Key Insights

Sweden's cybersecurity market is projected for significant expansion, driven by increasing digitalization and evolving threat landscapes. The market is estimated at $1.85 billion with a Compound Annual Growth Rate (CAGR) of 9.04% from 2025 to 2033. Growing awareness of sophisticated threats like ransomware, phishing, and data breaches necessitates advanced security solutions. Key sectors including BFSI, Healthcare, and Government & Defense are leading investment due to stringent regulatory compliance and the sensitive nature of data handled. The adoption of cloud-based security and demand for specialized services such as application, cloud, and data security are further propelling market growth. Leading companies are actively enhancing their presence and offerings, fostering competition and innovation.

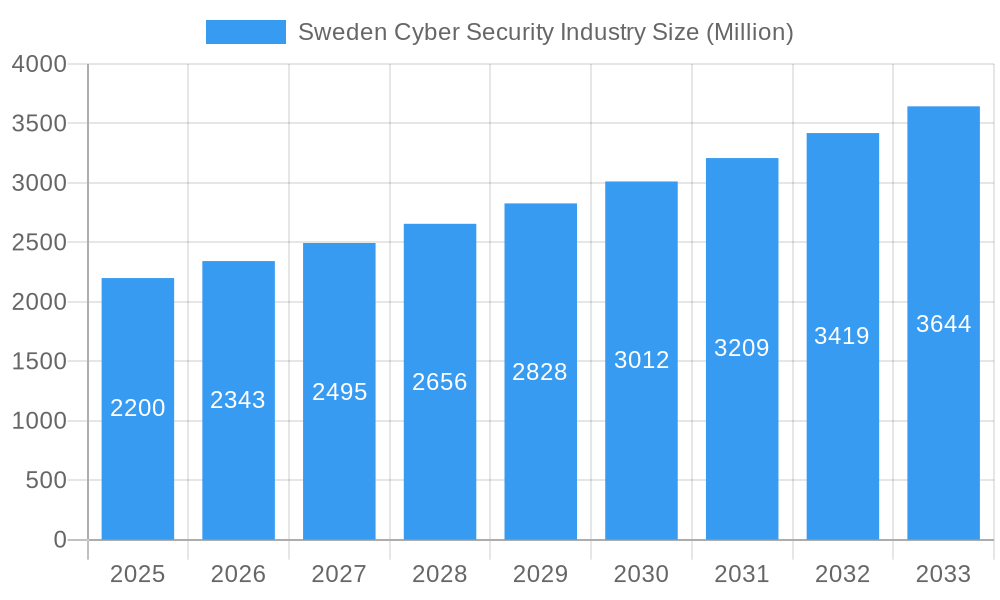

Sweden Cyber Security Industry Market Size (In Billion)

Key trends shaping the Swedish cybersecurity sector include the integration of AI and ML for advanced threat detection and response, the adoption of zero-trust architectures, and a strong emphasis on data privacy and GDPR compliance. The expanding Internet of Things (IoT) ecosystem across industries introduces new attack vectors, increasing the demand for comprehensive IoT security. While a cybersecurity skills shortage and implementation costs present challenges, the imperative for robust digital protection and the continuous evolution of cyber threats ensure a dynamic and growing market for cybersecurity solutions in Sweden, encompassing both cloud and on-premise deployments.

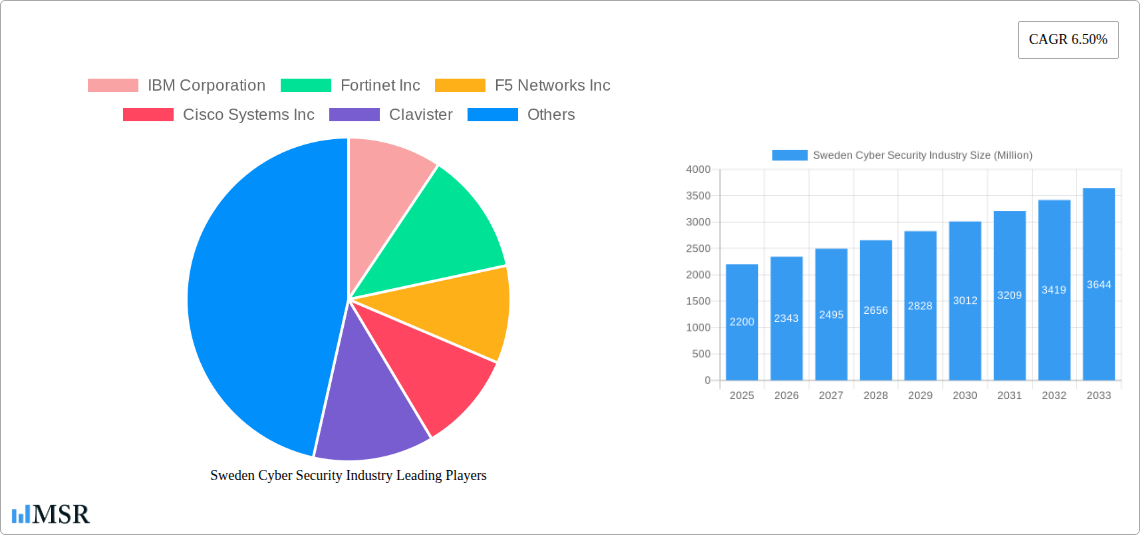

Sweden Cyber Security Industry Company Market Share

Gain critical insights into Sweden's dynamic cybersecurity market. This report, spanning 2019–2033 with a base year of 2025, provides a thorough analysis of market dynamics, emerging trends, and strategic opportunities. Identify key growth drivers, leading vendors, and critical challenges defining the future of cybersecurity in Sweden. An indispensable resource for industry professionals, IT leaders, and strategic planners navigating this high-growth sector.

Sweden Cyber Security Industry Market Concentration & Dynamics

The Swedish cyber security industry exhibits a dynamic market concentration, characterized by a healthy mix of established global players and innovative domestic enterprises. While major international corporations like IBM Corporation, Fortinet Inc, F5 Networks Inc, Cisco Systems Inc, Intel Security (Intel Corporation), and Dell Technologies Inc hold significant market share, specialized Swedish companies such as Clavister, AVG Technologies, and IDECSI Enterprise Security are carving out niche leadership in specific segments. The innovation ecosystem is robust, fueled by strong government investment in digital infrastructure and a highly skilled workforce. Regulatory frameworks, driven by GDPR and evolving national security mandates, are becoming increasingly stringent, pushing companies to adopt advanced security solutions and services. Substitute products, while present in the form of basic IT security tools, are largely outpaced by the sophisticated, integrated solutions demanded by modern cyber threats. End-user trends showcase a growing demand for comprehensive protection across all sectors, with BFSI, Healthcare, and Government & Defense leading adoption. Mergers and Acquisitions (M&A) activities are on the rise as larger players seek to expand their offerings and market reach, with an estimated 15-20 M&A deals annually in the past two years, reflecting ongoing consolidation and strategic expansion.

Sweden Cyber Security Industry Industry Insights & Trends

The Swedish cyber security market is poised for substantial growth, projected to reach approximately USD 10 Billion by 2033, with a Compound Annual Growth Rate (CAGR) of an impressive 15% during the forecast period of 2025–2033. This upward trajectory is primarily driven by an escalating volume and sophistication of cyber threats, including ransomware attacks, data breaches, and advanced persistent threats (APTs), which necessitate continuous investment in robust security infrastructure. The increasing digitalization of Swedish businesses across all sectors, from the traditionally conservative BFSI and Government & Defense to the rapidly transforming Manufacturing and Healthcare industries, creates a larger attack surface and, consequently, a greater demand for comprehensive cyber security solutions and services. Technological disruptions are a constant feature, with the integration of Artificial Intelligence (AI) and Machine Learning (ML) into security platforms for proactive threat detection and automated response, and the growing adoption of Zero Trust security models, significantly impacting market offerings. Evolving consumer behaviors, particularly in the wake of high-profile data breaches, have fostered a heightened awareness of data privacy and security, compelling organizations to prioritize customer data protection and demonstrate compliance with stringent data protection regulations. The surge in remote work, accelerated by recent global events, has further amplified the need for secure network access and endpoint security solutions, driving demand for cloud-based security services and VPN technologies. The Swedish government's commitment to becoming a leading digital nation, coupled with a strong emphasis on national security, provides a supportive environment for the cyber security industry, encouraging innovation and investment.

Key Markets & Segments Leading Sweden Cyber Security Industry

The Offering: Solution segment, particularly Cloud Security and Network Security, is currently dominating the Swedish cyber security market, accounting for an estimated 45% of the total market share in 2025. The escalating adoption of cloud computing across all industries, driven by its scalability, flexibility, and cost-effectiveness, necessitates advanced cloud security solutions to protect sensitive data and applications residing in the cloud. Similarly, the critical need to secure ever-expanding network perimeters against sophisticated threats fuels the dominance of network security solutions, including firewalls, intrusion detection/prevention systems, and secure access service edge (SASE) architectures.

- Cloud Security Drivers:

- Rapid adoption of hybrid and multi-cloud strategies by enterprises.

- Increased regulatory compliance requirements for cloud data protection.

- Growing threat landscape targeting cloud environments.

- Network Security Drivers:

- The rise of remote work and the need for secure connectivity.

- The proliferation of IoT devices expanding the network attack surface.

- Advanced persistent threats (APTs) targeting network infrastructure.

The End User: BFSI and IT and Telecommunication sectors are the primary drivers of demand, collectively representing approximately 30% of the market revenue in 2025. These sectors are prime targets for cyberattacks due to the sensitive nature of the data they handle and their critical role in the economy. Consequently, they invest heavily in advanced security solutions and services to safeguard financial assets, customer information, and essential infrastructure. The Government & Defense sector also shows significant market presence, driven by national security concerns and the need to protect critical national infrastructure.

- BFSI Dominance Drivers:

- High value of financial assets and sensitive customer data.

- Strict regulatory compliance mandates (e.g., PSD2, GDPR).

- Sophisticated and evolving threat actors targeting financial institutions.

- IT and Telecommunication Dominance Drivers:

- Critical infrastructure that, if compromised, can have widespread societal impact.

- Handling vast amounts of user data and network traffic.

- Continuous innovation in services requires robust, adaptable security.

In terms of Deployment, Cloud deployment models are rapidly gaining traction, accounting for an estimated 55% of the market share in 2025, owing to their agility, scalability, and cost-efficiency. However, On-premise solutions continue to hold a significant share, especially within highly regulated industries like Government & Defense and BFSI, where data residency and control are paramount.

Sweden Cyber Security Industry Product Developments

Recent product developments in the Swedish cyber security industry underscore a strong focus on AI-driven threat intelligence, integrated security platforms, and enhanced data protection capabilities. Companies are rapidly evolving their offerings to combat sophisticated attack vectors, with advancements in application security focusing on DevSecOps integration and automated vulnerability scanning. Cloud security solutions are increasingly incorporating advanced data loss prevention (DLP) and identity and access management (IAM) features to address the complexities of hybrid cloud environments. Network security is seeing innovations in zero-trust architecture implementation and sophisticated threat hunting tools. These advancements aim to provide proactive defense mechanisms, reducing response times and minimizing the impact of cyber incidents, thereby offering a competitive edge.

Challenges in the Sweden Cyber Security Industry Market

The Swedish cyber security industry faces several key challenges. A significant barrier is the persistent shortage of skilled cyber security professionals, impacting the ability of companies to implement and manage advanced security solutions effectively. Regulatory complexities, while driving adoption, can also pose implementation hurdles for businesses, particularly SMEs, requiring substantial investment to ensure full compliance. Furthermore, the rapidly evolving threat landscape means that security solutions can quickly become outdated, necessitating continuous updates and investment. Competitive pressures from both global giants and agile startups also intensify the market.

Forces Driving Sweden Cyber Security Industry Growth

Several forces are propelling the growth of the Swedish cyber security industry. The escalating frequency and sophistication of cyber threats globally and within Sweden are the primary drivers, compelling organizations to prioritize cyber resilience. The ongoing digital transformation across all sectors, including the adoption of IoT and cloud technologies, expands the attack surface and necessitates robust security measures. Government initiatives and increasing awareness of data privacy regulations like GDPR are creating a strong demand for compliance-driven security solutions. Furthermore, Sweden's strong emphasis on innovation and its supportive ecosystem for technology development foster continuous advancement in security technologies.

Challenges in the Sweden Cyber Security Industry Market

Long-term growth catalysts for the Swedish cyber security market lie in continuous technological innovation and strategic market expansion. The integration of AI and machine learning for predictive threat analysis and autonomous response systems represents a significant evolution. Partnerships and collaborations between cybersecurity firms, cloud providers, and industry-specific organizations are crucial for developing tailored and comprehensive security frameworks. Furthermore, expanding the reach of Swedish cyber security expertise into emerging markets and addressing the unique security needs of burgeoning sectors like the green tech industry will unlock new avenues for growth and solidify Sweden's position as a cyber security leader.

Emerging Opportunities in Sweden Cyber Security Industry

Emerging opportunities in the Swedish cyber security industry are abundant, driven by new technological frontiers and evolving consumer expectations. The growing adoption of edge computing and the Internet of Things (IoT) presents a significant opportunity for specialized IoT security solutions. The increasing demand for privacy-enhancing technologies (PETs) and the rise of decentralized identity solutions offer avenues for innovation in data protection and user authentication. Furthermore, the growing focus on cyber resilience and business continuity planning post-pandemic creates demand for advanced incident response and recovery services. Opportunities also exist in providing specialized cyber security training and awareness programs for the workforce.

Leading Players in the Sweden Cyber Security Industry Sector

- IBM Corporation

- Fortinet Inc

- F5 Networks Inc

- Cisco Systems Inc

- Clavister

- AVG Technologies

- Intel Security (Intel Corporation)

- Dell Technologies Inc

- Capgemini

- IDECSI Enterprise Security

Key Milestones in Sweden Cyber Security Industry Industry

- May 2022: Cisco announced the public release of the Cisco Cloud Controls Framework (CCF), a comprehensive aggregation of national and international security compliance and certification requirements designed to simplify security management and compliance efforts.

- March 2022: YesWeHack, Europe's Bug Bounty platform, partnered with Telenor Sweden to identify potential vulnerabilities in its telecom infrastructure and bolster customer data protection, highlighting a proactive approach to security through crowdsourced vulnerability discovery.

Strategic Outlook for Sweden Cyber Security Industry Market

The strategic outlook for the Sweden Cyber Security Industry is exceptionally strong, driven by a confluence of factors. The increasing demand for advanced solutions to combat sophisticated cyber threats, coupled with the ongoing digital transformation across all sectors, creates a fertile ground for growth. Strategic focus on integrating AI and machine learning for proactive threat detection and automated response will be critical. Furthermore, fostering public-private partnerships to enhance national cyber resilience and investing in cybersecurity talent development will be key accelerators. The industry is well-positioned to capitalize on the growing global demand for secure digital environments.

Sweden Cyber Security Industry Segmentation

-

1. Offering

-

1.1. Solution

- 1.1.1. Application Security

- 1.1.2. Cloud Security

- 1.1.3. Data Security

- 1.1.4. Network Security

- 1.1.5. Other Solutions

- 1.2. Services

-

1.1. Solution

-

2. Deployment

- 2.1. Cloud

- 2.2. On-premise

-

3. End User

- 3.1. BFSI

- 3.2. Healthcare

- 3.3. Manufacturing

- 3.4. Government & Defense

- 3.5. IT and Telecommunication

- 3.6. Other End Users

Sweden Cyber Security Industry Segmentation By Geography

- 1. Sweden

Sweden Cyber Security Industry Regional Market Share

Geographic Coverage of Sweden Cyber Security Industry

Sweden Cyber Security Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks

- 3.2.2 the evolution of MSSPs

- 3.2.3 and adoption of cloud-first strategy

- 3.3. Market Restrains

- 3.3.1. Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness

- 3.4. Market Trends

- 3.4.1. Cloud Segment is one of the Factor Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Sweden Cyber Security Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Solution

- 5.1.1.1. Application Security

- 5.1.1.2. Cloud Security

- 5.1.1.3. Data Security

- 5.1.1.4. Network Security

- 5.1.1.5. Other Solutions

- 5.1.2. Services

- 5.1.1. Solution

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. BFSI

- 5.3.2. Healthcare

- 5.3.3. Manufacturing

- 5.3.4. Government & Defense

- 5.3.5. IT and Telecommunication

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Sweden

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 IBM Corporation

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Fortinet Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 F5 Networks Inc

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Cisco Systems Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Clavister

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 AVG Technologies

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Intel Security (Intel Corporation)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Dell Technologies Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Capgemini

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 IDECSI Enterprise Security

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 IBM Corporation

List of Figures

- Figure 1: Sweden Cyber Security Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Sweden Cyber Security Industry Share (%) by Company 2025

List of Tables

- Table 1: Sweden Cyber Security Industry Revenue billion Forecast, by Offering 2020 & 2033

- Table 2: Sweden Cyber Security Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 3: Sweden Cyber Security Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Sweden Cyber Security Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Sweden Cyber Security Industry Revenue billion Forecast, by Offering 2020 & 2033

- Table 6: Sweden Cyber Security Industry Revenue billion Forecast, by Deployment 2020 & 2033

- Table 7: Sweden Cyber Security Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 8: Sweden Cyber Security Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sweden Cyber Security Industry?

The projected CAGR is approximately 9.04%.

2. Which companies are prominent players in the Sweden Cyber Security Industry?

Key companies in the market include IBM Corporation, Fortinet Inc, F5 Networks Inc, Cisco Systems Inc, Clavister, AVG Technologies, Intel Security (Intel Corporation), Dell Technologies Inc, Capgemini, IDECSI Enterprise Security.

3. What are the main segments of the Sweden Cyber Security Industry?

The market segments include Offering, Deployment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.85 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks. the evolution of MSSPs. and adoption of cloud-first strategy.

6. What are the notable trends driving market growth?

Cloud Segment is one of the Factor Driving the Market.

7. Are there any restraints impacting market growth?

Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness.

8. Can you provide examples of recent developments in the market?

May 2022 - Cisco announced that it had released the Cisco Cloud Controls Framework (CCF) to the public. Cisco CCF is a comprehensive set of national and international security compliance and certification requirements aggregated in one framework.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sweden Cyber Security Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sweden Cyber Security Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sweden Cyber Security Industry?

To stay informed about further developments, trends, and reports in the Sweden Cyber Security Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence