Key Insights

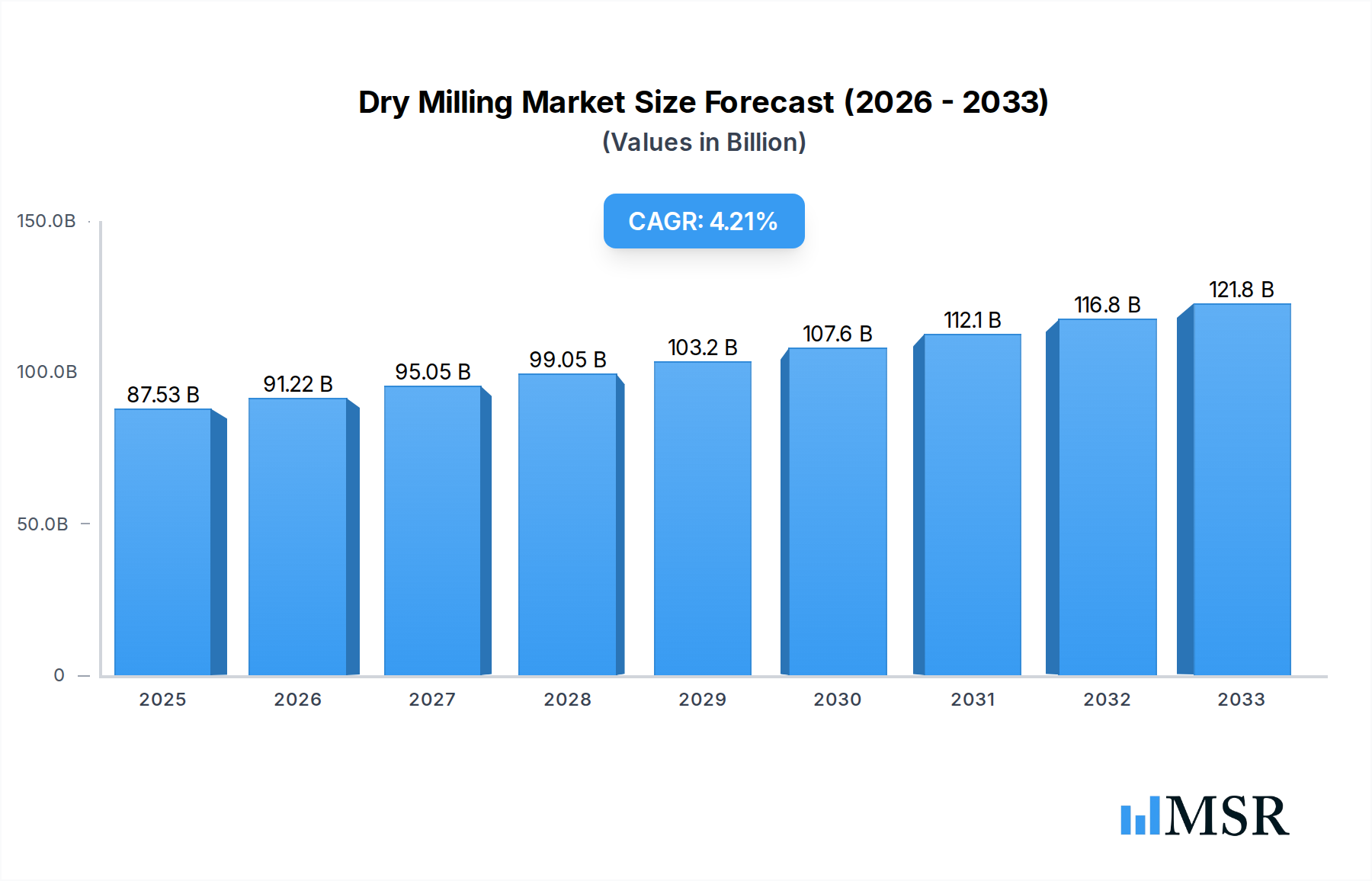

The global dry milling market is poised for significant expansion, with an estimated market size of $87,530 million and a projected Compound Annual Growth Rate (CAGR) of 4.2% from 2025 to 2033. This robust growth is primarily fueled by the increasing demand for corn-based products across diverse applications. The animal feed sector stands out as a major driver, necessitating substantial volumes of corn by-products like DDGS. Simultaneously, the burgeoning bioethanol industry, driven by global efforts to reduce reliance on fossil fuels, is creating substantial demand for corn as a feedstock for ethanol production. Furthermore, the food industry's continuous need for corn-derived ingredients such as corn grits, cornmeal, and corn flour for various food products and processed goods is another significant contributor to market expansion. Emerging economies, particularly in the Asia Pacific region, are witnessing rapid industrialization and urbanization, leading to enhanced consumption of corn-based products, thereby bolstering market growth.

Dry Milling Market Size (In Billion)

Navigating this dynamic landscape, several key trends and challenges will shape the market's trajectory. Innovations in dry milling technologies are emerging, focusing on improving efficiency, reducing waste, and enhancing the nutritional profile of milled corn products. The increasing focus on sustainability and circular economy principles is also influencing the market, with greater emphasis on utilizing by-products and minimizing environmental impact. However, the market faces certain restraints. Fluctuations in corn prices, influenced by weather patterns, global supply and demand, and geopolitical factors, can impact profitability and investment decisions. Stringent regulatory frameworks related to food safety, environmental impact, and biofuel mandates also present challenges for market participants. Despite these challenges, the overarching growth trajectory, driven by fundamental demand across key sectors and supported by technological advancements and evolving consumer preferences, positions the dry milling market for sustained and promising growth in the coming years.

Dry Milling Company Market Share

Dry Milling Market: Comprehensive Analysis & Future Outlook (2019-2033)

This in-depth market research report provides a definitive analysis of the global dry milling market, offering critical insights into its dynamics, growth trajectories, and future potential. Covering the study period of 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, this report is an essential resource for food manufacturers, feed producers, biofuel companies, investors, and industry stakeholders. We delve into the intricate workings of dry milling, exploring its applications in Fuel, Feed, and Food, and its key product segments including Ethanol, DDGS, Corn Grits, Cornmeal, and Corn Flour.

Dry Milling Market Concentration & Dynamics

The global dry milling market exhibits a moderately concentrated landscape, characterized by the strategic presence of several dominant players. Companies such as Cargill, Archer Daniels Midland Company, Bunge Limited, and SunoptA hold significant market share, driven by their extensive processing capacities, established supply chains, and diversified product portfolios. Innovation ecosystems are actively fostering advancements, particularly in optimizing corn processing for higher yields and creating value-added co-products. Regulatory frameworks, while varying by region, generally support the use of corn-derived products in food and feed, and increasingly in biofuels, influencing market access and operational standards. Substitute products, while present in certain applications (e.g., alternative grains in feed, other starches in food), face challenges in matching the cost-effectiveness and versatility of corn-based dry milled products. End-user trends are pointing towards increasing demand for sustainable and plant-based ingredients, a trend that dry milling is well-positioned to capitalize on. Mergers and acquisitions (M&A) activities have been notable, with an estimated over 20 significant M&A deals recorded within the historical period, aimed at expanding geographical reach, enhancing technological capabilities, and consolidating market position. This strategic consolidation underscores the competitive intensity and the drive for scale in the industry.

Dry Milling Industry Insights & Trends

The dry milling industry is poised for significant expansion, driven by a confluence of robust market growth drivers, transformative technological disruptions, and evolving consumer behaviors. The global dry milling market size is projected to reach over $150 billion by the end of the forecast period. A Compound Annual Growth Rate (CAGR) of approximately 4.5% is anticipated from 2025 to 2033, reflecting consistent and healthy expansion. Key growth drivers include the escalating global demand for animal feed, fueled by the rising consumption of meat and dairy products worldwide. The increasing adoption of biofuels, particularly ethanol, as a renewable energy source further bolsters market growth, supported by government mandates and environmental concerns. In the food sector, the versatility of dry milled corn products, such as corn grits and cornmeal, in various cuisines and processed food applications contributes to sustained demand. Technological advancements are playing a pivotal role, with innovations in milling efficiency, energy optimization, and the development of specialized corn varieties leading to improved yields and higher quality end-products. Furthermore, the focus on sustainability and the circular economy is encouraging the valorization of co-products like Distillers Dried Grains with Solubles (DDGS), enhancing their appeal as valuable animal feed ingredients. Evolving consumer preferences for natural, plant-based, and traceable food ingredients are also creating new avenues for dry milled corn products, particularly in niche food segments. The industry's ability to adapt to these dynamic trends will be crucial for continued success.

Key Markets & Segments Leading Dry Milling

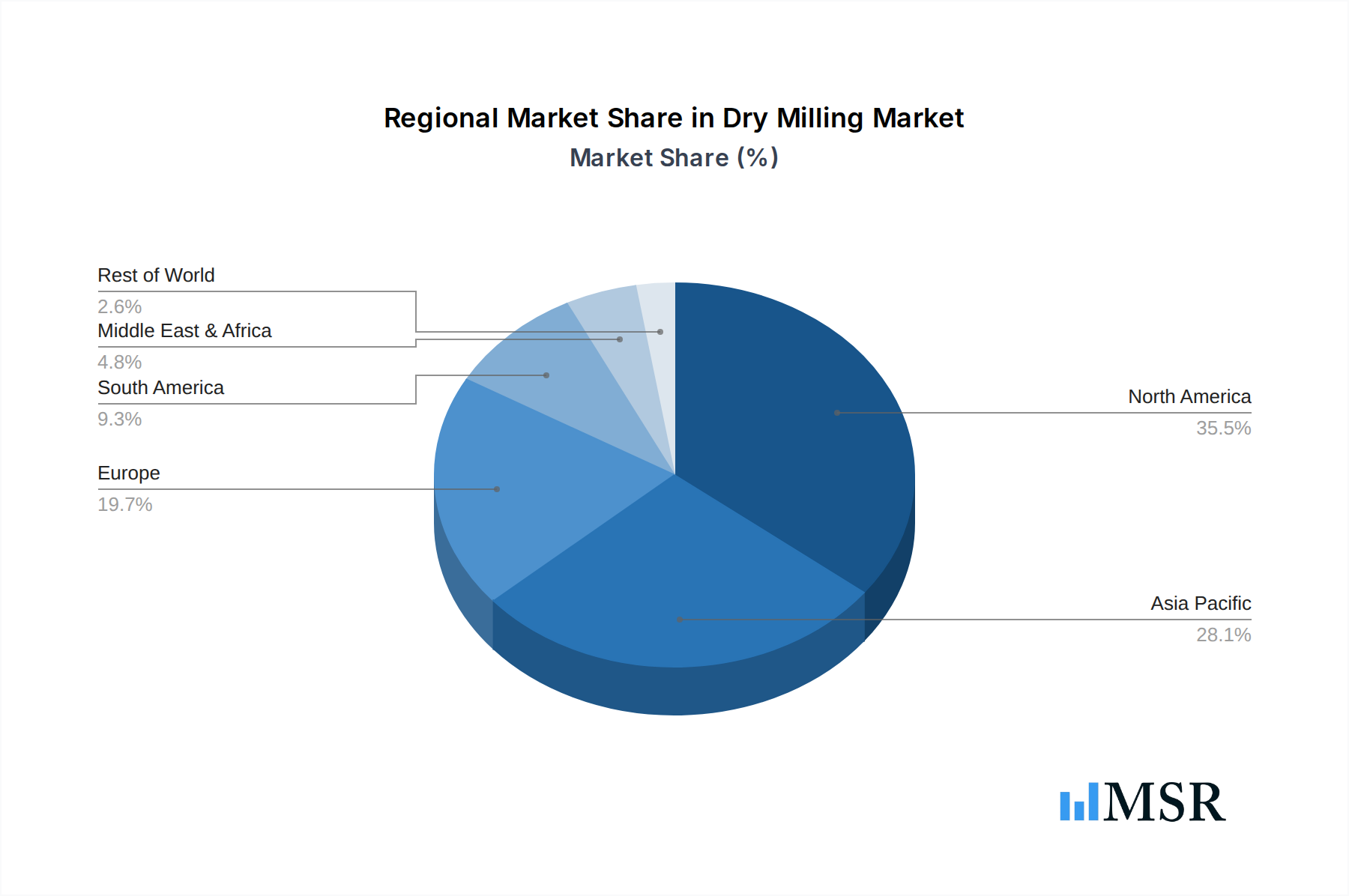

The North America region stands as a dominant force in the global dry milling market, with the United States spearheading its growth. This regional dominance is propelled by a combination of factors, including extensive corn cultivation, advanced agricultural infrastructure, and a well-established industrial base for processing.

Application: Fuel

The Fuel segment is a significant contributor to the dry milling market, primarily driven by the production of ethanol. The United States, in particular, has a substantial ethanol production capacity, supported by federal and state mandates for renewable fuel standards. Economic growth and government incentives for biofuel adoption are key drivers in this segment. The development of new fuel blends and advancements in engine technology also influence demand.

Application: Feed

The Feed segment is another cornerstone of the dry milling industry, with DDGS being a primary product. Growing global populations and increasing demand for meat and dairy products directly translate into a higher need for animal feed. The nutritional value and cost-effectiveness of DDGS make it a preferred ingredient for livestock and aquaculture. Economic development in emerging economies and improved livestock management practices are crucial drivers here.

Application: Food

The Food segment leverages various dry milled corn products, including Corn Grits, Cornmeal, and Corn Flour. The versatility of these ingredients in a wide array of food products, from breakfast cereals and baked goods to snacks and traditional cuisines, ensures consistent demand. Growing consumer interest in gluten-free options and plant-based diets also benefits corn-based food ingredients. Economic prosperity and evolving dietary habits in both developed and developing nations contribute to the segment's growth.

Product Type Dominance: Ethanol and DDGS

Within the product types, Ethanol and DDGS currently command the largest market share, reflecting their significant roles in the fuel and feed industries, respectively. The continued push for renewable energy and the robust demand for animal protein globally ensure the sustained leadership of these two product categories.

Dry Milling Product Developments

Recent product developments in the dry milling sector are focused on enhancing efficiency, sustainability, and the creation of value-added co-products. Innovations in milling technologies are leading to improved energy efficiency and reduced waste. The development of specialized corn varieties with higher starch content or specific protein profiles is enabling the production of tailor-made ingredients for diverse applications. Furthermore, there is a growing emphasis on the extraction of high-value compounds from corn processing by-products, such as antioxidants and nutraceuticals, expanding the market relevance of dry milled products beyond traditional uses and providing a competitive edge.

Challenges in the Dry Milling Market

Despite robust growth prospects, the dry milling market faces several challenges. Volatility in corn prices, influenced by weather patterns, global demand, and geopolitical factors, can significantly impact profitability. Stringent environmental regulations regarding water usage and waste disposal in processing facilities can increase operational costs. Supply chain disruptions, exacerbated by global events, can affect the availability and timely delivery of raw materials and finished products. Furthermore, intense competitive pressures from both domestic and international players, coupled with the potential for substitute products in certain applications, necessitate continuous innovation and cost optimization to maintain market share.

Forces Driving Dry Milling Growth

The dry milling industry is propelled by several potent growth forces. A primary driver is the increasing global demand for food and animal feed, directly linked to population growth and rising incomes. The growing adoption of biofuels, particularly ethanol, as a sustainable energy alternative, supported by government policies and environmental consciousness, is a significant growth catalyst. Technological advancements in milling processes, leading to increased efficiency and higher product yields, further enhance market attractiveness. Additionally, the inherent versatility of corn as a raw material, adaptable to a myriad of food, feed, and industrial applications, provides a stable foundation for sustained growth.

Long-Term Growth Catalysts in Dry Milling

Long-term growth catalysts for the dry milling market are deeply rooted in innovation and market expansion. The continuous pursuit of advanced processing technologies that improve yield, reduce energy consumption, and minimize environmental impact will be crucial. Strategic partnerships and collaborations between dry millers, technology providers, and end-users will foster the development of specialized products and new market applications. Furthermore, the expansion into emerging economies with growing populations and increasing demand for processed foods and animal feed presents significant untapped potential. The ongoing research into novel uses for corn co-products and the extraction of high-value compounds will also unlock new revenue streams.

Emerging Opportunities in Dry Milling

Emerging opportunities in the dry milling sector are diverse and promising. The burgeoning demand for plant-based food ingredients offers a significant avenue for corn-derived products like corn flour and corn grits. The increasing focus on sustainable and circular economy practices presents opportunities for valorizing by-products and developing innovative bio-based materials. Advancements in biotechnology are unlocking new applications for corn-derived starches and sugars in industrial sectors, such as bioplastics and pharmaceuticals. Furthermore, the development of value-added corn ingredients with enhanced nutritional profiles or specific functional properties caters to niche markets and premium product segments.

Leading Players in the Dry Milling Sector

- Cargill

- Archer Daniels Midland Company

- Bunge Limited

- SunoptA

- Didion Milling Inc.

- Semo Milling, LLC

- Lifeline Foods, LLC

- Pacific Ethanol Inc.

- Green Plains Inc.

- Flint Hills Resources, LP

- C.H. Guenther & Son, Incorporated

- Valero Energy Corporation

Key Milestones in Dry Milling Industry

- 2019: Significant investments announced in advanced ethanol production technologies to improve efficiency.

- 2020: Increased focus on DDGS as a premium animal feed ingredient due to supply chain disruptions in other feed components.

- 2021: Major players initiated R&D into novel food applications for corn grits and cornmeal, targeting gluten-free markets.

- 2022: Several companies expanded their processing capacities to meet rising global demand for corn-based biofuels and food ingredients.

- 2023: Growing emphasis on sustainable sourcing and processing practices within the industry.

- 2024: Advancements in co-product valorization, with new initiatives for extracting high-value compounds from DDGS.

Strategic Outlook for Dry Milling Market

The strategic outlook for the dry milling market remains exceptionally strong, driven by inherent demand in core sectors and emerging opportunities. Future growth will be accelerated by a continued focus on technological innovation, particularly in process optimization and the development of specialized corn derivatives. Expanding into untapped geographical markets, especially in Asia and Africa, will be crucial for long-term expansion. Strategic partnerships and vertical integration, from corn cultivation to end-product application, will enhance competitive advantage. The industry's ability to embrace sustainability, circular economy principles, and cater to evolving consumer preferences for plant-based and functional ingredients will define its trajectory towards achieving its full market potential.

Dry Milling Segmentation

-

1. Application

- 1.1. Fuel

- 1.2. Feed

- 1.3. Food

-

2. Type

- 2.1. Ethanol

- 2.2. DDGS

- 2.3. Corn Grits

- 2.4. Cornmeal

- 2.5. Corn Flour

- 2.6. Others

Dry Milling Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Dry Milling Regional Market Share

Geographic Coverage of Dry Milling

Dry Milling REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Dry Milling Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Fuel

- 5.1.2. Feed

- 5.1.3. Food

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Ethanol

- 5.2.2. DDGS

- 5.2.3. Corn Grits

- 5.2.4. Cornmeal

- 5.2.5. Corn Flour

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Dry Milling Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Fuel

- 6.1.2. Feed

- 6.1.3. Food

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Ethanol

- 6.2.2. DDGS

- 6.2.3. Corn Grits

- 6.2.4. Cornmeal

- 6.2.5. Corn Flour

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Dry Milling Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Fuel

- 7.1.2. Feed

- 7.1.3. Food

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Ethanol

- 7.2.2. DDGS

- 7.2.3. Corn Grits

- 7.2.4. Cornmeal

- 7.2.5. Corn Flour

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Dry Milling Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Fuel

- 8.1.2. Feed

- 8.1.3. Food

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Ethanol

- 8.2.2. DDGS

- 8.2.3. Corn Grits

- 8.2.4. Cornmeal

- 8.2.5. Corn Flour

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Dry Milling Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Fuel

- 9.1.2. Feed

- 9.1.3. Food

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Ethanol

- 9.2.2. DDGS

- 9.2.3. Corn Grits

- 9.2.4. Cornmeal

- 9.2.5. Corn Flour

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Dry Milling Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Fuel

- 10.1.2. Feed

- 10.1.3. Food

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Ethanol

- 10.2.2. DDGS

- 10.2.3. Corn Grits

- 10.2.4. Cornmeal

- 10.2.5. Corn Flour

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Cargill

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Archer Daniels Midland Company

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Bunge Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 SunoptA

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Didion Milling Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Semo Milling

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 LLc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Lifeline Foods

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 LLc

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Pacific Ethanol Inc.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Green Plains Inc.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Flint Hills Resources

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Lp

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 C.H. Guenther & Son

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Incorporated

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Valero Energy Corporation

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Cargill

List of Figures

- Figure 1: Global Dry Milling Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Dry Milling Revenue (million), by Application 2025 & 2033

- Figure 3: North America Dry Milling Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Dry Milling Revenue (million), by Type 2025 & 2033

- Figure 5: North America Dry Milling Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Dry Milling Revenue (million), by Country 2025 & 2033

- Figure 7: North America Dry Milling Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Dry Milling Revenue (million), by Application 2025 & 2033

- Figure 9: South America Dry Milling Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Dry Milling Revenue (million), by Type 2025 & 2033

- Figure 11: South America Dry Milling Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Dry Milling Revenue (million), by Country 2025 & 2033

- Figure 13: South America Dry Milling Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Dry Milling Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Dry Milling Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Dry Milling Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Dry Milling Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Dry Milling Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Dry Milling Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Dry Milling Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Dry Milling Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Dry Milling Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Dry Milling Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Dry Milling Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Dry Milling Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Dry Milling Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Dry Milling Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Dry Milling Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Dry Milling Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Dry Milling Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Dry Milling Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dry Milling Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Dry Milling Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Dry Milling Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Dry Milling Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Dry Milling Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Dry Milling Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Dry Milling Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Dry Milling Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Dry Milling Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Dry Milling Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Dry Milling Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Dry Milling Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Dry Milling Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Dry Milling Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Dry Milling Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Dry Milling Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Dry Milling Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Dry Milling Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Dry Milling Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dry Milling?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Dry Milling?

Key companies in the market include Cargill, Archer Daniels Midland Company, Bunge Limited, SunoptA, Didion Milling Inc., Semo Milling, LLc, Lifeline Foods, LLc, Pacific Ethanol Inc., Green Plains Inc., Flint Hills Resources, Lp, C.H. Guenther & Son, Incorporated, Valero Energy Corporation.

3. What are the main segments of the Dry Milling?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 87530 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dry Milling," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dry Milling report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dry Milling?

To stay informed about further developments, trends, and reports in the Dry Milling, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence