Key Insights

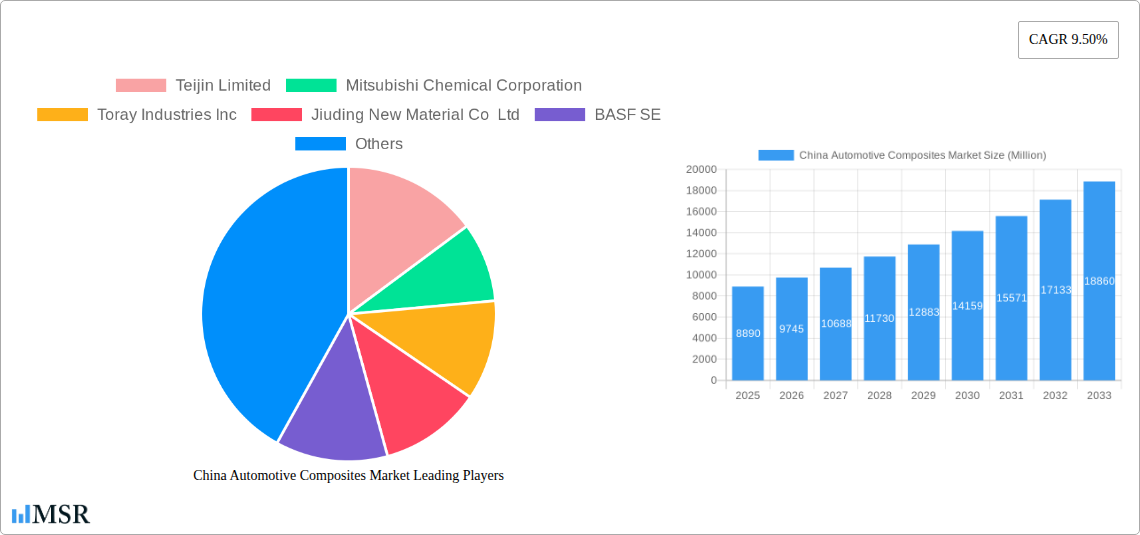

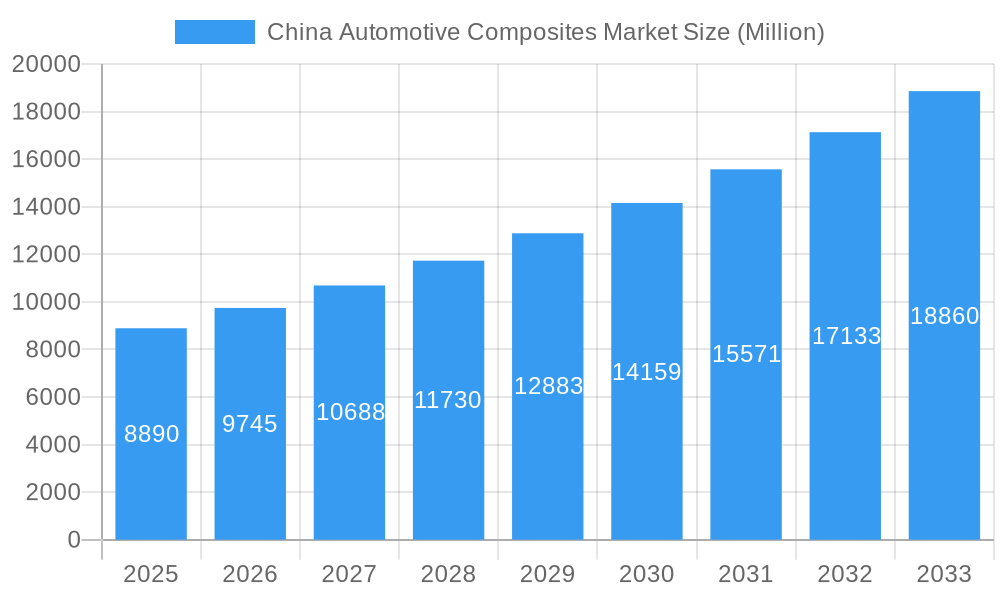

The China automotive composites market, valued at $8.89 billion in 2025, is projected to experience robust growth, driven by the increasing adoption of lightweight materials in vehicles to improve fuel efficiency and performance. The market's Compound Annual Growth Rate (CAGR) of 9.5% from 2025 to 2033 signifies significant expansion. Key drivers include stringent government regulations promoting fuel efficiency and emission reduction, coupled with the burgeoning electric vehicle (EV) sector in China. The growing demand for lightweight, high-strength composites in passenger cars and commercial vehicles further fuels market growth. Specific segments like battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) are anticipated to witness exceptionally high growth rates due to their reliance on lightweight components for extended range and reduced energy consumption. Material innovations, particularly in carbon fiber and thermoplastic polymers, are expected to contribute to market expansion. However, the high cost of some composite materials and the complex manufacturing processes associated with certain types of composites could pose challenges to market penetration. The dominance of thermoset polymers currently is likely to gradually shift toward a higher share for thermoplastics due to their recyclability and cost-effectiveness. Leading players like Teijin Limited, Mitsubishi Chemical Corporation, and Toray Industries Inc. are investing heavily in R&D and strategic partnerships to consolidate their market positions and capitalize on the burgeoning opportunities within this sector.

China Automotive Composites Market Market Size (In Billion)

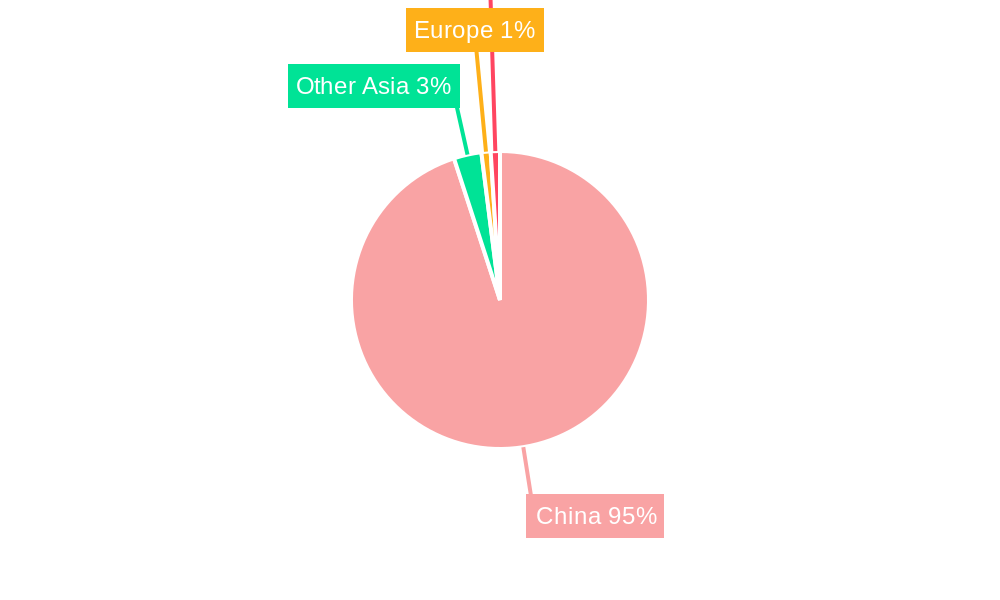

The regional dominance of China in this market is undeniable, reflecting the country's robust automotive industry and significant government support for technological advancements in the automotive sector. The market segmentation by process type (hand layup, resin transfer molding, etc.), and application (structural assembly, powertrain components, etc.) presents diverse avenues for growth. While challenges remain in terms of cost and manufacturing complexity, the long-term outlook for the China automotive composites market remains exceptionally positive, fueled by continuous innovation, favorable government policies, and the ongoing expansion of the Chinese automotive industry. The forecast period of 2025-2033 promises substantial market growth, with opportunities for both established players and new entrants focused on advanced material technologies and sustainable manufacturing practices.

China Automotive Composites Market Company Market Share

China Automotive Composites Market: A Comprehensive Analysis (2019-2033)

This in-depth report provides a comprehensive analysis of the burgeoning China automotive composites market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. Spanning the period 2019-2033, with a focus on 2025, this report meticulously examines market dynamics, growth drivers, key players, and emerging opportunities within this rapidly evolving sector. The market is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033).

China Automotive Composites Market Market Concentration & Dynamics

The China automotive composites market showcases a moderately concentrated landscape, with several major players holding significant market share. Key players such as Teijin Limited, Mitsubishi Chemical Corporation, and Toray Industries Inc. dominate the market, leveraging their technological prowess and established supply chains. However, the presence of several regional and emerging players fosters a dynamic competitive environment. Market concentration is further influenced by ongoing mergers and acquisitions (M&A) activities, with xx M&A deals recorded between 2019 and 2024.

- Market Share: Top 5 players account for approximately xx% of the total market share in 2025.

- Innovation Ecosystem: Strong government support for R&D in lightweight materials and electric vehicles fuels innovation within the sector. Collaborative ventures between automotive manufacturers and composite material suppliers are common.

- Regulatory Framework: Government regulations promoting fuel efficiency and emission reduction drive demand for lightweight composites. Stricter environmental standards also influence material selection and manufacturing processes.

- Substitute Products: Steel and aluminum remain primary competitors, but the increasing demand for fuel efficiency and design flexibility is pushing the adoption of composites.

- End-User Trends: The rising popularity of electric vehicles (EVs) and hybrid electric vehicles (HEVs) significantly boosts the demand for lightweight and high-performance composites. The preference for advanced vehicle features fuels demand in the interior and exterior applications.

- M&A Activities: Consolidation within the industry is expected to intensify as major players seek to expand their market reach and technological capabilities. This trend will further shape market dynamics and competitive intensity.

China Automotive Composites Market Industry Insights & Trends

The China automotive composites market is experiencing robust growth, driven by a confluence of factors. The increasing adoption of lightweight materials in automobiles to improve fuel efficiency and reduce emissions plays a significant role. The government's emphasis on developing the domestic automotive industry and its supportive policies are further accelerating market expansion. Technological advancements in composite materials, such as the development of high-strength carbon fiber, are enhancing their performance characteristics and applications. Consumer preference for enhanced vehicle aesthetics and safety also contributes to market growth. The market size in 2025 is estimated at xx Million, exhibiting a remarkable CAGR of xx% between 2019 and 2025.

Key Markets & Segments Leading China Automotive Composites Market

The passenger car segment dominates the China automotive composites market, accounting for approximately xx% of the total market value in 2025. However, the commercial vehicle segment is projected to witness faster growth during the forecast period, driven by increasing demand for fuel-efficient heavy-duty vehicles. Geographically, the eastern and coastal regions are leading the market, while western regions are showing strong growth potential.

Key Growth Drivers:

- Rapid Economic Growth: Increased disposable incomes and automotive sales propel market demand.

- Stringent Emission Regulations: Government mandates push the adoption of lightweight materials.

- Expanding Automotive Production: China's massive automotive manufacturing base provides a fertile ground for growth.

- Technological Advancements: Continuous innovations in composite materials expand their application possibilities.

Dominance Analysis:

- By Propulsion: Battery Electric Vehicles (BEVs) and Hybrid Electric Vehicles (HEVs) segments are expected to exhibit the highest growth due to increasing environmental concerns and government incentives.

- By Process Type: Resin Transfer Molding (RTM) and Injection Molding are widely adopted due to their ability to produce high-volume, high-quality composite parts efficiently.

- By Material Type: Carbon fiber reinforced polymers (CFRP) are gaining traction, especially in high-performance automotive applications, while glass fiber remains dominant in cost-sensitive applications.

- By Application: The structural assembly segment holds the largest market share, followed by powertrain components and interior applications.

- By Vehicle Type: Passenger cars dominate, though commercial vehicles are a rapidly growing segment.

China Automotive Composites Market Product Developments

Recent product innovations highlight the ongoing drive for enhanced performance and cost-effectiveness. Toray Industries' development of TORAYCA T1200 carbon fiber in October 2023 marks a significant advancement in strength and lightweighting capabilities. Similarly, Mitsubishi Chemical Group's collaboration with Honda on polymethyl methacrylate (acrylic resin) for automotive body parts expands material options for improved durability and aesthetics. These advancements signify a trend toward lighter, stronger, and more cost-effective composite solutions for automotive applications.

Challenges in the China Automotive Composites Market Market

The China automotive composites market faces several challenges. High raw material costs, particularly for carbon fiber, can impact profitability. Supply chain disruptions and geopolitical uncertainties pose risks to material availability and pricing. Intense competition among established and emerging players requires continuous innovation and cost optimization. Furthermore, strict environmental regulations necessitate compliance with stringent emission standards and waste management practices.

Forces Driving China Automotive Composites Market Growth

Technological advancements in composite materials, coupled with rising demand for fuel-efficient and lightweight vehicles, are major growth drivers. Government initiatives supporting the electric vehicle industry and promoting the use of advanced materials significantly influence market expansion. Furthermore, increasing consumer preference for improved vehicle design, performance, and safety characteristics drives the adoption of composite components.

Challenges in the China Automotive Composites Market Market

Long-term growth is predicated on continued innovation in composite materials, reducing production costs, and establishing robust supply chains. Strategic partnerships between material suppliers and automakers are crucial for technology transfer and market penetration. Expanding into new market segments and exploring niche applications will further fuel long-term expansion.

Emerging Opportunities in China Automotive Composites Market

Emerging opportunities include the growth of electric vehicles and the expansion of composite applications into new vehicle segments. The development of sustainable and recyclable composite materials represents a significant opportunity for environmentally conscious manufacturers. Exploring advanced manufacturing techniques such as 3D printing for composites could further open new avenues for product innovation and customization.

Leading Players in the China Automotive Composites Market Sector

- Teijin Limited

- Mitsubishi Chemical Corporation

- Toray Industries Inc

- Jiuding New Material Co Ltd

- BASF SE

- ALPEX Technologies Gmb

- SGL Group SE

- Hexcel Corporation

- Nipposn Sheet Glass Co Ltd

Key Milestones in China Automotive Composites Market Industry

- October 2023: Toray Industries, Inc. developed TORAYCA T1200 carbon fiber, significantly boosting material strength.

- October 2023: Mitsubishi Chemical Group and Honda Motor Company jointly developed a new polymethyl methacrylate (acrylic resin) material for automotive body parts, enhancing material options for automotive body parts manufacturing.

Strategic Outlook for China Automotive Composites Market Market

The China automotive composites market presents substantial growth potential over the next decade. Strategic partnerships, technological advancements, and continued government support are crucial for unlocking this potential. Focusing on cost-effective manufacturing, sustainable materials, and expanding into new applications will be key to long-term success in this dynamic and evolving market.

China Automotive Composites Market Segmentation

-

1. Vehicle Type

- 1.1. Passenger Car

- 1.2. Commercial Vehicles

-

2. Propulsion

- 2.1. Internal Combustion Engine

- 2.2. Battery Electric Vehicles

- 2.3. Hybrid Electric Vehicles

- 2.4. Plug-in Hybrid Electric Vehicles

- 2.5. Fuel Cell Electric Vehicles

-

3. Process Type

- 3.1. Hand Layup

- 3.2. Resin Transfer Molding

- 3.3. Vacuum Infusion Processing

- 3.4. Injection Molding

- 3.5. Compression Molding

-

4. Material Type

- 4.1. Thermoset Polymer

- 4.2. Thermoplastic Polymer

- 4.3. Carbon Fiber

- 4.4. Glass Fiber

- 4.5. Others

-

5. Application

- 5.1. Structural Assembly

- 5.2. Power train Component

- 5.3. Interior

- 5.4. Exterior

- 5.5. Others

China Automotive Composites Market Segmentation By Geography

- 1. China

China Automotive Composites Market Regional Market Share

Geographic Coverage of China Automotive Composites Market

China Automotive Composites Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.50% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Propulsion

- 5.2.1. Internal Combustion Engine

- 5.2.2. Battery Electric Vehicles

- 5.2.3. Hybrid Electric Vehicles

- 5.2.4. Plug-in Hybrid Electric Vehicles

- 5.2.5. Fuel Cell Electric Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Process Type

- 5.3.1. Hand Layup

- 5.3.2. Resin Transfer Molding

- 5.3.3. Vacuum Infusion Processing

- 5.3.4. Injection Molding

- 5.3.5. Compression Molding

- 5.4. Market Analysis, Insights and Forecast - by Material Type

- 5.4.1. Thermoset Polymer

- 5.4.2. Thermoplastic Polymer

- 5.4.3. Carbon Fiber

- 5.4.4. Glass Fiber

- 5.4.5. Others

- 5.5. Market Analysis, Insights and Forecast - by Application

- 5.5.1. Structural Assembly

- 5.5.2. Power train Component

- 5.5.3. Interior

- 5.5.4. Exterior

- 5.5.5. Others

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. China

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. China Automotive Composites Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Propulsion

- 6.2.1. Internal Combustion Engine

- 6.2.2. Battery Electric Vehicles

- 6.2.3. Hybrid Electric Vehicles

- 6.2.4. Plug-in Hybrid Electric Vehicles

- 6.2.5. Fuel Cell Electric Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Process Type

- 6.3.1. Hand Layup

- 6.3.2. Resin Transfer Molding

- 6.3.3. Vacuum Infusion Processing

- 6.3.4. Injection Molding

- 6.3.5. Compression Molding

- 6.4. Market Analysis, Insights and Forecast - by Material Type

- 6.4.1. Thermoset Polymer

- 6.4.2. Thermoplastic Polymer

- 6.4.3. Carbon Fiber

- 6.4.4. Glass Fiber

- 6.4.5. Others

- 6.5. Market Analysis, Insights and Forecast - by Application

- 6.5.1. Structural Assembly

- 6.5.2. Power train Component

- 6.5.3. Interior

- 6.5.4. Exterior

- 6.5.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Teijin Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mitsubishi Chemical Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toray Industries Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Jiuding New Material Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BASF SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 ALPEX Technologies Gmb

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 SGL Group SE

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Hexcel Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Nipposn Sheet Glass Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Teijin Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Automotive Composites Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Automotive Composites Market Share (%) by Company 2025

List of Tables

- Table 1: China Automotive Composites Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: China Automotive Composites Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 3: China Automotive Composites Market Revenue Million Forecast, by Process Type 2020 & 2033

- Table 4: China Automotive Composites Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 5: China Automotive Composites Market Revenue Million Forecast, by Application 2020 & 2033

- Table 6: China Automotive Composites Market Revenue Million Forecast, by Region 2020 & 2033

- Table 7: China Automotive Composites Market Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 8: China Automotive Composites Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 9: China Automotive Composites Market Revenue Million Forecast, by Process Type 2020 & 2033

- Table 10: China Automotive Composites Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 11: China Automotive Composites Market Revenue Million Forecast, by Application 2020 & 2033

- Table 12: China Automotive Composites Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Automotive Composites Market?

The projected CAGR is approximately 9.50%.

2. Which companies are prominent players in the China Automotive Composites Market?

Key companies in the market include Teijin Limited, Mitsubishi Chemical Corporation, Toray Industries Inc, Jiuding New Material Co Ltd, BASF SE, ALPEX Technologies Gmb, SGL Group SE, Hexcel Corporation, Nipposn Sheet Glass Co Ltd.

3. What are the main segments of the China Automotive Composites Market?

The market segments include Vehicle Type, Propulsion, Process Type, Material Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.89 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Lightweight Materials.

6. What are the notable trends driving market growth?

Passenger Car Hold Major Growth.

7. Are there any restraints impacting market growth?

High Expenses of Composite Processing and Manufacturing.

8. Can you provide examples of recent developments in the market?

In October 2023, Toray Industries, Inc. developed TORAYCA T1200 carbon fiber, which boasts the highest strength of 1,160 kilopounds per square inch (Ksi). This advancement will aid us in reducing our environmental footprint by using lighter carbon-fiber-reinforced plastic materials.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Automotive Composites Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Automotive Composites Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Automotive Composites Market?

To stay informed about further developments, trends, and reports in the China Automotive Composites Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence