Key Insights

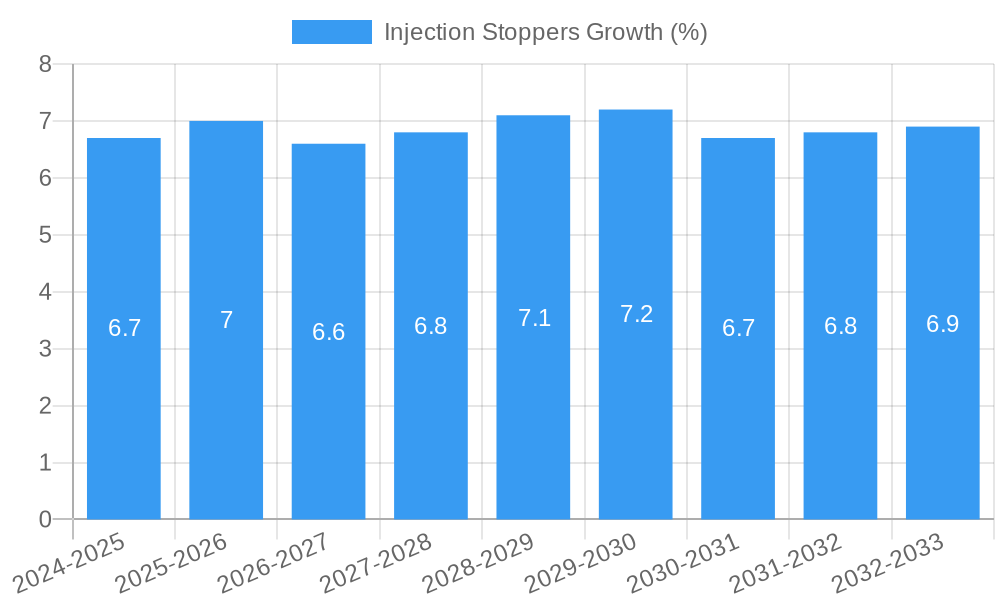

The global injection stoppers market is poised for significant expansion, driven by the increasing demand for advanced drug delivery systems and the burgeoning pharmaceutical industry. With an estimated market size of $1.2 billion in 2024, projected to reach $2.1 billion by 2033, the market is set to witness a robust Compound Annual Growth Rate (CAGR) of approximately 6.5%. This growth trajectory is largely fueled by the escalating prevalence of chronic diseases, necessitating greater reliance on injectable medications and consequently, a higher demand for reliable and sterile stoppers. The rise in biologics and biosimilars, which often require sophisticated packaging solutions, also contributes significantly to market expansion. Furthermore, government initiatives promoting healthcare access and the continuous innovation in pre-filled syringes and auto-injectors are key drivers. The market's value is denominated in millions of U.S. dollars, reflecting the substantial economic activity within this sector.

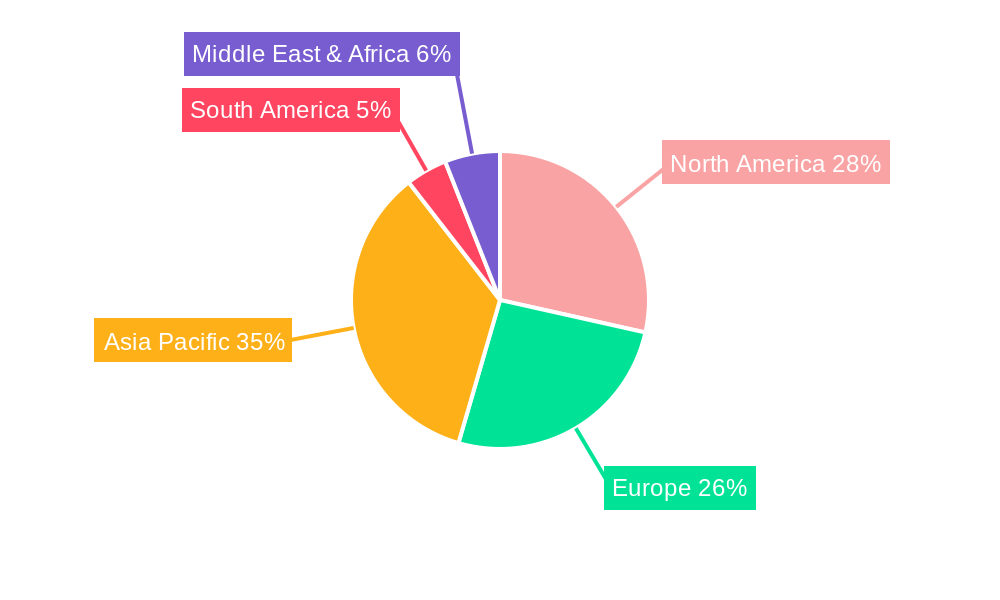

Geographically, Asia Pacific is emerging as a dominant force, driven by rapid industrialization, a large patient pool, and increasing healthcare expenditure in countries like China and India. North America and Europe, with their established pharmaceutical industries and high adoption rates of advanced drug delivery technologies, continue to hold substantial market shares. Key trends shaping the market include a growing preference for sterile and high-purity stoppers to ensure drug safety and efficacy, along with the development of novel materials and designs that offer enhanced compatibility and tamper-evidence. While the market exhibits strong growth potential, restraints such as stringent regulatory requirements for pharmaceutical packaging materials and the high cost of advanced manufacturing technologies could pose challenges. However, the continuous efforts by leading companies to invest in research and development and expand their product portfolios are expected to mitigate these challenges, ensuring a dynamic and evolving market landscape.

Injection Stoppers Market: Comprehensive Industry Report 2019-2033 (Forecast to 2033)

Unlock critical insights into the global Injection Stoppers market with this definitive industry report. Covering the period from 2019 to 2033, with a base and estimated year of 2025 and a robust forecast period from 2025 to 2033, this analysis delves deep into market dynamics, key trends, leading segments, product innovations, challenges, growth drivers, and strategic opportunities. Essential for pharmaceutical manufacturers, packaging solution providers, regulatory bodies, and investors, this report provides actionable intelligence to navigate the evolving landscape of parenteral drug delivery.

Injection Stoppers Market Concentration & Dynamics

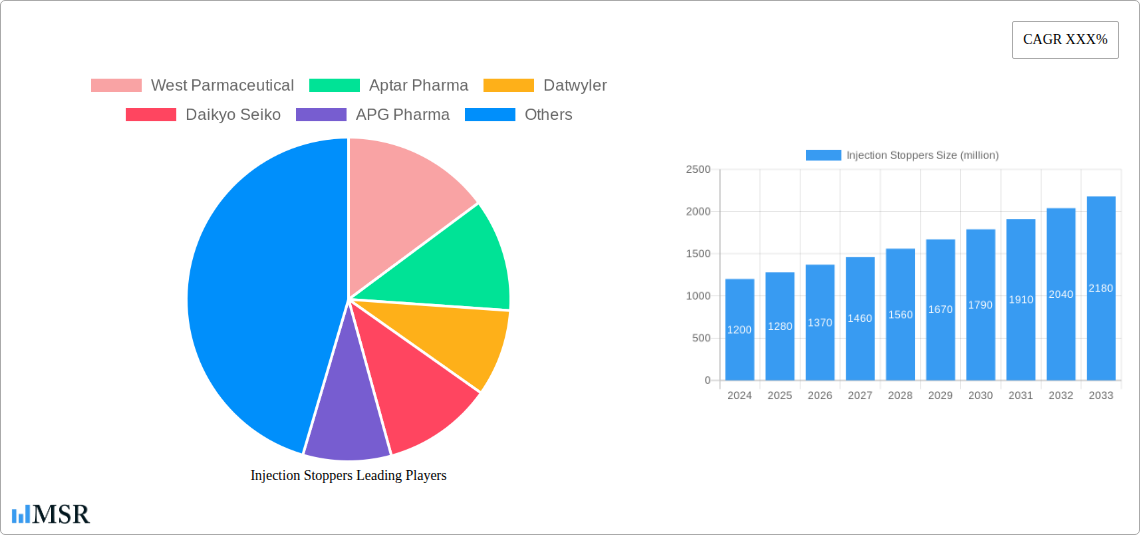

The global Injection Stoppers market exhibits a moderate to high concentration, with a few key players dominating significant market share, projected to be over 60% by 2025. Major corporations like West Pharmaceutical Services, Aptar Pharma, and Datwyler hold substantial influence, driven by their extensive product portfolios, established distribution networks, and robust R&D investments. The innovation ecosystem is characterized by continuous advancements in material science and manufacturing processes, focusing on enhanced drug compatibility, reduced extractables and leachables, and improved sealing integrity. Regulatory frameworks, spearheaded by entities like the FDA and EMA, play a pivotal role in shaping product development and market entry, emphasizing stringent quality control and safety standards. The threat of substitute products, while present in the form of alternative sealing mechanisms, remains relatively low due to the established efficacy and regulatory acceptance of injection stoppers in parenteral applications. End-user trends are increasingly leaning towards pre-filled syringes and auto-injectors, necessitating specialized stopper designs that ensure sterility and prevent contamination. Mergers and acquisitions (M&A) activities are a recurring theme, with an estimated 15-20 M&A deals annually within the broader pharmaceutical packaging sector, impacting the injection stopper landscape by consolidating market power and accelerating technology adoption. The market size for injection stoppers is projected to reach over $2.5 billion by 2025.

Injection Stoppers Industry Insights & Trends

The Injection Stoppers industry is poised for substantial growth, driven by a confluence of factors including an expanding global pharmaceutical market, a rising prevalence of chronic diseases, and advancements in drug delivery technologies. The market size for injection stoppers is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 6.5% from 2019 to 2033, reaching an estimated value exceeding $4.2 billion by 2033. Key growth drivers include the escalating demand for sterile and safe parenteral drug packaging, fueled by the continuous development of new biologics, vaccines, and therapeutic proteins. Technological disruptions are predominantly centered on material innovation, with a focus on developing elastomeric stoppers that offer superior chemical compatibility with a wider range of drug formulations, including sensitive biologics and cytotoxic drugs. The development of stoppers with enhanced barrier properties to prevent oxygen and moisture ingress, and reduced extractables and leachables, is also a significant trend. Evolving consumer behaviors, particularly the preference for self-administration of medications through pre-filled syringes and auto-injectors, are compelling manufacturers to innovate stoppers that facilitate ease of use, patient safety, and product integrity. Furthermore, the increasing adoption of advanced manufacturing techniques, such as injection molding and automated production, is enhancing efficiency and product consistency. The shift towards single-use systems in biopharmaceutical manufacturing also presents a growing opportunity for specialized injection stopper solutions. The market is also observing a trend towards customized stopper designs to meet the specific requirements of novel drug formulations and advanced delivery devices. The estimated market size for injection stoppers in the base year 2025 is $2.6 billion.

Key Markets & Segments Leading Injection Stoppers

The global Injection Stoppers market is characterized by distinct regional dominance and segment leadership. North America and Europe currently lead the market, driven by established pharmaceutical industries, high healthcare expenditure, and a strong presence of leading pharmaceutical companies and research institutions. Asia Pacific is emerging as a rapidly growing market, propelled by increasing investments in healthcare infrastructure, a growing patient population, and the expansion of generic drug manufacturing.

Dominant Segments:

Application:

- Pre-Filled Syringe (PFS): This segment holds the largest market share, projected to exceed 55% of the total market value by 2025. The surging demand for biologics, vaccines, and chronic disease management medications delivered via PFS is the primary driver. The convenience and reduced risk of needle-stick injuries associated with PFS further bolster its dominance.

- Auto-Injector: This segment is experiencing robust growth, anticipated to capture over 30% of the market by 2025. The increasing prevalence of chronic conditions requiring self-administration, coupled with advancements in auto-injector technology for improved patient compliance and usability, fuels this growth.

- Other: This segment, encompassing vials and other specialized parenteral delivery systems, accounts for the remaining market share but is witnessing steady growth due to its critical role in various therapeutic areas.

Type:

- Chlorobutyl Rubber: This type dominates the market, estimated to hold over 60% share by 2025. Its excellent chemical inertness, low permeability, and good elasticity make it ideal for a wide range of pharmaceutical applications, especially for sensitive drugs.

- Butyl Rubber: A significant segment, accounting for approximately 25% of the market, offering a good balance of cost-effectiveness and performance for various drug formulations.

- Dromobutyl Rubber: This specialized type is gaining traction, particularly for highly sensitive or complex drug formulations, representing a smaller but rapidly growing segment.

Drivers for Dominance:

- Economic Growth and Healthcare Spending: Higher disposable incomes and increased government spending on healthcare in leading regions translate to greater demand for pharmaceutical products and, consequently, injection stoppers.

- Infrastructure Development: Robust manufacturing and logistics infrastructure in key regions ensures efficient production and distribution of high-quality injection stoppers.

- Regulatory Support and Standards: Favorable regulatory environments that prioritize drug safety and efficacy indirectly promote the adoption of advanced injection stopper solutions.

- Technological Advancements: Continuous innovation in material science and manufacturing processes enables the development of stoppers that meet evolving drug formulation and delivery needs.

- Growing Biologics and Biosimilars Market: The expanding market for complex biological drugs and their biosimilar counterparts necessitates high-performance stoppers to maintain product stability and sterility.

Injection Stoppers Product Developments

Recent product developments in the Injection Stoppers market are sharply focused on enhancing drug compatibility, minimizing extractables and leachables, and improving user experience. Innovations include advanced elastomeric formulations, such as bromobutyl and chlorobutyl rubber compounds, engineered for superior resistance to a wide array of drug formulations, particularly sensitive biologics and vaccines. Development of stoppers with novel surface treatments and barrier coatings aims to further reduce interaction with the drug product, ensuring greater stability and shelf-life. Furthermore, there's a growing trend towards integrated stopper designs for pre-filled syringes and auto-injectors, simplifying assembly processes and enhancing product reliability. The market is also seeing advancements in sterile manufacturing techniques and specialized packaging solutions to maintain the integrity of stoppers throughout the supply chain, crucial for pandemic preparedness and routine pharmaceutical supply.

Challenges in the Injection Stoppers Market

The Injection Stoppers market faces several significant challenges. Stringent regulatory compliance remains a primary hurdle, requiring extensive testing and validation for new materials and designs to meet global pharmacopeial standards. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, can impact production schedules and cost-effectiveness. Competitive pressures from established players and emerging manufacturers necessitate continuous innovation and cost optimization. The increasing complexity of drug formulations, particularly biologics, demands stoppers with highly specific material properties, posing R&D challenges. Quantifiable impacts include potential delays in product launches and increased manufacturing costs due to rigorous quality control and material sourcing complexities. The market size is also influenced by the cost sensitivity of certain drug segments.

Forces Driving Injection Stoppers Growth

The growth of the Injection Stoppers market is primarily propelled by several key forces. The accelerating development and commercialization of biologics and vaccines are paramount, requiring advanced containment solutions. The rising global prevalence of chronic diseases like diabetes and autoimmune disorders drives demand for injectable therapeutics and associated packaging. Technological advancements in drug delivery devices, such as auto-injectors and pen injectors, necessitate specialized stopper designs that ensure precise dosing and patient safety. Increasing healthcare expenditure and improved access to healthcare in emerging economies also contribute significantly to market expansion. Furthermore, stringent quality and safety regulations by bodies like the FDA and EMA encourage the adoption of high-performance, reliable stopper solutions. The growing demand for pre-filled syringes for convenience and reduced administration errors is another major growth catalyst.

Challenges in the Injection Stoppers Market

Long-term growth catalysts for the Injection Stoppers market are rooted in ongoing innovation and strategic market expansion. Continuous material science research leading to the development of novel elastomers with enhanced chemical inertness, improved barrier properties, and biocompatibility will be critical. Strategic partnerships and collaborations between stopper manufacturers and pharmaceutical companies can accelerate the development and adoption of customized solutions for new drug modalities. Market expansion into underdeveloped regions with growing healthcare needs presents significant untapped potential. The increasing focus on sustainability and eco-friendly packaging solutions also offers an opportunity for differentiated product offerings. Furthermore, advancements in manufacturing technologies, such as Industry 4.0, can drive efficiency and reduce costs, making injection stoppers more accessible globally. The growing demand for personalized medicine will also require highly specialized and adaptable stopper solutions.

Emerging Opportunities in Injection Stoppers

Emerging opportunities in the Injection Stoppers market are diverse and rapidly evolving. The development of stoppers for gene therapies and cell therapies represents a significant growth avenue, requiring ultra-low extractables and leachables and precise sterility. The expansion of biosimilars creates a substantial demand for cost-effective yet high-quality stoppers that can match the performance of innovator products. The increasing trend towards home healthcare and remote patient monitoring will drive demand for stoppers compatible with portable and user-friendly injection devices. Furthermore, the focus on circular economy principles is creating opportunities for developing stoppers made from recycled or biodegradable materials, provided they meet stringent pharmaceutical standards. The growth of contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs) in the pharmaceutical industry also presents opportunities for direct engagement and supply agreements. The demand for specialized stoppers for lyophilized products is also on the rise.

Leading Players in the Injection Stoppers Sector

- West Pharmaceutical

- Aptar Pharma

- Datwyler

- Daikyo Seiko

- APG Pharma

- Sagar Rubber

- Bormioli Pharma

- Shandong Pharmaceutical Glass

- Jiangsu Hualan New Pharmaceutical Material

- Anhui Huaneng

- Hebei First Rubber Medical Technology

- Jiangsu Best New Medical Material

- Hubei Huaqiang High-tech

- Zhengzhou Aoxiang pharmaceutical packing

- Shengzhou Rubber & Plastic

Key Milestones in Injection Stoppers Industry

- 2019: Launch of novel elastomer formulations by West Pharmaceutical for enhanced compatibility with biologics.

- 2020: Aptar Pharma announces expansion of its sterile manufacturing capabilities to meet increased global demand for parenteral drug packaging.

- 2021: Datwyler introduces advanced stopper solutions with improved barrier properties to protect sensitive drug formulations.

- 2022: Daikyo Seiko invests in new R&D facilities to focus on next-generation elastomer technology.

- 2023: Significant increase in M&A activity within the broader pharmaceutical packaging sector, impacting consolidation in the stopper market.

- 2024: Growing emphasis on sustainable materials and manufacturing processes in stopper production.

Strategic Outlook for Injection Stoppers Market

The strategic outlook for the Injection Stoppers market is overwhelmingly positive, driven by sustained demand from the pharmaceutical industry and continuous innovation. Key growth accelerators include the ongoing development of novel therapeutics, particularly biologics and biosimilars, which require high-performance parenteral packaging. Strategic opportunities lie in expanding into emerging markets with growing healthcare needs and investing in R&D for advanced materials that address the challenges of complex drug formulations. Manufacturers who can offer integrated solutions, prioritize supply chain resilience, and embrace sustainable practices will be best positioned for success. The market's future potential is further bolstered by the increasing adoption of pre-filled syringes and auto-injectors, making high-quality injection stoppers indispensable components of modern drug delivery systems.

Injection Stoppers Segmentation

-

1. Application

- 1.1. Pre-Filled Syringe

- 1.2. Auto-injector

- 1.3. Other

-

2. Type

- 2.1. Butyl Rubber

- 2.2. Chlorobutyl Rubber

- 2.3. Dromobutyl Rubber

Injection Stoppers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Injection Stoppers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Injection Stoppers Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pre-Filled Syringe

- 5.1.2. Auto-injector

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Butyl Rubber

- 5.2.2. Chlorobutyl Rubber

- 5.2.3. Dromobutyl Rubber

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Injection Stoppers Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pre-Filled Syringe

- 6.1.2. Auto-injector

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Butyl Rubber

- 6.2.2. Chlorobutyl Rubber

- 6.2.3. Dromobutyl Rubber

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Injection Stoppers Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pre-Filled Syringe

- 7.1.2. Auto-injector

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Butyl Rubber

- 7.2.2. Chlorobutyl Rubber

- 7.2.3. Dromobutyl Rubber

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Injection Stoppers Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pre-Filled Syringe

- 8.1.2. Auto-injector

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Butyl Rubber

- 8.2.2. Chlorobutyl Rubber

- 8.2.3. Dromobutyl Rubber

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Injection Stoppers Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pre-Filled Syringe

- 9.1.2. Auto-injector

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Butyl Rubber

- 9.2.2. Chlorobutyl Rubber

- 9.2.3. Dromobutyl Rubber

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Injection Stoppers Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pre-Filled Syringe

- 10.1.2. Auto-injector

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Butyl Rubber

- 10.2.2. Chlorobutyl Rubber

- 10.2.3. Dromobutyl Rubber

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 West Parmaceutical

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Aptar Pharma

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Datwyler

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Daikyo Seiko

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 APG Pharma

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Sagar Rrubber

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bormioli Pharma

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Shandong Pharmaceutical Glass

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Jiangsu Hualan New Pharmaceutical Material

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Anhui Huaneng

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Hebei First Rubber Medical Technology

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Jiangsu Best New Medical Material

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Hubei Huaqiang High-tech

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zhengzhou Aoxiang pharmaceutical packing

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Shengzhou Rubber & Plastic

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 West Parmaceutical

List of Figures

- Figure 1: Global Injection Stoppers Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Injection Stoppers Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Injection Stoppers Revenue (million), by Application 2024 & 2032

- Figure 4: North America Injection Stoppers Volume (K), by Application 2024 & 2032

- Figure 5: North America Injection Stoppers Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Injection Stoppers Volume Share (%), by Application 2024 & 2032

- Figure 7: North America Injection Stoppers Revenue (million), by Type 2024 & 2032

- Figure 8: North America Injection Stoppers Volume (K), by Type 2024 & 2032

- Figure 9: North America Injection Stoppers Revenue Share (%), by Type 2024 & 2032

- Figure 10: North America Injection Stoppers Volume Share (%), by Type 2024 & 2032

- Figure 11: North America Injection Stoppers Revenue (million), by Country 2024 & 2032

- Figure 12: North America Injection Stoppers Volume (K), by Country 2024 & 2032

- Figure 13: North America Injection Stoppers Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Injection Stoppers Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Injection Stoppers Revenue (million), by Application 2024 & 2032

- Figure 16: South America Injection Stoppers Volume (K), by Application 2024 & 2032

- Figure 17: South America Injection Stoppers Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America Injection Stoppers Volume Share (%), by Application 2024 & 2032

- Figure 19: South America Injection Stoppers Revenue (million), by Type 2024 & 2032

- Figure 20: South America Injection Stoppers Volume (K), by Type 2024 & 2032

- Figure 21: South America Injection Stoppers Revenue Share (%), by Type 2024 & 2032

- Figure 22: South America Injection Stoppers Volume Share (%), by Type 2024 & 2032

- Figure 23: South America Injection Stoppers Revenue (million), by Country 2024 & 2032

- Figure 24: South America Injection Stoppers Volume (K), by Country 2024 & 2032

- Figure 25: South America Injection Stoppers Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Injection Stoppers Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Injection Stoppers Revenue (million), by Application 2024 & 2032

- Figure 28: Europe Injection Stoppers Volume (K), by Application 2024 & 2032

- Figure 29: Europe Injection Stoppers Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe Injection Stoppers Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe Injection Stoppers Revenue (million), by Type 2024 & 2032

- Figure 32: Europe Injection Stoppers Volume (K), by Type 2024 & 2032

- Figure 33: Europe Injection Stoppers Revenue Share (%), by Type 2024 & 2032

- Figure 34: Europe Injection Stoppers Volume Share (%), by Type 2024 & 2032

- Figure 35: Europe Injection Stoppers Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Injection Stoppers Volume (K), by Country 2024 & 2032

- Figure 37: Europe Injection Stoppers Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Injection Stoppers Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Injection Stoppers Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa Injection Stoppers Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa Injection Stoppers Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa Injection Stoppers Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa Injection Stoppers Revenue (million), by Type 2024 & 2032

- Figure 44: Middle East & Africa Injection Stoppers Volume (K), by Type 2024 & 2032

- Figure 45: Middle East & Africa Injection Stoppers Revenue Share (%), by Type 2024 & 2032

- Figure 46: Middle East & Africa Injection Stoppers Volume Share (%), by Type 2024 & 2032

- Figure 47: Middle East & Africa Injection Stoppers Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Injection Stoppers Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Injection Stoppers Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Injection Stoppers Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Injection Stoppers Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific Injection Stoppers Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific Injection Stoppers Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Injection Stoppers Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Injection Stoppers Revenue (million), by Type 2024 & 2032

- Figure 56: Asia Pacific Injection Stoppers Volume (K), by Type 2024 & 2032

- Figure 57: Asia Pacific Injection Stoppers Revenue Share (%), by Type 2024 & 2032

- Figure 58: Asia Pacific Injection Stoppers Volume Share (%), by Type 2024 & 2032

- Figure 59: Asia Pacific Injection Stoppers Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Injection Stoppers Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Injection Stoppers Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Injection Stoppers Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Injection Stoppers Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Injection Stoppers Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Injection Stoppers Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Injection Stoppers Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Injection Stoppers Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Injection Stoppers Volume K Forecast, by Type 2019 & 2032

- Table 7: Global Injection Stoppers Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Injection Stoppers Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Injection Stoppers Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Injection Stoppers Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Injection Stoppers Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Injection Stoppers Volume K Forecast, by Type 2019 & 2032

- Table 13: Global Injection Stoppers Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Injection Stoppers Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Injection Stoppers Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Injection Stoppers Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Injection Stoppers Revenue million Forecast, by Type 2019 & 2032

- Table 24: Global Injection Stoppers Volume K Forecast, by Type 2019 & 2032

- Table 25: Global Injection Stoppers Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Injection Stoppers Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Injection Stoppers Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Injection Stoppers Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Injection Stoppers Revenue million Forecast, by Type 2019 & 2032

- Table 36: Global Injection Stoppers Volume K Forecast, by Type 2019 & 2032

- Table 37: Global Injection Stoppers Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Injection Stoppers Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Injection Stoppers Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global Injection Stoppers Volume K Forecast, by Application 2019 & 2032

- Table 59: Global Injection Stoppers Revenue million Forecast, by Type 2019 & 2032

- Table 60: Global Injection Stoppers Volume K Forecast, by Type 2019 & 2032

- Table 61: Global Injection Stoppers Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Injection Stoppers Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Injection Stoppers Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global Injection Stoppers Volume K Forecast, by Application 2019 & 2032

- Table 77: Global Injection Stoppers Revenue million Forecast, by Type 2019 & 2032

- Table 78: Global Injection Stoppers Volume K Forecast, by Type 2019 & 2032

- Table 79: Global Injection Stoppers Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Injection Stoppers Volume K Forecast, by Country 2019 & 2032

- Table 81: China Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Injection Stoppers Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Injection Stoppers Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Injection Stoppers?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Injection Stoppers?

Key companies in the market include West Parmaceutical, Aptar Pharma, Datwyler, Daikyo Seiko, APG Pharma, Sagar Rrubber, Bormioli Pharma, Shandong Pharmaceutical Glass, Jiangsu Hualan New Pharmaceutical Material, Anhui Huaneng, Hebei First Rubber Medical Technology, Jiangsu Best New Medical Material, Hubei Huaqiang High-tech, Zhengzhou Aoxiang pharmaceutical packing, Shengzhou Rubber & Plastic.

3. What are the main segments of the Injection Stoppers?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Injection Stoppers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Injection Stoppers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Injection Stoppers?

To stay informed about further developments, trends, and reports in the Injection Stoppers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence