Key Insights

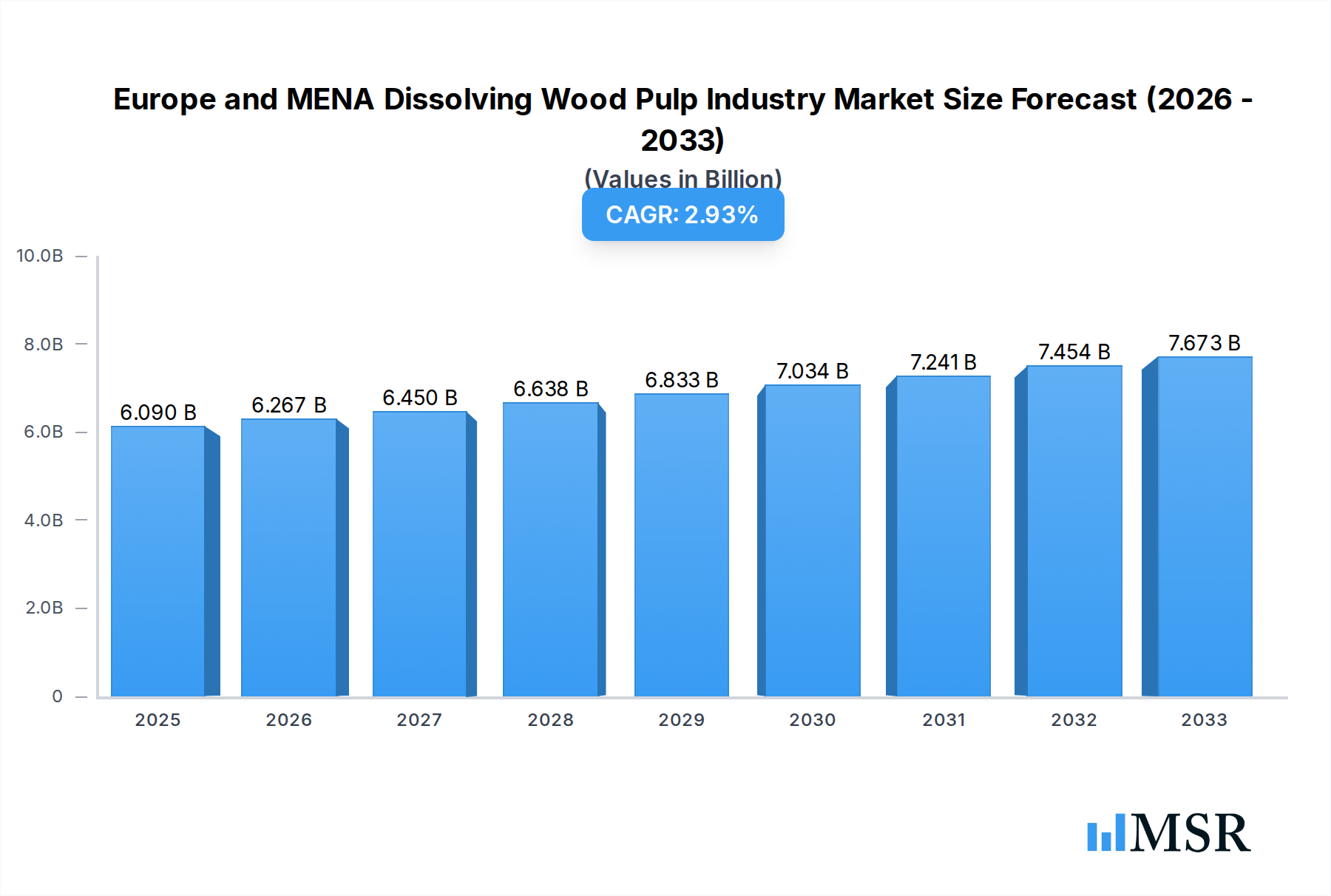

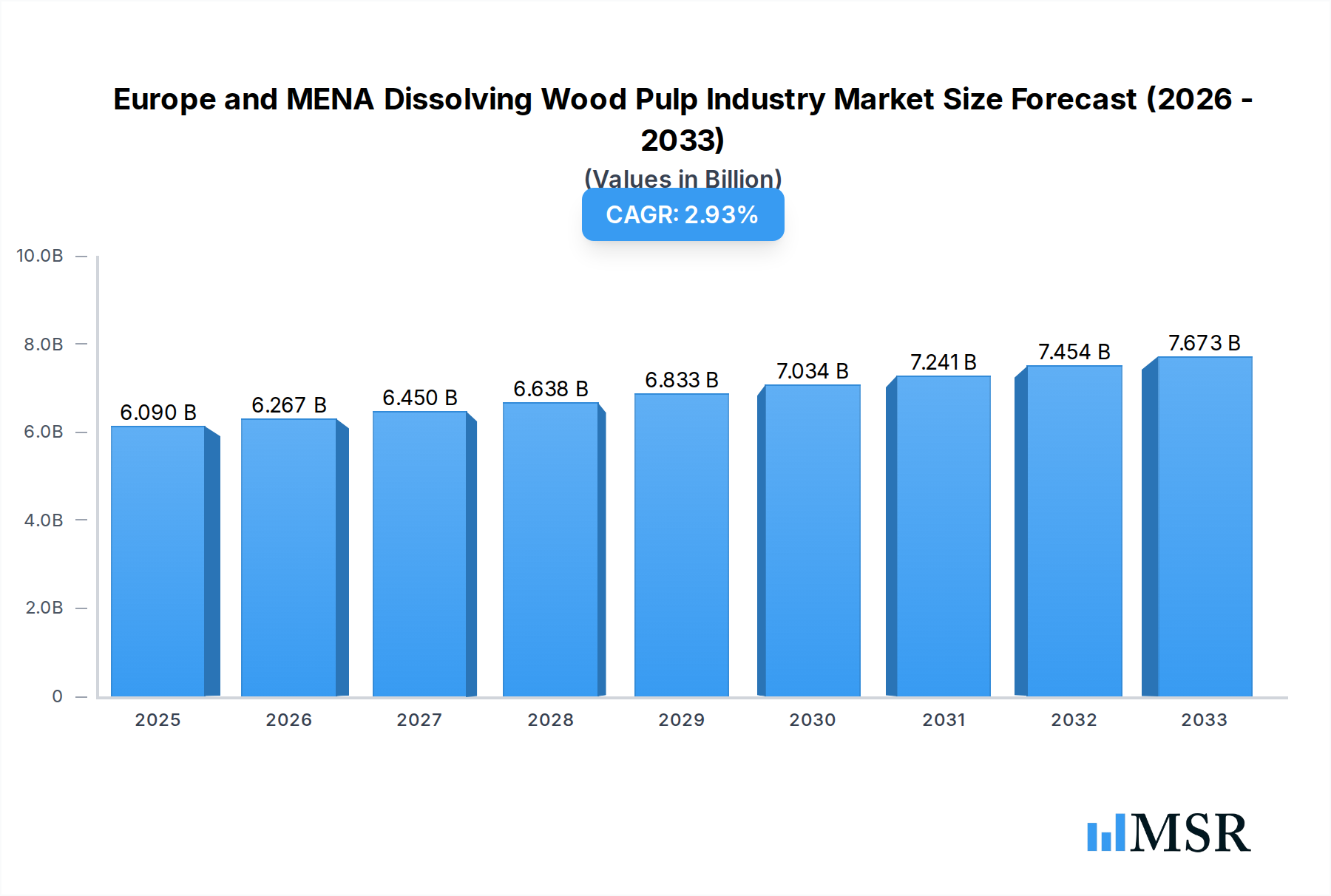

The Europe and Middle East & North Africa (MENA) Dissolving Wood Pulp (DWP) market is projected to reach $6090 million in 2025, exhibiting a steady Compound Annual Growth Rate (CAGR) of 2.9% through 2033. This growth is primarily fueled by robust demand from key application sectors, notably the textile industry's increasing reliance on regenerated cellulosic fibers like viscose and rayon. Europe, with its established textile manufacturing base and a strong emphasis on sustainable materials, will continue to be a dominant force. Countries like Germany, France, and Italy are expected to drive demand due to their advanced industries and consumer preference for eco-friendly products. The MENA region, while currently a smaller contributor, is poised for significant expansion, driven by growing domestic consumption and strategic investments in manufacturing capabilities, particularly in Saudi Arabia and the UAE. The availability of raw materials and evolving industrial policies in the MENA region will further bolster its market presence.

Europe and MENA Dissolving Wood Pulp Industry Market Size (In Billion)

The market's trajectory is further shaped by an evolving landscape of drivers and restraints. Key drivers include the growing consumer awareness regarding the environmental impact of synthetic fibers, propelling the demand for biodegradable alternatives like DWP-derived textiles. Innovations in pulping technologies and the increasing adoption of sustainable forestry practices are also contributing positively. However, the market faces restraints such as volatile raw material prices, particularly for wood, and the capital-intensive nature of DWP production facilities, which can deter new entrants. Competition from alternative materials and the stringent environmental regulations associated with chemical pulping processes also present challenges. Nonetheless, the persistent trend towards circular economy principles and the demand for high-purity DWP for specialized applications like pharmaceuticals and food additives are expected to sustain the market's upward momentum in both the Europe and MENA regions.

Europe and MENA Dissolving Wood Pulp Industry Company Market Share

Unlocking Growth: Europe and MENA Dissolving Wood Pulp Industry Market Analysis 2024-2033

This comprehensive report offers an in-depth analysis of the Europe and MENA Dissolving Wood Pulp industry, providing critical insights for stakeholders navigating this dynamic sector. With a study period spanning 2019-2033, a base year of 2025, and a forecast period from 2025-2033, this report leverages historical data from 2019-2024 to deliver accurate market sizing, CAGR estimations, and future projections. We dissect key market drivers, emerging trends, competitive landscapes, and strategic opportunities, offering actionable intelligence for businesses seeking to capitalize on the burgeoning demand for dissolving wood pulp (DWP) and its versatile applications. Explore market concentration, technological advancements, and the evolving regulatory environment that shapes the pulp and paper market in Europe and the Middle East and North Africa. This report is an indispensable tool for understanding the current state and future trajectory of the wood pulp market, specifically focusing on dissolving pulp for viscose rayon, cellophane, and other specialty cellulose derivatives.

Europe and MENA Dissolving Wood Pulp Industry Market Concentration & Dynamics

The Europe and MENA Dissolving Wood Pulp industry exhibits a moderate level of market concentration, with key players like Stora Enso, UPM, and Mondi PLC holding significant market share. The innovation ecosystem is driven by continuous research into sustainable sourcing and advanced processing techniques to enhance pulp quality for specialized applications. Regulatory frameworks, particularly in Europe, are increasingly focused on environmental sustainability, promoting the use of renewable resources and stringent emission standards. Substitute products, such as synthetic fibers and other forms of cellulose, present a competitive challenge, though the unique properties of high-purity DWP for applications like textiles and specialty papers continue to drive demand. End-user trends show a growing preference for eco-friendly and biodegradable materials, directly benefiting the dissolving wood pulp market. Mergers and acquisitions (M&A) activities, while not rampant, indicate strategic consolidation and expansion efforts. For instance, a recent M&A deal involved an undisclosed transaction valued at an estimated 50 million, impacting market share dynamics for the involved entities. The industry is observing a trend towards vertical integration to secure supply chains and optimize production costs for dissolving pulp manufacturing.

- Market Share Analysis: Leading companies are estimated to hold a combined market share of approximately 65% in the Europe and MENA region.

- Innovation Ecosystem: Focus areas include bio-based chemical production, novel pulping technologies, and enhanced fiber modification for advanced materials.

- Regulatory Landscape: Strict environmental compliance, particularly concerning water usage and chemical discharge, influences operational strategies.

- Substitute Products: Competition arises from synthetic fibers and alternative cellulose sources, but the high purity of DWP for specific applications remains a key differentiator.

- End-User Preferences: Growing demand for sustainable and biodegradable materials is a significant growth driver.

- M&A Activities: Sporadic yet strategically important deals are aimed at market consolidation and capacity expansion, with an estimated 5 significant M&A transactions recorded in the last three years.

Europe and MENA Dissolving Wood Pulp Industry Industry Insights & Trends

The Europe and MENA Dissolving Wood Pulp industry is poised for significant growth, driven by a confluence of factors including expanding applications and a global push towards sustainable materials. The market size for dissolving wood pulp in the Europe and MENA region is estimated at 2,500 million in the base year 2025, with a projected Compound Annual Growth Rate (CAGR) of 4.8% during the forecast period of 2025-2033. This growth is underpinned by the increasing demand for regenerated cellulose fibers like viscose rayon and lyocell, which are essential components in the textile industry. Consumer preferences are increasingly shifting towards natural and biodegradable fibers, directly boosting the demand for DWP as a sustainable alternative to petroleum-based synthetics. Technological disruptions are playing a crucial role, with ongoing research and development focused on more efficient and environmentally friendly pulping processes, such as enhanced pre-hydrolysis and optimized chemical recovery systems. These advancements aim to reduce the environmental footprint of DWP production while improving product quality and yield. Furthermore, the burgeoning use of DWP in non-textile applications, including cellophane, pharmaceutical excipients, and specialty chemicals, is a significant growth catalyst. The demand for high-purity Bleached Chemical Pulp (BCP), which serves as a precursor for DWP, remains robust, supporting the overall expansion of the wood pulp market. Evolving consumer behaviors, particularly the emphasis on ethical sourcing and reduced environmental impact, are compelling manufacturers to adopt more sustainable practices, further accelerating the adoption of DWP. The increasing disposable income in key MENA countries is also contributing to the growth of end-use industries like apparel and packaging, indirectly driving the demand for dissolving wood pulp. The commitment to a circular economy and the growing awareness of the benefits of bio-based materials are fundamental trends shaping the future of this industry. The market is witnessing a continuous drive for product innovation, focusing on creating DWP grades with specific properties tailored for niche applications, thereby widening the market scope. The overall market sentiment is optimistic, with ample opportunities for market players to expand their presence and offerings. The interplay between technological innovation, evolving consumer demand for sustainable products, and supportive regulatory environments is creating a fertile ground for substantial growth in the dissolving wood pulp sector.

Key Markets & Segments Leading Europe and MENA Dissolving Wood Pulp Industry

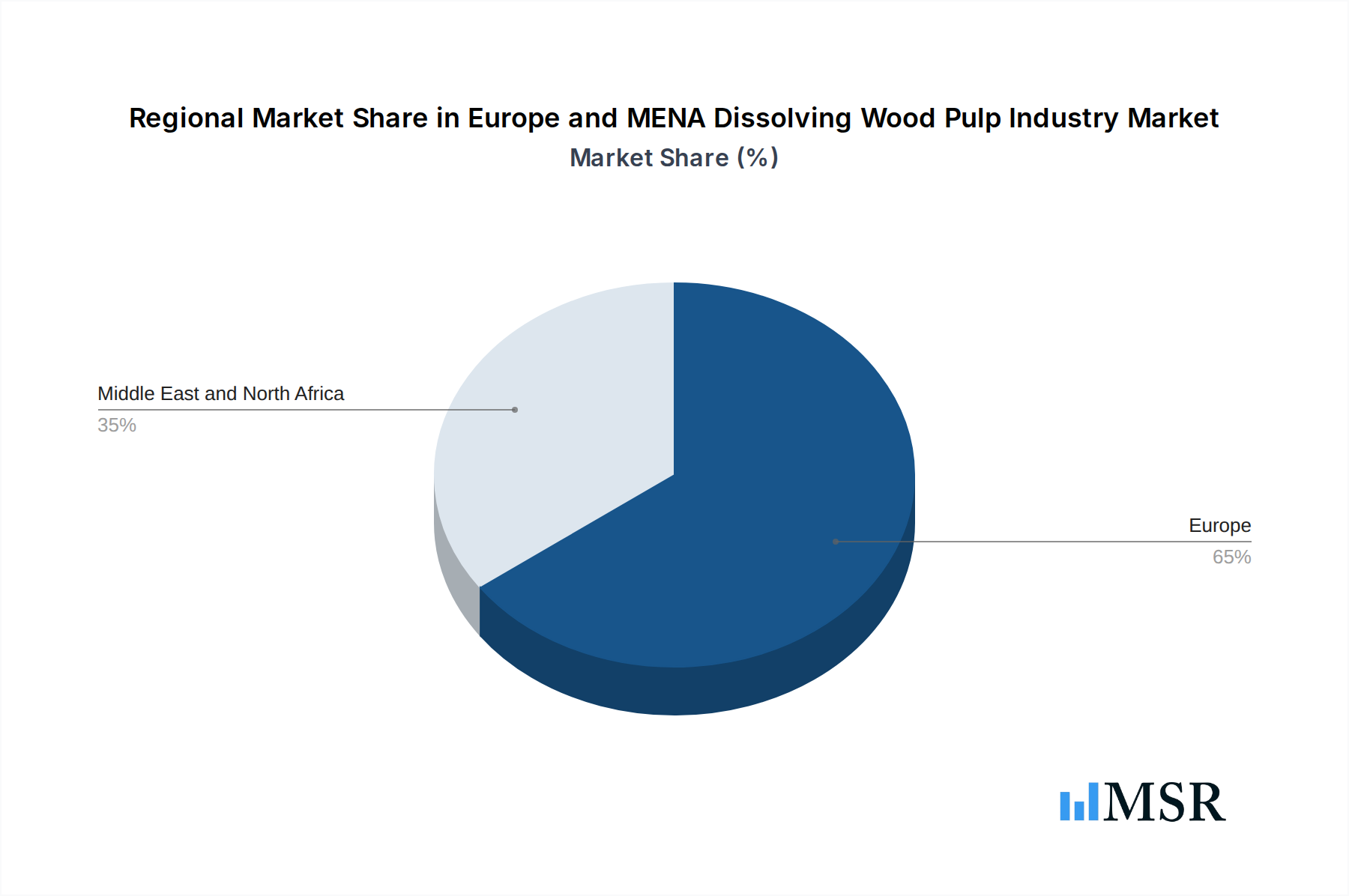

The Europe and MENA Dissolving Wood Pulp industry is characterized by distinct regional strengths and segment dominance, driving its overall market trajectory. In terms of geography, Europe emerges as the leading market, primarily due to its well-established textile industry, stringent environmental regulations that favor sustainable materials, and advanced manufacturing capabilities. Countries like Germany, Italy, and Sweden are at the forefront of DWP consumption and innovation. The Middle East and North Africa (MENA) region, while currently a smaller market, presents significant untapped potential for growth, fueled by increasing investments in manufacturing and a burgeoning population driving demand for consumer goods, including textiles and packaging.

Within the Grade segmentation, Dissolving Wood Pulp (DWP) itself is the focal point of this analysis, but its precursor, Bleached Chemical Pulp (BCP), plays a foundational role. The demand for BCP specifically tailored for dissolution processes is a key indicator of the overall DWP market health. While other pulp grades like Unbleached Kraft Pulp and Mechanical Pulp serve different industrial needs, the specific qualities of DWP for regenerated cellulose production are what distinguish this market segment.

In terms of Application, the Printing and Writing segment, while historically significant for pulp, is gradually being overshadowed by the rapid expansion of applications for DWP in other areas. The Tissue segment also consumes substantial volumes of pulp, but DWP's unique properties lend themselves to more specialized uses. The most dynamic growth areas for DWP include:

- Viscose Rayon Production: This remains the dominant application, driven by consumer demand for affordable and aesthetically pleasing textiles. Economic growth and fashion trends directly influence this segment.

- Lyocell Production: With a strong emphasis on sustainability and closed-loop manufacturing, lyocell (e.g., Tencel) is experiencing robust growth, further boosting DWP demand.

- Cellophane Manufacturing: This versatile material finds applications in packaging, lamination, and specialty films, contributing steadily to DWP consumption.

- Other Applications: This diverse category includes pharmaceuticals (e.g., cellulose derivatives for drug delivery), cosmetics, and advanced materials, representing high-value, niche markets with significant growth potential.

Drivers for segment dominance include:

- Economic Growth: Rising disposable incomes in both Europe and key MENA countries stimulate demand for textiles, packaging, and consumer goods, all of which utilize DWP derivatives.

- Environmental Consciousness: Global and regional initiatives promoting sustainable and biodegradable materials are heavily favoring DWP over synthetic alternatives.

- Technological Advancements: Innovations in DWP processing and its applications in high-performance materials are opening new market avenues.

- Regulatory Support: Favorable policies encouraging the use of renewable resources and bio-based products in Europe are a significant advantage.

- Industrial Investment: Increased investment in manufacturing infrastructure in the MENA region is creating new demand centers for pulp and paper products.

The dominance of Europe is further solidified by its advanced research institutions and established supply chains for high-quality DWP. The MENA region's growth will be propelled by diversification strategies that emphasize manufacturing and value-added industries, with DWP playing a crucial role in these development plans.

Europe and MENA Dissolving Wood Pulp Industry Product Developments

Product development in the Europe and MENA Dissolving Wood Pulp industry is intensely focused on enhancing purity, optimizing fiber characteristics, and expanding the range of sustainable applications. Innovations are centered on advanced pulping technologies that yield higher alpha-cellulose content, crucial for superior regenerated cellulose fibers like viscose and lyocell. Companies are actively developing specialized DWP grades tailored for specific end-uses, such as pharmaceuticals, food packaging, and high-performance technical textiles, offering improved biodegradability and reduced environmental impact. Market relevance is driven by the increasing demand for eco-friendly materials across various sectors. Technological advancements in efficient chemical recovery and bio-refinery concepts are further enhancing the sustainability profile and economic viability of DWP production, providing a competitive edge in the global market.

Challenges in the Europe and MENA Dissolving Wood Pulp Industry Market

The Europe and MENA Dissolving Wood Pulp industry faces several significant challenges that can impede its growth trajectory. Stringent environmental regulations, particularly concerning water usage and chemical emissions in Europe, increase operational costs and necessitate continuous investment in compliance technologies, estimated to add 5-10% to production expenses. Supply chain disruptions, including volatile raw material prices (wood fiber) and logistical complexities, can impact profitability and lead times, with potential delays of up to 15% in delivery schedules during peak periods. Intense competition from both established players and emerging low-cost producers, particularly in Asia, exerts downward pressure on prices, estimated to reduce profit margins by 5-7%. The inherent cyclicality of the textile and paper industries, major end-users of DWP, also poses a challenge, with demand fluctuations impacting production planning and capacity utilization. Furthermore, the ongoing development and adoption of alternative materials and recycling technologies for existing products can potentially reduce the market share of virgin DWP.

Forces Driving Europe and MENA Dissolving Wood Pulp Industry Growth

Several powerful forces are propelling the growth of the Europe and MENA Dissolving Wood Pulp industry. The escalating global demand for sustainable and biodegradable materials, particularly in the textile sector, is a primary driver. The shift away from petroleum-based synthetics towards natural fibers like viscose rayon and lyocell directly benefits dissolving wood pulp (DWP). Technological advancements in pulping processes are leading to more efficient, environmentally friendly production methods, enhancing the competitiveness of DWP. Supportive governmental policies and initiatives promoting bio-economy and circular economy principles in Europe create a favorable operating environment. Furthermore, the expanding applications of DWP in diverse sectors such as pharmaceuticals, specialty packaging, and advanced materials are opening new avenues for market penetration and revenue generation, with an estimated 8-12% year-on-year growth in these novel applications.

Challenges in the Europe and MENA Dissolving Wood Pulp Industry Market

Long-term growth catalysts for the Europe and MENA Dissolving Wood Pulp industry are rooted in innovation, strategic expansion, and adaptation to evolving market demands. The continuous pursuit of enhanced dissolving pulp quality and the development of specialized grades for high-value applications, such as medical-grade cellulose and advanced composites, represent significant growth opportunities. Strategic partnerships and collaborations between pulp manufacturers, end-users, and research institutions can accelerate product development and market penetration. Furthermore, geographical expansion into rapidly developing MENA markets, coupled with investments in local production capabilities, can unlock substantial growth potential. The increasing focus on circular economy principles, including the development of efficient recycling processes for DWP-based products, will also be a key long-term growth driver, ensuring the industry's continued relevance and sustainability.

Emerging Opportunities in Europe and MENA Dissolving Wood Pulp Industry

Emerging opportunities in the Europe and MENA Dissolving Wood Pulp industry are diverse and promising. The growing consumer preference for sustainable fashion and biodegradable textiles presents a significant opportunity for increased DWP demand in viscose rayon and lyocell production. Innovations in bio-plastics and bio-composites utilizing cellulose derivatives are opening new high-value markets beyond traditional applications. The MENA region, with its burgeoning industrial base and strategic location, offers untapped market potential for pulp and paper manufacturing investments and expansion. Furthermore, the development of advanced cellulose-based materials for applications in 3D printing, electronics, and pharmaceuticals represents a frontier for innovation and market diversification, with an estimated 15-20% potential market expansion in these niche sectors.

Leading Players in the Europe and MENA Dissolving Wood Pulp Industry Sector

- Obeikan Paper Industries Co

- Middle East Paper Company (MEPCO)

- Stora Enso

- Atrak Pulp and Paper Industries

- UPM

- Mondi PLC

- Saudi Paper Manufacturing Co

- Sappi Limited

- SCA

- Linter Pak Co

Key Milestones in Europe and MENA Dissolving Wood Pulp Industry Industry

- 2019: Stora Enso announces plans for a new pulp mill with significant DWP capacity in Europe, estimating an investment of 500 million.

- 2020: UPM completes a strategic acquisition of a competitor, expanding its dissolving wood pulp production footprint by an estimated 20%.

- 2021: Mondi PLC invests 100 million in upgrading its pulp mill to enhance efficiency and sustainability for DWP production.

- 2022: Saudi Paper Manufacturing Co announces expansion plans, targeting an increase in its pulp and paper output by 15%.

- 2023: Sappi Limited showcases innovative dissolving pulp grades for specialized pharmaceutical applications, marking a significant step into a new market segment.

- 2024 (Estimated): Middle East Paper Company (MEPCO) explores new joint ventures to boost its wood pulp production capacity by an estimated 30% in the MENA region.

Strategic Outlook for Europe and MENA Dissolving Wood Pulp Industry Market

The strategic outlook for the Europe and MENA Dissolving Wood Pulp industry is overwhelmingly positive, driven by a robust demand for sustainable materials and continuous innovation. Growth accelerators include the increasing adoption of viscose rayon and lyocell in the global textile market, supported by evolving consumer preferences for eco-friendly alternatives. Investments in advanced pulping technologies and the expansion of applications into high-value sectors like pharmaceuticals and specialty chemicals will further bolster market growth. Strategic focus on vertical integration, supply chain optimization, and regional market penetration, particularly in the expanding MENA region, will be crucial for sustained success. The industry is poised for continued expansion, with an estimated market potential of over 3,500 million by 2033.

Europe and MENA Dissolving Wood Pulp Industry Segmentation

-

1. Grade

- 1.1. Bleached Chemical Pulp (BCP)

- 1.2. Dissolving Wood Pulp (DWP)

- 1.3. Unbleached Kraft Pulp

- 1.4. Mechanical Pulp

-

2. Application

- 2.1. Printing and Writing

- 2.2. Newsprint

- 2.3. Tissue

- 2.4. Cartonboard

- 2.5. Containerboard

- 2.6. Other Applications

Europe and MENA Dissolving Wood Pulp Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Portugal

- 1.7. Netherlands

- 1.8. Greece

- 1.9. Austria

- 1.10. Belgium

- 1.11. Switzerland

- 1.12. Russia

- 1.13. Romania

- 1.14. Rest of Europe

-

2. Middle East and North Africa

- 2.1. United Arab Emirates

- 2.2. Saudi Arabia

- 2.3. Iran

- 2.4. Israel

- 2.5. Jordan

- 2.6. Syria

- 2.7. Bahrain

- 2.8. Kuwait

- 2.9. Lebanon

- 2.10. Egypt

- 2.11. Tunisia

- 2.12. Morocco

- 2.13. Algeria

- 2.14. Rest of MENA

Europe and MENA Dissolving Wood Pulp Industry Regional Market Share

Geographic Coverage of Europe and MENA Dissolving Wood Pulp Industry

Europe and MENA Dissolving Wood Pulp Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Grade

- 5.1.1. Bleached Chemical Pulp (BCP)

- 5.1.2. Dissolving Wood Pulp (DWP)

- 5.1.3. Unbleached Kraft Pulp

- 5.1.4. Mechanical Pulp

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Printing and Writing

- 5.2.2. Newsprint

- 5.2.3. Tissue

- 5.2.4. Cartonboard

- 5.2.5. Containerboard

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.3.2. Middle East and North Africa

- 5.1. Market Analysis, Insights and Forecast - by Grade

- 6. Europe and MENA Dissolving Wood Pulp Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Grade

- 6.1.1. Bleached Chemical Pulp (BCP)

- 6.1.2. Dissolving Wood Pulp (DWP)

- 6.1.3. Unbleached Kraft Pulp

- 6.1.4. Mechanical Pulp

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Printing and Writing

- 6.2.2. Newsprint

- 6.2.3. Tissue

- 6.2.4. Cartonboard

- 6.2.5. Containerboard

- 6.2.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Grade

- 7. Europe Europe and MENA Dissolving Wood Pulp Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Grade

- 7.1.1. Bleached Chemical Pulp (BCP)

- 7.1.2. Dissolving Wood Pulp (DWP)

- 7.1.3. Unbleached Kraft Pulp

- 7.1.4. Mechanical Pulp

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Printing and Writing

- 7.2.2. Newsprint

- 7.2.3. Tissue

- 7.2.4. Cartonboard

- 7.2.5. Containerboard

- 7.2.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Grade

- 8. Middle East and North Africa Europe and MENA Dissolving Wood Pulp Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Grade

- 8.1.1. Bleached Chemical Pulp (BCP)

- 8.1.2. Dissolving Wood Pulp (DWP)

- 8.1.3. Unbleached Kraft Pulp

- 8.1.4. Mechanical Pulp

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Printing and Writing

- 8.2.2. Newsprint

- 8.2.3. Tissue

- 8.2.4. Cartonboard

- 8.2.5. Containerboard

- 8.2.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Grade

- 9. Competitive Analysis

- 9.1. Company Profiles

- 9.1.1 Obeikan Paper Industries Co

- 9.1.1.1. Company Overview

- 9.1.1.2. Products

- 9.1.1.3. Company Financials

- 9.1.1.4. SWOT Analysis

- 9.1.2 Middle East Paper Company (MEPCO)

- 9.1.2.1. Company Overview

- 9.1.2.2. Products

- 9.1.2.3. Company Financials

- 9.1.2.4. SWOT Analysis

- 9.1.3 Stora Enso

- 9.1.3.1. Company Overview

- 9.1.3.2. Products

- 9.1.3.3. Company Financials

- 9.1.3.4. SWOT Analysis

- 9.1.4 Atrak Pulp and Paper Industries

- 9.1.4.1. Company Overview

- 9.1.4.2. Products

- 9.1.4.3. Company Financials

- 9.1.4.4. SWOT Analysis

- 9.1.5 UPM

- 9.1.5.1. Company Overview

- 9.1.5.2. Products

- 9.1.5.3. Company Financials

- 9.1.5.4. SWOT Analysis

- 9.1.6 Mondi PLC

- 9.1.6.1. Company Overview

- 9.1.6.2. Products

- 9.1.6.3. Company Financials

- 9.1.6.4. SWOT Analysis

- 9.1.7 Saudi Paper Manufacturing Co

- 9.1.7.1. Company Overview

- 9.1.7.2. Products

- 9.1.7.3. Company Financials

- 9.1.7.4. SWOT Analysis

- 9.1.8 Sappi Limited*List Not Exhaustive

- 9.1.8.1. Company Overview

- 9.1.8.2. Products

- 9.1.8.3. Company Financials

- 9.1.8.4. SWOT Analysis

- 9.1.9 SCA

- 9.1.9.1. Company Overview

- 9.1.9.2. Products

- 9.1.9.3. Company Financials

- 9.1.9.4. SWOT Analysis

- 9.1.10 Linter Pak Co

- 9.1.10.1. Company Overview

- 9.1.10.2. Products

- 9.1.10.3. Company Financials

- 9.1.10.4. SWOT Analysis

- 9.1.1 Obeikan Paper Industries Co

- 9.2. Market Entropy

- 9.2.1 Company's Key Areas Served

- 9.2.2 Recent Developments

- 9.3. Company Market Share Analysis 2025

- 9.3.1 Top 5 Companies Market Share Analysis

- 9.3.2 Top 3 Companies Market Share Analysis

- 9.4. List of Potential Customers

- 10. Research Methodology

List of Figures

- Figure 1: Europe and MENA Dissolving Wood Pulp Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Europe and MENA Dissolving Wood Pulp Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Grade 2020 & 2033

- Table 2: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Application 2020 & 2033

- Table 3: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Grade 2020 & 2033

- Table 5: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Application 2020 & 2033

- Table 6: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: France Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 12: Portugal Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 13: Netherlands Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Greece Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Austria Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Belgium Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 17: Switzerland Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Russia Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 19: Romania Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Grade 2020 & 2033

- Table 22: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Application 2020 & 2033

- Table 23: Europe and MENA Dissolving Wood Pulp Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: United Arab Emirates Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Saudi Arabia Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Iran Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Israel Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Jordan Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 29: Syria Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Bahrain Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 31: Kuwait Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Lebanon Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: Egypt Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: Tunisia Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: Morocco Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Algeria Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Rest of MENA Europe and MENA Dissolving Wood Pulp Industry Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe and MENA Dissolving Wood Pulp Industry?

The projected CAGR is approximately 2.9%.

2. Which companies are prominent players in the Europe and MENA Dissolving Wood Pulp Industry?

Key companies in the market include Obeikan Paper Industries Co, Middle East Paper Company (MEPCO), Stora Enso, Atrak Pulp and Paper Industries, UPM, Mondi PLC, Saudi Paper Manufacturing Co, Sappi Limited*List Not Exhaustive, SCA, Linter Pak Co.

3. What are the main segments of the Europe and MENA Dissolving Wood Pulp Industry?

The market segments include Grade, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 6090 million as of 2022.

5. What are some drivers contributing to market growth?

; Urbanization in the Country; Increased Foreign Direct Investments.

6. What are the notable trends driving market growth?

Bleached Chemical Pulp to Have Significant Impact on The Growth.

7. Are there any restraints impacting market growth?

; Reforms to Control the Use of Plastic Packaging.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe and MENA Dissolving Wood Pulp Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe and MENA Dissolving Wood Pulp Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe and MENA Dissolving Wood Pulp Industry?

To stay informed about further developments, trends, and reports in the Europe and MENA Dissolving Wood Pulp Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence