Key Insights

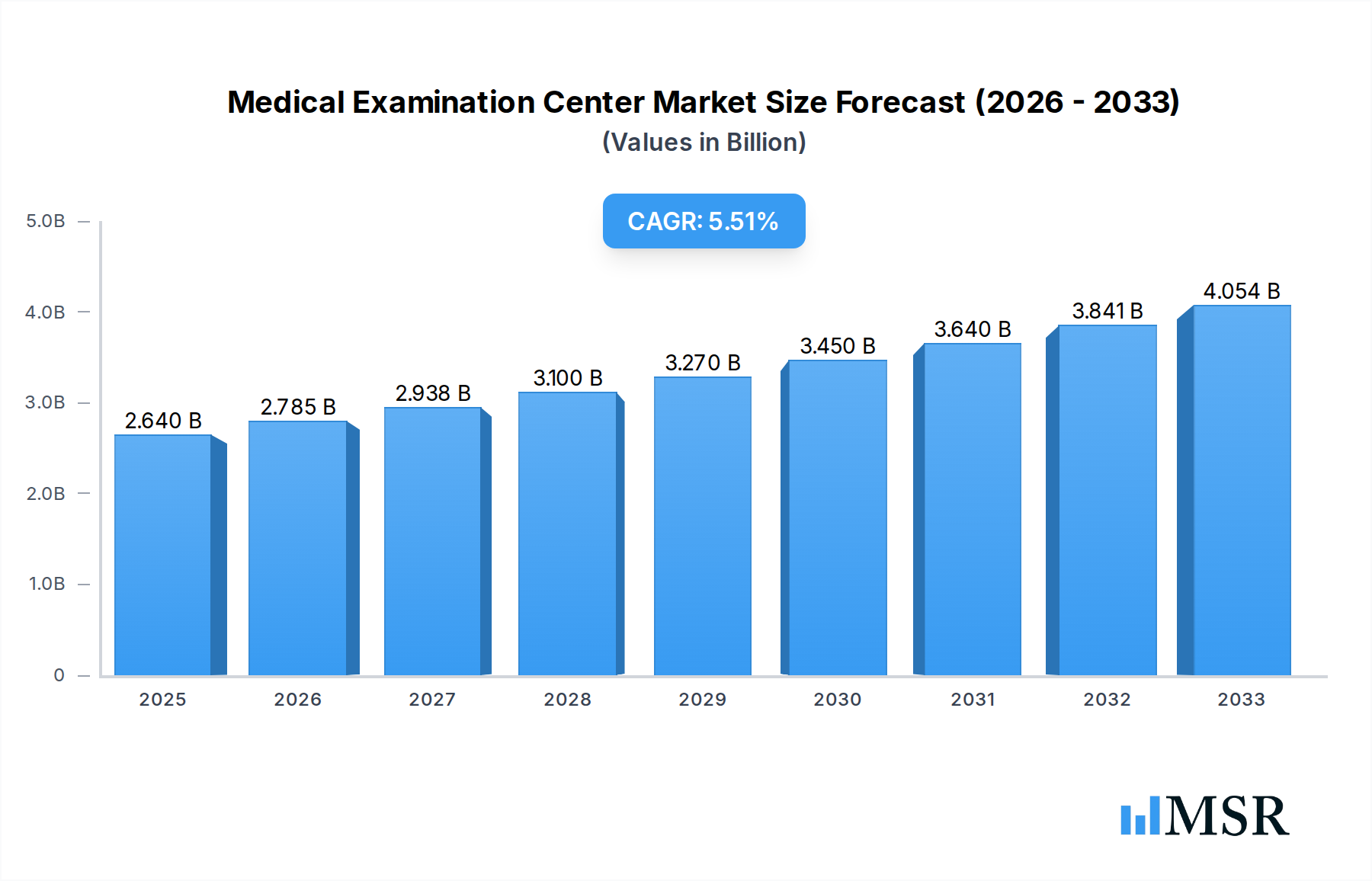

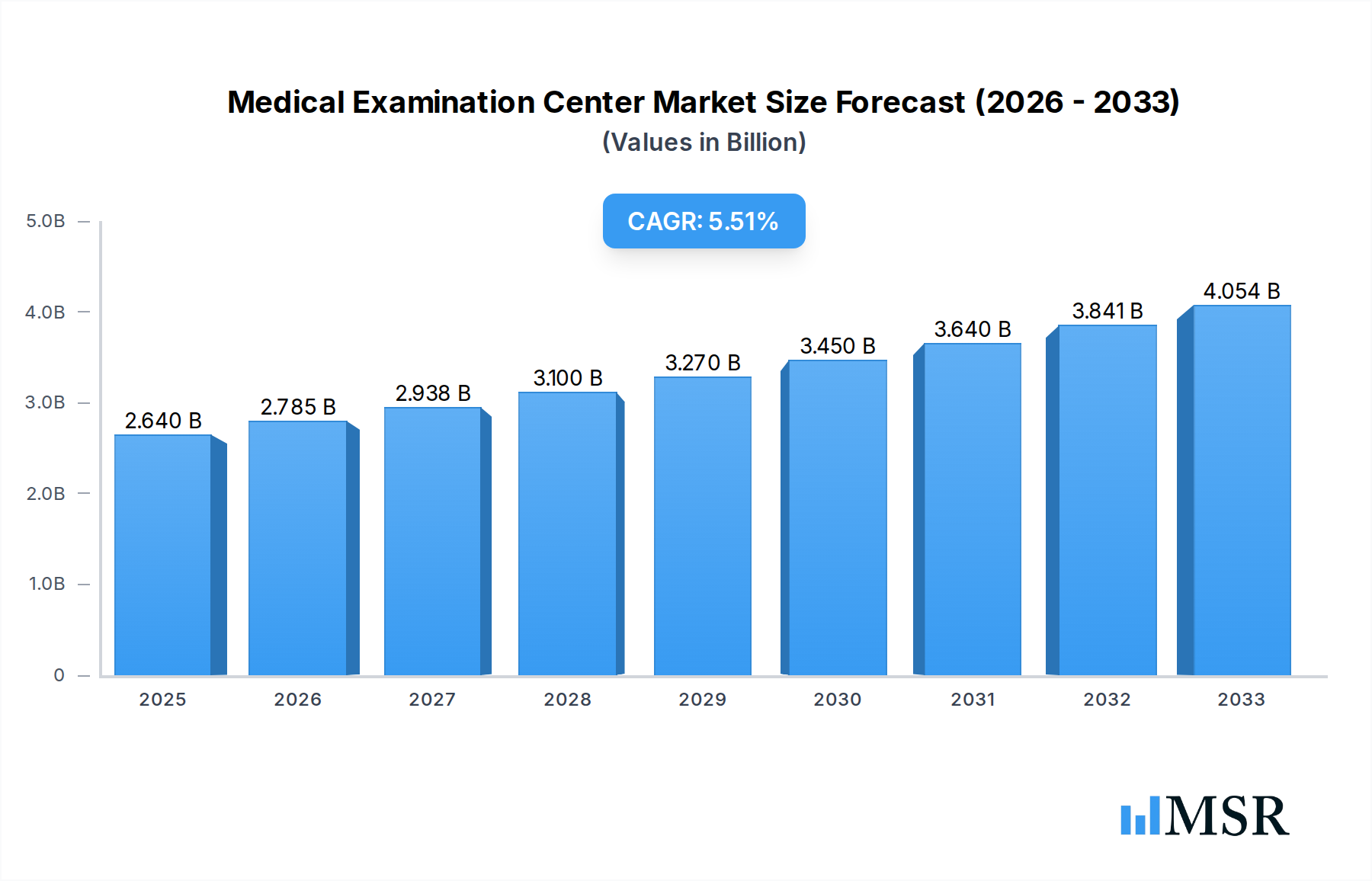

The global Medical Examination Center market is poised for robust growth, projected to reach $2.64 billion in 2025. Driven by an increasing emphasis on preventive healthcare and early disease detection, the market is expected to expand at a Compound Annual Growth Rate (CAGR) of 5.5% from 2025 to 2033. This upward trajectory is fueled by a confluence of factors including rising disposable incomes, growing awareness among individuals about the importance of regular health check-ups, and an aging global population that necessitates more frequent medical evaluations. Furthermore, advancements in diagnostic technologies and the expansion of healthcare infrastructure, particularly in emerging economies, are contributing significantly to market expansion. The segment for comprehensive physical examinations is likely to witness accelerated adoption as individuals seek a holistic understanding of their health status.

Medical Examination Center Market Size (In Billion)

The market dynamics are further shaped by key trends such as the integration of digital health solutions, offering more personalized and accessible examination experiences, and the growing demand for specialized health screening packages catering to specific demographics and health concerns. While the market enjoys strong growth, certain restraints might include the high cost associated with advanced diagnostic equipment and the availability of skilled healthcare professionals in certain regions. Key players like Kaiser Permanente, Bupa, Health 100, and Mayo Clinic are actively investing in expanding their service offerings and geographical reach to capitalize on these opportunities. The market is segmented into enterprise and individual applications, with routine and comprehensive physical examinations forming the core service types, indicating a broad spectrum of demand across various user groups and needs.

Medical Examination Center Company Market Share

Medical Examination Center Market: Comprehensive Analysis and Future Outlook (2019–2033)

This in-depth report provides a definitive analysis of the global Medical Examination Center Market, offering a granular view of its current landscape and projected trajectory. Covering the historical period of 2019–2024, the base year of 2025, and a comprehensive forecast period extending to 2033, this research is an indispensable resource for industry stakeholders, including healthcare providers, medical diagnostic companies, investors, and policy makers. We dissect market dynamics, identify key growth drivers, analyze emerging trends, and highlight strategic opportunities within the healthcare services and preventive medicine sectors. Our analysis includes an extensive overview of market concentration, technological innovations, regulatory environments, and competitive strategies.

Medical Examination Center Market Concentration & Dynamics

The Medical Examination Center Market exhibits a moderate to high level of concentration, with several dominant global players vying for market share. Key players like Kaiser Permanente, Bupa, and Mayo Clinic have established extensive networks and brand recognition, contributing to their significant market share, estimated to be in the billions. The innovation ecosystem is characterized by continuous investment in advanced diagnostic technologies and the integration of digital health solutions. Regulatory frameworks, while varying across regions, generally focus on patient safety, data privacy, and quality standards, influencing operational strategies. Substitute products, such as self-diagnostic kits and telehealth consultations for initial assessments, are emerging but do not fully replace the need for comprehensive medical examinations. End-user trends indicate a growing demand for personalized health assessments and preventive care, particularly among aging populations and health-conscious individuals. Merger and acquisition (M&A) activities are moderately prevalent, with approximately 50–75 deals anticipated annually, primarily aimed at expanding geographical reach, acquiring technological capabilities, or consolidating service offerings.

Medical Examination Center Industry Insights & Trends

The Medical Examination Center Market is experiencing robust growth, driven by an increasing awareness of preventive healthcare and the escalating burden of chronic diseases. The global market size is projected to reach USD 1,500 billion by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period of 2025–2033. Technological disruptions are at the forefront of this evolution, with advancements in AI-powered diagnostics, wearable health trackers, and advanced imaging techniques enhancing the accuracy and efficiency of medical examinations. These innovations enable earlier disease detection and more personalized treatment plans. Evolving consumer behaviors are also shaping the market, with individuals increasingly seeking proactive health management solutions. There is a palpable shift towards comprehensive physical examinations that go beyond basic screenings, offering detailed insights into an individual's overall health status and risk factors. The integration of telemedicine for follow-ups and preliminary consultations further streamlines the patient journey. The demand for routine physical examination and comprehensive physical examination services remains high, catering to both individual wellness goals and employer-mandated health checks.

Key Markets & Segments Leading Medical Examination Center

The Enterprise segment, encompassing corporate wellness programs and employee health screenings, is a dominant force in the Medical Examination Center Market. This dominance is propelled by several key drivers:

- Economic Growth: Growing economies globally translate to increased corporate profitability and a greater emphasis on employee well-being, leading to higher investment in health benefits.

- Healthcare Cost Management: Employers recognize that investing in preventive care reduces long-term healthcare costs associated with chronic illnesses and lost productivity.

- Regulatory Compliance: Many jurisdictions mandate certain health checks for employees, further boosting demand.

The Individuals segment also represents a significant market share, driven by increasing health consciousness, aging demographics, and a desire for personalized health insights. Routine and comprehensive physical examinations are crucial for early disease detection and management.

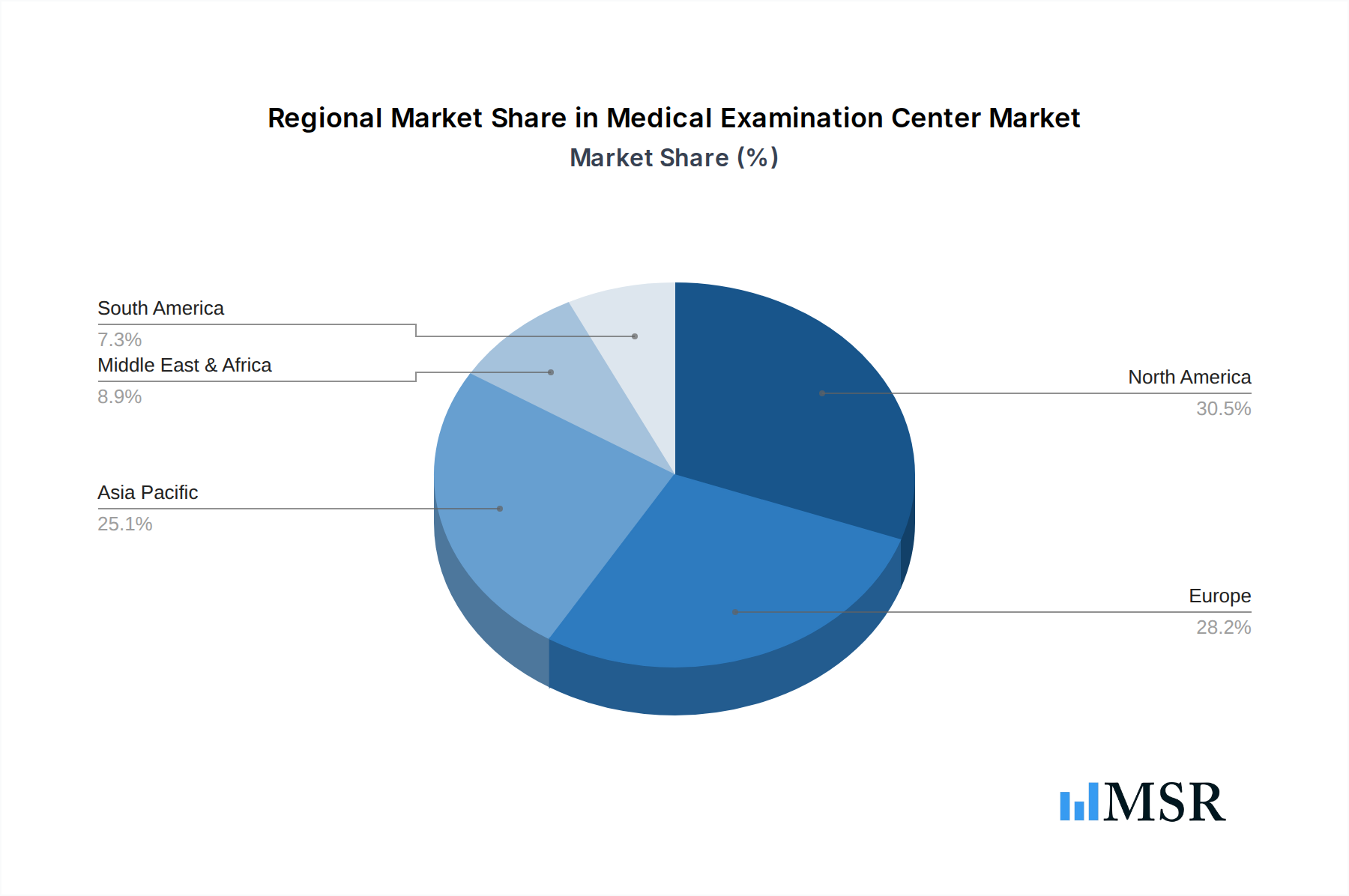

Geographically, North America and Europe currently lead the market due to well-established healthcare infrastructure, higher disposable incomes, and strong awareness of preventive health. However, the Asia-Pacific region is emerging as a high-growth market, fueled by rapid economic development, a growing middle class, and increasing penetration of private healthcare facilities. Countries like China and India, with their large populations and rising health expenditures, are becoming pivotal. The demand for routine physical examination is widespread across all demographics, while comprehensive physical examination is gaining traction among higher-income groups and individuals with known health concerns or family histories of disease.

Medical Examination Center Product Developments

Product developments in the Medical Examination Center Market are characterized by the integration of cutting-edge technologies. AI-powered diagnostic tools are revolutionizing image analysis and anomaly detection, offering unprecedented accuracy in identifying potential health issues. Advanced genetic testing and biomarker analysis are enabling highly personalized risk assessments and preventive strategies. The development of integrated digital platforms allows for seamless data management, appointment scheduling, and secure patient portal access, enhancing the overall patient experience. These innovations not only improve diagnostic capabilities but also provide a competitive edge for medical examination centers by offering more precise, efficient, and patient-centric services.

Challenges in the Medical Examination Center Market

The Medical Examination Center Market faces several significant challenges that can impact growth and operational efficiency. Regulatory hurdles, including evolving data privacy laws (like GDPR and HIPAA) and stringent accreditation requirements, can increase compliance costs and complexity. Supply chain issues for specialized medical equipment and consumables can lead to delays and increased operational expenses, estimated to cause a 5–10% increase in operational costs. Intense competition from a diverse range of providers, from large hospital networks to smaller independent clinics, pressures pricing and necessitates continuous innovation to maintain market share. Furthermore, the cost of advanced technology adoption can be a significant barrier for smaller players.

Forces Driving Medical Examination Center Growth

Several key forces are propelling the Medical Examination Center Market forward. Technological advancements, such as AI in diagnostics and advanced imaging, are enhancing the precision and scope of examinations. The increasing global prevalence of chronic diseases and an aging population are driving demand for proactive health monitoring and early detection services. Growing health consciousness among individuals and a greater emphasis on employee wellness programs by corporations are also significant catalysts. Government initiatives promoting preventive healthcare and improved access to medical services further contribute to market expansion. The integration of digital health solutions, including telemedicine and wearable devices, is making healthcare more accessible and convenient.

Long-Term Growth Catalysts in the Medical Examination Center Market

Long-term growth in the Medical Examination Center Market will be fueled by sustained innovation and strategic market expansion. Continuous research and development in areas like personalized medicine, genomics, and advanced preventive diagnostics will create new service offerings and attract a wider clientele. Strategic partnerships between medical examination centers, research institutions, and technology providers will accelerate the adoption of novel solutions and enhance service delivery. Furthermore, expanding into underserved geographical regions and developing specialized examination packages tailored to specific demographic needs or health concerns will unlock new revenue streams and solidify market leadership. The increasing focus on preventative health by governments and insurance providers globally will also act as a significant long-term growth accelerator.

Emerging Opportunities in Medical Examination Center

Emerging opportunities within the Medical Examination Center Market are ripe for strategic exploitation. The growing demand for niche diagnostic services, such as advanced cancer screenings, cardiovascular risk assessments, and metabolic health evaluations, presents significant potential. The expansion of telemedicine and remote monitoring capabilities allows for continuous patient engagement beyond the examination visit, fostering loyalty and recurring revenue. The development of integrated wellness programs that combine medical examinations with lifestyle coaching and nutritional guidance caters to a growing consumer preference for holistic health solutions. Furthermore, tapping into emerging markets with developing healthcare infrastructures and rising disposable incomes offers substantial growth prospects for global medical examination center providers.

Leading Players in the Medical Examination Center Sector

- Kaiser Permanente

- Bupa

- Health 100

- IKang Group

- Japanese Red Cross

- Rich Healthcare

- Mayo Clinic

- Nuffield Health

- Cleveland Clinic

- Cooper Aerobics

- Samsung Total Healthcare Center

- Milord Health Group

- Seoul National University Hospital

- PL Tokyo Health Care Center

- Sun Medical Center

- Mediway Medical

- St. Luke’s International Hospital

- Seoul Medicare

- Lifescan Medical Centre

- Raffles Medical Group

- Tokyo Midtown Clinic

- AcuMed Medical

Key Milestones in Medical Examination Center Industry

- 2019: Increased adoption of AI for radiology image analysis, enhancing diagnostic accuracy.

- 2020 (Early): Surge in demand for infectious disease screening services (e.g., COVID-19 testing).

- 2020 (Mid): Expansion of telehealth and remote consultation services by numerous medical examination centers.

- 2021: Introduction of advanced genetic screening panels for personalized disease risk assessment.

- 2022: Greater integration of wearable health tracker data into comprehensive health reports.

- 2023: Strategic acquisitions by larger players to expand service offerings and geographical reach.

- 2024: Development of AI-driven platforms for predictive health analytics and early intervention.

- 2025 (Projected): Increased focus on mental health assessments as part of comprehensive check-ups.

- 2026 (Projected): Rollout of personalized nutrition and lifestyle plans based on genomic data.

- 2027 (Projected): Wider adoption of liquid biopsy techniques for early cancer detection.

- 2028 (Projected): Development of blockchain-based secure health record management systems.

- 2030 (Projected): Significant growth in on-demand and mobile medical examination services.

- 2033 (Projected): Full integration of personalized medicine into routine health check-ups across leading healthcare providers.

Strategic Outlook for Medical Examination Center Market

The strategic outlook for the Medical Examination Center Market is overwhelmingly positive, characterized by sustained growth and transformative innovation. Future expansion will be driven by the deepening integration of advanced technologies like AI, IoT, and big data analytics to provide hyper-personalized and predictive healthcare solutions. A key growth accelerator will be the continued emphasis on preventive medicine, driven by both individual consumer demand and supportive governmental policies aimed at reducing long-term healthcare burdens. Partnerships between technology firms, healthcare providers, and insurance companies will foster a more holistic and accessible healthcare ecosystem. Strategic opportunities lie in expanding into rapidly developing economies, catering to the growing demand for specialized comprehensive physical examination services, and leveraging digital platforms to enhance patient engagement and convenience, solidifying the market's trajectory towards a future of proactive and personalized health management.

Medical Examination Center Segmentation

-

1. Application

- 1.1. Enterprise

- 1.2. Individuals

-

2. Type

- 2.1. Routine Physical Examination

- 2.2. Comprehensive Physical Examination

- 2.3. Others

Medical Examination Center Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Examination Center Regional Market Share

Geographic Coverage of Medical Examination Center

Medical Examination Center REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Examination Center Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Enterprise

- 5.1.2. Individuals

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Routine Physical Examination

- 5.2.2. Comprehensive Physical Examination

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Examination Center Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Enterprise

- 6.1.2. Individuals

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Routine Physical Examination

- 6.2.2. Comprehensive Physical Examination

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Examination Center Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Enterprise

- 7.1.2. Individuals

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Routine Physical Examination

- 7.2.2. Comprehensive Physical Examination

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Examination Center Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Enterprise

- 8.1.2. Individuals

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Routine Physical Examination

- 8.2.2. Comprehensive Physical Examination

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Examination Center Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Enterprise

- 9.1.2. Individuals

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Routine Physical Examination

- 9.2.2. Comprehensive Physical Examination

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Examination Center Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Enterprise

- 10.1.2. Individuals

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Routine Physical Examination

- 10.2.2. Comprehensive Physical Examination

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Kaiser Permanente

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bupa

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Health 100

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 IKang Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Japanese Red Cross

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Rich Healthcare

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Mayo Clinic

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nuffield Health

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Cleveland Clinic

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cooper Aerobics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Samsung Total Healthcare Center

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Milord Health Group

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Seoul National University Hospital

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 PL Tokyo Health Care Center

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Sun Medical Center

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Mediway Medical

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 St. Luke’s International Hospital

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Seoul Medicare

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Lifescan Medical Centre

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Raffles Medical Group

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Tokyo Midtown Clinic

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 AcuMed Medical

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.1 Kaiser Permanente

List of Figures

- Figure 1: Global Medical Examination Center Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Medical Examination Center Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Medical Examination Center Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Examination Center Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Medical Examination Center Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Medical Examination Center Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Medical Examination Center Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Examination Center Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Medical Examination Center Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Examination Center Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Medical Examination Center Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Medical Examination Center Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Medical Examination Center Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Examination Center Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Medical Examination Center Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Examination Center Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Medical Examination Center Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Medical Examination Center Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Medical Examination Center Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Examination Center Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Examination Center Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Examination Center Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Medical Examination Center Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Medical Examination Center Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Examination Center Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Examination Center Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Examination Center Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Examination Center Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Medical Examination Center Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Medical Examination Center Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Examination Center Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Examination Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Examination Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Medical Examination Center Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Medical Examination Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Medical Examination Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Medical Examination Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Examination Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Medical Examination Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Medical Examination Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Examination Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Medical Examination Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Medical Examination Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Examination Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Medical Examination Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Medical Examination Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Examination Center Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Medical Examination Center Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Medical Examination Center Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Examination Center Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Examination Center?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Medical Examination Center?

Key companies in the market include Kaiser Permanente, Bupa, Health 100, IKang Group, Japanese Red Cross, Rich Healthcare, Mayo Clinic, Nuffield Health, Cleveland Clinic, Cooper Aerobics, Samsung Total Healthcare Center, Milord Health Group, Seoul National University Hospital, PL Tokyo Health Care Center, Sun Medical Center, Mediway Medical, St. Luke’s International Hospital, Seoul Medicare, Lifescan Medical Centre, Raffles Medical Group, Tokyo Midtown Clinic, AcuMed Medical.

3. What are the main segments of the Medical Examination Center?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Examination Center," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Examination Center report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Examination Center?

To stay informed about further developments, trends, and reports in the Medical Examination Center, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence