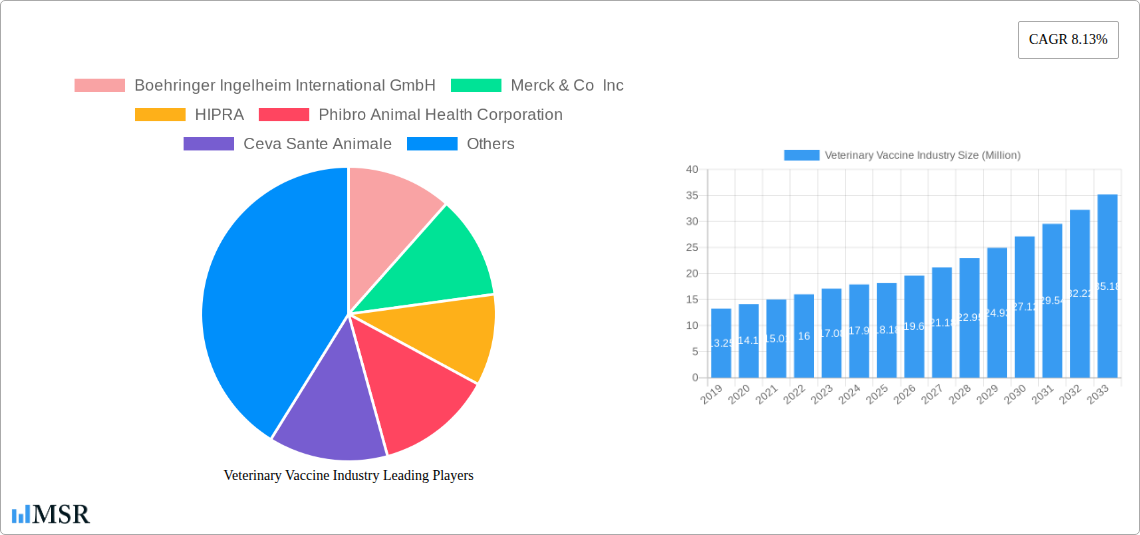

Key Insights

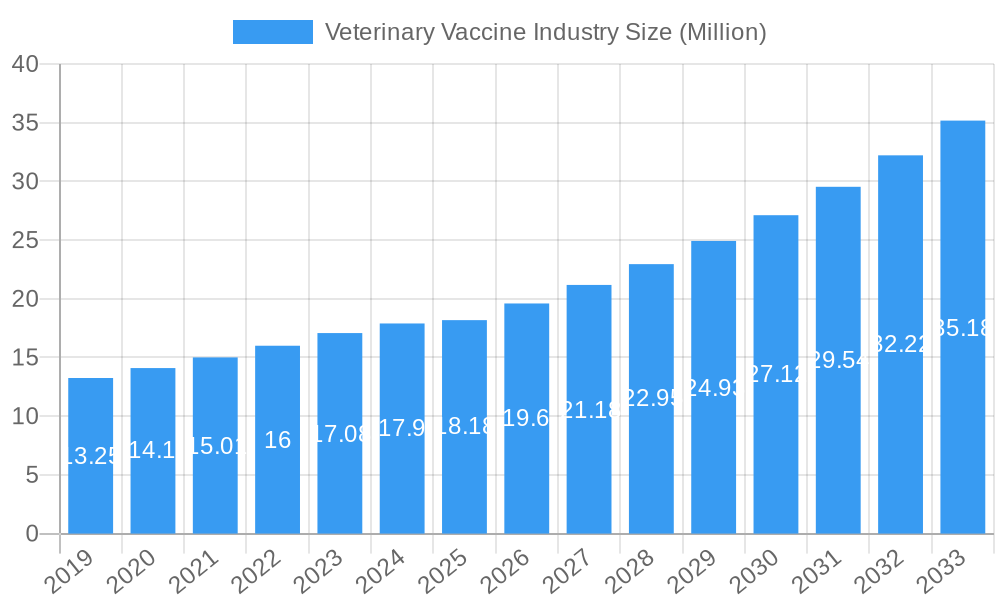

The global veterinary vaccine market is experiencing robust expansion, projected to reach an estimated USD 18.18 billion by 2025. This significant growth is fueled by a compound annual growth rate (CAGR) of 8.13% over the forecast period of 2025-2033. A primary driver for this upward trajectory is the increasing global demand for animal protein, which in turn necessitates enhanced animal health management and disease prevention through vaccination, especially in the livestock sector. Growing pet ownership worldwide and a heightened awareness among owners regarding the importance of preventative care for their companion animals further contribute to market expansion. Technological advancements in vaccine development, including the emergence of recombinant and subunit vaccines offering improved efficacy and safety profiles, are also playing a crucial role. The market is segmented into distinct categories, with livestock vaccines, encompassing bovine, poultry, and porcine vaccines, holding a substantial share. Companion animal vaccines, catering to canine, feline, and equine health, represent a rapidly growing segment.

Veterinary Vaccine Industry Market Size (In Million)

The market's dynamism is shaped by several influential trends. The rising prevalence of zoonotic diseases, which can transmit between animals and humans, is driving increased investment in animal health surveillance and preventative measures, including vaccination programs. Furthermore, the development of novel vaccine delivery systems and the increasing adoption of combination vaccines are enhancing convenience and compliance for both livestock producers and pet owners. However, the market faces certain restraints, including the high cost associated with research and development of new vaccines and the stringent regulatory approval processes in various regions. Fluctuations in raw material prices and the potential for vaccine hesitancy among some stakeholders can also pose challenges. Despite these hurdles, the sustained focus on animal welfare, coupled with the ongoing need to safeguard animal populations from infectious diseases, ensures a promising outlook for the veterinary vaccine industry. Key players are actively engaged in strategic partnerships and mergers to expand their product portfolios and geographical reach, solidifying their positions in this competitive landscape.

Veterinary Vaccine Industry Company Market Share

Here's the SEO-optimized and engaging report description for the Veterinary Vaccine Industry, incorporating all your requirements:

Veterinary Vaccine Industry Market Concentration & Dynamics

The global veterinary vaccine market exhibits a moderate to high concentration, dominated by a few key players in the animal health sector. These industry giants leverage extensive R&D capabilities and robust distribution networks to maintain their significant market share. Innovation ecosystems are flourishing, driven by advancements in biotechnology and a growing understanding of animal diseases. Regulatory frameworks, while crucial for ensuring product safety and efficacy, also present a significant barrier to entry for smaller entities. The landscape is further shaped by the availability of substitute products such as antibiotics and other prophylactic treatments, though vaccines remain the cornerstone of disease prevention. End-user trends are increasingly focused on preventative healthcare for both livestock and companion animals, driven by concerns over food safety, animal welfare, and the human-animal bond. Mergers and acquisitions (M&A) activities have been a consistent feature, with companies strategically acquiring smaller biotech firms or consolidating to expand their product portfolios and geographical reach. For instance, recent M&A deal counts indicate a strategic consolidation trend.

- Market Share: Major players like Zoetis Inc., Merck & Co. Inc., and Boehringer Ingelheim International GmbH hold a substantial collective market share, estimated in the billions of dollars.

- M&A Activities: The past few years have seen numerous M&A deals, with an estimated xx number of significant transactions aimed at portfolio enhancement and market expansion.

- Innovation Hubs: North America and Europe are primary hubs for veterinary vaccine innovation, with increasing R&D investments.

Veterinary Vaccine Industry Industry Insights & Trends

The global veterinary vaccine market is poised for significant expansion, projected to reach an estimated USD 20,000 million by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period of 2025–2033. This robust growth is underpinned by several key drivers. The increasing global demand for animal protein, coupled with the rising prevalence of zoonotic diseases, is a primary catalyst for enhanced biosecurity measures in livestock farming. Furthermore, the growing humanization of pets has led to a surge in demand for advanced companion animal vaccines, as owners increasingly prioritize their pets' health and longevity. Technological disruptions are revolutionizing vaccine development. Advances in recombinant vaccine technology, mRNA platforms, and gene editing are enabling the creation of safer, more effective, and faster-to-develop vaccines. These innovations are crucial for combating emerging infectious diseases and addressing antimicrobial resistance. Evolving consumer behaviors, characterized by a greater emphasis on animal welfare and preventative healthcare, are also fueling market growth. Pet owners are more willing to invest in regular vaccinations and health check-ups, while livestock producers are adopting proactive disease management strategies to improve herd health and reduce economic losses. The increasing adoption of digital technologies, such as remote monitoring and AI-driven diagnostics, is also indirectly supporting the veterinary vaccine market by enabling more targeted and efficient disease prevention strategies. Economic growth in developing regions, particularly in Asia-Pacific and Latin America, is contributing to increased livestock production and a growing pet population, thereby expanding the market for veterinary vaccines.

Key Markets & Segments Leading Veterinary Vaccine Industry

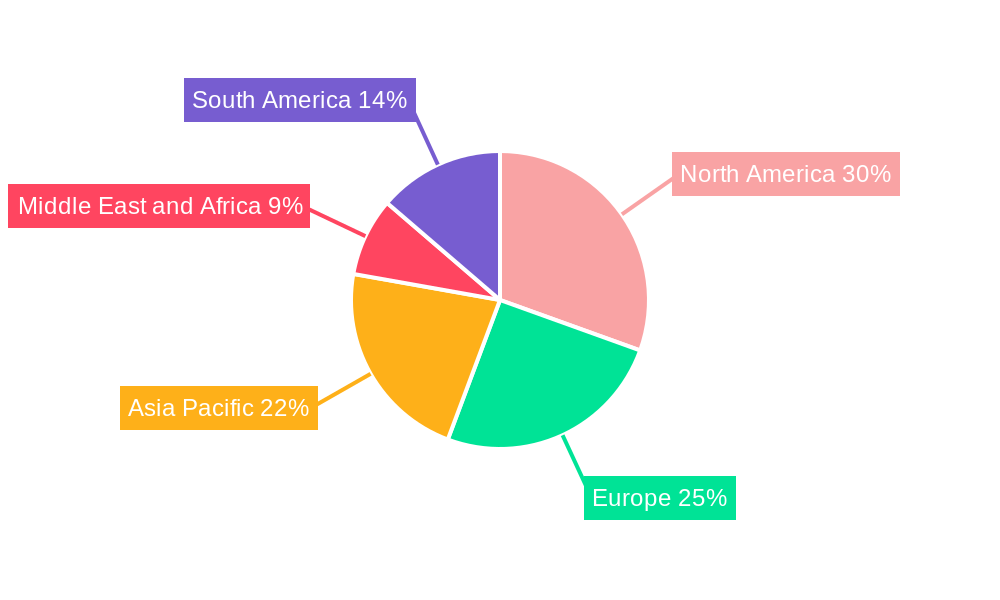

The global veterinary vaccine market is characterized by distinct regional and segment-driven dominance. In terms of geography, North America and Europe currently lead, driven by high pet ownership rates, advanced veterinary infrastructure, and significant R&D investments. However, the Asia-Pacific region is emerging as a high-growth market due to expanding livestock populations, increasing disposable incomes supporting pet ownership, and government initiatives promoting animal health.

Within the Vaccine Type segment, Livestock Vaccines represent the largest share, driven by the global demand for animal protein and the economic importance of disease prevention in large-scale farming operations.

- Livestock Vaccines:

- Poultry Vaccines: This sub-segment is a major contributor due to the high volume of poultry production globally and the susceptibility of birds to various diseases. Economic growth and the rising demand for poultry meat are key drivers.

- Bovine Vaccines: Essential for preventing widespread diseases like Foot-and-Mouth Disease and Bovine Viral Diarrhea, this segment is critical for dairy and beef industries. The focus on food safety and animal welfare further bolsters its importance.

- Porcine Vaccines: The swine industry's economic significance and the threat of devastating diseases like Porcine Reproductive and Respiratory Syndrome (PRRS) make this a crucial vaccine category.

- Other Livestock Vaccines: This includes vaccines for sheep, goats, and other farm animals, contributing to diversified agricultural economies.

Companion Animal Vaccines are also experiencing substantial growth, fueled by the increasing humanization of pets.

- Companion Animal Vaccines:

- Canine Vaccines: With high rates of dog ownership, vaccines for diseases like rabies, distemper, and parvovirus remain a cornerstone of the companion animal market.

- Feline Vaccines: Cat ownership is on the rise, driving demand for vaccines against feline leukemia virus, rabies, and other common feline ailments.

- Equine Vaccines: While a smaller segment, vaccines for horses are vital for preventing diseases like West Nile Virus and Equine Influenza, especially in regions with strong equestrian cultures and racing industries.

By Technology, Inactivated Vaccines and Live Attenuated Vaccines currently hold significant market share due to their established efficacy and widespread use. However, Recombinant Vaccines are rapidly gaining traction, offering improved safety profiles and the potential for multi-component vaccines.

- Technology:

- Live Attenuated Vaccines: Offer strong and long-lasting immunity but may pose risks in immunocompromised animals.

- Inactivated Vaccines: Generally safer and more stable, but often require adjuvants and booster doses for optimal immunity.

- Toxoid Vaccines: Crucial for bacterial diseases where toxins, not the bacteria themselves, cause harm.

- Recombinant Vaccines: Represent the future of vaccine development, offering high specificity, safety, and the potential for cost-effective production.

Veterinary Vaccine Industry Product Developments

Recent product developments highlight the industry's commitment to innovation and addressing evolving disease threats. The launch of Merck Animal Health's Nobivac Intra-Trac Oral BbPi in September 2022 signifies a major advancement in canine respiratory disease prevention, offering a dual-action oral vaccine. Simultaneously, the development of the Lumpi-ProVacInd. vaccine by ICAR-NRCE and IVRI in August 2022 demonstrates significant progress in combating Lumpy Skin Disease in bovines, particularly crucial for emerging markets. These innovations, utilizing cutting-edge technologies like live-attenuation and oral delivery systems, underscore the industry's focus on providing convenient, effective, and targeted solutions that enhance animal welfare and reduce economic losses.

Challenges in the Veterinary Vaccine Industry Market

The veterinary vaccine market faces several hurdles that can impede growth and market penetration. Stringent and varied regulatory requirements across different regions create complexity and lengthy approval processes for new vaccines. Supply chain disruptions, exacerbated by geopolitical events and pandemics, can impact the availability of raw materials and finished products. Furthermore, high research and development costs associated with novel vaccine technologies can be a barrier, especially for smaller companies. Price sensitivity among some end-users, particularly in developing economies, and the prevalence of counterfeit products also pose significant challenges.

- Regulatory Hurdles: Extended approval timelines and differing standards in key markets.

- Supply Chain Vulnerabilities: Dependence on global sourcing for critical components.

- R&D Investment Strain: High costs for developing and validating advanced vaccine technologies.

- Market Access & Affordability: Balancing innovative pricing with accessibility for diverse customer segments.

Forces Driving Veterinary Vaccine Industry Growth

Several powerful forces are propelling the growth of the veterinary vaccine industry. The increasing recognition of the One Health concept, emphasizing the interconnectedness of human, animal, and environmental health, is a major driver, highlighting the importance of preventing zoonotic diseases through robust animal vaccination programs. The growing global population and rising demand for animal protein necessitate enhanced livestock productivity, where vaccines play a critical role in disease prevention and herd health management. Furthermore, the escalating trend of pet humanization translates into increased spending on pet healthcare, including routine and advanced vaccinations. Technological advancements, particularly in recombinant and mRNA vaccine platforms, are enabling the development of safer, more effective, and targeted vaccines, opening up new therapeutic avenues.

Challenges in the Veterinary Vaccine Industry Market

While growth is robust, the veterinary vaccine market must navigate long-term challenges. Ensuring equitable access to advanced vaccines in emerging markets remains crucial, requiring innovative pricing strategies and localized distribution networks. The ongoing threat of pathogen evolution necessitates continuous research and development to create vaccines that can adapt to new strains and emerging diseases. Addressing public perception and education regarding vaccine safety and efficacy is vital to combat vaccine hesitancy, particularly in the companion animal segment. Moreover, the industry must actively contribute to antimicrobial stewardship by promoting vaccination as a primary disease prevention strategy, thereby reducing reliance on antibiotics.

Emerging Opportunities in Veterinary Vaccine Industry

Significant emerging opportunities exist within the veterinary vaccine landscape. The development of novel vaccine delivery systems, such as oral and transdermal routes, promises enhanced convenience and reduced stress for animals. The burgeoning field of genomic sequencing and bioinformatics is enabling faster identification of new vaccine targets and the design of highly specific vaccines. The growing demand for therapeutic vaccines, aimed at treating existing diseases rather than just preventing them, presents a vast untapped market. Furthermore, the expansion into specialty animal markets, including aquaculture and exotic pets, offers new avenues for growth. The increasing adoption of digital health platforms for animal monitoring and disease surveillance creates opportunities for integrated vaccination management solutions.

Leading Players in the Veterinary Vaccine Industry Sector

- Boehringer Ingelheim International GmbH

- Merck & Co Inc

- HIPRA

- Phibro Animal Health Corporation

- Ceva Sante Animale

- Virbac

- Elanco Animal Health

- Zoetis Inc

- Hester Biosciences Limited

Key Milestones in Veterinary Vaccine Industry Industry

- September 2022: Merck Animal Health launched Nobivac Intra-Trac Oral BbPi, a dual-prevention oral vaccine for canine respiratory pathogens. This innovation enhances convenience and efficacy in canine healthcare.

- August 2022: The ICAR-National Research Centre on Equines (ICAR-NRCE), Hisar, in collaboration with ICAR-Indian Veterinary Research Institute (IVRI), developed Lumpi-ProVacInd., a homologous live-attenuated Lumpy Skin Disease vaccine. This development offers a critical solution for bovine health and economic stability in affected regions.

Strategic Outlook for Veterinary Vaccine Industry Market

The strategic outlook for the veterinary vaccine market remains highly optimistic, driven by sustained demand and continuous innovation. Key growth accelerators include the ongoing expansion of companion animal ownership, the persistent need for disease prevention in global livestock production, and the rapid advancements in vaccine technology, such as mRNA and subunit vaccines. Strategic opportunities lie in strengthening R&D pipelines for novel vaccines against emerging infectious diseases and expanding market penetration in under-served regions. Collaborations between industry players, academic institutions, and regulatory bodies will be crucial for accelerating product development and ensuring global vaccine accessibility. Furthermore, a focus on sustainability and the integration of digital technologies will shape the future landscape, promising enhanced efficacy, improved animal welfare, and greater economic benefits for stakeholders across the animal health value chain.

Veterinary Vaccine Industry Segmentation

-

1. Vaccine Type

-

1.1. Livestock Vaccines

- 1.1.1. Bovine Vaccines

- 1.1.2. Poultry Vaccines

- 1.1.3. Porcine Vaccines

- 1.1.4. Other Livestock Vaccines

-

1.2. By Companion Animal Vaccines

- 1.2.1. Canine Vaccines

- 1.2.2. Feline Vaccines

- 1.2.3. Equine Vaccines

-

1.1. Livestock Vaccines

-

2. Technology

- 2.1. Live Attenuated Vaccines

- 2.2. Inactivated Vaccines

- 2.3. Toxoid Vaccines

- 2.4. Recombinant Vaccines

- 2.5. Other Technologies

Veterinary Vaccine Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Veterinary Vaccine Industry Regional Market Share

Geographic Coverage of Veterinary Vaccine Industry

Veterinary Vaccine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 5.1.1. Livestock Vaccines

- 5.1.1.1. Bovine Vaccines

- 5.1.1.2. Poultry Vaccines

- 5.1.1.3. Porcine Vaccines

- 5.1.1.4. Other Livestock Vaccines

- 5.1.2. By Companion Animal Vaccines

- 5.1.2.1. Canine Vaccines

- 5.1.2.2. Feline Vaccines

- 5.1.2.3. Equine Vaccines

- 5.1.1. Livestock Vaccines

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Live Attenuated Vaccines

- 5.2.2. Inactivated Vaccines

- 5.2.3. Toxoid Vaccines

- 5.2.4. Recombinant Vaccines

- 5.2.5. Other Technologies

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 6. Global Veterinary Vaccine Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 6.1.1. Livestock Vaccines

- 6.1.1.1. Bovine Vaccines

- 6.1.1.2. Poultry Vaccines

- 6.1.1.3. Porcine Vaccines

- 6.1.1.4. Other Livestock Vaccines

- 6.1.2. By Companion Animal Vaccines

- 6.1.2.1. Canine Vaccines

- 6.1.2.2. Feline Vaccines

- 6.1.2.3. Equine Vaccines

- 6.1.1. Livestock Vaccines

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Live Attenuated Vaccines

- 6.2.2. Inactivated Vaccines

- 6.2.3. Toxoid Vaccines

- 6.2.4. Recombinant Vaccines

- 6.2.5. Other Technologies

- 6.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 7. North America Veterinary Vaccine Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 7.1.1. Livestock Vaccines

- 7.1.1.1. Bovine Vaccines

- 7.1.1.2. Poultry Vaccines

- 7.1.1.3. Porcine Vaccines

- 7.1.1.4. Other Livestock Vaccines

- 7.1.2. By Companion Animal Vaccines

- 7.1.2.1. Canine Vaccines

- 7.1.2.2. Feline Vaccines

- 7.1.2.3. Equine Vaccines

- 7.1.1. Livestock Vaccines

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Live Attenuated Vaccines

- 7.2.2. Inactivated Vaccines

- 7.2.3. Toxoid Vaccines

- 7.2.4. Recombinant Vaccines

- 7.2.5. Other Technologies

- 7.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 8. Europe Veterinary Vaccine Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 8.1.1. Livestock Vaccines

- 8.1.1.1. Bovine Vaccines

- 8.1.1.2. Poultry Vaccines

- 8.1.1.3. Porcine Vaccines

- 8.1.1.4. Other Livestock Vaccines

- 8.1.2. By Companion Animal Vaccines

- 8.1.2.1. Canine Vaccines

- 8.1.2.2. Feline Vaccines

- 8.1.2.3. Equine Vaccines

- 8.1.1. Livestock Vaccines

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Live Attenuated Vaccines

- 8.2.2. Inactivated Vaccines

- 8.2.3. Toxoid Vaccines

- 8.2.4. Recombinant Vaccines

- 8.2.5. Other Technologies

- 8.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 9. Asia Pacific Veterinary Vaccine Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 9.1.1. Livestock Vaccines

- 9.1.1.1. Bovine Vaccines

- 9.1.1.2. Poultry Vaccines

- 9.1.1.3. Porcine Vaccines

- 9.1.1.4. Other Livestock Vaccines

- 9.1.2. By Companion Animal Vaccines

- 9.1.2.1. Canine Vaccines

- 9.1.2.2. Feline Vaccines

- 9.1.2.3. Equine Vaccines

- 9.1.1. Livestock Vaccines

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Live Attenuated Vaccines

- 9.2.2. Inactivated Vaccines

- 9.2.3. Toxoid Vaccines

- 9.2.4. Recombinant Vaccines

- 9.2.5. Other Technologies

- 9.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 10. Middle East and Africa Veterinary Vaccine Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 10.1.1. Livestock Vaccines

- 10.1.1.1. Bovine Vaccines

- 10.1.1.2. Poultry Vaccines

- 10.1.1.3. Porcine Vaccines

- 10.1.1.4. Other Livestock Vaccines

- 10.1.2. By Companion Animal Vaccines

- 10.1.2.1. Canine Vaccines

- 10.1.2.2. Feline Vaccines

- 10.1.2.3. Equine Vaccines

- 10.1.1. Livestock Vaccines

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Live Attenuated Vaccines

- 10.2.2. Inactivated Vaccines

- 10.2.3. Toxoid Vaccines

- 10.2.4. Recombinant Vaccines

- 10.2.5. Other Technologies

- 10.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 11. South America Veterinary Vaccine Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 11.1.1. Livestock Vaccines

- 11.1.1.1. Bovine Vaccines

- 11.1.1.2. Poultry Vaccines

- 11.1.1.3. Porcine Vaccines

- 11.1.1.4. Other Livestock Vaccines

- 11.1.2. By Companion Animal Vaccines

- 11.1.2.1. Canine Vaccines

- 11.1.2.2. Feline Vaccines

- 11.1.2.3. Equine Vaccines

- 11.1.1. Livestock Vaccines

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Live Attenuated Vaccines

- 11.2.2. Inactivated Vaccines

- 11.2.3. Toxoid Vaccines

- 11.2.4. Recombinant Vaccines

- 11.2.5. Other Technologies

- 11.1. Market Analysis, Insights and Forecast - by Vaccine Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Boehringer Ingelheim International GmbH

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Merck & Co Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 HIPRA

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Phibro Animal Health Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ceva Sante Animale

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Virbac

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Elanco Animal Health

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Zoetis Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hester Biosciences Limited

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Boehringer Ingelheim International GmbH

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Veterinary Vaccine Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Veterinary Vaccine Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Veterinary Vaccine Industry Revenue (Million), by Vaccine Type 2025 & 2033

- Figure 4: North America Veterinary Vaccine Industry Volume (K Unit), by Vaccine Type 2025 & 2033

- Figure 5: North America Veterinary Vaccine Industry Revenue Share (%), by Vaccine Type 2025 & 2033

- Figure 6: North America Veterinary Vaccine Industry Volume Share (%), by Vaccine Type 2025 & 2033

- Figure 7: North America Veterinary Vaccine Industry Revenue (Million), by Technology 2025 & 2033

- Figure 8: North America Veterinary Vaccine Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 9: North America Veterinary Vaccine Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: North America Veterinary Vaccine Industry Volume Share (%), by Technology 2025 & 2033

- Figure 11: North America Veterinary Vaccine Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Veterinary Vaccine Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Veterinary Vaccine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Veterinary Vaccine Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Veterinary Vaccine Industry Revenue (Million), by Vaccine Type 2025 & 2033

- Figure 16: Europe Veterinary Vaccine Industry Volume (K Unit), by Vaccine Type 2025 & 2033

- Figure 17: Europe Veterinary Vaccine Industry Revenue Share (%), by Vaccine Type 2025 & 2033

- Figure 18: Europe Veterinary Vaccine Industry Volume Share (%), by Vaccine Type 2025 & 2033

- Figure 19: Europe Veterinary Vaccine Industry Revenue (Million), by Technology 2025 & 2033

- Figure 20: Europe Veterinary Vaccine Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 21: Europe Veterinary Vaccine Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Europe Veterinary Vaccine Industry Volume Share (%), by Technology 2025 & 2033

- Figure 23: Europe Veterinary Vaccine Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Veterinary Vaccine Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Veterinary Vaccine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Veterinary Vaccine Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Veterinary Vaccine Industry Revenue (Million), by Vaccine Type 2025 & 2033

- Figure 28: Asia Pacific Veterinary Vaccine Industry Volume (K Unit), by Vaccine Type 2025 & 2033

- Figure 29: Asia Pacific Veterinary Vaccine Industry Revenue Share (%), by Vaccine Type 2025 & 2033

- Figure 30: Asia Pacific Veterinary Vaccine Industry Volume Share (%), by Vaccine Type 2025 & 2033

- Figure 31: Asia Pacific Veterinary Vaccine Industry Revenue (Million), by Technology 2025 & 2033

- Figure 32: Asia Pacific Veterinary Vaccine Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 33: Asia Pacific Veterinary Vaccine Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 34: Asia Pacific Veterinary Vaccine Industry Volume Share (%), by Technology 2025 & 2033

- Figure 35: Asia Pacific Veterinary Vaccine Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Pacific Veterinary Vaccine Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Veterinary Vaccine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Veterinary Vaccine Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa Veterinary Vaccine Industry Revenue (Million), by Vaccine Type 2025 & 2033

- Figure 40: Middle East and Africa Veterinary Vaccine Industry Volume (K Unit), by Vaccine Type 2025 & 2033

- Figure 41: Middle East and Africa Veterinary Vaccine Industry Revenue Share (%), by Vaccine Type 2025 & 2033

- Figure 42: Middle East and Africa Veterinary Vaccine Industry Volume Share (%), by Vaccine Type 2025 & 2033

- Figure 43: Middle East and Africa Veterinary Vaccine Industry Revenue (Million), by Technology 2025 & 2033

- Figure 44: Middle East and Africa Veterinary Vaccine Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 45: Middle East and Africa Veterinary Vaccine Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 46: Middle East and Africa Veterinary Vaccine Industry Volume Share (%), by Technology 2025 & 2033

- Figure 47: Middle East and Africa Veterinary Vaccine Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Middle East and Africa Veterinary Vaccine Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa Veterinary Vaccine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Veterinary Vaccine Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Veterinary Vaccine Industry Revenue (Million), by Vaccine Type 2025 & 2033

- Figure 52: South America Veterinary Vaccine Industry Volume (K Unit), by Vaccine Type 2025 & 2033

- Figure 53: South America Veterinary Vaccine Industry Revenue Share (%), by Vaccine Type 2025 & 2033

- Figure 54: South America Veterinary Vaccine Industry Volume Share (%), by Vaccine Type 2025 & 2033

- Figure 55: South America Veterinary Vaccine Industry Revenue (Million), by Technology 2025 & 2033

- Figure 56: South America Veterinary Vaccine Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 57: South America Veterinary Vaccine Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 58: South America Veterinary Vaccine Industry Volume Share (%), by Technology 2025 & 2033

- Figure 59: South America Veterinary Vaccine Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: South America Veterinary Vaccine Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America Veterinary Vaccine Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America Veterinary Vaccine Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Veterinary Vaccine Industry Revenue Million Forecast, by Vaccine Type 2020 & 2033

- Table 2: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Vaccine Type 2020 & 2033

- Table 3: Global Veterinary Vaccine Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 4: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 5: Global Veterinary Vaccine Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Veterinary Vaccine Industry Revenue Million Forecast, by Vaccine Type 2020 & 2033

- Table 8: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Vaccine Type 2020 & 2033

- Table 9: Global Veterinary Vaccine Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 10: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 11: Global Veterinary Vaccine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Veterinary Vaccine Industry Revenue Million Forecast, by Vaccine Type 2020 & 2033

- Table 20: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Vaccine Type 2020 & 2033

- Table 21: Global Veterinary Vaccine Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 22: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 23: Global Veterinary Vaccine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Germany Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: France Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Italy Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Italy Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Spain Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Spain Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Veterinary Vaccine Industry Revenue Million Forecast, by Vaccine Type 2020 & 2033

- Table 38: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Vaccine Type 2020 & 2033

- Table 39: Global Veterinary Vaccine Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 40: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 41: Global Veterinary Vaccine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: China Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: China Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Japan Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Japan Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: India Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Australia Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Australia Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: South Korea Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: South Korea Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global Veterinary Vaccine Industry Revenue Million Forecast, by Vaccine Type 2020 & 2033

- Table 56: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Vaccine Type 2020 & 2033

- Table 57: Global Veterinary Vaccine Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 58: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 59: Global Veterinary Vaccine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: GCC Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: GCC Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: South Africa Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: South Africa Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of Middle East and Africa Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: Rest of Middle East and Africa Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: Global Veterinary Vaccine Industry Revenue Million Forecast, by Vaccine Type 2020 & 2033

- Table 68: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Vaccine Type 2020 & 2033

- Table 69: Global Veterinary Vaccine Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 70: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 71: Global Veterinary Vaccine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 72: Global Veterinary Vaccine Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 73: Brazil Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Brazil Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Argentina Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Argentina Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Rest of South America Veterinary Vaccine Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: Rest of South America Veterinary Vaccine Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Veterinary Vaccine Industry?

The projected CAGR is approximately 8.13%.

2. Which companies are prominent players in the Veterinary Vaccine Industry?

Key companies in the market include Boehringer Ingelheim International GmbH, Merck & Co Inc, HIPRA, Phibro Animal Health Corporation, Ceva Sante Animale, Virbac, Elanco Animal Health, Zoetis Inc, Hester Biosciences Limited.

3. What are the main segments of the Veterinary Vaccine Industry?

The market segments include Vaccine Type, Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 18.18 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidence of Livestock Diseases; Increasing Pet Adoption Globally; Initiatives by Government Agencies. Animal Associations. and Leading Players.

6. What are the notable trends driving market growth?

The Canine Vaccines Segment is Expected to Hold a Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Storage Costs for Vaccines; Shortage of Veterinarians and Skilled Farm Workers.

8. Can you provide examples of recent developments in the market?

In September 2022, Merck Animal Health launched NobivacIntra-Trac Oral BbPi for the dual prevention of two major canine respiratory pathogens.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Veterinary Vaccine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Veterinary Vaccine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Veterinary Vaccine Industry?

To stay informed about further developments, trends, and reports in the Veterinary Vaccine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence