Key Insights

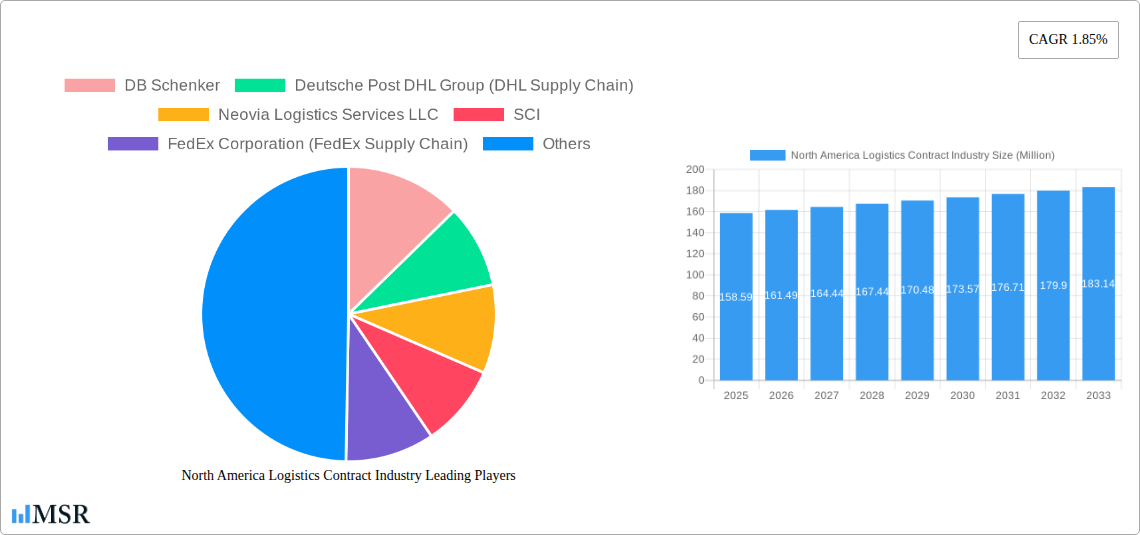

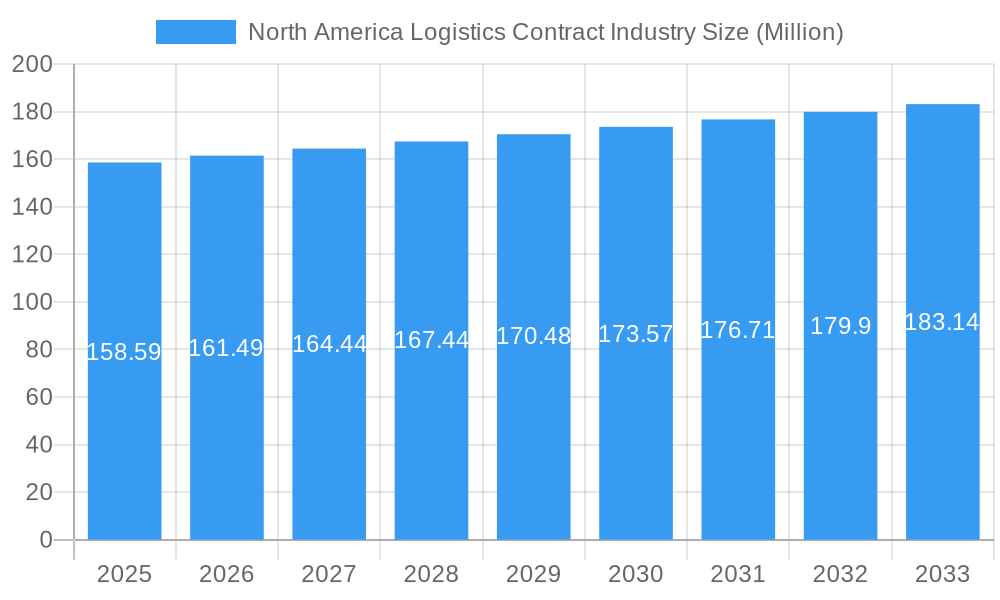

The North American Logistics Contract market is poised for steady growth, projected to reach $158.59 million in 2025. This expansion is driven by the increasing demand for efficient supply chain management across various industries, including manufacturing, automotive, consumer goods, retail, high-tech, and healthcare. Companies are increasingly recognizing the strategic advantages of outsourcing logistics functions to specialized providers, enabling them to focus on core competencies and improve operational agility. The market is witnessing a significant trend towards sophisticated, technology-driven solutions, encompassing advanced tracking, real-time visibility, and data analytics, which are crucial for optimizing complex supply chains and mitigating risks. Furthermore, the growing e-commerce sector is a substantial catalyst, necessitating faster and more reliable delivery services, which contract logistics providers are well-equipped to offer.

North America Logistics Contract Industry Market Size (In Million)

Despite a modest Compound Annual Growth Rate (CAGR) of 1.85% projected over the forecast period (2025-2033), the North American logistics contract market is characterized by a dynamic competitive landscape. Key players like DB Schenker, Deutsche Post DHL Group (DHL Supply Chain), and FedEx Corporation are investing heavily in expanding their service portfolios and technological capabilities to cater to evolving client needs. While the market benefits from strong demand drivers, potential restraints such as rising operational costs, labor shortages, and increasing regulatory complexities could moderate growth. The segment of "Outsourced" logistics is expected to dominate as businesses prioritize cost-efficiency and specialized expertise. North America, with its robust industrial base and advanced infrastructure, is a central hub for these operations, with the United States leading the market share within the region.

North America Logistics Contract Industry Company Market Share

North America Logistics Contract Industry: Market Insights, Trends & Future Outlook (2019-2033)

This comprehensive report delves into the dynamic North America Logistics Contract Industry, offering in-depth analysis of market concentration, growth drivers, key segments, and strategic outlook. Covering the historical period of 2019-2024, base year 2025, and a forecast period extending to 2033, this study provides actionable insights for industry stakeholders seeking to capitalize on evolving market trends and technological advancements. With an estimated market size projected to reach xx Million by 2025, and a CAGR of xx%, this report is your essential guide to navigating the competitive landscape of contract logistics in North America.

North America Logistics Contract Industry Market Concentration & Dynamics

The North America Logistics Contract Industry exhibits a moderately concentrated market structure, with a few dominant players holding significant market share. Innovation ecosystems are flourishing, driven by advancements in automation, AI, and data analytics, fostering greater efficiency and visibility across supply chains. Regulatory frameworks, while generally supportive of trade, can present regional variations impacting cross-border logistics. Substitute products, such as in-house logistics operations, are diminishing as businesses increasingly recognize the cost-effectiveness and specialized expertise offered by contract logistics providers. End-user trends are shifting towards greater demand for specialized services in sectors like Healthcare and Pharmaceuticals and High-tech. Mergers and acquisitions (M&A) activity remains robust, with an estimated xx M&A deals recorded in the historical period, signaling consolidation and strategic expansion by leading companies. Key metrics reveal market share for the top 5 players is approximately xx%.

North America Logistics Contract Industry Industry Insights & Trends

The North America Logistics Contract Industry is poised for substantial growth, driven by a confluence of factors including robust economic activity, expanding e-commerce penetration, and increasing demand for supply chain optimization. The market size, estimated at xx Million in 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025-2033. Technological disruptions are at the forefront of this evolution, with the widespread adoption of Warehouse Management Systems (WMS), Transportation Management Systems (TMS), and the burgeoning integration of AI and automation in warehousing and last-mile delivery. Evolving consumer behaviors, characterized by an insatiable appetite for faster delivery times and personalized logistics experiences, are compelling contract logistics providers to innovate and enhance their service offerings. The increasing complexity of global supply chains also necessitates more sophisticated and flexible logistics solutions, further fueling demand for contract services. Furthermore, the growing emphasis on sustainability is driving the adoption of green logistics practices, including route optimization for fuel efficiency and the use of electric vehicles, creating new avenues for service differentiation. The industry is witnessing a significant shift towards predictive analytics to anticipate demand fluctuations and optimize inventory management, thereby minimizing waste and enhancing customer satisfaction. The rise of omnichannel retail strategies necessitates integrated logistics networks capable of seamlessly managing inventory across various sales channels, a core competency of advanced contract logistics providers.

Key Markets & Segments Leading North America Logistics Contract Industry

The Outsourced segment is a dominant force within the North America Logistics Contract Industry, accounting for an estimated xx% of the market share. This dominance is fueled by businesses of all sizes seeking to leverage the expertise, scalability, and cost efficiencies offered by third-party logistics (3PL) providers, allowing them to focus on their core competencies.

- Drivers of Outsourced Segment Dominance:

- Cost Savings: Outsourcing eliminates the need for capital investment in infrastructure, technology, and personnel, leading to significant operational cost reductions.

- Scalability and Flexibility: Businesses can easily scale their logistics operations up or down based on seasonal demand or market fluctuations without incurring fixed costs.

- Access to Expertise and Technology: 3PL providers offer specialized knowledge in warehousing, transportation, and supply chain management, along with access to advanced technologies that individual companies may not possess.

- Improved Efficiency and Speed: Contract logistics specialists often implement optimized processes and technologies that lead to faster order fulfillment and delivery times.

Among end-users, the Consumer Goods and Retail sector represents a leading segment, contributing approximately xx% to the overall market revenue. This is directly attributable to the rapid growth of e-commerce, the increasing complexity of retail supply chains, and the constant pressure to meet consumer demands for faster and more convenient delivery options.

- Drivers of Consumer Goods and Retail Segment Dominance:

- E-commerce Boom: The exponential growth of online retail necessitates robust and efficient logistics solutions for order fulfillment, warehousing, and last-mile delivery.

- Omnichannel Strategies: Retailers are increasingly adopting omnichannel approaches, requiring integrated logistics networks to manage inventory and fulfill orders across online and brick-and-mortar channels.

- Demand for Fast and Flexible Delivery: Consumers expect rapid delivery times and flexible options, pushing retailers to partner with logistics providers who can meet these expectations.

- Inventory Management Complexity: Managing diverse product assortments and fluctuating demand requires sophisticated inventory management and warehousing solutions.

The Manufacturing and Automotive sector also holds significant sway, contributing an estimated xx% to the market. This segment benefits from the industry's need for specialized transportation, just-in-time inventory management, and the complexities of global supply chains for components and finished goods.

- Drivers of Manufacturing and Automotive Segment Dominance:

- Just-In-Time (JIT) Manufacturing: The reliance on JIT principles requires precise and reliable logistics to ensure timely delivery of components to production lines.

- Global Supply Chains: Automotive and manufacturing companies often operate with intricate global supply networks, demanding expert management of international shipping, customs, and warehousing.

- Specialized Handling Requirements: Certain manufactured goods and automotive parts require specialized handling, storage, and transportation, which contract logistics providers are equipped to offer.

- Reverse Logistics: Managing returns, repairs, and recalls for manufactured goods and vehicles is a critical function facilitated by specialized logistics services.

The Healthcare and Pharmaceuticals sector, though representing a smaller but rapidly growing segment (xx%), is a critical area of focus due to its stringent regulatory requirements, the need for temperature-controlled logistics, and the increasing demand for pharmaceutical and medical device distribution.

- Drivers of Healthcare and Pharmaceuticals Segment Growth:

- Strict Regulatory Compliance: The sector demands adherence to rigorous regulations, necessitating specialized logistics providers with expertise in compliance and handling of sensitive goods.

- Temperature-Controlled Logistics: Many pharmaceutical and medical products require precise temperature control throughout the supply chain, a service offered by specialized contract logistics companies.

- Growing Healthcare Demands: An aging population and advancements in medical treatments are driving increased demand for pharmaceuticals and medical devices, thereby boosting logistics needs.

- Cold Chain Integrity: Maintaining the integrity of the cold chain from manufacturing to patient delivery is paramount and requires sophisticated logistics solutions.

North America Logistics Contract Industry Product Developments

Innovations in the North America Logistics Contract Industry are primarily centered around the integration of advanced technologies to enhance efficiency, visibility, and sustainability. This includes the deployment of autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) in warehouses for optimized picking and sorting, as demonstrated by DHL's significant use of LocusBots. Furthermore, the development of sophisticated data analytics platforms powered by AI and machine learning enables predictive logistics, real-time tracking, and proactive issue resolution. Cloud-based transportation management systems are becoming standard, offering seamless integration across supply chain partners. The market is also seeing advancements in sustainable logistics solutions, such as electric vehicle fleets for last-mile delivery and route optimization software to minimize carbon emissions, contributing to competitive edges and increased market relevance.

Challenges in the North America Logistics Contract Industry Market

The North America Logistics Contract Industry faces several significant challenges, including:

- Labor Shortages: A persistent shortage of skilled truck drivers and warehouse personnel impacts operational capacity and increases labor costs.

- Rising Fuel Costs: Volatile fuel prices directly affect transportation expenses, squeezing profit margins for logistics providers.

- Supply Chain Disruptions: Geopolitical events, natural disasters, and unexpected demand surges can lead to significant disruptions, causing delays and increased costs.

- Cybersecurity Threats: The increasing reliance on digital systems makes the industry vulnerable to cyberattacks, posing risks to data integrity and operational continuity.

- Infrastructure Bottlenecks: Congested ports, aging road networks, and limited rail capacity can create significant delays and inefficiencies.

Forces Driving North America Logistics Contract Industry Growth

Several key forces are propelling the growth of the North America Logistics Contract Industry. The relentless expansion of e-commerce continues to be a primary driver, necessitating more sophisticated and efficient fulfillment and delivery solutions. Technological advancements, particularly in automation, AI, and data analytics, are enabling greater operational efficiency, reduced costs, and enhanced visibility across supply chains. Furthermore, the increasing complexity of global supply chains and the growing demand for specialized logistics services, such as cold chain management and last-mile delivery, are compelling businesses to outsource these functions to expert contract logistics providers. Economic growth and increasing consumer spending power further contribute to higher demand for goods and, consequently, for logistics services.

Challenges in the North America Logistics Contract Industry Market

Long-term growth catalysts within the North America Logistics Contract Industry are deeply rooted in continuous innovation and strategic market expansion. The ongoing development and adoption of advanced technologies like blockchain for enhanced transparency and traceability in supply chains, and the further integration of IoT devices for real-time asset monitoring, are crucial. Partnerships and collaborations between logistics providers, technology firms, and end-users are fostering new service models and customized solutions. Market expansions into emerging regions and the development of specialized logistics offerings for niche industries, such as biotechnology and renewable energy, are also significant growth accelerators. The increasing focus on sustainability and the development of circular economy logistics solutions will further shape future growth trajectories.

Emerging Opportunities in North America Logistics Contract Industry

Emerging opportunities in the North America Logistics Contract Industry are abundant and diverse. The growing demand for sustainable and green logistics solutions presents a significant avenue for growth, with companies investing in electric vehicle fleets and optimizing routes for reduced emissions. The expansion of cross-border e-commerce, particularly between North America and other regions, creates opportunities for specialized international shipping and customs brokerage services. The increasing need for temperature-controlled logistics for pharmaceuticals, medical devices, and perishable goods offers a niche but high-value market. Furthermore, the development of end-to-end supply chain visibility solutions leveraging IoT and AI is creating opportunities for providers to offer integrated data management and analytics services, enhancing predictive capabilities and operational efficiency for their clients. The rise of direct-to-consumer (DTC) models in various sectors also necessitates flexible and agile last-mile delivery solutions.

Leading Players in the North America Logistics Contract Industry Sector

- DB Schenker

- Deutsche Post DHL Group (DHL Supply Chain)

- Neovia Logistics Services LLC

- SCI

- FedEx Corporation (FedEx Supply Chain)

- United Parcel Service Inc (UPS Supply Chain Solutions)

- Schnedier National

- Yusen Logistics Co Ltd

- Penske Logistics Inc

- Kuehne + Nagel International AG

- CEVA Logistics

- PiVAL International

- TIBA

- XPO Logistics Inc

- Americold

- Hellmann Worldwide Logistics GmbH & Co KG

- Geodis

- J B Hunt Transport Services Inc

- Ryder System Inc

Key Milestones in North America Logistics Contract Industry Industry

- June 2022: DHL Supply Chain, a division of Deutsche Post DHL Group and a leader in contract logistics in the Americas, announced that its North American facilities, utilizing LocusBots from Locus Robotics, had processed over 100 million units. This significant achievement occurred at the DHL facility in Hanover Township, Pennsylvania, while fulfilling orders for a major apparel retailer. This facility is one of over a dozen DHL locations in North America employing more than 2,000 LocusBots, more than any other contract logistics provider.

- February 2022: The Life Sciences and Healthcare (LSHC) sector of Deutsche Post DHL Group announced an investment exceeding USD 400 million to expand its pharmaceutical and medical device distribution network by 27% in the current year, adding nearly 3 million square feet. DHL Supply Chain, a global and North American contract logistics leader, plans to establish six new US sites by the end of 2022. This investment aims to bring essential healthcare supplies closer to business partners and patients and covers the costs of outfitting and launching new or expanded operations, as well as investing in new infrastructure and technologies.

Strategic Outlook for North America Logistics Contract Industry Market

The strategic outlook for the North America Logistics Contract Industry is exceptionally strong, driven by sustained demand for efficient, agile, and technology-enabled supply chain solutions. Key growth accelerators include the continued expansion of e-commerce, the increasing complexity of global trade, and the growing imperative for supply chain resilience and sustainability. Companies that can effectively integrate advanced technologies such as AI, automation, and IoT will be best positioned to capture market share. Strategic partnerships, mergers, and acquisitions will continue to shape the competitive landscape, leading to consolidation and the emergence of integrated service providers. Focus on developing specialized logistics capabilities, particularly in high-growth sectors like healthcare and pharmaceuticals, and investing in green logistics initiatives will be paramount for long-term success and market leadership. The industry's ability to adapt to evolving consumer expectations and regulatory changes will dictate its future trajectory.

North America Logistics Contract Industry Segmentation

-

1. Type

- 1.1. Insourced

- 1.2. Outsourced

-

2. End User

- 2.1. Manufacturing and Automotive

- 2.2. Consumer Goods and Retail

- 2.3. High-tech

- 2.4. Healthcare and Pharmaceuticals

- 2.5. Other End Users

North America Logistics Contract Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

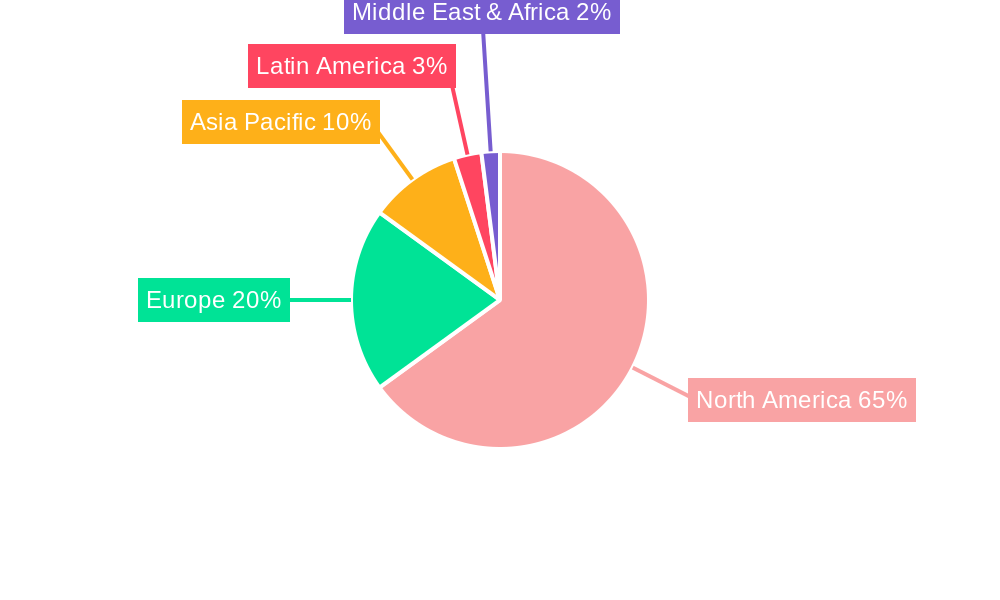

North America Logistics Contract Industry Regional Market Share

Geographic Coverage of North America Logistics Contract Industry

North America Logistics Contract Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Insourced

- 5.1.2. Outsourced

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Manufacturing and Automotive

- 5.2.2. Consumer Goods and Retail

- 5.2.3. High-tech

- 5.2.4. Healthcare and Pharmaceuticals

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Logistics Contract Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Insourced

- 6.1.2. Outsourced

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Manufacturing and Automotive

- 6.2.2. Consumer Goods and Retail

- 6.2.3. High-tech

- 6.2.4. Healthcare and Pharmaceuticals

- 6.2.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Deutsche Post DHL Group (DHL Supply Chain)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Neovia Logistics Services LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 SCI

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FedEx Corporation (FedEx Supply Chain)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 United Parcel Service Inc (UPS Supply Chain Solutions)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Schnedier National*6 3 Other Companies (Key Information/Overview)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yusen Logistics Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Penske Logistics Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Kuehne + Nagel International AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 CEVA Logistics

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 PiVAL International

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 TIBA

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 XPO Logistics Inc

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Americold

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Hellmann Worldwide Logistics GmbH & Co KG

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Geodis

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 J B Hunt Transport Services Inc

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Ryder System Inc

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Logistics Contract Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Logistics Contract Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Logistics Contract Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: North America Logistics Contract Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: North America Logistics Contract Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: North America Logistics Contract Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: North America Logistics Contract Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: North America Logistics Contract Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Logistics Contract Industry?

The projected CAGR is approximately 1.85%.

2. Which companies are prominent players in the North America Logistics Contract Industry?

Key companies in the market include DB Schenker, Deutsche Post DHL Group (DHL Supply Chain), Neovia Logistics Services LLC, SCI, FedEx Corporation (FedEx Supply Chain), United Parcel Service Inc (UPS Supply Chain Solutions), Schnedier National*6 3 Other Companies (Key Information/Overview), Yusen Logistics Co Ltd, Penske Logistics Inc, Kuehne + Nagel International AG, CEVA Logistics, PiVAL International, TIBA, XPO Logistics Inc, Americold, Hellmann Worldwide Logistics GmbH & Co KG, Geodis, J B Hunt Transport Services Inc, Ryder System Inc.

3. What are the main segments of the North America Logistics Contract Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 158.59 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increased Outsourcing of Services4.; Increasing Demand For Contract Logistics In Italy. France. And Poland4.; Growth Of Ecommerce Sector Across Europe.

6. What are the notable trends driving market growth?

Growing E-commerce in the Region Driving the Contract Logistics Market.

7. Are there any restraints impacting market growth?

4.; Increasing Competition In The European Contract Logistics Market.

8. Can you provide examples of recent developments in the market?

Jun 2022: DHL Supply Chain, in contract logistics in the Americas and a division of Deutsche Post DHL Group, revealed that LocusBots from Locus Robotics had selected more than 100 million units in its North American facilities. The achievement was made at the DHL facility in Hanover Township, Pennsylvania, while completing orders for a significant clothes retailer. The facility where the milestone was reached is one of over a dozen DHL locations in North America that employ more than 2,000 LocusBots-more than any other contract logistics provider.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Logistics Contract Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Logistics Contract Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Logistics Contract Industry?

To stay informed about further developments, trends, and reports in the North America Logistics Contract Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence