Key Insights

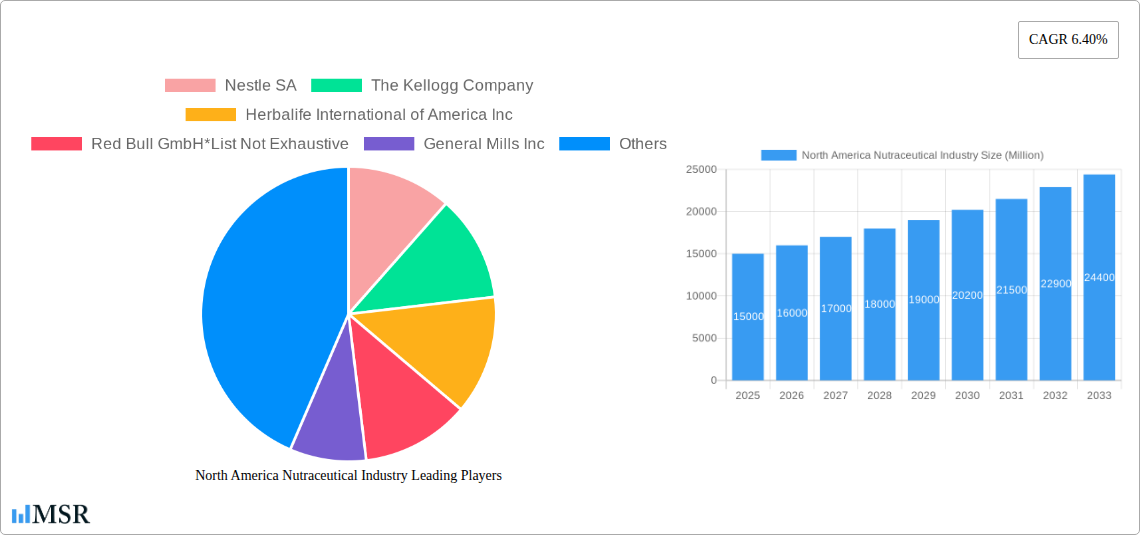

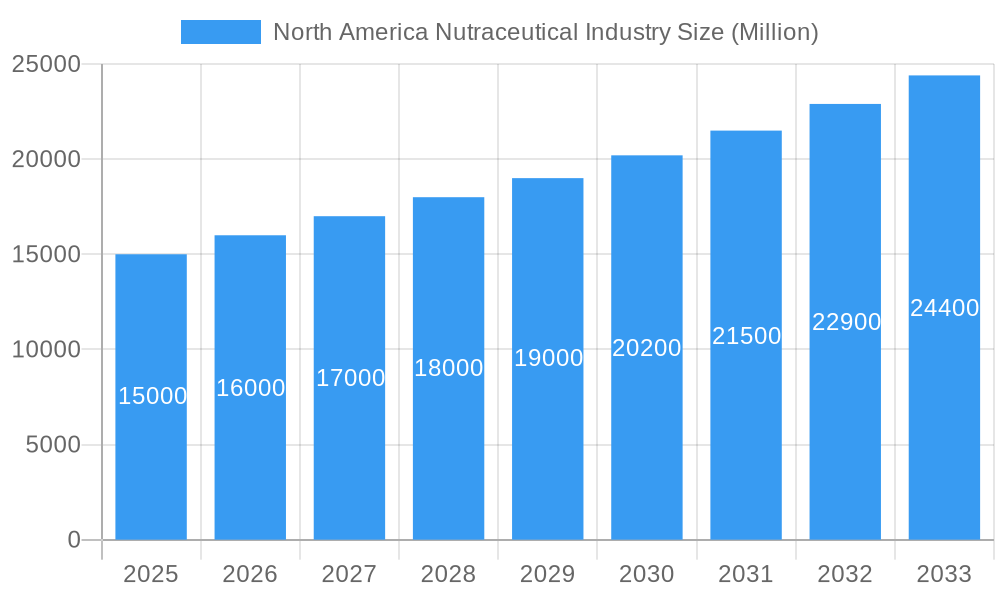

The North American nutraceutical market, valued at approximately $XX million in 2025, is projected to experience robust growth, driven by increasing health consciousness among consumers and rising prevalence of chronic diseases. A compound annual growth rate (CAGR) of 6.40% from 2025 to 2033 indicates a significant expansion of this market. Key drivers include the rising demand for functional foods and beverages, dietary supplements catering to specific health needs (e.g., immunity, gut health, cognitive function), and the increasing adoption of online retail channels. Consumer preference shifts towards natural and organic ingredients are also fueling market growth. While specific market segmentation data is limited, the substantial presence of major players like Nestle, Kellogg's, and Herbalife signifies the market's maturity and profitability. The market's growth is further bolstered by successful marketing strategies emphasizing preventative healthcare and the integration of nutraceuticals into daily routines.

North America Nutraceutical Industry Market Size (In Billion)

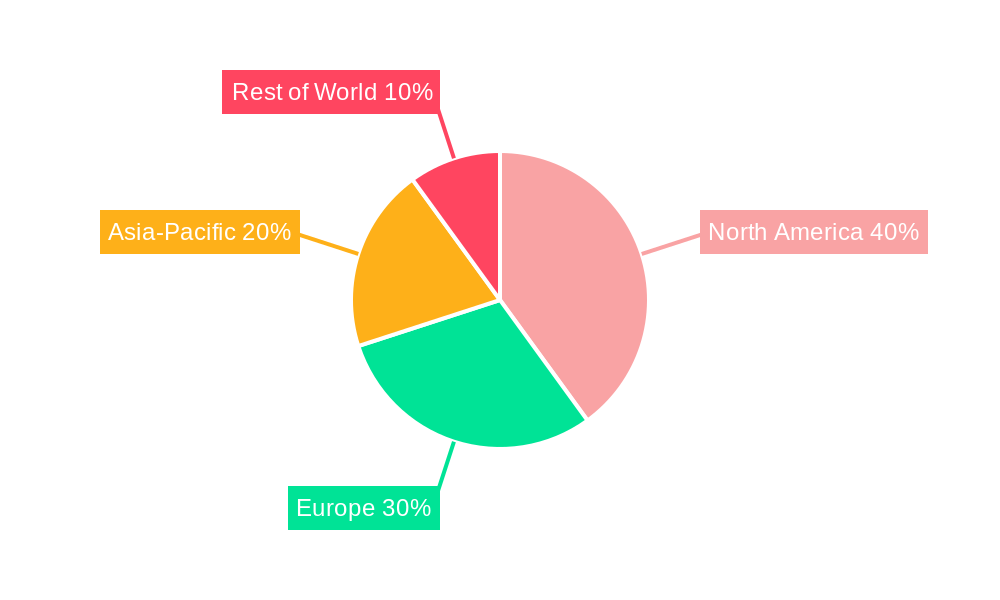

However, the market faces certain restraints. Regulatory hurdles surrounding product labeling and claims, coupled with varying consumer perceptions about the efficacy and safety of certain nutraceuticals, could potentially temper growth. Pricing pressures, particularly within the competitive functional beverage segment, and concerns about ingredient sourcing and sustainability also pose challenges. Despite these factors, the overall market outlook remains positive, with continued growth driven by technological advancements in product development, innovative marketing, and a growing consumer base actively seeking natural solutions for health and wellness. The dominance of North America within the global nutraceutical market suggests a significant opportunity for sustained expansion in the coming years, with considerable potential for market penetration through diversified distribution channels and product diversification.

North America Nutraceutical Industry Company Market Share

North America Nutraceutical Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the North America nutraceutical industry, encompassing market size, growth drivers, key segments, competitive landscape, and future outlook. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. This report is crucial for industry stakeholders, investors, and businesses seeking to understand and navigate this dynamic market. The report leverages extensive primary and secondary research, offering actionable insights for strategic decision-making.

North America Nutraceutical Industry Market Concentration & Dynamics

The North American nutraceutical market exhibits a moderately concentrated landscape, with key players like Nestle SA, The Kellogg Company, Herbalife International of America Inc, and Pfizer Inc holding significant market share. However, the presence of numerous smaller players and emerging brands indicates a dynamic competitive environment. The industry is characterized by continuous innovation in product formulations, delivery systems, and marketing strategies. Regulatory frameworks, particularly those related to labeling and ingredient safety, play a significant role in shaping market dynamics. Substitute products, such as traditional herbal remedies and dietary supplements, exert competitive pressure. Consumer trends, focused on health and wellness, drive demand, while the prevalence of M&A activities signals industry consolidation and expansion.

- Market Concentration: The top 5 players hold approximately xx% of the market share in 2025 (estimated).

- M&A Activity: An average of xx M&A deals were recorded annually during the historical period (2019-2024).

- Innovation Ecosystem: Significant investment in R&D drives the development of novel nutraceuticals with enhanced efficacy and bioavailability.

- Regulatory Framework: Stringent regulations regarding ingredient labeling and safety standards influence product development and marketing strategies.

North America Nutraceutical Industry Insights & Trends

The North America nutraceutical market is experiencing robust growth, driven by increasing health consciousness among consumers, rising disposable incomes, and growing demand for convenient and functional food and beverage products. The market size reached $xx Million in 2024 and is projected to reach $xx Million by 2033, exhibiting a CAGR of xx% during the forecast period. This growth is fueled by several key factors, including the escalating prevalence of chronic diseases, increasing awareness of the benefits of preventive healthcare, and the rising popularity of personalized nutrition. Technological advancements in areas like targeted delivery systems and precision fermentation are further contributing to market expansion. Changes in consumer behavior, including a preference for natural and organic ingredients, are shaping product development and marketing strategies.

Key Markets & Segments Leading North America Nutraceutical Industry

Dominant Segments:

- Type: Functional foods dominate the market, driven by consumer preference for convenient and nutrient-rich options. Dietary supplements represent a substantial segment, with growth fueled by demand for targeted health benefits. Functional beverages demonstrate significant growth potential, driven by convenience and increasing health consciousness.

- Distribution Channel: Supermarkets/hypermarkets are the largest distribution channel, offering wide product availability and accessibility. Online retail stores are experiencing rapid growth, driven by increased e-commerce penetration and convenience. Specialty stores cater to a niche market seeking premium and specialized products.

Drivers:

- Economic Growth: Rising disposable incomes lead to increased spending on health and wellness products.

- Health & Wellness Awareness: Growing awareness of chronic diseases boosts demand for preventive healthcare measures.

- Technological Advancements: Innovations in product formulation and delivery systems enhance efficacy and consumer appeal.

Dominance Analysis: The functional food segment holds the largest market share due to its broad appeal and incorporation into everyday diets. Supermarkets/hypermarkets represent the dominant distribution channel due to their extensive reach and established infrastructure.

North America Nutraceutical Industry Product Developments

The North American nutraceutical industry witnesses continuous innovation in product formats, formulations, and delivery systems. Technological advancements, such as nanotechnology for enhanced bioavailability and personalized nutrition approaches based on genetic testing and microbiome analysis, are driving product development. This leads to highly targeted nutraceuticals that offer customized health benefits, creating a competitive edge for manufacturers. The emphasis is on natural and organic ingredients, sustainable sourcing practices, and convenient formats, reflecting growing consumer preferences.

Challenges in the North America Nutraceutical Industry Market

The North America nutraceutical industry faces challenges including stringent regulatory requirements for product approval and labeling, leading to increased costs and time-to-market. Supply chain disruptions caused by geopolitical instability and natural disasters can impact ingredient availability and cost. Intense competition from both established players and emerging brands necessitates continuous innovation and efficient marketing strategies to maintain market share. These factors combined can negatively affect profitability and growth potential.

Forces Driving North America Nutraceutical Industry Growth

The North America nutraceutical industry's growth is fueled by several key factors: increasing consumer awareness of the importance of preventive healthcare; technological advancements in formulation, delivery, and personalization; favorable government regulations supporting the industry; and the growing adoption of e-commerce platforms for convenient product purchases. The rising prevalence of chronic diseases such as heart disease and diabetes further drives demand for effective nutraceutical solutions.

Long-Term Growth Catalysts in the North America Nutraceutical Industry

Long-term growth in the North American nutraceutical sector is projected to be driven by continued innovation in product development, strategic partnerships to leverage complementary expertise, and expansions into new and emerging markets. Focus on personalized nutrition solutions tailored to individual needs will further propel market expansion. Investing in research and development for more effective and safer nutraceuticals is key to long-term success.

Emerging Opportunities in North America Nutraceutical Industry

Emerging opportunities in the North American nutraceutical market include the increasing adoption of personalized nutrition strategies based on genomic and microbiome data, the expansion of product offerings into specific health conditions like gut health, cognitive function, and immune support, and the exploration of new delivery methods such as liposomes and nanotechnology for enhanced efficacy. These opportunities are expected to attract further investment and innovation in the coming years.

Leading Players in the North America Nutraceutical Industry Sector

Key Milestones in North America Nutraceutical Industry

- 2020: Increased focus on immunity-boosting supplements due to the COVID-19 pandemic.

- 2021: Several major acquisitions in the dietary supplement segment.

- 2022: Launch of several personalized nutrition products based on genetic testing.

- 2023: Growing emphasis on sustainable sourcing practices and eco-friendly packaging.

- 2024: Significant investment in R&D for new product formulations and delivery methods.

Strategic Outlook for North America Nutraceutical Industry Market

The North America nutraceutical market is poised for significant growth, fueled by ongoing innovation, expanding consumer awareness, and strategic partnerships. Future market potential lies in personalized nutrition, functional foods integration, and the exploitation of novel delivery systems. Companies that invest in research and development, focus on consumer-centric product development, and strategically navigate regulatory landscapes are expected to achieve substantial market success.

North America Nutraceutical Industry Segmentation

-

1. Type

-

1.1. Functional Food

- 1.1.1. Cereal

- 1.1.2. Bakery and Confectionery

- 1.1.3. Dairy

- 1.1.4. Snacks

- 1.1.5. Other Functional Foods

-

1.2. Functional Beverages

- 1.2.1. Energy Drinks

- 1.2.2. Sports Drinks

- 1.2.3. Fortified Juice

- 1.2.4. Dairy and Dairy Alternative Beverages

- 1.2.5. Other Functional Beverages

-

1.3. Dietary Supplements

- 1.3.1. Vitamins

- 1.3.2. Minerals

- 1.3.3. Botanicals

- 1.3.4. Enzymes

- 1.3.5. Fatty Acids

- 1.3.6. Proteins

- 1.3.7. Other Dietary Supplements

-

1.1. Functional Food

-

2. Distribution Channel

- 2.1. Specialty Stores

- 2.2. Supermarkets/Hypermarkets

- 2.3. Convenience Stores

- 2.4. Online Retail Stores

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

- 3.4. Rest of North America

North America Nutraceutical Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

North America Nutraceutical Industry Regional Market Share

Geographic Coverage of North America Nutraceutical Industry

North America Nutraceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Functional Food

- 5.1.1.1. Cereal

- 5.1.1.2. Bakery and Confectionery

- 5.1.1.3. Dairy

- 5.1.1.4. Snacks

- 5.1.1.5. Other Functional Foods

- 5.1.2. Functional Beverages

- 5.1.2.1. Energy Drinks

- 5.1.2.2. Sports Drinks

- 5.1.2.3. Fortified Juice

- 5.1.2.4. Dairy and Dairy Alternative Beverages

- 5.1.2.5. Other Functional Beverages

- 5.1.3. Dietary Supplements

- 5.1.3.1. Vitamins

- 5.1.3.2. Minerals

- 5.1.3.3. Botanicals

- 5.1.3.4. Enzymes

- 5.1.3.5. Fatty Acids

- 5.1.3.6. Proteins

- 5.1.3.7. Other Dietary Supplements

- 5.1.1. Functional Food

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Specialty Stores

- 5.2.2. Supermarkets/Hypermarkets

- 5.2.3. Convenience Stores

- 5.2.4. Online Retail Stores

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.3.4. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.4.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Nutraceutical Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Functional Food

- 6.1.1.1. Cereal

- 6.1.1.2. Bakery and Confectionery

- 6.1.1.3. Dairy

- 6.1.1.4. Snacks

- 6.1.1.5. Other Functional Foods

- 6.1.2. Functional Beverages

- 6.1.2.1. Energy Drinks

- 6.1.2.2. Sports Drinks

- 6.1.2.3. Fortified Juice

- 6.1.2.4. Dairy and Dairy Alternative Beverages

- 6.1.2.5. Other Functional Beverages

- 6.1.3. Dietary Supplements

- 6.1.3.1. Vitamins

- 6.1.3.2. Minerals

- 6.1.3.3. Botanicals

- 6.1.3.4. Enzymes

- 6.1.3.5. Fatty Acids

- 6.1.3.6. Proteins

- 6.1.3.7. Other Dietary Supplements

- 6.1.1. Functional Food

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Specialty Stores

- 6.2.2. Supermarkets/Hypermarkets

- 6.2.3. Convenience Stores

- 6.2.4. Online Retail Stores

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.3.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United States North America Nutraceutical Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Functional Food

- 7.1.1.1. Cereal

- 7.1.1.2. Bakery and Confectionery

- 7.1.1.3. Dairy

- 7.1.1.4. Snacks

- 7.1.1.5. Other Functional Foods

- 7.1.2. Functional Beverages

- 7.1.2.1. Energy Drinks

- 7.1.2.2. Sports Drinks

- 7.1.2.3. Fortified Juice

- 7.1.2.4. Dairy and Dairy Alternative Beverages

- 7.1.2.5. Other Functional Beverages

- 7.1.3. Dietary Supplements

- 7.1.3.1. Vitamins

- 7.1.3.2. Minerals

- 7.1.3.3. Botanicals

- 7.1.3.4. Enzymes

- 7.1.3.5. Fatty Acids

- 7.1.3.6. Proteins

- 7.1.3.7. Other Dietary Supplements

- 7.1.1. Functional Food

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Specialty Stores

- 7.2.2. Supermarkets/Hypermarkets

- 7.2.3. Convenience Stores

- 7.2.4. Online Retail Stores

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.3.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Canada North America Nutraceutical Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Functional Food

- 8.1.1.1. Cereal

- 8.1.1.2. Bakery and Confectionery

- 8.1.1.3. Dairy

- 8.1.1.4. Snacks

- 8.1.1.5. Other Functional Foods

- 8.1.2. Functional Beverages

- 8.1.2.1. Energy Drinks

- 8.1.2.2. Sports Drinks

- 8.1.2.3. Fortified Juice

- 8.1.2.4. Dairy and Dairy Alternative Beverages

- 8.1.2.5. Other Functional Beverages

- 8.1.3. Dietary Supplements

- 8.1.3.1. Vitamins

- 8.1.3.2. Minerals

- 8.1.3.3. Botanicals

- 8.1.3.4. Enzymes

- 8.1.3.5. Fatty Acids

- 8.1.3.6. Proteins

- 8.1.3.7. Other Dietary Supplements

- 8.1.1. Functional Food

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Specialty Stores

- 8.2.2. Supermarkets/Hypermarkets

- 8.2.3. Convenience Stores

- 8.2.4. Online Retail Stores

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.3.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Mexico North America Nutraceutical Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Functional Food

- 9.1.1.1. Cereal

- 9.1.1.2. Bakery and Confectionery

- 9.1.1.3. Dairy

- 9.1.1.4. Snacks

- 9.1.1.5. Other Functional Foods

- 9.1.2. Functional Beverages

- 9.1.2.1. Energy Drinks

- 9.1.2.2. Sports Drinks

- 9.1.2.3. Fortified Juice

- 9.1.2.4. Dairy and Dairy Alternative Beverages

- 9.1.2.5. Other Functional Beverages

- 9.1.3. Dietary Supplements

- 9.1.3.1. Vitamins

- 9.1.3.2. Minerals

- 9.1.3.3. Botanicals

- 9.1.3.4. Enzymes

- 9.1.3.5. Fatty Acids

- 9.1.3.6. Proteins

- 9.1.3.7. Other Dietary Supplements

- 9.1.1. Functional Food

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Specialty Stores

- 9.2.2. Supermarkets/Hypermarkets

- 9.2.3. Convenience Stores

- 9.2.4. Online Retail Stores

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.3.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of North America North America Nutraceutical Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Functional Food

- 10.1.1.1. Cereal

- 10.1.1.2. Bakery and Confectionery

- 10.1.1.3. Dairy

- 10.1.1.4. Snacks

- 10.1.1.5. Other Functional Foods

- 10.1.2. Functional Beverages

- 10.1.2.1. Energy Drinks

- 10.1.2.2. Sports Drinks

- 10.1.2.3. Fortified Juice

- 10.1.2.4. Dairy and Dairy Alternative Beverages

- 10.1.2.5. Other Functional Beverages

- 10.1.3. Dietary Supplements

- 10.1.3.1. Vitamins

- 10.1.3.2. Minerals

- 10.1.3.3. Botanicals

- 10.1.3.4. Enzymes

- 10.1.3.5. Fatty Acids

- 10.1.3.6. Proteins

- 10.1.3.7. Other Dietary Supplements

- 10.1.1. Functional Food

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Specialty Stores

- 10.2.2. Supermarkets/Hypermarkets

- 10.2.3. Convenience Stores

- 10.2.4. Online Retail Stores

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. United States

- 10.3.2. Canada

- 10.3.3. Mexico

- 10.3.4. Rest of North America

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Nestle SA

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 The Kellogg Company

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Herbalife International of America Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Red Bull GmbH*List Not Exhaustive

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 General Mills Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 PepsiCo Inc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Amway Corp

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Abbott Laboratories

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Nature's Bounty Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Pfizer Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Nestle SA

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: North America Nutraceutical Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Nutraceutical Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Nutraceutical Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Nutraceutical Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: North America Nutraceutical Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: North America Nutraceutical Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: North America Nutraceutical Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: North America Nutraceutical Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 7: North America Nutraceutical Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 8: North America Nutraceutical Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: North America Nutraceutical Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: North America Nutraceutical Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: North America Nutraceutical Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: North America Nutraceutical Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: North America Nutraceutical Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: North America Nutraceutical Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: North America Nutraceutical Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: North America Nutraceutical Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: North America Nutraceutical Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: North America Nutraceutical Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 19: North America Nutraceutical Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: North America Nutraceutical Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Nutraceutical Industry?

The projected CAGR is approximately 7.7%.

2. Which companies are prominent players in the North America Nutraceutical Industry?

Key companies in the market include Nestle SA, The Kellogg Company, Herbalife International of America Inc, Red Bull GmbH*List Not Exhaustive, General Mills Inc, PepsiCo Inc, Amway Corp, Abbott Laboratories, Nature's Bounty Inc, Pfizer Inc.

3. What are the main segments of the North America Nutraceutical Industry?

The market segments include Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 636.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Popularity of On-the-Go Snacking Options; Trend Of Clean Label and Plant-Based Bars.

6. What are the notable trends driving market growth?

Growing Efficacy of Functional Foods and their Botanical Active Ingredients.

7. Are there any restraints impacting market growth?

Availability of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Nutraceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Nutraceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Nutraceutical Industry?

To stay informed about further developments, trends, and reports in the North America Nutraceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence