across several key segments and protein types. Pea protein and soy protein currently lead the market in terms of volume and application breadth, driven by their versatility, cost-effectiveness, and established presence in various food and beverage categories.

Protein Type Dominance:

- Pea Protein: Its high protein content, neutral flavor profile, and excellent emulsifying properties make it a favored ingredient in meat alternative products, dairy and dairy alternative products, and sport/performance nutrition supplements. Economic growth in the health and wellness sector directly fuels its demand.

- Soy Protein: A long-standing staple, soy protein continues to hold significant market share in food and beverages, particularly in bakery, meat alternative products, and dairy alternative products. Its affordability and established supply chain contribute to its sustained popularity.

- Hemp Protein: Growing in popularity due to its complete amino acid profile and nutritional benefits, hemp protein is carving out a niche in supplements and health-conscious food and beverage applications. Infrastructure development supporting local hemp cultivation is a key driver.

- Rice Protein: Increasingly used as a hypoallergenic alternative, rice protein is gaining traction in baby food and infant formula, and sport/performance nutrition. Advancements in processing technology are enhancing its digestibility and functional properties.

- Other Plant Proteins (e.g., Fava Bean, Lentil): Emerging protein sources are gaining traction, driven by innovation and a desire for diversification. Investments in agricultural research and development are crucial for their expansion.

End-User Segment Dominance:

- Food and Beverages: This is the largest and most dynamic segment, encompassing a wide array of sub-categories.

- Meat/Poultry/Seafood and Meat Alternative Products: This sub-segment is experiencing explosive growth, driven by consumer demand for sustainable and ethical alternatives. Innovation in taste, texture, and nutritional profile is paramount.

- Dairy and Dairy Alternative Products: The surge in plant-based milk, yogurt, and cheese alternatives is a major growth engine. Consumer preferences for non-dairy options are a primary driver.

- Bakery and Snacks: Plant-based proteins are being incorporated to enhance nutritional value and cater to health-conscious consumers seeking protein-rich options.

- Supplements: This segment is a significant growth area, particularly for Sport/Performance Nutrition. Consumers are actively seeking protein powders and bars to support athletic performance and recovery. Elderly Nutrition and Medical Nutrition also represent a growing market as the population ages.

- Animal Feed: While a traditional application, the demand for plant-based proteins in animal feed is evolving with a focus on more sustainable and digestible options.

Australia Plant-Based Protein Industry Product Developments

Product innovation in the Australia plant-based protein industry is rapidly evolving. Manufacturers are focusing on developing protein isolates and concentrates with improved functionality, taste, and texture. Key advancements include the development of novel extraction techniques for underutilized plant sources like fava beans and lentils, yielding high-purity protein ingredients. Applications are expanding beyond traditional meat and dairy alternatives to include innovative snacks, ready-to-eat meals, and functional beverages. The focus on clean-label formulations and allergen-free options provides a competitive edge, meeting growing consumer demand for transparency and specific dietary needs.

Challenges in the Australia Plant-Based Protein Industry Market

The Australia plant-based protein industry faces several challenges that could impede its rapid growth. Supply chain complexities and the need for consistent, high-quality sourcing of raw materials, particularly for newer plant protein types, remain a concern. Price parity with conventional animal proteins can also be a barrier for some consumer segments. Furthermore, regulatory hurdles related to novel food ingredients and labeling standards require careful navigation. The significant capital investment required for scaling up production facilities and competitive pressures from both domestic and international players necessitate strategic planning and efficient operations.

Forces Driving Australia Plant-Based Protein Industry Growth

Several powerful forces are driving the expansion of the Australia plant-based protein industry. Evolving consumer preferences for healthier, more sustainable, and ethically sourced food options are paramount. Technological advancements in protein extraction, processing, and formulation are leading to improved product quality and a wider range of applications. Government initiatives and support for the plant-based sector, including research funding and sustainability targets, are creating a favorable operating environment. The increasing investment from major food corporations and venture capital firms signals strong market confidence and a commitment to growth.

Challenges in the Australia Plant-Based Protein Industry Market

Long-term growth catalysts for the Australia plant-based protein industry lie in continued innovation and market expansion. Strategic partnerships between ingredient suppliers and food manufacturers will be crucial for developing next-generation products. Expanding into export markets will unlock significant growth potential. Furthermore, ongoing investment in research and development to overcome remaining taste, texture, and nutritional challenges will solidify plant-based proteins as mainstream choices. The development of a robust and resilient domestic supply chain for a wider variety of plant protein sources will also be a key enabler of sustained growth.

Emerging Opportunities in Australia Plant-Based Protein Industry

The Australia plant-based protein industry is ripe with emerging opportunities. The development of high-performance plant-based proteins for specialized applications, such as those requiring enhanced digestibility or specific amino acid profiles, presents a lucrative avenue. Exploring novel protein sources beyond the current leaders, such as algae or insect-derived proteins (where regulations permit), could open new market segments. The increasing demand for plant-based pet food and animal feed solutions offers substantial growth potential. Furthermore, leveraging Australia's reputation for high-quality agricultural produce to develop premium, traceable plant-based ingredients for international markets represents a significant opportunity.

Leading Players in the Australia Plant-Based Protein Industry Sector

- Cargill Incorporated

- The Archer-Daniels-Midland Company

- Manildra Group

- International Flavors & Fragrances Inc

- Bunge Limited

- Australian Plant Proteins Pty Ltd

- Axiom Foods Inc

- Ingredion Incorporated

- Koninklijke DSM N V

- Kerry Group plc

Key Milestones in Australia Plant-Based Protein Industry Industry

- May 2021: Kerry established a state-of-the-art Food Technology and Innovation Center of Excellence in Queensland, Australia, enhancing its regional R&D capabilities and serving as its new headquarters for Australia and New Zealand.

- April 2021: Bunge Ltd. invested approximately AUD 45.7 Million in Australian Plant Proteins (APP), facilitating the expansion of APP's production of plant protein isolates, including fava bean, yellow lentil, and red lentil isolate powders.

- February 2021: International Flavors & Fragrances (IFF) merged with DuPont's Nutrition & Biosciences division, significantly expanding its portfolio of plant-based proteins available in Australia and globally.

Strategic Outlook for Australia Plant-Based Protein Industry Market

The strategic outlook for the Australia plant-based protein market is exceptionally positive, with significant growth accelerators in play. Continued investment in product innovation focusing on enhanced sensory attributes and nutritional profiles will be key. Expanding the application range into categories like ready-to-drink beverages and functional foods will capture new consumer segments. Strategic partnerships and collaborations across the value chain, from agriculture to retail, will foster market penetration and brand loyalty. Furthermore, capitalizing on Australia's strong agricultural reputation to export high-value plant-based ingredients globally represents a substantial strategic opportunity for sustained market leadership.

Australia Plant-Based Protein Industry Segmentation

-

1. Protein Type

- 1.1. Hemp Protein

- 1.2. Pea Protein

- 1.3. Potato Protein

- 1.4. Rice Protein

- 1.5. Soy Protein

- 1.6. Wheat Protein

- 1.7. Other Plant Protein

-

2. End-User

- 2.1. Animal Feed

- 2.2. Personal Care and Cosmetics

-

2.3. Food and Beverages

- 2.3.1. Bakery

- 2.3.2. Breakfast Cereals

- 2.3.3. Condiments/Sauces

- 2.3.4. Confectionery

- 2.3.5. Dairy and Dairy Alternative Products

- 2.3.6. Meat/Poultry/Seafood and Meat Alternative Products

- 2.3.7. RTE/RTC Food Products

- 2.3.8. Snacks

-

2.4. Supplements

- 2.4.1. Baby Food and Infant Formula

- 2.4.2. Elderly Nutrition and Medical Nutrition

- 2.4.3. Sport/Performance Nutrition

Australia Plant-Based Protein Industry Segmentation By Geography

- 1. Australia

Australia Plant-Based Protein Industry Regional Market Share

Geographic Coverage of Australia Plant-Based Protein Industry

Australia Plant-Based Protein Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Vegan Food & Beverages Driving the Market; Intolerance and Allergies Associated with Animal Protein Products

- 3.3. Market Restrains

- 3.3.1. High Market Penetration of Animal Protein

- 3.4. Market Trends

- 3.4.1. Increasing Demand for Plant-based Food & Beverages

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Plant-Based Protein Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Protein Type

- 5.1.1. Hemp Protein

- 5.1.2. Pea Protein

- 5.1.3. Potato Protein

- 5.1.4. Rice Protein

- 5.1.5. Soy Protein

- 5.1.6. Wheat Protein

- 5.1.7. Other Plant Protein

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Animal Feed

- 5.2.2. Personal Care and Cosmetics

- 5.2.3. Food and Beverages

- 5.2.3.1. Bakery

- 5.2.3.2. Breakfast Cereals

- 5.2.3.3. Condiments/Sauces

- 5.2.3.4. Confectionery

- 5.2.3.5. Dairy and Dairy Alternative Products

- 5.2.3.6. Meat/Poultry/Seafood and Meat Alternative Products

- 5.2.3.7. RTE/RTC Food Products

- 5.2.3.8. Snacks

- 5.2.4. Supplements

- 5.2.4.1. Baby Food and Infant Formula

- 5.2.4.2. Elderly Nutrition and Medical Nutrition

- 5.2.4.3. Sport/Performance Nutrition

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Protein Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Cargill Incorporated

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 The Archer-Daniels-Midland Company

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Manildra Group

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 International Flavors & Fragrances Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Bunge Limited

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Australian Plant Proteins Pty Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Axiom Foods Inc

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Ingredion Incorporated

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Koninklijke DSM N V *List Not Exhaustive

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Kerry Group plc

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Cargill Incorporated

List of Figures

- Figure 1: Australia Plant-Based Protein Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Australia Plant-Based Protein Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Plant-Based Protein Industry Revenue million Forecast, by Protein Type 2020 & 2033

- Table 2: Australia Plant-Based Protein Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 3: Australia Plant-Based Protein Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Australia Plant-Based Protein Industry Revenue million Forecast, by Protein Type 2020 & 2033

- Table 5: Australia Plant-Based Protein Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 6: Australia Plant-Based Protein Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Plant-Based Protein Industry?

The projected CAGR is approximately 5.39%.

2. Which companies are prominent players in the Australia Plant-Based Protein Industry?

Key companies in the market include Cargill Incorporated, The Archer-Daniels-Midland Company, Manildra Group, International Flavors & Fragrances Inc, Bunge Limited, Australian Plant Proteins Pty Ltd, Axiom Foods Inc, Ingredion Incorporated, Koninklijke DSM N V *List Not Exhaustive, Kerry Group plc.

3. What are the main segments of the Australia Plant-Based Protein Industry?

The market segments include Protein Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 149.52 million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Vegan Food & Beverages Driving the Market; Intolerance and Allergies Associated with Animal Protein Products.

6. What are the notable trends driving market growth?

Increasing Demand for Plant-based Food & Beverages.

7. Are there any restraints impacting market growth?

High Market Penetration of Animal Protein.

8. Can you provide examples of recent developments in the market?

May 2021: Kerry made a significant announcement regarding the establishment of a state-of-the-art Food Technology and Innovation Center of Excellence in Queensland, Australia. This facility is poised to serve as Kerry's new headquarters for its operations in Australia and New Zealand. Concurrently, Kerry's existing facility in Sydney will continue to operate as a specialized research and development applications hub. With comprehensive capabilities, including pilot plants, cutting-edge laboratories, and advanced testing facilities, the newly inaugurated Kerry Australia and New Zealand Development and Application Centre in Brisbane has substantially bolstered Kerry's research and development capabilities within the region.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Plant-Based Protein Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Plant-Based Protein Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Plant-Based Protein Industry?

To stay informed about further developments, trends, and reports in the Australia Plant-Based Protein Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence