Key Insights

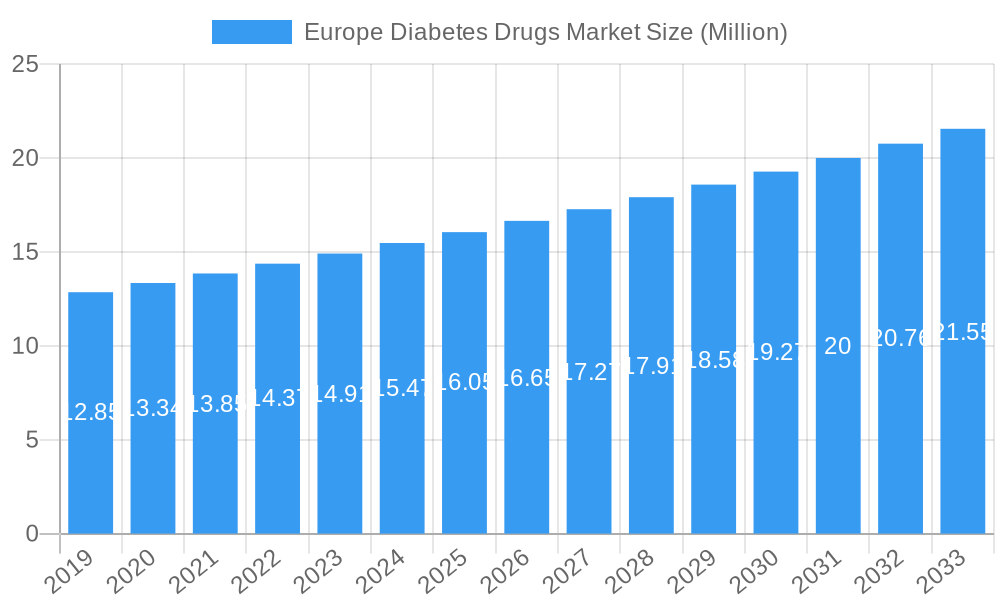

The European diabetes drugs market is poised for robust growth, projected to reach approximately USD 16.43 billion by 2025, with a compound annual growth rate (CAGR) of 4.25% through 2033. This expansion is primarily fueled by the increasing prevalence of diabetes across the continent, driven by factors such as aging populations, sedentary lifestyles, and rising obesity rates. Key market drivers include a growing awareness of diabetes management, advancements in therapeutic research and development leading to more effective and targeted treatments, and supportive government initiatives aimed at improving chronic disease care. The market's dynamism is further evidenced by significant investments in novel drug formulations and delivery systems.

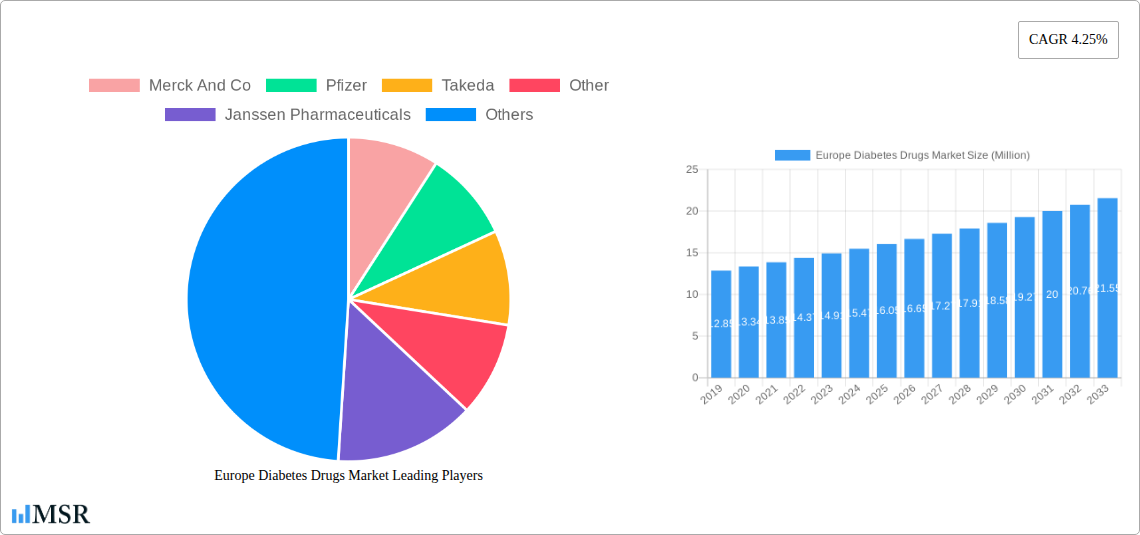

Europe Diabetes Drugs Market Market Size (In Million)

The market is segmented into various product types, with Insulins, Oral Anti-diabetic Drugs, and Non-Insulin Injectable Drugs forming the core offerings. The application segments are primarily Type 1 and Type 2 Diabetes, with Type 2 Diabetes accounting for the larger share due to its higher incidence. Emerging trends include the rise of GLP-1 receptor agonists and SGLT2 inhibitors, known for their cardiovascular and renal benefits, and a greater focus on personalized medicine approaches. Despite the promising growth trajectory, the market faces restraints such as high drug development costs, stringent regulatory pathways for new drug approvals, and potential pricing pressures from healthcare systems seeking to manage expenditure. Leading companies like Novo Nordisk A/S, Sanofi Aventis, and Eli Lilly are actively shaping the market through innovation and strategic partnerships.

Europe Diabetes Drugs Market Company Market Share

Europe Diabetes Drugs Market: Comprehensive Analysis & Growth Forecast (2019-2033)

Report Description:

This in-depth Europe Diabetes Drugs Market report provides an exhaustive analysis of the European diabetes therapeutics market, covering Type 1 Diabetes and Type 2 Diabetes treatment landscapes from 2019 to 2033. With a base year of 2025, the report offers precise market size estimations and a robust forecast period of 2025–2033, driven by critical insights into oral anti-diabetic drugs, insulins, non-insulin injectable drugs, and combination drugs. Uncover key market dynamics, emerging trends in diabetes drug development, and the competitive strategies of leading pharmaceutical giants. This report is an essential resource for pharmaceutical companies, biotechnology firms, healthcare providers, investors, and regulatory bodies seeking to understand and capitalize on the evolving European diabetes treatment market.

Europe Diabetes Drugs Market Market Concentration & Dynamics

The Europe Diabetes Drugs Market exhibits a moderate to high market concentration, characterized by the significant presence of established multinational pharmaceutical corporations. Key players dominate market share through extensive research and development pipelines, strategic partnerships, and strong brand recognition. The innovation ecosystem is vibrant, with continuous advancements in drug discovery, particularly in novel diabetes therapies and improved delivery systems for insulins and injectable anti-diabetic drugs. Regulatory frameworks in the EU, while stringent, foster innovation by providing pathways for the approval of groundbreaking treatments. However, the presence of substitute products, including lifestyle interventions and medical devices, exerts competitive pressure. End-user trends are increasingly focused on patient-centric care, personalized medicine, and therapies that offer improved glycemic control with reduced side effects and comorbidities, such as heart failure management, as evidenced by recent approvals for SGLT2 inhibitors. Merger and acquisition (M&A) activities, while not overtly dominant, play a role in consolidating market presence and acquiring promising late-stage pipeline assets, though specific M&A deal counts are not publicly available for this detailed segment. The market share distribution among key players is dynamic, with leaders like Novo Nordisk A/S consistently holding a substantial portion, particularly in the insulin and GLP-1 receptor agonist segments.

Europe Diabetes Drugs Market Industry Insights & Trends

The Europe Diabetes Drugs Market is poised for significant growth, driven by a confluence of factors. The market size is projected to reach approximately $XX Billion by 2033, with a Compound Annual Growth Rate (CAGR) of around XX% during the forecast period of 2025–2033. A primary growth driver is the increasing prevalence of diabetes across Europe, attributed to aging populations, sedentary lifestyles, and rising obesity rates, leading to a larger patient pool requiring therapeutic interventions. Technological disruptions are profoundly impacting the market. The development and widespread adoption of oral anti-diabetic drugs, particularly SGLT2 inhibitors and DPP-4 inhibitors, have revolutionized Type 2 Diabetes management by offering superior glycemic control and significant cardiovascular and renal benefits. Similarly, advancements in insulin formulations and delivery devices, including smart pens and continuous glucose monitoring (CGM) systems, are enhancing patient adherence and treatment efficacy. Evolving consumer behaviors are also shaping the market. Patients are becoming more informed and actively involved in their treatment decisions, seeking therapies that not only manage blood glucose but also address comorbidities and improve overall quality of life. This is evident in the growing demand for combination drugs that offer simplified dosing regimens and synergistic therapeutic effects. Furthermore, the pharmaceutical industry is witnessing a shift towards personalized medicine, with a greater emphasis on pharmacogenomics and tailoring treatments to individual patient profiles. The successful expansion of indications for drugs like Forxiga to include various stages of heart failure underscores the trend of diabetes medications addressing broader cardiovascular and renal health concerns, thereby expanding their market potential and driving revenue growth. The sustained investment in research and development by key players, focusing on novel drug targets and mechanisms of action, will continue to fuel innovation and market expansion.

Key Markets & Segments Leading Europe Diabetes Drugs Market

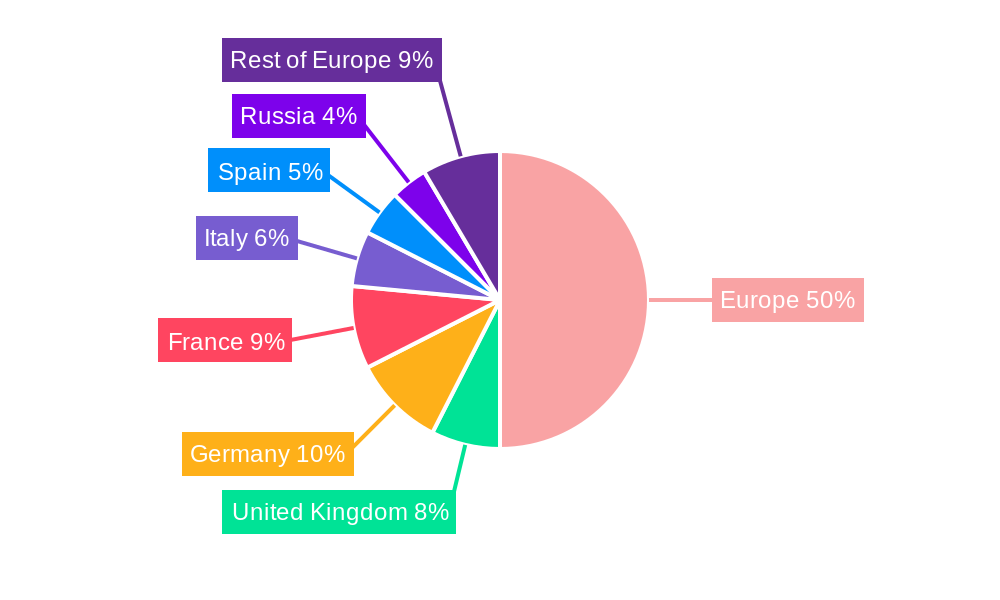

The Europe Diabetes Drugs Market is predominantly led by Type 2 Diabetes applications, accounting for the largest share due to its significantly higher prevalence across the continent. Within product types, Oral Anti-diabetic Drugs command a substantial market share, driven by their convenience, efficacy, and broad applicability in managing Type 2 Diabetes. Germany, the UK, France, Italy, and Spain represent the key markets within Europe, exhibiting robust healthcare infrastructure, high disposable incomes, and a proactive approach to chronic disease management.

Dominant Segment: Type 2 Diabetes Applications

- Economic Growth: A strong European economy translates to increased healthcare spending and accessibility to advanced diabetes treatments for a larger population.

- Lifestyle Factors: Rising obesity rates and sedentary lifestyles in these major economies contribute to a higher incidence of Type 2 Diabetes, creating sustained demand for therapeutics.

- Healthcare Infrastructure: Advanced healthcare systems in these countries ensure early diagnosis, regular monitoring, and effective prescription of diabetes medications.

Leading Product Type: Oral Anti-diabetic Drugs

- Patient Preference: Oral formulations are generally preferred by patients over injectables due to ease of administration and greater convenience in daily routines.

- Therapeutic Advancements: Continuous innovation in classes like SGLT2 inhibitors and DPP-4 inhibitors has led to drugs with improved efficacy and a favorable safety profile, making them first-line or second-line treatments for many Type 2 Diabetes patients.

- Cost-Effectiveness: While newer biologics are expensive, well-established oral anti-diabetic drugs often offer a more cost-effective solution for managing large patient populations.

Emerging Trends in Other Segments:

- Insulins: Despite the rise of oral and injectable non-insulin therapies, insulins remain crucial for advanced Type 2 Diabetes management and are the cornerstone of Type 1 Diabetes treatment. The development of biosimilar insulins is also expanding access and affordability.

- Non-Insulin Injectable Drugs: This segment, particularly GLP-1 receptor agonists, is experiencing rapid growth driven by their significant weight loss benefits and cardiovascular protective effects, making them increasingly popular for managing complex Type 2 Diabetes cases.

- Combination Drugs: The convenience and synergistic therapeutic benefits of fixed-dose combination drugs are gaining traction, simplifying treatment regimens and improving patient adherence.

Europe Diabetes Drugs Market Product Developments

Recent product developments in the Europe Diabetes Drugs Market highlight a strategic focus on addressing unmet needs and expanding therapeutic utility. The European Union's approval of Forxiga (dapagliflozin) in February 2023 to cover patients across the full spectrum of left ventricular ejection fraction (LVEF) for heart failure (HF) demonstrates the growing recognition of SGLT2 inhibitors' benefits beyond glycemic control, extending their market relevance to cardiovascular disease management. Similarly, in March 2022, Eli Lilly and Boehringer Ingelheim secured EU approval for Jardiance (empagliflozin) for heart failure treatment, further solidifying the role of SGLT2 inhibitors in managing cardiometabolic conditions. These advancements underscore a trend towards developing multi-benefit therapies that target diabetes and its associated comorbidities, offering a competitive edge and expanding the addressable market for these innovative drugs.

Challenges in the Europe Diabetes Drugs Market Market

The Europe Diabetes Drugs Market faces several challenges that impact its growth trajectory. Regulatory hurdles remain a significant barrier, with stringent approval processes for new drugs and complex reimbursement policies across different EU member states. Supply chain disruptions, exacerbated by geopolitical factors and global health crises, can affect the availability and cost of raw materials and finished products. Intense competition from both branded and generic manufacturers, alongside the increasing availability of biosimilar insulins, puts pressure on pricing and market share. Furthermore, patient adherence to complex treatment regimens, particularly for injectable therapies, remains a persistent challenge that limits the full realization of therapeutic benefits and market potential.

Forces Driving Europe Diabetes Drugs Market Growth

Several key forces are propelling the growth of the Europe Diabetes Drugs Market. Technologically, continuous innovation in drug discovery has led to the development of more effective and safer oral anti-diabetic drugs and non-insulin injectable drugs, such as GLP-1 receptor agonists and SGLT2 inhibitors, which offer added benefits like weight loss and cardiovascular protection. Economically, rising healthcare expenditures across Europe and the increasing affordability of treatments, including the growing presence of biosimilar insulins, are expanding market access. Regulatory factors, while stringent, have also been supportive of innovative treatments that demonstrate clear clinical advantages and address unmet medical needs, as seen with the expanded indications for SGLT2 inhibitors in heart failure. The growing awareness and diagnosis rates of diabetes further contribute to a larger patient pool seeking effective therapeutic solutions.

Challenges in the Europe Diabetes Drugs Market Market

The Europe Diabetes Drugs Market is poised for long-term growth, driven by sustained innovation and strategic market expansions. Continued investment in research and development by leading pharmaceutical companies is focused on novel drug targets and mechanisms of action, promising breakthrough treatments for complex diabetes management. Strategic partnerships and collaborations are facilitating faster drug development and market penetration, while geographical market expansions into emerging European economies with growing diabetes prevalence offer significant untapped potential. The increasing emphasis on value-based healthcare and the development of drugs that demonstrate comprehensive patient outcomes, including addressing comorbidities, will further accelerate market adoption and revenue growth.

Emerging Opportunities in Europe Diabetes Drugs Market

Emerging opportunities in the Europe Diabetes Drugs Market are abundant and multifaceted. The burgeoning field of personalized medicine, leveraging genetic profiling and advanced diagnostics, presents a significant opportunity to tailor diabetes treatments to individual patient needs, enhancing efficacy and reducing adverse events. The growing demand for digital health solutions, including remote patient monitoring and AI-powered therapeutic management platforms, offers avenues for improved patient engagement and better disease control. Furthermore, the expanding indication for diabetes drugs to manage associated cardiovascular and renal diseases creates substantial new market segments. Exploring underserved patient populations and developing innovative delivery mechanisms for existing and new therapies also represent key opportunities for market players to differentiate themselves and capture market share.

Leading Players in the Europe Diabetes Drugs Market Sector

- Merck And Co

- Pfizer

- Takeda

- Janssen Pharmaceuticals

- Eli Lilly

- Novartis

- AstraZeneca

- Sanofi Aventis

- Bristol Myers Squibb

- Novo Nordisk A/S

- Boehringer Ingelheim

- Astellas

Key Milestones in Europe Diabetes Drugs Market Industry

- February 2023: Forxiga (dapagliflozin) received European Union approval to extend its indication for heart failure (HF) with reduced ejection fraction (HFrEF) to encompass patients across the full spectrum of left ventricular ejection fraction (LVEF), including HF with mildly reduced and preserved ejection fraction (HFmrEF, HFpEF). This development significantly expands the market reach of SGLT2 inhibitors beyond glycemic control, positioning them as key players in cardiovascular and renal disease management.

- March 2022: Eli Lilly and Boehringer Ingelheim obtained European Union approval for Jardiance (empagliflozin) as a treatment for heart failure. This followed a prior label expansion for Jardiance in the US for heart failure treatment, underscoring the growing clinical and market significance of SGLT2 inhibitors in managing cardiometabolic conditions.

Strategic Outlook for Europe Diabetes Drugs Market Market

The strategic outlook for the Europe Diabetes Drugs Market is highly positive, driven by sustained innovation and a growing understanding of diabetes as a complex cardiometabolic disease. Key growth accelerators include the continued development of next-generation oral anti-diabetic drugs and non-insulin injectable drugs with enhanced efficacy, improved safety profiles, and additional benefits like weight management and organ protection. Strategic partnerships and collaborations between pharmaceutical companies, research institutions, and technology providers will be crucial for accelerating drug development and market access. Furthermore, expanding the therapeutic scope of existing drugs to encompass a broader range of diabetes-related comorbidities, such as cardiovascular and renal diseases, presents a significant opportunity for market players to solidify their positions and drive future growth in this dynamic and evolving sector.

Europe Diabetes Drugs Market Segmentation

-

1. Product Type

- 1.1. Insulins

- 1.2. Oral Anti-diabetic Drugs

- 1.3. Non-Insulin Injectable Drugs

- 1.4. Combination Drugs

-

2. Application

- 2.1. Type 1 Diabetes

- 2.2. Type 2 Diabetes

Europe Diabetes Drugs Market Segmentation By Geography

- 1. United Kingdom

- 2. Germany

- 3. Italy

- 4. Spain

- 5. France

- 6. Russia

- 7. Rest of Europe

Europe Diabetes Drugs Market Regional Market Share

Geographic Coverage of Europe Diabetes Drugs Market

Europe Diabetes Drugs Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Insulins

- 5.1.2. Oral Anti-diabetic Drugs

- 5.1.3. Non-Insulin Injectable Drugs

- 5.1.4. Combination Drugs

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Type 1 Diabetes

- 5.2.2. Type 2 Diabetes

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.3.2. Germany

- 5.3.3. Italy

- 5.3.4. Spain

- 5.3.5. France

- 5.3.6. Russia

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Insulins

- 6.1.2. Oral Anti-diabetic Drugs

- 6.1.3. Non-Insulin Injectable Drugs

- 6.1.4. Combination Drugs

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Type 1 Diabetes

- 6.2.2. Type 2 Diabetes

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. United Kingdom Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Insulins

- 7.1.2. Oral Anti-diabetic Drugs

- 7.1.3. Non-Insulin Injectable Drugs

- 7.1.4. Combination Drugs

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Type 1 Diabetes

- 7.2.2. Type 2 Diabetes

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Germany Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Insulins

- 8.1.2. Oral Anti-diabetic Drugs

- 8.1.3. Non-Insulin Injectable Drugs

- 8.1.4. Combination Drugs

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Type 1 Diabetes

- 8.2.2. Type 2 Diabetes

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Italy Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Insulins

- 9.1.2. Oral Anti-diabetic Drugs

- 9.1.3. Non-Insulin Injectable Drugs

- 9.1.4. Combination Drugs

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Type 1 Diabetes

- 9.2.2. Type 2 Diabetes

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Spain Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Insulins

- 10.1.2. Oral Anti-diabetic Drugs

- 10.1.3. Non-Insulin Injectable Drugs

- 10.1.4. Combination Drugs

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Type 1 Diabetes

- 10.2.2. Type 2 Diabetes

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. France Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Insulins

- 11.1.2. Oral Anti-diabetic Drugs

- 11.1.3. Non-Insulin Injectable Drugs

- 11.1.4. Combination Drugs

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Type 1 Diabetes

- 11.2.2. Type 2 Diabetes

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Russia Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Insulins

- 12.1.2. Oral Anti-diabetic Drugs

- 12.1.3. Non-Insulin Injectable Drugs

- 12.1.4. Combination Drugs

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Type 1 Diabetes

- 12.2.2. Type 2 Diabetes

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Rest of Europe Europe Diabetes Drugs Market Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 13.1.1. Insulins

- 13.1.2. Oral Anti-diabetic Drugs

- 13.1.3. Non-Insulin Injectable Drugs

- 13.1.4. Combination Drugs

- 13.2. Market Analysis, Insights and Forecast - by Application

- 13.2.1. Type 1 Diabetes

- 13.2.2. Type 2 Diabetes

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Merck And Co

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 Pfizer

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Takeda

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Other

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Janssen Pharmaceuticals

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Eli Lilly

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Novartis

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 AstraZeneca

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Sanofi Aventis

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 Bristol Myers Squibb

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 Novo Nordisk A/S

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 Boehringer Ingelheim

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.13 Astellas

- 14.1.13.1. Company Overview

- 14.1.13.2. Products

- 14.1.13.3. Company Financials

- 14.1.13.4. SWOT Analysis

- 14.1.14 Novo Nordisk A/S

- 14.1.14.1. Company Overview

- 14.1.14.2. Products

- 14.1.14.3. Company Financials

- 14.1.14.4. SWOT Analysis

- 14.1.1 Merck And Co

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Europe Diabetes Drugs Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Diabetes Drugs Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 3: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Europe Diabetes Drugs Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Diabetes Drugs Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 9: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 11: Europe Diabetes Drugs Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Europe Diabetes Drugs Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 14: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 15: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 17: Europe Diabetes Drugs Market Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Europe Diabetes Drugs Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 20: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 21: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 22: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 23: Europe Diabetes Drugs Market Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Europe Diabetes Drugs Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 26: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 27: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Europe Diabetes Drugs Market Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Europe Diabetes Drugs Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 32: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 33: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 35: Europe Diabetes Drugs Market Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Europe Diabetes Drugs Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 37: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 38: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 39: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 41: Europe Diabetes Drugs Market Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Europe Diabetes Drugs Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: Europe Diabetes Drugs Market Revenue Million Forecast, by Product Type 2020 & 2033

- Table 44: Europe Diabetes Drugs Market Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 45: Europe Diabetes Drugs Market Revenue Million Forecast, by Application 2020 & 2033

- Table 46: Europe Diabetes Drugs Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 47: Europe Diabetes Drugs Market Revenue Million Forecast, by Country 2020 & 2033

- Table 48: Europe Diabetes Drugs Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Diabetes Drugs Market?

The projected CAGR is approximately 4.25%.

2. Which companies are prominent players in the Europe Diabetes Drugs Market?

Key companies in the market include Merck And Co, Pfizer, Takeda, Other, Janssen Pharmaceuticals, Eli Lilly, Novartis, AstraZeneca, Sanofi Aventis, Bristol Myers Squibb, Novo Nordisk A/S, Boehringer Ingelheim, Astellas, Novo Nordisk A/S.

3. What are the main segments of the Europe Diabetes Drugs Market?

The market segments include Product Type , Application .

4. Can you provide details about the market size?

The market size is estimated to be USD 16.43 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Prevalence of Short Bowel Syndrome and GI disorders such as volvulus. Inflammatory bowel disease (IBD). Crohn's disease (CD) etc.; Rising Efforts in the Launch of Effective Treatments and Awareness Programs by Non-Profit Organizations.

6. What are the notable trends driving market growth?

The Oral anti-diabetic drugs segment held the highest market share in the Europe Diabetes Drugs Market in the current year.

7. Are there any restraints impacting market growth?

Lack of Availability of the Approved Drugs in Developing Countries; Lethal Adverse Complications like Colonic Cancer. Polyps along with Common Side Effects Associated with the Medication.

8. Can you provide examples of recent developments in the market?

Feburary 2023: Forxiga (dapagliflozin) has been approved in the European Union to extend the indication for heart failure (HF) with reduced ejection fraction (HFrEF) to cover patients across the full spectrum of left ventricular ejection fraction (LVEF), including HF with mildly reduced and preserved ejection fraction (HFmrEF, HFpEF).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Diabetes Drugs Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Diabetes Drugs Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Diabetes Drugs Market?

To stay informed about further developments, trends, and reports in the Europe Diabetes Drugs Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence