Key Insights

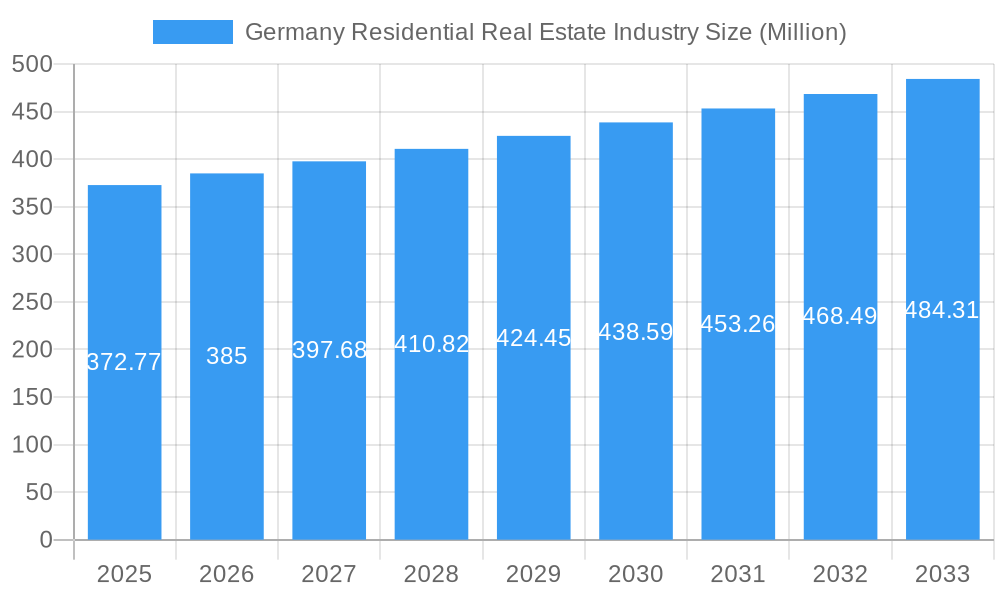

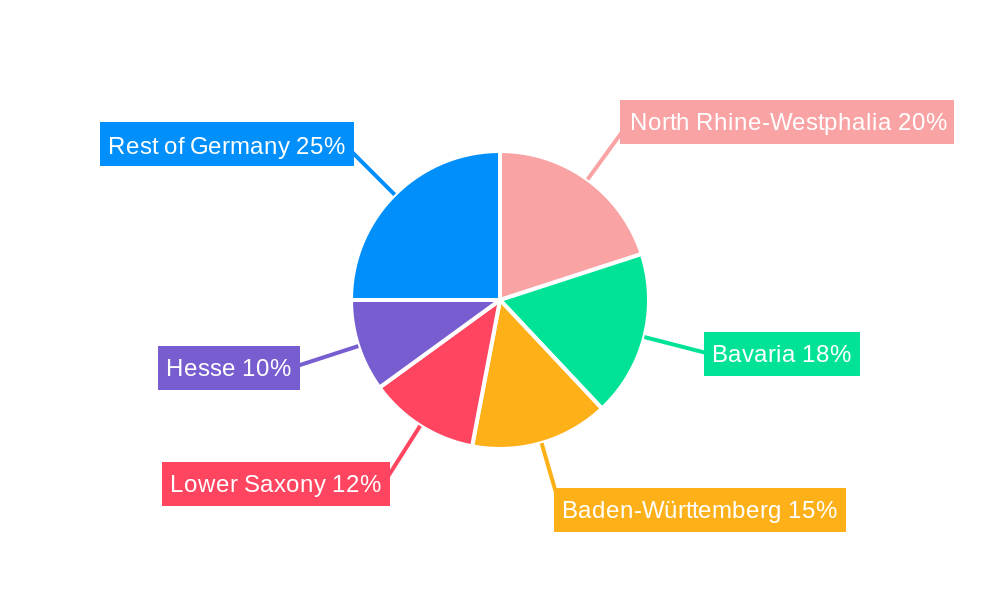

The German residential real estate market, valued at €372.77 million in 2025, is projected to experience robust growth, driven by a steadily increasing population, urbanization trends, and a persistent demand for housing, particularly in major cities like Berlin, Munich, and Hamburg. The market's Compound Annual Growth Rate (CAGR) exceeding 3.06% indicates a consistently expanding market over the forecast period (2025-2033). Strong economic performance in Germany and favorable lending conditions further contribute to market expansion. However, challenges remain, including limited land availability, particularly in urban areas, leading to increased construction costs and potentially impacting affordability. Government regulations aimed at ensuring sustainable development and affordable housing also play a significant role in shaping market dynamics. The market segmentation reveals a strong preference for condominiums and apartments, particularly in urban centers, while villas and landed houses remain popular in suburban and rural areas. Key players like Vonovia SE and Deutsche Wohnen SE are actively involved in shaping the market through their developments and acquisitions. Regional variations exist, with North Rhine-Westphalia, Bavaria, Baden-Württemberg, and Lower Saxony representing significant regional markets reflecting population density and economic activity. The ongoing evolution of market conditions suggests a dynamic landscape with continued opportunities for growth but also challenges concerning sustainable and affordable housing solutions.

Germany Residential Real Estate Industry Market Size (In Million)

The forecast period (2025-2033) indicates sustained growth driven by ongoing population shifts, economic expansion, and investments in infrastructure. While regulatory changes and potential economic fluctuations pose risks, the long-term outlook remains positive. The increasing demand for sustainable and energy-efficient housing is also reshaping market trends. Investors are increasingly focusing on eco-friendly developments, and this trend is expected to drive further market segmentation. The competition among established players and new entrants contributes to innovation and potentially improves housing options for the German population. A focus on innovative construction methods and the integration of smart home technologies is also transforming the sector.

Germany Residential Real Estate Industry Company Market Share

Germany Residential Real Estate Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the German residential real estate market, offering invaluable insights for investors, developers, and industry stakeholders. Covering the period 2019-2033, with a focus on 2025, this report unveils market dynamics, key trends, and future growth opportunities within this dynamic sector. The study encompasses key segments, including villas and landed houses, condominiums and apartments, across major cities like Berlin, Hamburg, Cologne, and Munich, and the rest of Germany. The market size is estimated at xx Million in 2025, projected to reach xx Million by 2033, with a CAGR of xx%.

Germany Residential Real Estate Industry Market Concentration & Dynamics

The German residential real estate market exhibits a moderately concentrated landscape, dominated by large players like Vonovia SE and Deutsche Wohnen SE, holding significant market share. However, a vibrant ecosystem of smaller developers and housing cooperatives like Wohnungsbaugenossenschaft Musikwinkel eG (WBG) and SAGA Siedlungs-Aktiengesellschaft Hamburg also contributes significantly. The market is influenced by stringent regulatory frameworks focusing on affordability and sustainability. Substitute products, such as rental housing and co-living spaces, are gaining traction. End-user trends show increasing demand for sustainable, energy-efficient properties in urban areas. M&A activity has been significant in recent years, with xx major deals recorded between 2019 and 2024, driving consolidation within the industry.

- Market Share: Vonovia SE and Deutsche Wohnen SE hold a combined market share of approximately xx%.

- M&A Activity: xx major mergers and acquisitions recorded between 2019 and 2024.

- Regulatory Landscape: Stringent building codes and rent control measures impact market dynamics.

- Innovation: Focus on sustainable building materials and smart home technologies.

Germany Residential Real Estate Industry Industry Insights & Trends

The German residential real estate market is driven by several key factors, including robust population growth, particularly in major cities, and a strong economy. Technological disruptions, such as PropTech solutions impacting property management and online brokerage, are transforming the industry. Evolving consumer behaviors, including a preference for sustainable and energy-efficient housing, are shaping demand. The market experienced significant growth in the historical period (2019-2024) and is expected to continue its expansion during the forecast period (2025-2033), fueled by factors such as urbanisation, growing household incomes and increased demand for rental accommodations. This growth is reflected in the market size, estimated at xx Million in 2025, and projected to reach xx Million by 2033, representing a CAGR of xx%.

Key Markets & Segments Leading Germany Residential Real Estate Industry

Berlin, Munich, and Hamburg are the leading markets, exhibiting strong demand and price appreciation. Condominiums and apartments constitute the largest segment, driven by urban population density and lifestyle preferences.

Dominant Regions:

- Berlin: High demand due to strong employment opportunities and population growth.

- Munich: High demand fueled by strong economic activity and limited supply.

- Hamburg: Attractive location and port city status drive market growth.

Dominant Segment:

- Condominiums and Apartments: Largest segment due to high population density in urban areas.

Growth Drivers:

- Economic Growth: Strong economic performance contributes to increased purchasing power.

- Population Growth: Urbanization drives demand for residential properties.

- Infrastructure Development: Improved public transportation and amenities enhance desirability.

Germany Residential Real Estate Industry Product Developments

Recent product innovations focus on sustainable building materials, energy-efficient designs, and smart home technology integration. These advancements cater to environmentally conscious buyers and enhance property value. The increasing adoption of PropTech solutions such as virtual tours and online property platforms is also enhancing the competitiveness within the market.

Challenges in the Germany Residential Real Estate Industry Market

The German residential real estate market faces challenges including stringent regulatory requirements, rising construction costs, and limited land availability in urban areas, which are impacting supply and affordability. Competition from established and emerging players also exerts pressure on profit margins. Furthermore, fluctuating interest rates and economic uncertainty pose risks to market stability. These factors can lead to delays in project completion, increased costs and reduced market liquidity.

Forces Driving Germany Residential Real Estate Industry Growth

The industry is propelled by robust economic growth and increasing urbanization, driving demand for residential properties. Government initiatives promoting sustainable housing and infrastructure development further stimulate market growth. Technological advancements in construction techniques and materials also contribute to efficiency and affordability.

Long-Term Growth Catalysts in the Germany Residential Real Estate Industry

Long-term growth catalysts include continued investments in sustainable building practices, strategic partnerships among developers and technology firms, and expansion into new markets like affordable housing. Innovations in construction technologies and the increased adoption of PropTech will further enhance efficiency, making the sector more resilient to market fluctuations.

Emerging Opportunities in Germany Residential Real Estate Industry

Emerging opportunities lie in the growing demand for sustainable and energy-efficient housing, the increasing adoption of smart home technologies, and the expansion of co-living and rental housing models. Focus on affordable housing solutions and the development of properties in suburban areas can also unlock significant opportunities.

Leading Players in the Germany Residential Real Estate Industry Sector

- Deutsche Wohnen SE

- Wohnungsbaugenossenschaft Musikwinkel eG (WBG)

- Consus Real Estate

- Vonovia SE

- Residia Care Holding GmbH & Co

- SAGA Siedlungs-Aktiengesellschaft Hamburg

- Vivawest

- ABG Frankfurt Holding

- 6 3 Other Companies

- Degewo

- LEG Immobilien SE

Key Milestones in Germany Residential Real Estate Industry Industry

- 2020: Increased government regulations on energy efficiency standards for new buildings.

- 2021: Launch of several PropTech platforms disrupting traditional brokerage models.

- 2022: Significant M&A activity consolidating market share amongst major players.

- 2023: Focus on sustainable building materials gaining momentum.

Strategic Outlook for Germany Residential Real Estate Industry Market

The German residential real estate market is poised for continued growth, driven by strong fundamentals and emerging opportunities. Strategic partnerships, technological advancements, and a focus on sustainable development will be crucial for navigating market challenges and realizing long-term success. The market is expected to remain dynamic with increased focus on meeting the growing demand for affordable and sustainable housing solutions.

Germany Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Villas and Landed Houses

- 1.2. Condominiums and Apartments

-

2. Key Cities

- 2.1. Berlin

- 2.2. Hamburg

- 2.3. Cologne

- 2.4. Munich

- 2.5. Rest of Germany

Germany Residential Real Estate Industry Segmentation By Geography

- 1. Germany

Germany Residential Real Estate Industry Regional Market Share

Geographic Coverage of Germany Residential Real Estate Industry

Germany Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 3.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Villas and Landed Houses

- 5.1.2. Condominiums and Apartments

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Berlin

- 5.2.2. Hamburg

- 5.2.3. Cologne

- 5.2.4. Munich

- 5.2.5. Rest of Germany

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Residential Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Villas and Landed Houses

- 6.1.2. Condominiums and Apartments

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Berlin

- 6.2.2. Hamburg

- 6.2.3. Cologne

- 6.2.4. Munich

- 6.2.5. Rest of Germany

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Deutsche Wohnen SE

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Wohnungsbaugenossenschaft Musikwinkel eG (WBG)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Consus Real Estate

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Vonovia SE

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Residia Care Holding GmbH & Co

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 SAGA Siedlungs-Aktiengesellschaft Hamburg

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Vivawest

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ABG Frankfurt Holding**List Not Exhaustive 6 3 Other Companie

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Degewo

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 LEG Immobilien SE

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Deutsche Wohnen SE

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Germany Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Germany Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Germany Residential Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Germany Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Germany Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Germany Residential Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Residential Real Estate Industry?

The projected CAGR is approximately > 3.06%.

2. Which companies are prominent players in the Germany Residential Real Estate Industry?

Key companies in the market include Deutsche Wohnen SE, Wohnungsbaugenossenschaft Musikwinkel eG (WBG), Consus Real Estate, Vonovia SE, Residia Care Holding GmbH & Co, SAGA Siedlungs-Aktiengesellschaft Hamburg, Vivawest, ABG Frankfurt Holding**List Not Exhaustive 6 3 Other Companie, Degewo, LEG Immobilien SE.

3. What are the main segments of the Germany Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 372.77 Million as of 2022.

5. What are some drivers contributing to market growth?

Strong Demand and Rising Construction Activities to Drive the Market; Rising House Prices in Germany Affecting Demand in the Market.

6. What are the notable trends driving market growth?

Strong Demand And Rising Construction Activities To Drive The Market.

7. Are there any restraints impacting market growth?

Weak economic environment.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Germany Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence