Key Insights

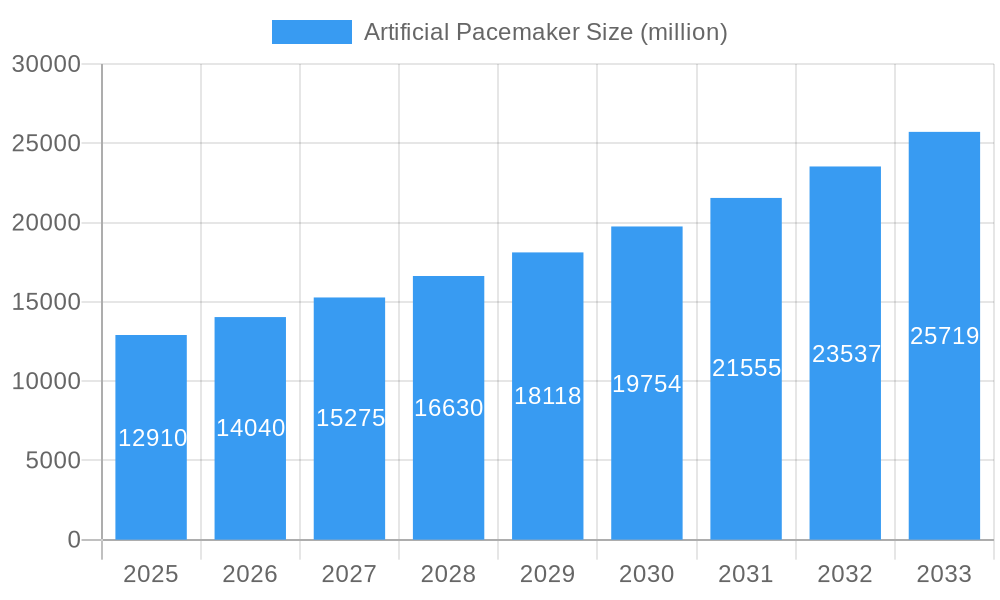

The global artificial pacemaker market is poised for significant expansion, projected to reach USD 12.91 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 9.7% anticipated throughout the forecast period of 2025-2033. This impressive growth is fueled by several key drivers, including the increasing prevalence of cardiovascular diseases, particularly bradycardia and atrial fibrillation, which necessitate pacing therapies. Advances in pacemaker technology, such as miniaturization, improved battery life, and the development of leadless pacemakers, are enhancing patient outcomes and driving adoption. Furthermore, an aging global population, with its inherent susceptibility to heart conditions, contributes substantially to market demand. The growing awareness of the benefits of cardiac pacing and the expanding healthcare infrastructure in emerging economies further bolster market prospects.

Artificial Pacemaker Market Size (In Billion)

The market is segmented by application into bradycardia, atrial fibrillation, heart failure, and syncope, with each segment experiencing growth driven by specific patient needs and therapeutic advancements. Temporary cardiac pacing, single-chamber, and double-chamber cardiac pacing represent the key types, with ongoing innovation aimed at providing more personalized and effective treatment solutions. Leading companies such as Medtronic, Abbott, and Boston Scientific are at the forefront of this dynamic market, investing heavily in research and development to introduce next-generation devices. Geographically, North America and Europe currently dominate the market due to established healthcare systems and high adoption rates of advanced medical technologies. However, the Asia Pacific region is expected to witness the fastest growth, driven by increasing healthcare expenditure, a large patient pool, and government initiatives promoting cardiovascular health.

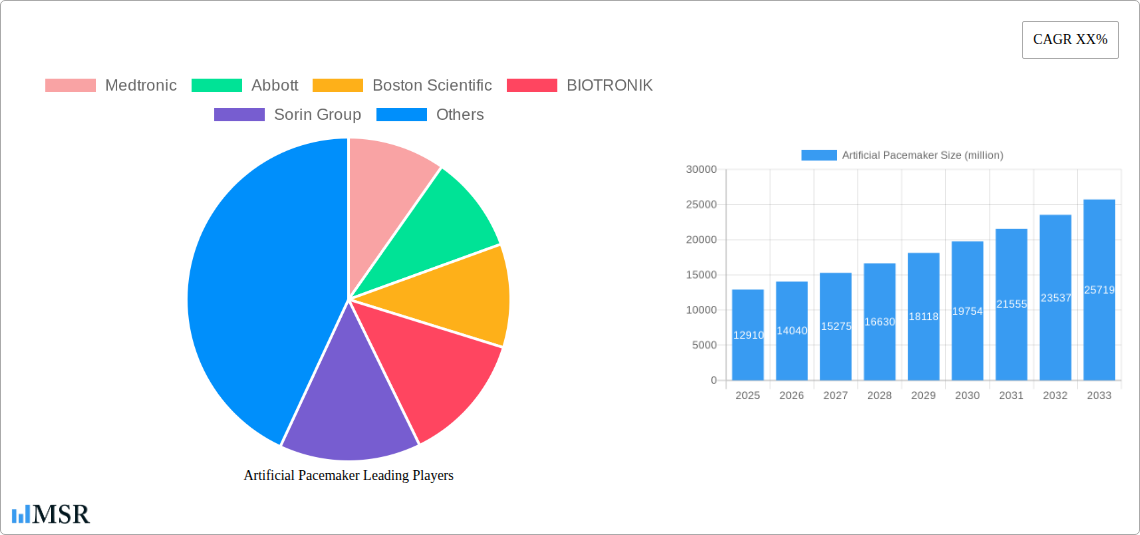

Artificial Pacemaker Company Market Share

Absolutely! Here is an SEO-optimized and engaging report description for the Artificial Pacemaker market, designed to attract industry stakeholders and drive search visibility, incorporating all your specified details and adhering to your structure and word counts.

Artificial Pacemaker Market Concentration & Dynamics

The global artificial pacemaker market, projected to reach $25 billion by 2033, exhibits a moderate to high concentration, dominated by key players including Medtronic, Abbott, and Boston Scientific, who collectively hold an estimated 65% of the market share. This dynamic landscape is fueled by continuous innovation, an evolving regulatory environment, and a growing awareness of cardiac health. Innovation ecosystems are robust, with significant R&D investments directed towards miniaturization, battery longevity, and enhanced remote monitoring capabilities. Substitute products, such as implantable cardioverter-defibrillators (ICDs) and novel therapeutic approaches, pose a growing but currently limited threat due to distinct application areas. End-user trends highlight a preference for minimally invasive procedures and long-term device reliability, driving demand for advanced pacing solutions. Mergers and acquisitions (M&A) activities are a significant factor, with an estimated 15 major deals recorded in the historical period (2019-2024), valued at over $5 billion, indicating strategic consolidation and efforts to expand product portfolios and market reach. BIOTRONIK, Sorin Group, IMZ, Medico, CCC, Pacetronix, Cardioelectronica, Qinming Medical, and Neuroiz are also pivotal contributors, each carving out specific niches through specialized technologies and regional strengths. The influence of these companies shapes the market's competitive intensity and innovation trajectory.

Artificial Pacemaker Industry Insights & Trends

The artificial pacemaker industry is poised for substantial growth, driven by an increasing prevalence of cardiovascular diseases and an aging global population. The market size was valued at $15 billion in the base year 2025, and is forecast to expand at a Compound Annual Growth Rate (CAGR) of 5.5% from 2025 to 2033. This upward trajectory is underpinned by several key market growth drivers. Firstly, the escalating incidence of conditions like bradycardia and atrial fibrillation, directly necessitating pacing therapy, forms the bedrock of sustained demand. Secondly, significant technological disruptions are revolutionizing the field. Innovations such as leadless pacemakers, smaller and more sophisticated implantable devices, and advanced remote patient monitoring systems are enhancing patient outcomes and reducing healthcare burdens. The development of AI-powered algorithms for personalized pacing strategies is another crucial trend, promising to optimize therapy and improve quality of life. Evolving consumer behaviors also play a role, with patients increasingly seeking less invasive procedures and devices that offer greater autonomy and long-term reliability. The integration of smart technologies, enabling continuous data feedback and proactive health management, is transforming the patient-provider relationship. Furthermore, favorable reimbursement policies and increasing healthcare expenditure in emerging economies are creating new avenues for market expansion. The industry's ability to adapt to these multifaceted drivers will be critical in navigating the opportunities and challenges ahead.

Key Markets & Segments Leading Artificial Pacemaker

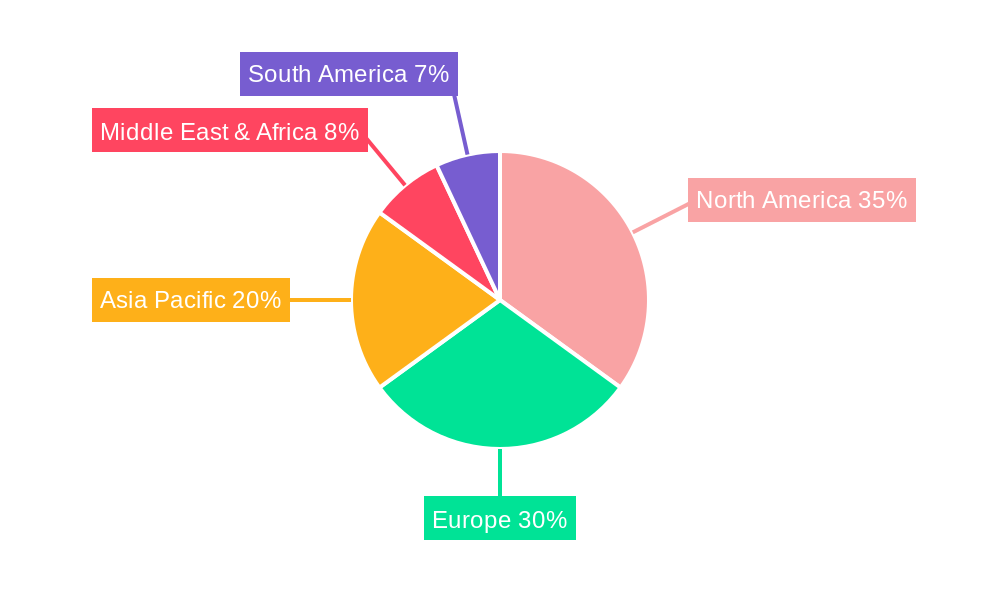

The artificial pacemaker market's dominance is largely attributed to the North America region, specifically the United States, which accounts for an estimated 40% of the global market share. This leadership is fueled by a confluence of factors, including advanced healthcare infrastructure, high disposable incomes, a well-established regulatory framework that encourages innovation, and a high prevalence of cardiovascular conditions. Within the Application segment, Bradycardia remains the most dominant, representing over 50% of the market due to its widespread occurrence and the direct necessity of pacing for rate regulation. Atrial Fibrillation is the second largest application, with its prevalence increasing due to aging populations and lifestyle factors, driving demand for sophisticated pacing solutions. Heart Failure applications are also experiencing significant growth, as pacemakers, particularly cardiac resynchronization therapy (CRT) devices, become integral to managing this complex condition.

- Drivers of Dominance in North America:

- Economic Growth & High Healthcare Expenditure: Significant investment in advanced medical technologies and procedures.

- Advanced Healthcare Infrastructure: Widespread availability of hospitals, specialized cardiac centers, and trained electrophysiologists.

- Favorable Reimbursement Policies: Robust insurance coverage for pacemaker implantation and follow-up care.

- High Incidence of Cardiovascular Diseases: A large patient pool suffering from conditions requiring pacing.

- Proactive Regulatory Environment: FDA's role in facilitating rapid adoption of innovative technologies.

Within the Types segment, Double-Chamber Cardiac Pacing leads the market, accounting for approximately 45% of all pacemaker implants due to its efficacy in mimicking natural heart rhythm and managing various arrhythmias. Single Chamber Cardiac Pacing follows, representing about 30%, primarily for simpler bradycardia cases. The Others category, which includes advanced pacing techniques and newer technologies like leadless pacemakers, is experiencing the fastest growth, driven by technological advancements and patient preference for less invasive solutions. The market's future growth will be significantly influenced by the expansion of these segments, particularly in emerging economies seeking to upgrade their cardiac care capabilities.

Artificial Pacemaker Product Developments

Recent product developments in the artificial pacemaker market are characterized by relentless innovation aimed at enhancing patient outcomes and procedural efficiency. The emergence of leadless pacemakers represents a significant leap forward, offering smaller, fully implantable solutions that eliminate the risks associated with transvenous leads. Advances in battery technology are leading to longer device longevity, reducing the need for replacement surgeries. Furthermore, the integration of sophisticated algorithms for adaptive pacing and remote monitoring capabilities are empowering clinicians with real-time patient data, enabling personalized therapy adjustments and early detection of potential issues. These innovations are not only improving the quality of life for patients but also enhancing the diagnostic and therapeutic precision for healthcare providers.

Challenges in the Artificial Pacemaker Market

The artificial pacemaker market, despite its robust growth, faces several significant challenges. Regulatory hurdles and lengthy approval processes for novel devices can slow down market penetration, particularly in regions with stringent oversight. Supply chain disruptions, exacerbated by geopolitical factors and component shortages, can impact manufacturing timelines and product availability, leading to an estimated 5% increase in production costs in recent years. High device costs and limited reimbursement in certain developing economies restrict widespread access. Furthermore, increasing competition from both established players and emerging innovators necessitates continuous investment in R&D and market penetration strategies. The development of alternative therapies also presents a potential long-term challenge to traditional pacemaker reliance.

Forces Driving Artificial Pacemaker Growth

The artificial pacemaker market is propelled by a potent combination of technological, economic, and demographic forces. A primary driver is the growing global prevalence of cardiovascular diseases, particularly arrhythmias like bradycardia and atrial fibrillation, which directly necessitate pacemaker implantation. This is compounded by the aging global population, as older individuals are more susceptible to cardiac conditions. Technological advancements, such as the development of leadless pacemakers, improved battery life, and sophisticated remote monitoring systems, enhance patient outcomes and drive adoption of newer, more advanced devices. Favorable reimbursement policies and increasing healthcare expenditure, especially in emerging markets, are also significant growth accelerators.

Challenges in the Artificial Pacemaker Market

Long-term growth catalysts for the artificial pacemaker market are deeply rooted in sustained innovation and strategic market expansion. The continuous refinement of minimally invasive implantation techniques will further reduce patient recovery times and improve procedural safety, encouraging wider adoption. The development of smarter pacemakers with enhanced AI-driven diagnostics and predictive capabilities will offer more personalized and proactive patient care. Partnerships between device manufacturers and healthcare providers to establish remote patient management programs will also be crucial, improving adherence and early intervention. Furthermore, strategic market expansion into underserved emerging economies, focusing on affordability and accessible training, presents a significant long-term growth opportunity.

Emerging Opportunities in Artificial Pacemaker

Emerging opportunities in the artificial pacemaker market are ripe for exploitation by innovative companies. The burgeoning field of remote patient monitoring (RPM), powered by connected devices and AI analytics, presents a significant avenue for enhanced patient care and value-based service offerings. The development of biocompatible and biodegradable pacing technologies could revolutionize the field, reducing long-term complications. As healthcare systems globally focus on preventative cardiology, pacemakers integrated with advanced diagnostics for early arrhythmia detection offer immense potential. Furthermore, the increasing demand for personalized medicine is driving the development of bespoke pacing algorithms tailored to individual patient physiology and lifestyle, opening new market segments.

Leading Players in the Artificial Pacemaker Sector

- Medtronic

- Abbott

- Boston Scientific

- BIOTRONIK

- Sorin Group

- IMZ

- Medico

- CCC

- Pacetronix

- Cardioelectronica

- Qinming Medical

- Neuroiz

Key Milestones in Artificial Pacemaker Industry

- 2019: Launch of next-generation leadless pacemaker technology with enhanced battery life.

- 2020: Significant increase in M&A activity with an estimated $2 billion in deals focused on remote monitoring solutions.

- 2021: Regulatory approval for novel AI-driven algorithms to optimize cardiac pacing.

- 2022: Introduction of smaller, fully subcutaneous pacemaker systems catering to specific patient needs.

- 2023: Expansion of remote patient monitoring services by major players, covering an estimated 1.5 million patients globally.

- 2024: Pilot programs initiated for biodegradable pacing leads in select markets.

Strategic Outlook for Artificial Pacemaker Market

The strategic outlook for the artificial pacemaker market is one of sustained and diversified growth. Key accelerators include a continued focus on the development and adoption of leadless and miniaturized pacing systems, which address patient demand for less invasive solutions and reduce procedural complications. The integration of advanced AI and machine learning into pacemaker functionality for predictive diagnostics and personalized therapy optimization will be paramount. Furthermore, strategic partnerships aimed at expanding remote patient management infrastructure and increasing accessibility in emerging markets will unlock significant untapped potential. The market is poised for further consolidation and innovation, driven by the persistent need for effective cardiac rhythm management solutions.

Artificial Pacemaker Segmentation

-

1. Application

- 1.1. Bradycardia

- 1.2. Atrial Fibrillation

- 1.3. Heart Failure

- 1.4. Syncope

-

2. Types

- 2.1. Temporary Cardiac Pacing

- 2.2. Single Chamber Cardiac Pacing

- 2.3. Double-Chamber Cardiac Pacing

- 2.4. Others

Artificial Pacemaker Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Artificial Pacemaker Regional Market Share

Geographic Coverage of Artificial Pacemaker

Artificial Pacemaker REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Artificial Pacemaker Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Bradycardia

- 5.1.2. Atrial Fibrillation

- 5.1.3. Heart Failure

- 5.1.4. Syncope

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Temporary Cardiac Pacing

- 5.2.2. Single Chamber Cardiac Pacing

- 5.2.3. Double-Chamber Cardiac Pacing

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Artificial Pacemaker Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Bradycardia

- 6.1.2. Atrial Fibrillation

- 6.1.3. Heart Failure

- 6.1.4. Syncope

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Temporary Cardiac Pacing

- 6.2.2. Single Chamber Cardiac Pacing

- 6.2.3. Double-Chamber Cardiac Pacing

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Artificial Pacemaker Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Bradycardia

- 7.1.2. Atrial Fibrillation

- 7.1.3. Heart Failure

- 7.1.4. Syncope

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Temporary Cardiac Pacing

- 7.2.2. Single Chamber Cardiac Pacing

- 7.2.3. Double-Chamber Cardiac Pacing

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Artificial Pacemaker Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Bradycardia

- 8.1.2. Atrial Fibrillation

- 8.1.3. Heart Failure

- 8.1.4. Syncope

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Temporary Cardiac Pacing

- 8.2.2. Single Chamber Cardiac Pacing

- 8.2.3. Double-Chamber Cardiac Pacing

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Artificial Pacemaker Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Bradycardia

- 9.1.2. Atrial Fibrillation

- 9.1.3. Heart Failure

- 9.1.4. Syncope

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Temporary Cardiac Pacing

- 9.2.2. Single Chamber Cardiac Pacing

- 9.2.3. Double-Chamber Cardiac Pacing

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Artificial Pacemaker Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Bradycardia

- 10.1.2. Atrial Fibrillation

- 10.1.3. Heart Failure

- 10.1.4. Syncope

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Temporary Cardiac Pacing

- 10.2.2. Single Chamber Cardiac Pacing

- 10.2.3. Double-Chamber Cardiac Pacing

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Medtronic

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Abbott

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Boston Scientific

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BIOTRONIK

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sorin Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 IMZ

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Medico

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 CCC

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Pacetronix

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cardioelectronica

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Qinming Medical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Neuroiz

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Medtronic

List of Figures

- Figure 1: Global Artificial Pacemaker Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Artificial Pacemaker Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Artificial Pacemaker Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Artificial Pacemaker Volume (K), by Application 2025 & 2033

- Figure 5: North America Artificial Pacemaker Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Artificial Pacemaker Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Artificial Pacemaker Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Artificial Pacemaker Volume (K), by Types 2025 & 2033

- Figure 9: North America Artificial Pacemaker Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Artificial Pacemaker Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Artificial Pacemaker Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Artificial Pacemaker Volume (K), by Country 2025 & 2033

- Figure 13: North America Artificial Pacemaker Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Artificial Pacemaker Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Artificial Pacemaker Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Artificial Pacemaker Volume (K), by Application 2025 & 2033

- Figure 17: South America Artificial Pacemaker Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Artificial Pacemaker Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Artificial Pacemaker Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Artificial Pacemaker Volume (K), by Types 2025 & 2033

- Figure 21: South America Artificial Pacemaker Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Artificial Pacemaker Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Artificial Pacemaker Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Artificial Pacemaker Volume (K), by Country 2025 & 2033

- Figure 25: South America Artificial Pacemaker Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Artificial Pacemaker Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Artificial Pacemaker Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Artificial Pacemaker Volume (K), by Application 2025 & 2033

- Figure 29: Europe Artificial Pacemaker Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Artificial Pacemaker Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Artificial Pacemaker Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Artificial Pacemaker Volume (K), by Types 2025 & 2033

- Figure 33: Europe Artificial Pacemaker Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Artificial Pacemaker Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Artificial Pacemaker Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Artificial Pacemaker Volume (K), by Country 2025 & 2033

- Figure 37: Europe Artificial Pacemaker Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Artificial Pacemaker Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Artificial Pacemaker Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Artificial Pacemaker Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Artificial Pacemaker Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Artificial Pacemaker Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Artificial Pacemaker Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Artificial Pacemaker Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Artificial Pacemaker Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Artificial Pacemaker Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Artificial Pacemaker Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Artificial Pacemaker Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Artificial Pacemaker Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Artificial Pacemaker Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Artificial Pacemaker Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Artificial Pacemaker Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Artificial Pacemaker Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Artificial Pacemaker Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Artificial Pacemaker Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Artificial Pacemaker Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Artificial Pacemaker Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Artificial Pacemaker Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Artificial Pacemaker Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Artificial Pacemaker Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Artificial Pacemaker Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Artificial Pacemaker Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Artificial Pacemaker Revenue undefined Forecast, by Region 2020 & 2033

- Table 2: Global Artificial Pacemaker Volume K Forecast, by Region 2020 & 2033

- Table 3: Global Artificial Pacemaker Revenue undefined Forecast, by Application 2020 & 2033

- Table 4: Global Artificial Pacemaker Volume K Forecast, by Application 2020 & 2033

- Table 5: Global Artificial Pacemaker Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Artificial Pacemaker Volume K Forecast, by Types 2020 & 2033

- Table 7: Global Artificial Pacemaker Revenue undefined Forecast, by Region 2020 & 2033

- Table 8: Global Artificial Pacemaker Volume K Forecast, by Region 2020 & 2033

- Table 9: Global Artificial Pacemaker Revenue undefined Forecast, by Application 2020 & 2033

- Table 10: Global Artificial Pacemaker Volume K Forecast, by Application 2020 & 2033

- Table 11: Global Artificial Pacemaker Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Artificial Pacemaker Volume K Forecast, by Types 2020 & 2033

- Table 13: Global Artificial Pacemaker Revenue undefined Forecast, by Country 2020 & 2033

- Table 14: Global Artificial Pacemaker Volume K Forecast, by Country 2020 & 2033

- Table 15: United States Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: United States Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Canada Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Canada Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Mexico Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Mexico Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 21: Global Artificial Pacemaker Revenue undefined Forecast, by Application 2020 & 2033

- Table 22: Global Artificial Pacemaker Volume K Forecast, by Application 2020 & 2033

- Table 23: Global Artificial Pacemaker Revenue undefined Forecast, by Types 2020 & 2033

- Table 24: Global Artificial Pacemaker Volume K Forecast, by Types 2020 & 2033

- Table 25: Global Artificial Pacemaker Revenue undefined Forecast, by Country 2020 & 2033

- Table 26: Global Artificial Pacemaker Volume K Forecast, by Country 2020 & 2033

- Table 27: Brazil Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Brazil Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Argentina Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Argentina Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Rest of South America Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 33: Global Artificial Pacemaker Revenue undefined Forecast, by Application 2020 & 2033

- Table 34: Global Artificial Pacemaker Volume K Forecast, by Application 2020 & 2033

- Table 35: Global Artificial Pacemaker Revenue undefined Forecast, by Types 2020 & 2033

- Table 36: Global Artificial Pacemaker Volume K Forecast, by Types 2020 & 2033

- Table 37: Global Artificial Pacemaker Revenue undefined Forecast, by Country 2020 & 2033

- Table 38: Global Artificial Pacemaker Volume K Forecast, by Country 2020 & 2033

- Table 39: United Kingdom Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: United Kingdom Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 41: Germany Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Germany Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 43: France Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: France Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Italy Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Italy Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Spain Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Spain Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Russia Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Russia Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Benelux Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Benelux Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Nordics Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Nordics Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Rest of Europe Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 56: Rest of Europe Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 57: Global Artificial Pacemaker Revenue undefined Forecast, by Application 2020 & 2033

- Table 58: Global Artificial Pacemaker Volume K Forecast, by Application 2020 & 2033

- Table 59: Global Artificial Pacemaker Revenue undefined Forecast, by Types 2020 & 2033

- Table 60: Global Artificial Pacemaker Volume K Forecast, by Types 2020 & 2033

- Table 61: Global Artificial Pacemaker Revenue undefined Forecast, by Country 2020 & 2033

- Table 62: Global Artificial Pacemaker Volume K Forecast, by Country 2020 & 2033

- Table 63: Turkey Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Turkey Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 65: Israel Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: Israel Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 67: GCC Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: GCC Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 69: North Africa Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: North Africa Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 71: South Africa Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: South Africa Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Rest of Middle East & Africa Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 74: Rest of Middle East & Africa Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 75: Global Artificial Pacemaker Revenue undefined Forecast, by Application 2020 & 2033

- Table 76: Global Artificial Pacemaker Volume K Forecast, by Application 2020 & 2033

- Table 77: Global Artificial Pacemaker Revenue undefined Forecast, by Types 2020 & 2033

- Table 78: Global Artificial Pacemaker Volume K Forecast, by Types 2020 & 2033

- Table 79: Global Artificial Pacemaker Revenue undefined Forecast, by Country 2020 & 2033

- Table 80: Global Artificial Pacemaker Volume K Forecast, by Country 2020 & 2033

- Table 81: China Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: China Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 83: India Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: India Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 85: Japan Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: Japan Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 87: South Korea Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: South Korea Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 89: ASEAN Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: ASEAN Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Oceania Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Oceania Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

- Table 93: Rest of Asia Pacific Artificial Pacemaker Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 94: Rest of Asia Pacific Artificial Pacemaker Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Artificial Pacemaker?

The projected CAGR is approximately 9.7%.

2. Which companies are prominent players in the Artificial Pacemaker?

Key companies in the market include Medtronic, Abbott, Boston Scientific, BIOTRONIK, Sorin Group, IMZ, Medico, CCC, Pacetronix, Cardioelectronica, Qinming Medical, Neuroiz.

3. What are the main segments of the Artificial Pacemaker?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Artificial Pacemaker," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Artificial Pacemaker report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Artificial Pacemaker?

To stay informed about further developments, trends, and reports in the Artificial Pacemaker, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence