Key Insights

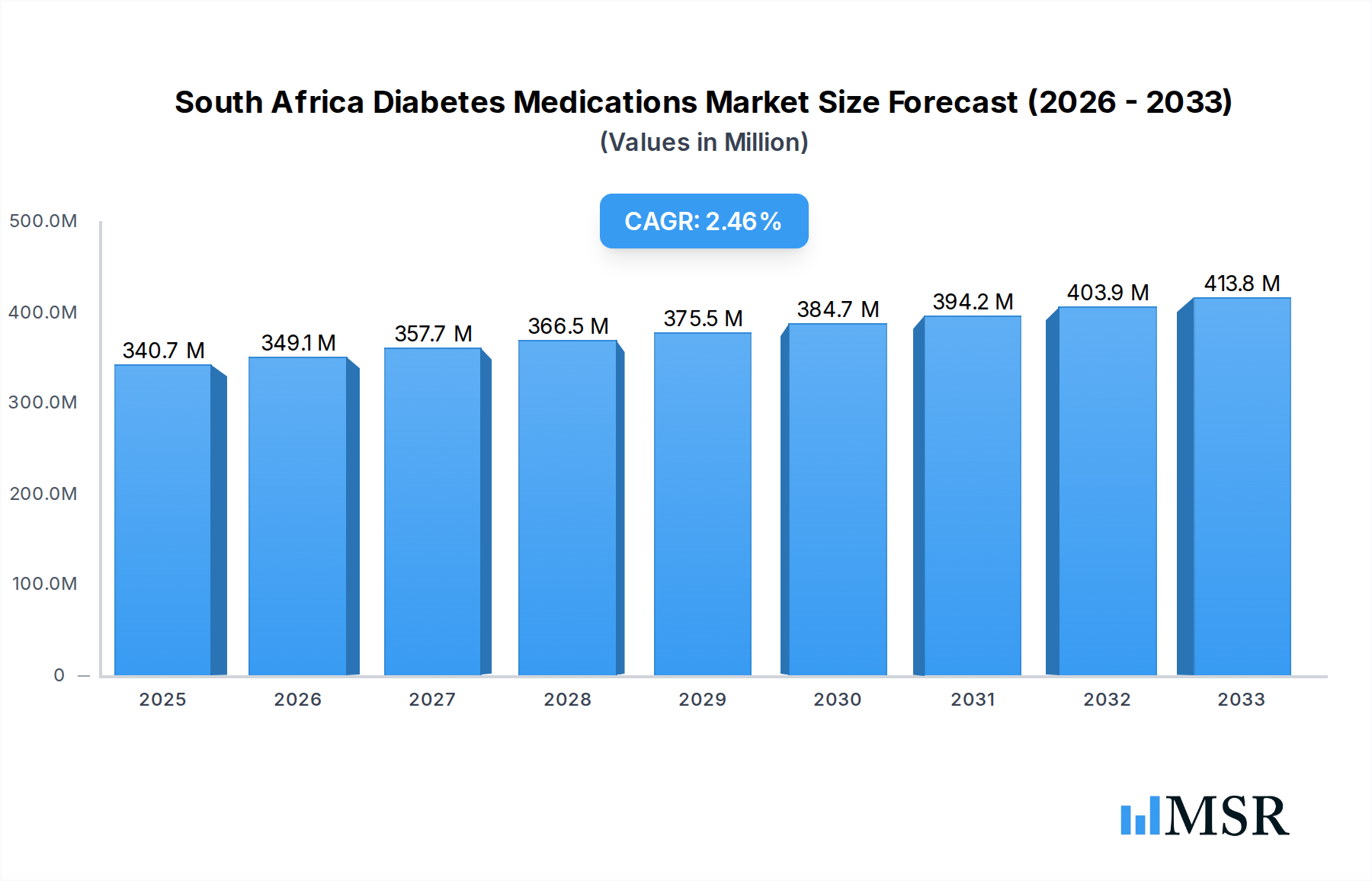

The South African diabetes medications market is poised for steady growth, with a projected market size of $340.72 million in 2025, expanding at a Compound Annual Growth Rate (CAGR) of 2.46% through 2033. This growth is underpinned by increasing diabetes prevalence, a growing awareness of treatment options, and advancements in pharmaceutical research. Key market drivers include the rising incidence of type 2 diabetes, an aging population with a higher predisposition to chronic diseases, and expanding healthcare access, particularly in urban centers like Gauteng and Western Cape. The market's expansion is also fueled by the introduction of novel therapeutic agents and the increasing adoption of both oral anti-diabetic drugs and advanced injectable treatments. The demand for insulin and non-insulin injectable drugs is particularly strong, reflecting a shift towards more effective and patient-convenient management of diabetes.

South Africa Diabetes Medications Market Market Size (In Million)

The competitive landscape in South Africa is dynamic, featuring global pharmaceutical giants such as Novo Nordisk A/S, Sanofi Aventis, and Eli Lilly, alongside local players contributing to market innovation and accessibility. However, the market faces certain restraints, including the high cost of some advanced diabetes medications, which can limit accessibility for a significant portion of the population. Affordability and reimbursement policies play a crucial role in shaping market penetration. Furthermore, lifestyle-related factors and the need for comprehensive diabetes management programs, encompassing diet, exercise, and regular monitoring, continue to be critical areas for development and public health initiatives to truly combat the rising tide of diabetes in the region. Despite these challenges, the overall outlook for the South African diabetes medications market remains positive, driven by unmet medical needs and ongoing efforts to improve patient outcomes.

South Africa Diabetes Medications Market Company Market Share

South Africa Diabetes Medications Market: Comprehensive Report (2019–2033)

This in-depth market research report provides a granular analysis of the South Africa Diabetes Medications Market, offering unparalleled insights for industry stakeholders. Covering the historical period of 2019-2024 and a forecast period extending from 2025 to 2033, with a base year of 2025, this report is your definitive guide to understanding market dynamics, growth drivers, competitive landscape, and emerging opportunities within South Africa's rapidly evolving diabetes treatment sector. We delve into key drug classes, regional market nuances, and the strategic initiatives of leading pharmaceutical giants, equipping you with the knowledge to navigate this critical market.

South Africa Diabetes Medications Market Market Concentration & Dynamics

The South Africa Diabetes Medications Market exhibits a moderate to high concentration, with a few key players dominating a significant portion of the market share. However, the competitive landscape is dynamic, influenced by continuous innovation and strategic partnerships. The innovation ecosystem is spurred by global pharmaceutical research and development, with local adaptations and clinical trials playing a crucial role. Regulatory frameworks, overseen by entities like the South African Health Products Regulatory Authority (SAHPRA), are stringent but evolving to accommodate new therapeutic advancements.

- Market Concentration: Dominated by key players like Novo Nordisk A/S, Sanofi Aventis, and Eli Lilly, who hold substantial market share in insulin and oral anti-diabetic segments.

- Innovation Ecosystem: Driven by global R&D, with a focus on novel drug delivery systems, combination therapies, and personalized medicine approaches for diabetes management.

- Regulatory Frameworks: SAHPRA's stringent approval processes ensure drug safety and efficacy, influencing market entry timelines for new medications.

- Substitute Products: Traditional treatments and lifestyle modifications act as substitutes, but the growing prevalence of diabetes necessitates advanced pharmacological interventions.

- End-User Trends: Increasing patient awareness, demand for convenience, and access to affordable treatments are shaping prescribing patterns.

- M&A Activities: While significant M&A activity is less frequent in this specific market, strategic collaborations and licensing agreements are common to expand market reach and product portfolios. The M&A deal count for major acquisitions specifically within the South African diabetes medication sector is estimated to be low, typically less than 5 significant deals observed in the historical period.

South Africa Diabetes Medications Market Industry Insights & Trends

The South Africa Diabetes Medications Market is experiencing robust growth, projected to achieve a significant market size of over xx Million by 2025 and grow at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This expansion is fundamentally driven by a confluence of escalating diabetes prevalence, increasing healthcare expenditure, and a growing emphasis on proactive disease management. The rising incidence of type 2 diabetes, directly linked to lifestyle changes, urbanization, and an aging population, is the primary catalyst. Technological advancements are revolutionizing treatment paradigms, with the introduction of advanced insulins, sophisticated oral anti-diabetic agents like SGLT2 inhibitors and GLP-1 receptor agonists, and innovative injectable non-insulin therapies offering improved efficacy and patient adherence.

Furthermore, evolving consumer behaviors are playing a pivotal role. Patients are becoming more informed and actively involved in their treatment decisions, seeking therapies that offer not just glycemic control but also cardiovascular and renal benefits, reflecting a holistic approach to diabetes care. The government's increasing focus on public health initiatives and the expansion of medical aid coverage are further bolstering market access and affordability. The integration of digital health solutions, such as continuous glucose monitoring (CGM) devices and diabetes management apps, is enhancing patient engagement and adherence, indirectly driving the demand for medications that complement these technologies. The competitive landscape is characterized by intense research and development efforts focused on developing drugs with fewer side effects, improved convenience, and better patient outcomes. Key players are investing heavily in clinical trials and strategic partnerships to secure market leadership. The market is also witnessing a trend towards combination therapies, offering more effective glycemic control with a single prescription, thereby improving patient compliance and reducing the pill burden. The underlying economic stability and growing disposable income in certain segments of the South African population also contribute to the increasing demand for advanced and more expensive diabetes medications. The overall trend is towards more personalized and patient-centric treatment strategies.

Key Markets & Segments Leading South Africa Diabetes Medications Market

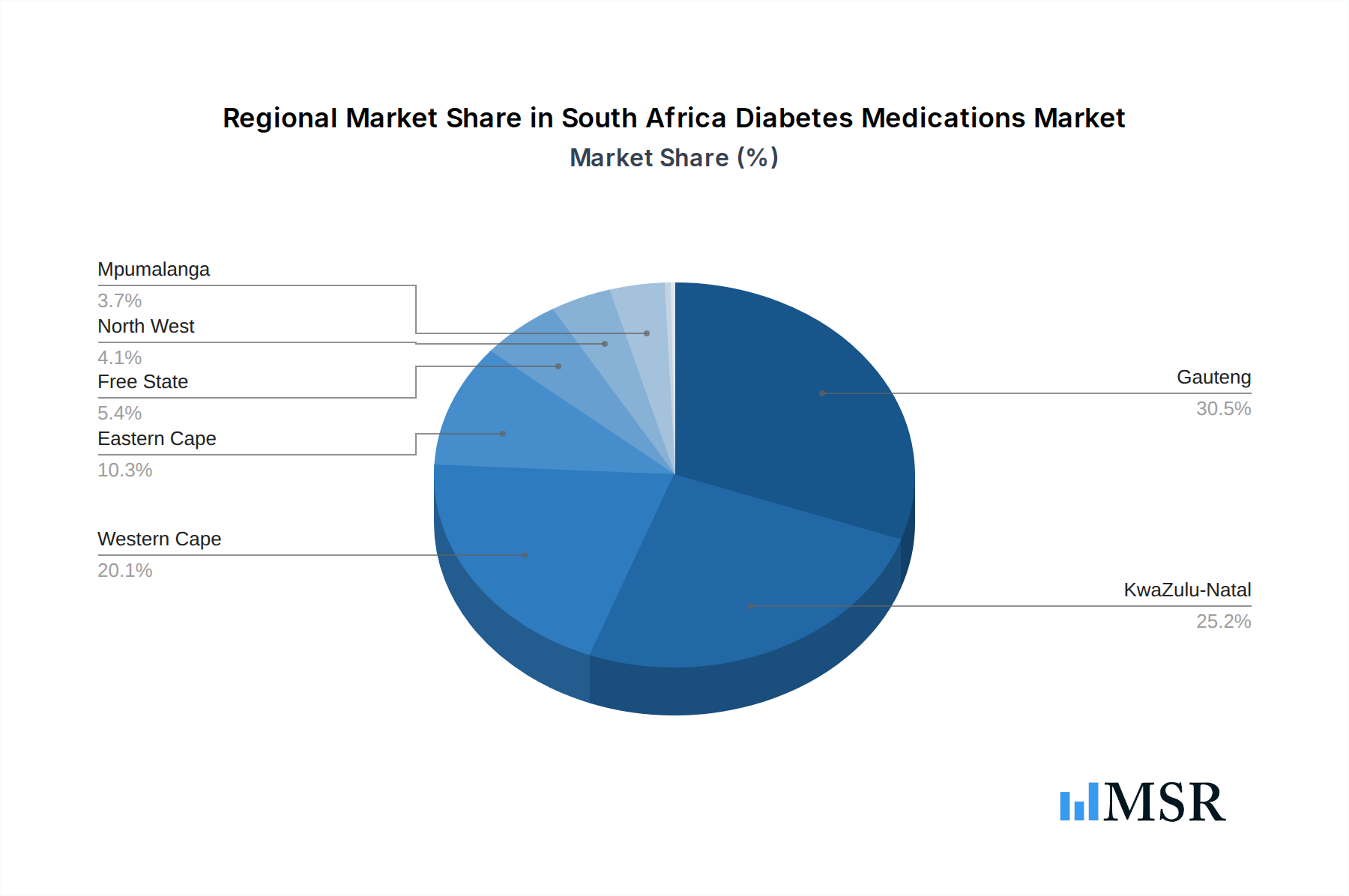

The South Africa Diabetes Medications Market is dynamically segmented, with Oral Anti-diabetic drugs currently leading in terms of market share and volume, closely followed by Insulins. However, the Non-insulin injectable drugs segment is exhibiting the fastest growth rate, driven by innovation and increasing physician preference for advanced therapeutic options. Geographically, Gauteng emerges as the dominant region, accounting for the largest market share due to its high population density, advanced healthcare infrastructure, and concentration of medical specialists.

Dominant Drug Class: Oral Anti-diabetic drugs

- Drivers: High prevalence of type 2 diabetes, patient convenience, cost-effectiveness compared to injectables, and a wide array of approved generic and branded options.

- Detailed Dominance: Oral anti-diabetics, including metformin, sulfonylureas, DPP-4 inhibitors, and SGLT2 inhibitors, form the cornerstone of initial diabetes management for a vast majority of patients in South Africa. Their accessibility and familiarity among both healthcare providers and patients contribute to their sustained market leadership.

Fastest Growing Drug Class: Non-insulin injectable drugs

- Drivers: Superior efficacy in glycemic control, cardiovascular and renal protective benefits of newer agents (GLP-1 RAs), and increasing adoption for complex diabetes cases.

- Detailed Dominance: The advent of GLP-1 receptor agonists and newer insulin formulations has significantly boosted this segment. These drugs offer a more targeted approach to diabetes management, addressing weight management and cardiovascular risks alongside blood sugar control.

Leading Region: Gauteng

- Drivers: Highest population density in South Africa, leading to a larger patient pool. Advanced and well-established healthcare infrastructure, including tertiary hospitals and specialized diabetes clinics. Concentration of key opinion leaders and prescribing physicians. Higher disposable income and better access to medical aid schemes, facilitating the uptake of advanced medications.

- Detailed Dominance: Gauteng's economic and demographic significance translates directly into higher demand for all categories of diabetes medications. The presence of major pharmaceutical company headquarters and distribution hubs further solidifies its leading position.

Significant Contributing Regions: KwaZulu-Natal and Western Cape also represent substantial markets due to their significant populations and developing healthcare systems.

South Africa Diabetes Medications Market Product Developments

Product innovation in the South Africa Diabetes Medications Market is primarily focused on enhancing efficacy, improving patient convenience, and mitigating side effects. Key developments include the launch of newer generation oral anti-diabetic drugs with combined benefits, advanced insulin formulations offering more physiological profiles, and novel non-insulin injectable therapies like GLP-1 receptor agonists that provide significant weight loss and cardiovascular protection. The market is also seeing a rise in combination products, simplifying treatment regimens and improving patient adherence.

Challenges in the South Africa Diabetes Medications Market Market

The South Africa Diabetes Medications Market faces several challenges that could impede its growth trajectory. Regulatory hurdles, including lengthy approval processes for new drugs and variations in pricing regulations, can delay market entry. Supply chain disruptions, exacerbated by logistical complexities and import dependencies, can lead to stockouts and affect patient access. Affordability and access remain significant concerns, particularly for lower-income populations, as advanced therapies are often expensive. Intense competitive pressures from both branded and generic manufacturers can impact profit margins. The limited awareness and adoption of newer technologies in rural areas also pose a barrier.

Forces Driving South Africa Diabetes Medications Market Growth

Several powerful forces are driving the growth of the South Africa Diabetes Medications Market. The escalating prevalence of diabetes, a direct consequence of changing lifestyles and an aging population, is the most significant driver. Increased healthcare expenditure and improved access to medical insurance are enhancing the affordability of treatments. Technological advancements leading to the development of more effective and patient-friendly medications are creating new market opportunities. Growing patient awareness and demand for comprehensive diabetes management, including benefits beyond glycemic control, are also propelling market expansion. Government initiatives aimed at improving public health outcomes further support market growth.

Challenges in the South Africa Diabetes Medications Market Market

Long-term growth catalysts for the South Africa Diabetes Medications Market are rooted in sustained innovation and strategic market expansion. The ongoing development of novel drug classes with enhanced efficacy and improved safety profiles, such as next-generation incretins and advanced insulin analogs, will continue to drive demand. Strategic partnerships between pharmaceutical companies, research institutions, and healthcare providers will accelerate the clinical validation and adoption of new treatments. Furthermore, expanding access to these advanced therapies in underserved regions through innovative distribution models and patient support programs will unlock significant market potential.

Emerging Opportunities in South Africa Diabetes Medications Market

Emerging opportunities in the South Africa Diabetes Medications Market are ripe for exploration. The increasing demand for personalized medicine tailored to individual patient profiles and genetic predispositions presents a significant avenue for growth. The burgeoning digital health ecosystem, encompassing remote patient monitoring and AI-driven diagnostic tools, offers a platform to integrate advanced medication management. Growing interest in preventative diabetes care and early intervention strategies also opens doors for innovative therapeutic approaches. Furthermore, the expansion of the generic drug market, particularly for established oral anti-diabetic agents, can cater to a broader patient base and drive volume growth.

Leading Players in the South Africa Diabetes Medications Market Sector

- Novo Nordisk A/S

- Sanofi Aventis

- Eli Lilly

- Merck and Co

- Pfizer

- Janssen Pharmaceuticals

- Boehringer Ingelheim

- AstraZeneca

- Takeda

- Bristol Myers Squibb

- Astellas

- Other

Key Milestones in South Africa Diabetes Medications Market Industry

- September 2023: Novo Nordisk revealed a fresh collaboration aimed at setting up human insulin manufacturing in South Africa, demonstrating an increased dedication to delivering essential treatment to individuals with diabetes throughout Africa.

- December 2022: Boehringer Ingelheim announced The DINAMO Phase III clinical trial met its primary endpoint by demonstrating a statistically significant reduction in HbA1c with empagliflozin compared with placebo for children and adolescents aged 10-17 years living with type 2 diabetes. The DINAMO (Diabetes Study of Linagliptin and Empagliflozin In Children And Adolescents) trial included youth aged 10-17 with type 2 diabetes and HbA1c 6.5% and 10.5%.

Strategic Outlook for South Africa Diabetes Medications Market Market

The strategic outlook for the South Africa Diabetes Medications Market remains highly positive, driven by sustained demand and ongoing innovation. Growth accelerators include the continued introduction of novel therapeutic agents with demonstrated cardiovascular and renal benefits, expanding market access through public-private partnerships, and leveraging digital health technologies for improved patient engagement and adherence. The market is expected to witness further consolidation through strategic alliances and licensing agreements to expand product portfolios and geographical reach. Companies focusing on patient-centric solutions and cost-effective treatment options will be well-positioned for long-term success.

South Africa Diabetes Medications Market Segmentation

-

1. Drug Class

- 1.1. Oral Anti-diabetic drugs

- 1.2. Insulins

- 1.3. Non-insulin injectable drugs

-

2. Region

- 2.1. Gauteng

- 2.2. KwaZulu-Natal

- 2.3. Western Cape

- 2.4. Eastern Cape

- 2.5. Free State

- 2.6. North West

- 2.7. Mpumalanga

- 2.8. Northern Cape

- 2.9. Limpopo

South Africa Diabetes Medications Market Segmentation By Geography

- 1. South Africa

South Africa Diabetes Medications Market Regional Market Share

Geographic Coverage of South Africa Diabetes Medications Market

South Africa Diabetes Medications Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.46% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 5.1.1. Oral Anti-diabetic drugs

- 5.1.2. Insulins

- 5.1.3. Non-insulin injectable drugs

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Gauteng

- 5.2.2. KwaZulu-Natal

- 5.2.3. Western Cape

- 5.2.4. Eastern Cape

- 5.2.5. Free State

- 5.2.6. North West

- 5.2.7. Mpumalanga

- 5.2.8. Northern Cape

- 5.2.9. Limpopo

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. South Africa

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 6. South Africa Diabetes Medications Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 6.1.1. Oral Anti-diabetic drugs

- 6.1.2. Insulins

- 6.1.3. Non-insulin injectable drugs

- 6.2. Market Analysis, Insights and Forecast - by Region

- 6.2.1. Gauteng

- 6.2.2. KwaZulu-Natal

- 6.2.3. Western Cape

- 6.2.4. Eastern Cape

- 6.2.5. Free State

- 6.2.6. North West

- 6.2.7. Mpumalanga

- 6.2.8. Northern Cape

- 6.2.9. Limpopo

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Pfizer

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Takeda

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Other

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Janssen Pharmaceuticals

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Eli Lilly

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Novartis

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Merck and Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 AstraZeneca

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sanofi Aventis

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Bristol Myers Squibb

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Novo Nordisk A/S

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Boehringer Ingelheim

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Sanofi Aventis

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Astellas

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 Pfizer

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Africa Diabetes Medications Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South Africa Diabetes Medications Market Share (%) by Company 2025

List of Tables

- Table 1: South Africa Diabetes Medications Market Revenue Million Forecast, by Drug Class 2020 & 2033

- Table 2: South Africa Diabetes Medications Market Revenue Million Forecast, by Region 2020 & 2033

- Table 3: South Africa Diabetes Medications Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: South Africa Diabetes Medications Market Revenue Million Forecast, by Drug Class 2020 & 2033

- Table 5: South Africa Diabetes Medications Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: South Africa Diabetes Medications Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Africa Diabetes Medications Market?

The projected CAGR is approximately 2.46%.

2. Which companies are prominent players in the South Africa Diabetes Medications Market?

Key companies in the market include Pfizer, Takeda, Other, Janssen Pharmaceuticals, Eli Lilly, Novartis, Merck and Co, AstraZeneca, Sanofi Aventis, Bristol Myers Squibb, Novo Nordisk A/S, Boehringer Ingelheim, Sanofi Aventis, Astellas.

3. What are the main segments of the South Africa Diabetes Medications Market?

The market segments include Drug Class, Region.

4. Can you provide details about the market size?

The market size is estimated to be USD 340.72 Million as of 2022.

5. What are some drivers contributing to market growth?

; The Rise in Global Prevalence of Cases of Obesity due to Modern Sedentary Lifestyles; Rise in Awareness and Disposable Income in Developed Economies.

6. What are the notable trends driving market growth?

The oral anti-diabetic drugs segment holds the highest market share in the South Africa Diabetes Drugs Market in the current year.

7. Are there any restraints impacting market growth?

; Highly Cost of Branded Products in Emerging Countries; Severe Adverse Associated with Medication Including Seizures. Suicidal Attempts and Even Death; Adoption of Traditional Yoga and Herbal Products.

8. Can you provide examples of recent developments in the market?

Spetmber 2023: Novo Nordisk has revealed a fresh collaboration aimed at setting up human insulin manufacturing in South Africa, demonstrating an increased dedication to delivering essential treatment to individuals with diabetes throughout Africa.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Africa Diabetes Medications Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Africa Diabetes Medications Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Africa Diabetes Medications Market?

To stay informed about further developments, trends, and reports in the South Africa Diabetes Medications Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence