Key Insights

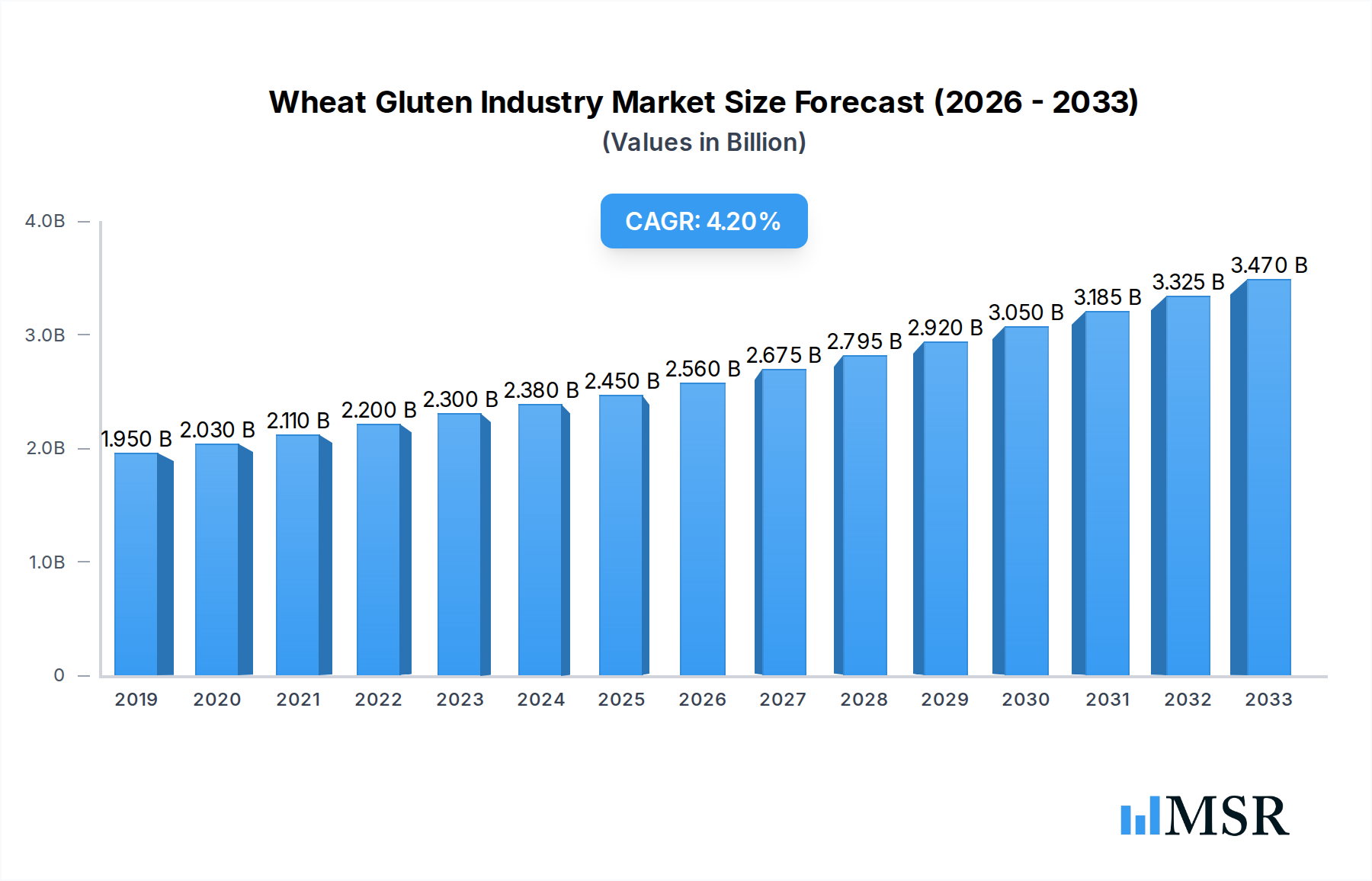

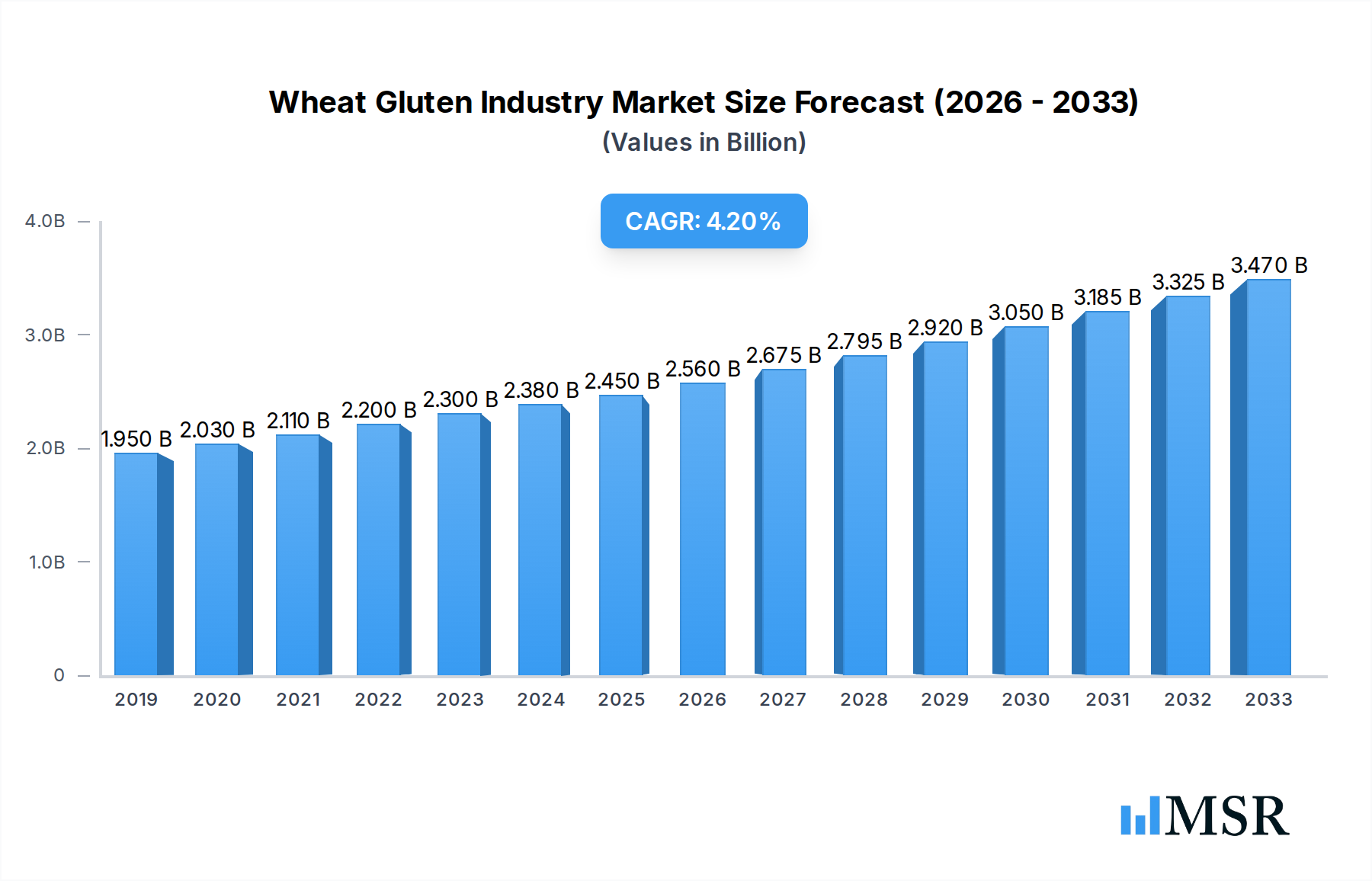

The global Wheat Gluten market is poised for substantial growth, projected to reach $2450 million by 2025. This expansion is fueled by a robust Compound Annual Growth Rate (CAGR) of 4.5% over the forecast period of 2025-2033. The increasing demand for high-protein food products, driven by growing health consciousness and the rising popularity of plant-based diets, is a primary catalyst. Wheat gluten, a vital ingredient in baked goods, offers enhanced texture, elasticity, and nutritional value, making it indispensable for manufacturers. Furthermore, its application in dietary supplements and animal feed is also contributing to market expansion. The market's growth trajectory is supported by technological advancements in gluten extraction and processing, leading to improved product quality and wider applications. Emerging economies, particularly in the Asia Pacific region, represent significant growth opportunities due to increasing disposable incomes and evolving dietary preferences.

Wheat Gluten Industry Market Size (In Billion)

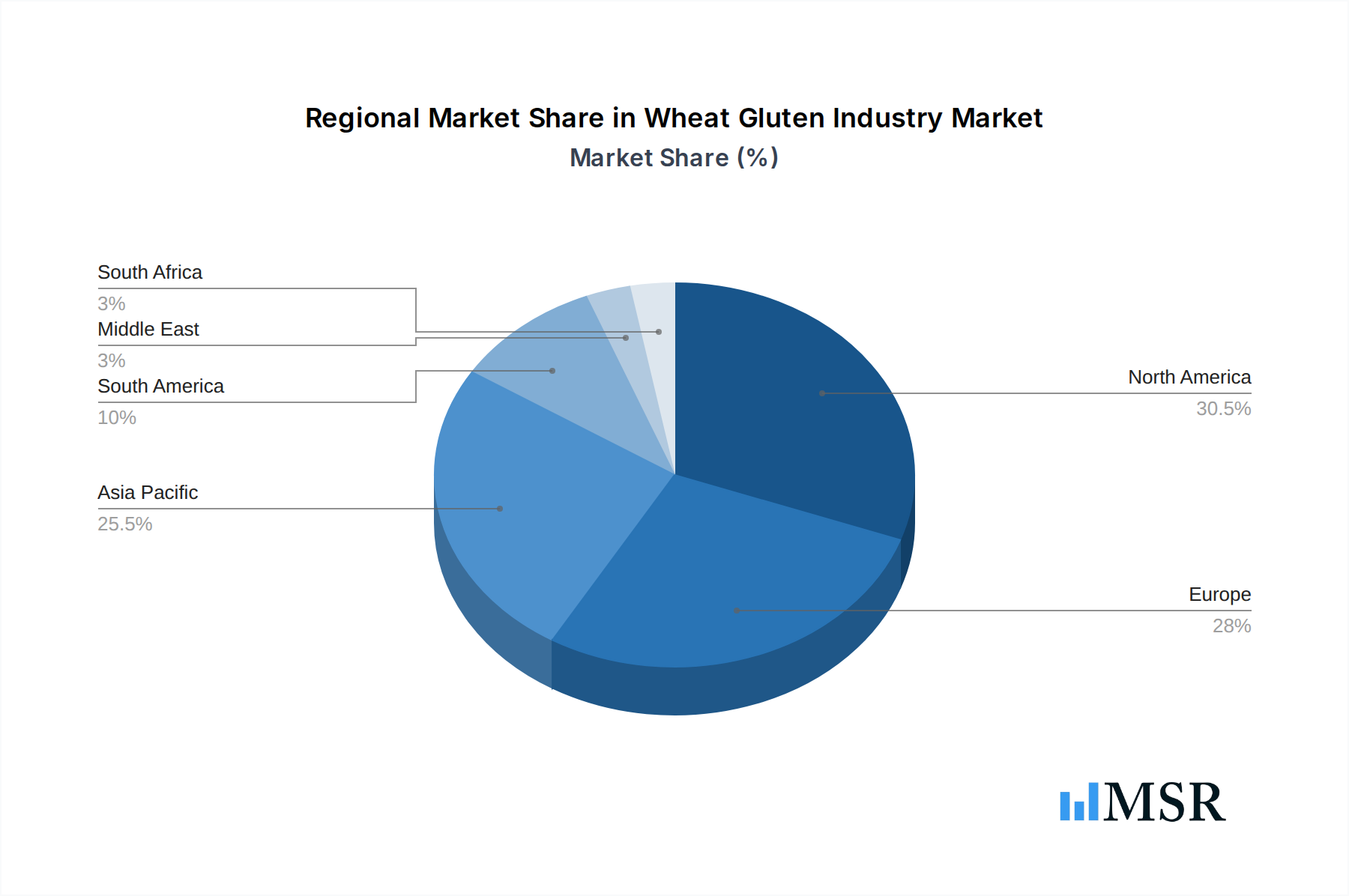

The market is characterized by diverse segmentation, with the Liquid and Powder forms catering to different industry needs. Key application segments include Bakery & Confectionery, which remains the dominant segment owing to the essential role of gluten in bread, pasta, and pastries. The Supplements segment is witnessing rapid growth as consumers seek convenient sources of protein. Animal feed applications are also expanding as the livestock industry increasingly recognizes the nutritional benefits of gluten. While the market exhibits strong growth drivers, certain restraints, such as the availability of gluten-free alternatives and fluctuating wheat prices, warrant strategic consideration by market players. Leading companies such as Cargill Inc., Ardent Mills LLC, and Anhui Ante Food are actively investing in research and development and expanding their production capacities to capitalize on these trends, particularly in key regions like North America and Europe, which are expected to maintain significant market share.

Wheat Gluten Industry Company Market Share

Unlock the full potential of the global wheat gluten market with this in-depth, SEO-optimized industry report. Covering the historical period from 2019 to 2024 and projecting growth through 2033, with a base and estimated year of 2025, this report provides critical insights for stakeholders in the vital wheat protein industry. We delve into the market size of wheat gluten, CAGR of wheat gluten, global wheat gluten market trends, and demand for wheat gluten, offering actionable intelligence on vital wheat ingredients, essential food proteins, and innovative food ingredients. Discover key growth drivers, emerging opportunities, and strategic outlooks to optimize wheat gluten sourcing, enhance bakery product formulations, and expand animal feed applications. This report is an indispensable tool for wheat gluten manufacturers, food ingredient suppliers, bakery and confectionery businesses, supplement companies, and animal feed producers seeking a competitive edge in this dynamic sector.

Wheat Gluten Industry Market Concentration & Dynamics

The global wheat gluten market exhibits a moderate to high degree of market concentration, with key players like Cargill Inc, Ardent Mills LLC, and Tereos holding significant market share. Innovation ecosystems are burgeoning, driven by advancements in processing technologies and the development of specialized gluten variants for diverse applications. Regulatory frameworks, primarily concerning food safety and labeling, are becoming increasingly stringent, impacting product development and market entry. Substitute products, such as plant-based proteins like pea and soy protein, present a competitive challenge, though wheat gluten's unique functional properties in bakery applications continue to ensure its dominance. End-user trends lean towards the demand for high-protein ingredients, gluten-free alternatives (paradoxically, driving interest in the functional properties of gluten itself for specific textures), and sustainable sourcing. Mergers and acquisitions (M&A) activities, while not excessively frequent, play a crucial role in consolidating market share and expanding geographical reach. Recent M&A activities have focused on companies with advanced wheat protein extraction capabilities and those serving niche markets. The market share of leading companies is estimated to be in the range of 10-25%, with the top 5 players accounting for over 50% of the global market. The number of significant M&A deals in the past five years is estimated to be between 10-20.

Wheat Gluten Industry Industry Insights & Trends

The wheat gluten industry is experiencing robust growth, driven by an escalating demand for high-quality proteins across various sectors. The global wheat gluten market size was valued at an estimated XX million USD in 2024 and is projected to reach approximately XX million USD by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025-2033. Market growth is underpinned by several key factors. Firstly, the booming bakery and confectionery industry remains the primary consumer, leveraging wheat gluten's exceptional viscoelastic properties to enhance dough structure, texture, and shelf-life in breads, pastries, and noodles. The growing popularity of processed foods and convenience meals further fuels this demand. Secondly, the animal feed sector is increasingly incorporating vital wheat gluten as a digestible protein source, improving animal health and growth performance, especially in aquaculture and poultry. Thirdly, the nutritional supplements market is witnessing a rise in demand for wheat gluten as a source of plant-based protein, catering to health-conscious consumers and the vegan demographic. Technological disruptions are centered on optimizing wheat gluten extraction processes, leading to higher purity and tailored functionalities. Advancements in enzymatic hydrolysis and modified gluten technologies are creating new avenues for specialized applications. Evolving consumer behaviors, such as the increasing awareness of health and wellness, coupled with the pursuit of sustainable and plant-based food options, are significant market shapers. While demand for gluten-free products is prevalent, the unique functional contribution of wheat gluten in specific food matrices continues to be appreciated, driving innovation in product development and formulation. The future of wheat gluten lies in its versatility and its ability to meet diverse nutritional and functional requirements.

Key Markets & Segments Leading Wheat Gluten Industry

The Asia Pacific region stands as the dominant force in the global wheat gluten industry, driven by its massive population, burgeoning food processing sector, and increasing disposable incomes. Within this region, China and India are leading consumption hubs. The dominant form of wheat gluten in this market is Powder, accounting for an estimated XX% of the total market share. This is primarily due to its ease of storage, transportation, and application in a wide array of food products. The bakery & confectionery segment is by far the largest application, contributing an estimated XX% to the global wheat gluten market revenue. This dominance is fueled by the vast consumption of bread, noodles, biscuits, and other baked goods, where wheat gluten plays a crucial role in texture, elasticity, and volume. Economic growth in emerging economies, coupled with rapid urbanization, has led to a significant increase in the demand for processed foods, further bolstering the bakery and confectionery sector's reliance on wheat gluten.

Drivers for Dominance in Asia Pacific:

- High Population Density: A large consumer base for staple food products.

- Rapid Urbanization: Increasing demand for convenient and processed food options.

- Growth of Food Processing Industry: Expansion of manufacturing capabilities for various food products.

- Increasing Disposable Incomes: Greater purchasing power for a wider range of food items.

- Cultural Significance of Wheat-Based Foods: Staple diets in many Asian countries heavily rely on wheat.

Dominance of Powder Form:

- Shelf Stability: Powdered gluten has a longer shelf life compared to liquid forms.

- Ease of Handling and Measurement: Simplifies manufacturing processes.

- Versatility in Applications: Can be easily incorporated into dry mixes and various formulations.

- Cost-Effectiveness: Often more economical in terms of logistics and storage.

The supplements segment is experiencing a significant growth trajectory, driven by the rising health consciousness and the demand for plant-based protein powders. While still smaller than bakery, its CAGR is projected to be higher in the coming years. The animal feed segment also represents a substantial market, with its growth linked to the expansion of the global meat and aquaculture industries.

Wheat Gluten Industry Product Developments

Product innovation in the wheat gluten industry is characterized by the development of specialized vital wheat gluten variants and improved processing techniques. Companies are focusing on creating gluten with enhanced functional properties, such as improved water-holding capacity, emulsification capabilities, and heat stability. For instance, the launch of gluten-free wheat starch with minimal gluten protein, like that by Lantmännen Biorefineries, caters to the growing demand for allergen-friendly options while still leveraging the underlying wheat processing expertise. Furthermore, the expansion of manufacturing facilities, such as by PureField Ingredients, signifies an increased capacity to meet the growing demand for sustainable wheat protein. These developments highlight a market that is not only expanding in volume but also in sophistication, offering tailored solutions for diverse industry needs and reinforcing the competitive edge of innovative players.

Challenges in the Wheat Gluten Industry Market

The wheat gluten industry faces several challenges that can impact its growth trajectory. Regulatory hurdles related to food safety standards and allergen labeling can increase compliance costs and necessitate product reformulation. Supply chain disruptions, exacerbated by geopolitical factors and climate change, can lead to price volatility and availability issues for raw wheat. Competitive pressures from alternative protein sources, such as soy and pea protein, and the increasing consumer preference for gluten-free diets present significant restraints. Quantifiably, these challenges can lead to an estimated 2-5% increase in production costs and a potential reduction in market share by 1-3% for companies unable to adapt their strategies.

Forces Driving Wheat Gluten Industry Growth

Several powerful forces are propelling the growth of the wheat gluten industry. Technological advancements in wheat gluten extraction and modification are enhancing its functionality and opening new application avenues. The escalating global demand for high-protein food ingredients due to growing health awareness and fitness trends is a major driver. Furthermore, the increasing adoption of wheat gluten in the animal feed industry as a cost-effective and highly digestible protein source is contributing significantly to market expansion. Regulatory support for the use of wheat-derived ingredients in various food applications, coupled with growing consumer acceptance of functional food ingredients, also provides a supportive environment for growth.

Challenges in the Wheat Gluten Industry Market

Long-term growth catalysts for the wheat gluten industry lie in strategic innovation and market expansion. Continued investment in research and development for novel wheat protein applications, beyond traditional food uses, such as in biodegradable plastics or biopharmaceuticals, presents a significant opportunity. Strategic partnerships and collaborations between wheat gluten suppliers and end-users can foster product development tailored to specific market needs. Furthermore, geographical expansion into untapped emerging markets with a growing middle class and increasing demand for processed foods will be crucial for sustained growth. The industry's ability to adapt to evolving dietary trends and proactively address consumer concerns surrounding gluten will also be a key determinant of its long-term success.

Emerging Opportunities in Wheat Gluten Industry

Emerging opportunities in the wheat gluten industry are manifold, driven by evolving consumer preferences and technological advancements. The growing demand for plant-based meat alternatives offers a significant avenue for wheat gluten's textural and binding properties. Innovations in hydrolyzed wheat gluten for enhanced digestibility and bioavailability are creating new markets in sports nutrition and functional foods. The development of specialized wheat gluten ingredients for pet food formulations, catering to specific dietary needs and preferences, also represents a growing niche. Furthermore, the increasing focus on sustainable agriculture and traceable supply chains presents an opportunity for companies to differentiate themselves by offering ethically sourced and environmentally friendly wheat gluten products.

Leading Players in the Wheat Gluten Industry Sector

- Ardent Mills LLC

- Bryan W Nash & Sons Limited

- Sungold Corporation

- Pioneer Industries Limited

- Anhui Ante Food

- Cargill Inc

- Crespel & Deiters GmbH

- Tereos

- Royal Ingredients Group

- MGP Ingredients

Key Milestones in Wheat Gluten Industry Industry

- March 2022: Lantmännen Biorefinery launched gluten-free wheat starch from Autumn wheat harvested in Sweden. This fine white powder, containing approximately 0.35% gluten protein, is designed for use in bakery products, addressing the demand for allergen-friendly ingredients.

- February 2022: PureField Ingredients announced the expansion of its wheat protein manufacturing facility in Russell, Kansas. This expansion increased production capacity by 50% to meet the rising global demand for sustainable wheat protein.

- December 2021: ICM Inc partnered with Summit Agricultural Group to construct a wheat protein ingredient plant in Phillipsburg, Kansas. This collaboration aims to bolster the production of wheat gluten ingredients for food and specialty feed applications.

Strategic Outlook for Wheat Gluten Industry Market

The strategic outlook for the wheat gluten industry is characterized by sustained growth driven by innovation and market diversification. Key growth accelerators include the continuous development of specialized gluten variants tailored for novel food applications, such as plant-based foods and convenience meals. Strategic opportunities lie in expanding the reach of wheat gluten into the burgeoning pet food and animal nutrition sectors, where its protein content is highly valued. Furthermore, a focus on enhancing the sustainability of wheat gluten production and transparent sourcing will be critical for capturing market share from environmentally conscious consumers. The industry is poised for robust expansion, with an emphasis on high-value, functional wheat gluten ingredients that cater to evolving global dietary needs and preferences.

Wheat Gluten Industry Segmentation

-

1. Form

- 1.1. Liquid

- 1.2. Powder

-

2. Application

- 2.1. Bakery & confectionery

- 2.2. Supplements

- 2.3. Animal feed

- 2.4. Others

Wheat Gluten Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Russia

- 2.5. Italy

- 2.6. Spain

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

- 5. Middle East

-

6. South Africa

- 6.1. Saudi Arabia

- 6.2. Rest of Middle East

Wheat Gluten Industry Regional Market Share

Geographic Coverage of Wheat Gluten Industry

Wheat Gluten Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Form

- 5.1.1. Liquid

- 5.1.2. Powder

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Bakery & confectionery

- 5.2.2. Supplements

- 5.2.3. Animal feed

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East

- 5.3.6. South Africa

- 5.1. Market Analysis, Insights and Forecast - by Form

- 6. Wheat Gluten Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Form

- 6.1.1. Liquid

- 6.1.2. Powder

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Bakery & confectionery

- 6.2.2. Supplements

- 6.2.3. Animal feed

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Form

- 7. North America Wheat Gluten Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Form

- 7.1.1. Liquid

- 7.1.2. Powder

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Bakery & confectionery

- 7.2.2. Supplements

- 7.2.3. Animal feed

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Form

- 8. Europe Wheat Gluten Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Form

- 8.1.1. Liquid

- 8.1.2. Powder

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Bakery & confectionery

- 8.2.2. Supplements

- 8.2.3. Animal feed

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Form

- 9. Asia Pacific Wheat Gluten Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Form

- 9.1.1. Liquid

- 9.1.2. Powder

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Bakery & confectionery

- 9.2.2. Supplements

- 9.2.3. Animal feed

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Form

- 10. South America Wheat Gluten Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Form

- 10.1.1. Liquid

- 10.1.2. Powder

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Bakery & confectionery

- 10.2.2. Supplements

- 10.2.3. Animal feed

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Form

- 11. Middle East Wheat Gluten Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Form

- 11.1.1. Liquid

- 11.1.2. Powder

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Bakery & confectionery

- 11.2.2. Supplements

- 11.2.3. Animal feed

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Form

- 12. South Africa Wheat Gluten Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Form

- 12.1.1. Liquid

- 12.1.2. Powder

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Bakery & confectionery

- 12.2.2. Supplements

- 12.2.3. Animal feed

- 12.2.4. Others

- 12.1. Market Analysis, Insights and Forecast - by Form

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Ardent Mills LLC

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Bryan W Nash & Sons Limited

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Sungold Corporation

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Pioneer Industries Limited

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Anhui Ante Food

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Cargill Inc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Crespel & Deiters GmbH*List Not Exhaustive

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Tereos

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Royal Ingredients Group

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 MGP Ingredients

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Ardent Mills LLC

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Wheat Gluten Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Wheat Gluten Industry Share (%) by Company 2025

List of Tables

- Table 1: Wheat Gluten Industry Revenue million Forecast, by Form 2020 & 2033

- Table 2: Wheat Gluten Industry Revenue million Forecast, by Application 2020 & 2033

- Table 3: Wheat Gluten Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Wheat Gluten Industry Revenue million Forecast, by Form 2020 & 2033

- Table 5: Wheat Gluten Industry Revenue million Forecast, by Application 2020 & 2033

- Table 6: Wheat Gluten Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Rest of North America Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Wheat Gluten Industry Revenue million Forecast, by Form 2020 & 2033

- Table 12: Wheat Gluten Industry Revenue million Forecast, by Application 2020 & 2033

- Table 13: Wheat Gluten Industry Revenue million Forecast, by Country 2020 & 2033

- Table 14: United Kingdom Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Germany Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: France Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Russia Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Italy Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Spain Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: Wheat Gluten Industry Revenue million Forecast, by Form 2020 & 2033

- Table 22: Wheat Gluten Industry Revenue million Forecast, by Application 2020 & 2033

- Table 23: Wheat Gluten Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: India Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: China Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Japan Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Australia Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Rest of Asia Pacific Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Wheat Gluten Industry Revenue million Forecast, by Form 2020 & 2033

- Table 30: Wheat Gluten Industry Revenue million Forecast, by Application 2020 & 2033

- Table 31: Wheat Gluten Industry Revenue million Forecast, by Country 2020 & 2033

- Table 32: Brazil Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: Argentina Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Rest of South America Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Wheat Gluten Industry Revenue million Forecast, by Form 2020 & 2033

- Table 36: Wheat Gluten Industry Revenue million Forecast, by Application 2020 & 2033

- Table 37: Wheat Gluten Industry Revenue million Forecast, by Country 2020 & 2033

- Table 38: Wheat Gluten Industry Revenue million Forecast, by Form 2020 & 2033

- Table 39: Wheat Gluten Industry Revenue million Forecast, by Application 2020 & 2033

- Table 40: Wheat Gluten Industry Revenue million Forecast, by Country 2020 & 2033

- Table 41: Saudi Arabia Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Middle East Wheat Gluten Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wheat Gluten Industry?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Wheat Gluten Industry?

Key companies in the market include Ardent Mills LLC, Bryan W Nash & Sons Limited, Sungold Corporation, Pioneer Industries Limited, Anhui Ante Food, Cargill Inc, Crespel & Deiters GmbH*List Not Exhaustive, Tereos, Royal Ingredients Group, MGP Ingredients.

3. What are the main segments of the Wheat Gluten Industry?

The market segments include Form, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 2450 million as of 2022.

5. What are some drivers contributing to market growth?

Wide Applications and Functionality; Demand For Gluten-Free Products.

6. What are the notable trends driving market growth?

Consumers Inclination Towards Healthy and Organic Food.

7. Are there any restraints impacting market growth?

Easy Availability of Economically Feasible Alternatives.

8. Can you provide examples of recent developments in the market?

In March 2022, Lantmännen Biorefinaries launched gluten-free wheat starch from Autumn wheat harvested in Sweden. The product is a fine white powder with a neutral taste that contains about 0.35% gluten protein. The product is launched for its use in bakery products.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wheat Gluten Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wheat Gluten Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wheat Gluten Industry?

To stay informed about further developments, trends, and reports in the Wheat Gluten Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence