Key Insights

The Indian Metal Packaging Industry is set for substantial growth, projected to reach a market size of 141.7 billion by 2033. This expansion is driven by a Compound Annual Growth Rate (CAGR) of 3.9% from the base year 2025. Key growth drivers include rising consumer demand in the beverage and food sectors, where metal packaging offers superior shelf-life, durability, and brand appeal. Increasing urbanization and disposable incomes further fuel the consumption of packaged goods, directly benefiting the market. A growing preference for sustainable and recyclable packaging solutions also positions metal favorably against plastics. The Paint & Chemicals and Industrial sectors also contribute significantly to demand, propelled by manufacturing and infrastructure development.

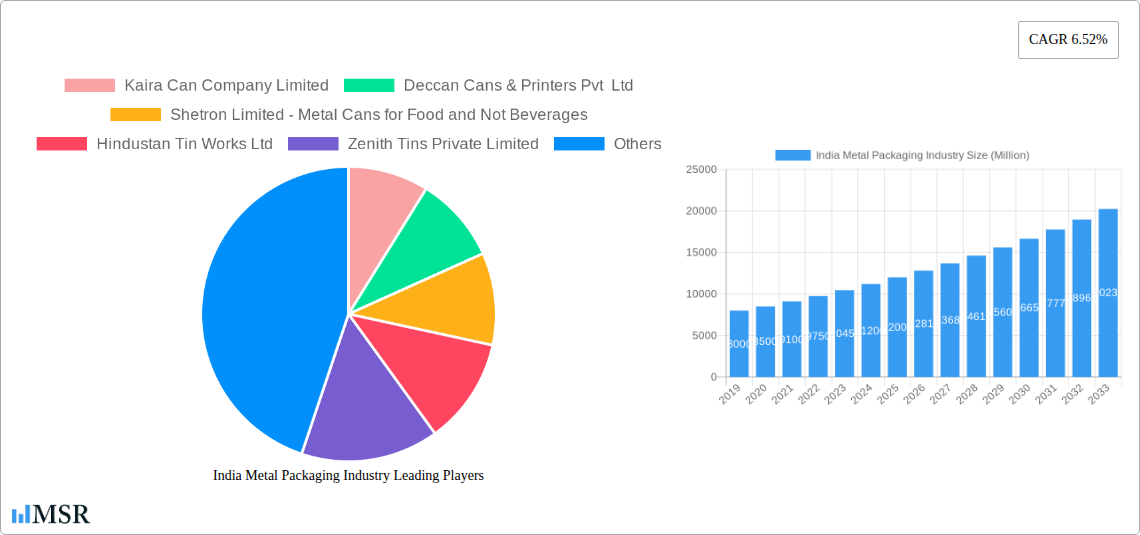

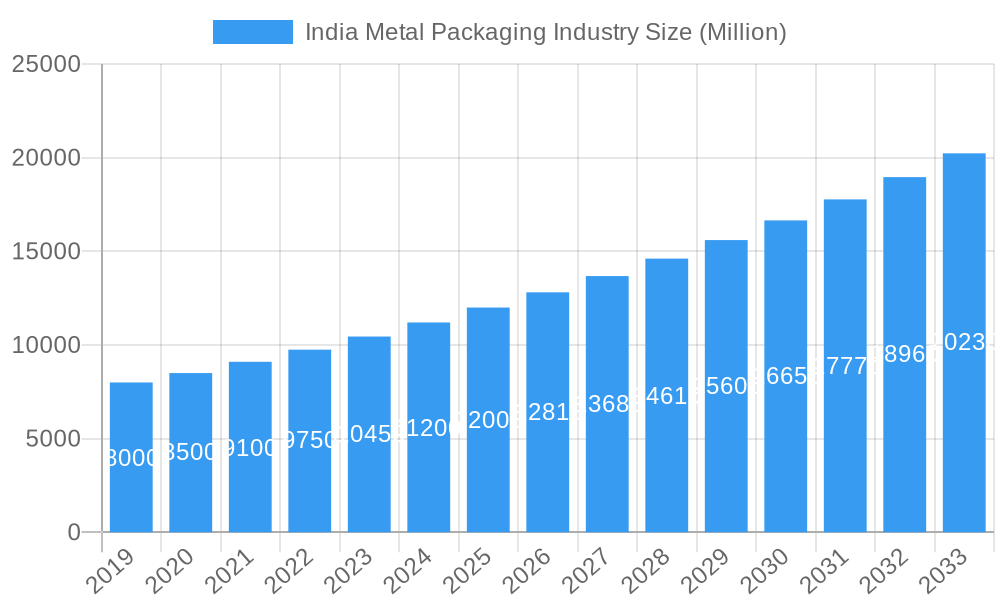

India Metal Packaging Industry Market Size (In Billion)

Market expansion is further supported by an evolving product landscape. While traditional cans (food, beverage, aerosol) remain dominant, demand for bulk containers, shipping barrels, and drums is increasing, reflecting a maturing industrial supply chain. Innovations in metal processing and coating technologies enhance functionality and aesthetics. However, the industry faces challenges such as raw material price volatility (aluminum and steel) and competition from alternative packaging materials. Strategic sourcing, technological advancements, and efficient production are crucial for sustained growth and market leadership.

India Metal Packaging Industry Company Market Share

India Metal Packaging Industry Report: Market Analysis, Trends, and Future Outlook (2019-2033)

Unlock critical insights into India's burgeoning metal packaging sector with this comprehensive report. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this analysis delves into market dynamics, key segments, product innovations, and the strategic roadmap for stakeholders. Discover growth drivers, challenges, and emerging opportunities within the Indian metal cans, steel packaging, and aluminum packaging markets, driven by robust demand from beverage, food, and industrial sectors.

India Metal Packaging Industry Market Concentration & Dynamics

The India metal packaging industry exhibits a moderate to high market concentration, with a few dominant players holding significant market share, particularly in the aluminum cans and steel cans for food segments. Innovation is a key differentiator, with companies focusing on lightweighting, enhanced barrier properties, and sustainable packaging solutions to meet evolving consumer and regulatory demands. The regulatory framework is progressively aligning with global standards for food safety and environmental impact, influencing material choices and manufacturing processes. Substitute products, such as flexible packaging and PET bottles, continue to pose a competitive challenge, necessitating continuous innovation in metal packaging performance and cost-effectiveness. End-user trends indicate a strong preference for convenience and sustainability, driving demand for resealable containers and recyclable metal packaging. Merger and acquisition (M&A) activities are sporadic but strategic, often aimed at expanding production capacity, integrating supply chains, or acquiring new technologies. The total M&A deal count historically stands at xx, signifying focused consolidation rather than widespread fragmentation.

India Metal Packaging Industry Industry Insights & Trends

The India metal packaging industry is poised for substantial growth, projected to reach an estimated market size of over INR 5,000 Million by 2025, with a projected Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period (2025–2033). This expansion is fueled by several key factors. Firstly, the rapidly growing Indian middle class and increasing disposable incomes are driving higher consumption of packaged goods, particularly in the beverage and food sectors, directly benefiting the demand for food cans and beverage cans. Secondly, technological advancements in manufacturing, such as improved coating technologies and enhanced can designs, are leading to more efficient and cost-effective production of high-quality metal packaging. Thirdly, a growing consumer awareness regarding the recyclability and premium feel of metal packaging, especially aluminum cans, is further boosting its adoption. The Paints and Chemicals sector also presents a significant demand for durable shipping barrels and drums and bulk containers, supported by industrial growth. The government's focus on 'Make in India' initiatives and infrastructure development further underpins the industry's upward trajectory. Evolving consumer behaviors, such as a preference for single-serving packs and on-the-go consumption, are also creating new opportunities for specialized metal packaging formats.

Key Markets & Segments Leading India Metal Packaging Industry

The beverage and food end-user verticals are unequivocally the dominant segments driving the India metal packaging industry. Within these, aluminum cans and steel cans are the primary material types.

Product Type Dominance:

- Cans: This category, encompassing food cans and beverage cans, holds the largest market share. The rising demand for carbonated soft drinks, juices, and processed foods directly translates into a significant need for these packaging formats. The increasing popularity of ready-to-drink beverages and convenient meal solutions further solidifies this segment's leadership.

- Aerosol Cans: While smaller than food and beverage cans, aerosol cans are experiencing steady growth, particularly driven by the personal care and home care sectors. Innovations in dispensing technology and product formulations are expanding their applications.

- Bulk Containers and Shipping Barrels and Drums: The industrial and paints and chemicals end-user verticals heavily rely on these for safe storage and transportation of goods. Infrastructure development and manufacturing output are key drivers for this segment.

- Caps and Closures: Essential for all packaging types, this segment's growth is intrinsically linked to the overall metal packaging market.

End-User Vertical Dominance:

- Beverage: This vertical is a primary growth engine, propelled by the expanding consumption of carbonated drinks, juices, and other packaged beverages.

- Food: The demand for processed foods, ready-to-eat meals, and preserved food items makes this another crucial segment.

- Paints and Chemicals: The need for robust and safe containment for these products ensures consistent demand for shipping barrels and drums and bulk containers.

The dominance of these segments is underpinned by factors such as:

- Economic Growth: A rising GDP and increasing consumer spending directly impact demand for packaged goods.

- Urbanization: Growing urban populations lead to higher consumption of convenience foods and beverages.

- Infrastructure Development: Expansion in manufacturing and logistics necessitates robust packaging solutions for industrial goods.

- Consumer Preferences: A growing preference for premium, recyclable, and aesthetically pleasing packaging favors metal.

India Metal Packaging Industry Product Developments

Recent product developments highlight the industry's focus on enhancing functionality and sustainability. Innovations include the introduction of lightweight aluminum cans for beverages, reducing material usage and transportation costs. Advancements in coating technology are improving product shelf-life and preventing contamination in food cans. For the industrial sector, the development of stronger and more corrosion-resistant shipping barrels and drums is crucial for hazardous material transport. The personal care sector is seeing a rise in sophisticated aerosol cans with improved valve systems for precise dispensing. The emphasis is on offering tailored packaging solutions that meet specific product requirements while adhering to environmental regulations.

Challenges in the India Metal Packaging Industry Market

The India metal packaging industry faces several challenges. Volatile raw material prices, particularly for aluminum and steel, can impact profitability and pricing strategies. Intense competition from substitute packaging materials like PET and flexible packaging necessitates continuous innovation and cost optimization. Stringent environmental regulations regarding waste management and recycling, while beneficial in the long run, require significant investment in new technologies and infrastructure. Supply chain disruptions, as witnessed in recent global events, can affect the availability and cost of raw materials and finished goods. The market share of metal packaging is currently estimated at xx%, indicating a significant opportunity to capture more share from substitutes.

Forces Driving India Metal Packaging Industry Growth

Several forces are propelling the growth of the India metal packaging industry. Increasing disposable incomes and a burgeoning middle class are boosting demand for packaged consumer goods, especially beverages and food. Growing consumer preference for recyclable and sustainable packaging options is a significant catalyst, with metal being a highly recyclable material. Technological advancements in can manufacturing are leading to lighter, stronger, and more cost-effective packaging. The government's focus on "Make in India" initiatives and infrastructure development is stimulating the industrial sector, thereby increasing demand for industrial packaging solutions. Furthermore, the shift towards convenience-oriented packaging for on-the-go consumption is also a key driver.

Challenges in the India Metal Packaging Industry Market

Long-term growth catalysts for the India metal packaging industry lie in continuous innovation and market expansion. Investment in advanced recycling technologies and infrastructure will solidify metal's sustainability credentials, addressing environmental concerns and appealing to eco-conscious consumers. Developing smart packaging solutions with embedded tracking or authentication features can enhance value for industrial clients. Strategic partnerships and collaborations with beverage and food manufacturers to develop bespoke packaging solutions will foster deeper integration. Exploring untapped segments, such as specialty foods and niche beverage markets, and expanding export capabilities will further diversify revenue streams and reduce reliance on domestic market fluctuations.

Emerging Opportunities in India Metal Packaging Industry

Emerging opportunities in the India metal packaging industry are manifold. The growing demand for ready-to-drink (RTD) beverages presents a significant opportunity for aluminum cans. The expanding e-commerce sector is creating a need for durable and protective shipping barrels and drums and bulk containers. Innovations in flexible metal packaging could offer new solutions for food products. Furthermore, the increasing focus on health and wellness products is creating opportunities for specialized packaging that maintains product integrity and freshness. The potential for reusable metal packaging systems and the adoption of Industry 4.0 technologies in manufacturing are also promising avenues for growth and efficiency.

Leading Players in the India Metal Packaging Industry Sector

- Kaira Can Company Limited

- Deccan Cans & Printers Pvt Ltd

- Shetron Limited - Metal Cans for Food and Not Beverages

- Hindustan Tin Works Ltd

- Zenith Tins Private Limited

- Hi-Can Industries Pvt Ltd

- Asian Aerosol Group

- Petrox Packaging (I) Pvt Ltd

- Ball India (Ball Corporation)

- Casablanca Industries Pvt Ltd - Only Aerosol Cans

Key Milestones in India Metal Packaging Industry Industry

- November 2022: Chennai-based The Lip Balm Company launched the Travel Minis from the LIPrepare collection. Available in 1 g squeeze tubes, it lasts up to 56 uses and is ideal for sensitive lips. The prepared group has four flavors: Apple Ko, Chocolate Ko, Peach Ko, and Strawberry Ko. This highlights innovation in niche product packaging.

- August 2022: Varun Beverages, a bottling company of PepsiCo's beverages, planned to invest about INR 1,200 crore (approximately USD 1.5 billion) to inflate its production capacity in India by 2023. Similarly, Coca-Cola bottlers in India were investing USD 1 billion to increase their beverage production capacity by 30-40% by March 2023. These raised production plans will significantly aid the growth of metal cans in carbonated and non-carbonated drinks during the forecast period.

Strategic Outlook for India Metal Packaging Industry Market

The strategic outlook for the India metal packaging industry is highly positive, driven by a confluence of economic growth, evolving consumer preferences, and technological advancements. Future growth will be accelerated by a continued focus on sustainability and circular economy principles, encouraging greater adoption of recycled materials and improved end-of-life management. Strategic opportunities lie in diversifying product portfolios to cater to emerging segments like health foods and specialized industrial chemicals. Investing in automation and digitalization within manufacturing facilities will enhance efficiency and product quality. Furthermore, fostering strong partnerships with key end-users and exploring export markets will be crucial for long-term expansion and market leadership. The industry is well-positioned to capitalize on India's demographic dividend and increasing demand for high-quality, sustainable packaging solutions.

India Metal Packaging Industry Segmentation

-

1. Materials Type

- 1.1. Aluminum

- 1.2. Steel

-

2. Product Type

-

2.1. Cans

- 2.1.1. Food Cans

- 2.1.2. Beverage Cans

- 2.1.3. Aerosol Cans

- 2.2. Bulk Containers

- 2.3. Shipping Barrels and Drums

- 2.4. Caps and Closures

- 2.5. Other Product Types

-

2.1. Cans

-

3. End-User Vertical

- 3.1. Beverage

- 3.2. Food

- 3.3. Paints and Chemicals

- 3.4. Industrial

- 3.5. Other End-users

India Metal Packaging Industry Segmentation By Geography

- 1. India

India Metal Packaging Industry Regional Market Share

Geographic Coverage of India Metal Packaging Industry

India Metal Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Materials Type

- 5.1.1. Aluminum

- 5.1.2. Steel

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Cans

- 5.2.1.1. Food Cans

- 5.2.1.2. Beverage Cans

- 5.2.1.3. Aerosol Cans

- 5.2.2. Bulk Containers

- 5.2.3. Shipping Barrels and Drums

- 5.2.4. Caps and Closures

- 5.2.5. Other Product Types

- 5.2.1. Cans

- 5.3. Market Analysis, Insights and Forecast - by End-User Vertical

- 5.3.1. Beverage

- 5.3.2. Food

- 5.3.3. Paints and Chemicals

- 5.3.4. Industrial

- 5.3.5. Other End-users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by Materials Type

- 6. India Metal Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Materials Type

- 6.1.1. Aluminum

- 6.1.2. Steel

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Cans

- 6.2.1.1. Food Cans

- 6.2.1.2. Beverage Cans

- 6.2.1.3. Aerosol Cans

- 6.2.2. Bulk Containers

- 6.2.3. Shipping Barrels and Drums

- 6.2.4. Caps and Closures

- 6.2.5. Other Product Types

- 6.2.1. Cans

- 6.3. Market Analysis, Insights and Forecast - by End-User Vertical

- 6.3.1. Beverage

- 6.3.2. Food

- 6.3.3. Paints and Chemicals

- 6.3.4. Industrial

- 6.3.5. Other End-users

- 6.1. Market Analysis, Insights and Forecast - by Materials Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Kaira Can Company Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Deccan Cans & Printers Pvt Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Shetron Limited - Metal Cans for Food and Not Beverages

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hindustan Tin Works Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Zenith Tins Private Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Hi-Can Industries Pvt Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Asian Aerosol Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Petrox Packaging (I) Pvt Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Ball India (Ball Corporation)*List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Casablanca Industries Pvt Ltd - Only Aerosol Cans

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Kaira Can Company Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Metal Packaging Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India Metal Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: India Metal Packaging Industry Revenue billion Forecast, by Materials Type 2020 & 2033

- Table 2: India Metal Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: India Metal Packaging Industry Revenue billion Forecast, by End-User Vertical 2020 & 2033

- Table 4: India Metal Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: India Metal Packaging Industry Revenue billion Forecast, by Materials Type 2020 & 2033

- Table 6: India Metal Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 7: India Metal Packaging Industry Revenue billion Forecast, by End-User Vertical 2020 & 2033

- Table 8: India Metal Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Metal Packaging Industry?

The projected CAGR is approximately 3.9%.

2. Which companies are prominent players in the India Metal Packaging Industry?

Key companies in the market include Kaira Can Company Limited, Deccan Cans & Printers Pvt Ltd, Shetron Limited - Metal Cans for Food and Not Beverages, Hindustan Tin Works Ltd, Zenith Tins Private Limited, Hi-Can Industries Pvt Ltd, Asian Aerosol Group, Petrox Packaging (I) Pvt Ltd, Ball India (Ball Corporation)*List Not Exhaustive, Casablanca Industries Pvt Ltd - Only Aerosol Cans.

3. What are the main segments of the India Metal Packaging Industry?

The market segments include Materials Type, Product Type, End-User Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 141.7 billion as of 2022.

5. What are some drivers contributing to market growth?

High Recyclability Rates of Metal Packaging; High Recyclability of Metal Cans.

6. What are the notable trends driving market growth?

Cans are Expected to Hold Significant Share.

7. Are there any restraints impacting market growth?

Increasing Operational Costs.

8. Can you provide examples of recent developments in the market?

November 2022: Chennai-based, The Lip Balm Company, known for its unique products, whether a concept, vegan, innovative packaging, or 100% plant-based tints, launched the Travel Minis from the LIPrepare collection. Available in 1 g squeeze tubes, it lasts up to 56 uses and is ideal for sensitive lips. The prepared group has four flavors Apple Ko, Chocolate Ko, Peach Ko, and Strawberry Ko.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Metal Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Metal Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Metal Packaging Industry?

To stay informed about further developments, trends, and reports in the India Metal Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence