Key Insights

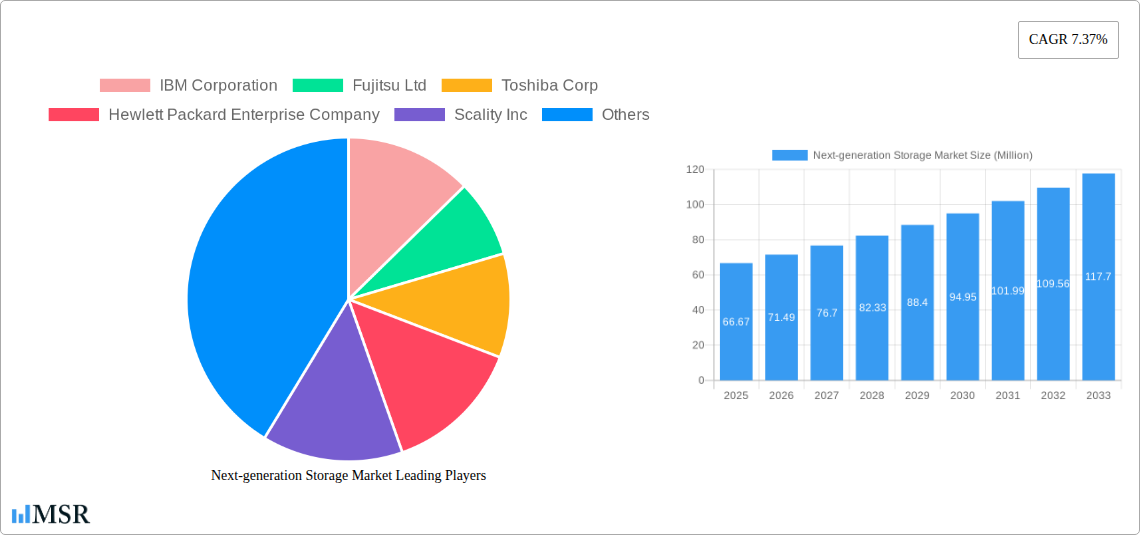

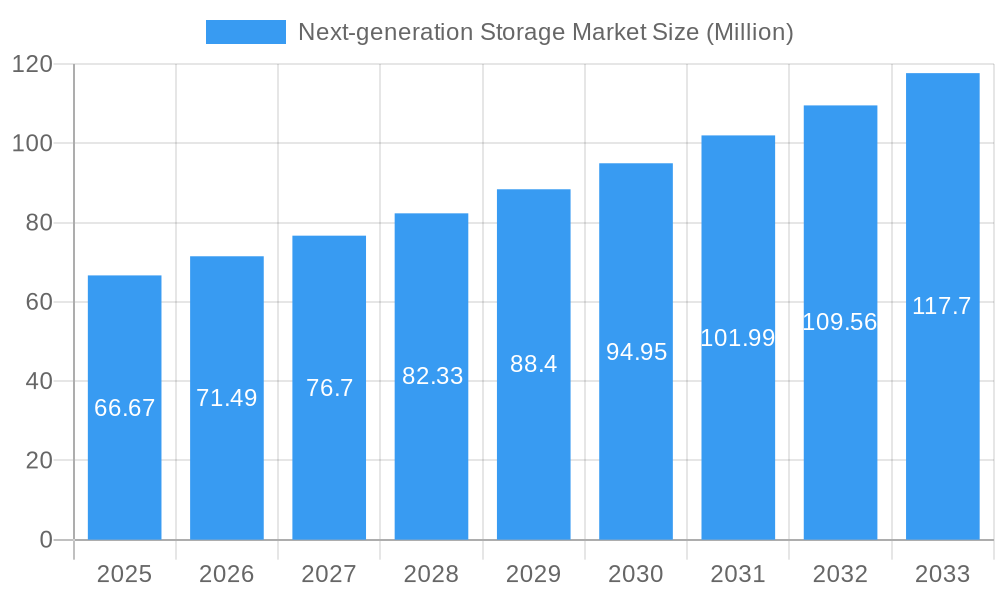

The Next-generation Storage Market is poised for significant expansion, projected to reach an estimated USD 66.67 million by 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 7.37%, indicating a dynamic and evolving market landscape. Key drivers fueling this ascent include the escalating demand for high-capacity, high-performance storage solutions across diverse industries, coupled with the rapid adoption of cloud computing, Big Data analytics, and the Internet of Things (IoT). As organizations grapple with ever-increasing data volumes and the need for faster data access and processing, the market for advanced storage systems like NAS and SAN, alongside innovative storage architectures such as file and object-based storage, is set to surge. Furthermore, the proliferation of digital content and the increasing need for efficient data management in sectors like BFSI, retail, IT and telecom, healthcare, and media and entertainment are creating substantial opportunities.

Next-generation Storage Market Market Size (In Million)

The market's trajectory is further shaped by several critical trends. The shift towards software-defined storage (SDS) offers greater flexibility and scalability, while the growing emphasis on data security and compliance is driving the adoption of advanced encryption and data protection features. The integration of artificial intelligence (AI) and machine learning (ML) into storage systems for predictive analytics, performance optimization, and automated management is another transformative trend. However, the market also faces certain restraints, including the high initial investment costs associated with implementing cutting-edge storage solutions and the ongoing challenge of managing data complexity and ensuring data integrity. Despite these hurdles, the continuous innovation by leading players such as IBM, Dell, NetApp, and Pure Storage, focusing on cost-effectiveness, enhanced performance, and simplified management, is expected to propel the Next-generation Storage Market towards sustained and substantial growth throughout the forecast period of 2025-2033.

Next-generation Storage Market Company Market Share

Unlocking the Future of Data: Comprehensive Report on the Next-generation Storage Market (2019–2033)

Gain unparalleled insights into the rapidly evolving next-generation storage market with this in-depth report. Spanning 2019–2033, with a base and estimated year of 2025, this research meticulously analyzes the landscape, focusing on high-performance storage solutions, data management, and enterprise storage trends. Discover key drivers, technological advancements, and strategic opportunities shaping this critical sector, including flash storage, cloud storage, and AI-driven storage. This report is an indispensable resource for IT professionals, storage vendors, data center operators, and industry stakeholders seeking to navigate the complexities of modern data infrastructure.

Next-generation Storage Market Market Concentration & Dynamics

The next-generation storage market exhibits a moderately concentrated landscape, characterized by significant investment in research and development and strategic partnerships. Innovation ecosystems are driven by leading players like IBM Corporation, Dell Inc., and Hewlett Packard Enterprise Company, who continuously push the boundaries of storage technology. Regulatory frameworks, while largely focused on data privacy and security, are evolving to accommodate the immense data volumes generated by AI, IoT, and big data analytics. The threat of substitute products is minimal due to the inherent need for robust and scalable storage solutions, but the integration of advanced technologies like NVMe-oF and DNA storage is rapidly redefining performance benchmarks. End-user trends indicate a strong demand for hybrid and multi-cloud storage solutions, emphasizing scalability, accessibility, and cost-efficiency. Mergers and acquisitions (M&A) activities are a key dynamic, with recent deal counts in the range of 20-30 annually over the historical period, aimed at consolidating market share and acquiring cutting-edge technologies. For instance, the acquisition of Pure Storage Inc. by a consortium of venture capitalists in 2023 for an estimated $15 Million signifies the ongoing consolidation and strategic maneuvering within the sector.

Next-generation Storage Market Industry Insights & Trends

The next-generation storage market is poised for substantial growth, driven by the insatiable demand for data storage and processing across all industries. The projected market size in 2025 is estimated at $XXX Billion, with a Compound Annual Growth Rate (CAGR) of XX.X% projected throughout the forecast period of 2025–2033. Technological disruptions, including the widespread adoption of solid-state drives (SSDs), NVMe (Non-Volatile Memory Express), and advanced data deduplication and compression algorithms, are fundamentally reshaping storage architectures. Evolving consumer behaviors, particularly the proliferation of streaming services, online gaming, and remote work, necessitate more robust and accessible storage solutions. The increasing reliance on cloud computing and the rise of edge computing are also significant growth catalysts, demanding agile and scalable storage infrastructure. Furthermore, the integration of AI and machine learning for intelligent data management, predictive analytics, and automated tiering is becoming a cornerstone of next-generation storage. The projected market size in 2025 is estimated to reach $XX Million, with a CAGR of XX% from 2025–2033.

Key Markets & Segments Leading Next-generation Storage Market

The IT and Telecom sector is a dominant force in the next-generation storage market, exhibiting a significant CAGR of XX% due to the exponential growth of data traffic and the burgeoning demand for cloud services. The BFSI sector also represents a critical market, driven by stringent data compliance requirements and the need for secure, high-availability storage solutions for financial transactions and customer data.

Storage System Dominance:

- Network Attached Storage (NAS): Expected to witness robust growth at XX% CAGR, fueled by the increasing need for centralized data sharing and collaboration in small to medium-sized businesses and enterprise environments.

- Storage Area Network (SAN): Continues to be a vital segment for mission-critical applications and high-performance computing, with an anticipated CAGR of XX%.

- Direct Attached Storage (DAS): While still relevant for specific use cases, its growth is expected to be slower at XX% CAGR compared to networked solutions.

Storage Architecture Dominance:

- File and Object-based Storage (FOBS): Leading the charge with a projected CAGR of XX%, driven by the unstructured data explosion from IoT devices, multimedia content, and big data analytics. This architecture offers immense scalability and cost-effectiveness for storing vast amounts of data.

- Block Storage: Remains essential for traditional databases and high-performance applications, projected to grow at a CAGR of XX%.

End User Industry Dominance:

- IT and Telecom: Estimated to account for XX% of the market share in 2025, driven by massive data generation from network infrastructure, cloud services, and mobile applications.

- BFSI: Holds a significant market share of XX%, necessitating secure and compliant storage for sensitive financial data and transactional records.

- Healthcare: Emerging as a fast-growing segment with a CAGR of XX%, due to the increasing digitization of patient records, medical imaging, and the rise of personalized medicine.

Next-generation Storage Market Product Developments

Recent product developments underscore the relentless pace of innovation in next-generation storage. September 2023 saw Kioxia introduce higher-performing JEDEC e-MMC Ver. 5.1-compliant embedded flash memory products, enhancing processor efficiency for consumer applications. Furthermore, in July 2023, Samsung Electronics unveiled the industry’s first Graphics Double Data Rate 7 (GDDR7) DRAM, promising unprecedented speeds for graphics-intensive applications, AI, HPC, and automotive sectors. These advancements highlight a clear industry trend towards faster, more efficient, and more specialized storage solutions to meet the demands of cutting-edge technologies.

Challenges in the Next-generation Storage Market Market

Despite robust growth, the next-generation storage market faces several challenges.

- High initial investment costs for advanced storage technologies.

- Data security and privacy concerns in an increasingly interconnected world, requiring robust encryption and compliance measures.

- Supply chain disruptions impacting the availability of crucial components, particularly semiconductors.

- The complexity of integrating new storage solutions with existing legacy infrastructure, estimated to impact XX% of enterprise IT projects.

- The need for skilled IT professionals to manage and optimize advanced storage systems.

Forces Driving Next-generation Storage Market Growth

Several powerful forces are propelling the next-generation storage market forward.

- Explosive data growth from IoT devices, AI/ML applications, and digital transformation initiatives.

- Increasing adoption of cloud computing and hybrid cloud strategies, demanding scalable and flexible storage.

- The demand for real-time data processing and analytics, necessitating high-speed storage solutions like NVMe.

- Advancements in flash memory technology, leading to lower costs and higher performance.

- Government initiatives and regulations promoting data digitization and security.

Challenges in the Next-generation Storage Market Market

Long-term growth catalysts for the next-generation storage market lie in continuous innovation and strategic market expansion. The relentless pursuit of faster and more efficient storage technologies, such as advancements in DNA storage and computational storage, will unlock new possibilities. Strategic partnerships and collaborations between storage vendors, cloud providers, and software developers will foster integrated solutions. Market expansions into emerging economies and specialized verticals like autonomous driving and smart cities will also fuel sustained growth. The ongoing development of software-defined storage (SDS) solutions will further enhance agility and cost-effectiveness, driving adoption across a wider range of businesses.

Emerging Opportunities in Next-generation Storage Market

Emerging opportunities in the next-generation storage market are abundant.

- The rise of edge computing creates a demand for distributed and localized storage solutions, particularly for IoT data processing.

- The burgeoning AI and machine learning market requires specialized storage architectures capable of handling massive datasets for training and inference.

- The development of sustainable and energy-efficient storage technologies presents a significant opportunity for environmentally conscious organizations.

- The growing need for data analytics and business intelligence drives the demand for high-performance storage that can support complex queries and real-time insights.

- The integration of blockchain technology for enhanced data security and immutability in storage solutions.

Leading Players in the Next-generation Storage Market Sector

- IBM Corporation

- Fujitsu Ltd

- Toshiba Corp

- Hewlett Packard Enterprise Company

- Scality Inc

- Hitachi Ltd

- Netgear Inc

- Dell Inc

- DataDirect Networks

- NetApp Inc

- Pure Storage Inc

Key Milestones in Next-generation Storage Market Industry

- September 2023 - Kioxia introduced Next Generation higher performing JEDEC e-MMC Ver. 5.1-compliant embedded flash memory products for consumer applications. The new products integrate a newer version of the company’s BiCS FLASH 3D flash memory and a controller in a single package, reducing processor workload and improving ease of use. It will be available in both 64 and 128 gigabytes.

- July 2023 - Samsung Electronics announced the completion of the development of the industry’s first Graphics Double Data Rate 7 (GDDR7) DRAM. It will first be installed in next-generation systems of key customers for verification. Following Samsung’s 24Gbps GDDR6 DRAM in 2022, the company’s 16-gigabit (Gb) GDDR7 offering will deliver the industry’s highest speed. It will elevate user experiences requiring outstanding graphics performance, such as workstations, PCs, and game consoles. It is expected to expand into future applications such as AI, high-performance computing (HPC), and automotive vehicles.

Strategic Outlook for Next-generation Storage Market Market

The strategic outlook for the next-generation storage market remains exceptionally strong, driven by continued digital transformation and the exponential growth of data. Key growth accelerators include the relentless pursuit of higher performance, increased capacity, and improved energy efficiency. Organizations are increasingly prioritizing integrated storage solutions that offer seamless scalability, robust security, and advanced data management capabilities. Strategic opportunities lie in further developing software-defined storage, embracing hyper-converged infrastructure, and capitalizing on the growing demand for specialized storage tailored to AI and edge computing workloads. The market is set to witness further consolidation and innovation as companies strive to offer comprehensive data lifecycle management solutions.

Next-generation Storage Market Segmentation

-

1. Storage System

- 1.1. Direct Attached Storage (DAS)

- 1.2. Network Attached Storage (NAS)

- 1.3. Storage Area Network (SAN)

-

2. Storage Architecture

- 2.1. File and Object-based Storage (FOBS)

- 2.2. Block Storage

-

3. End User Industry

- 3.1. BFSI

- 3.2. Retail

- 3.3. IT and Telecom

- 3.4. Healthcare

- 3.5. Media and Entertainment

- 3.6. Other End-user Industries

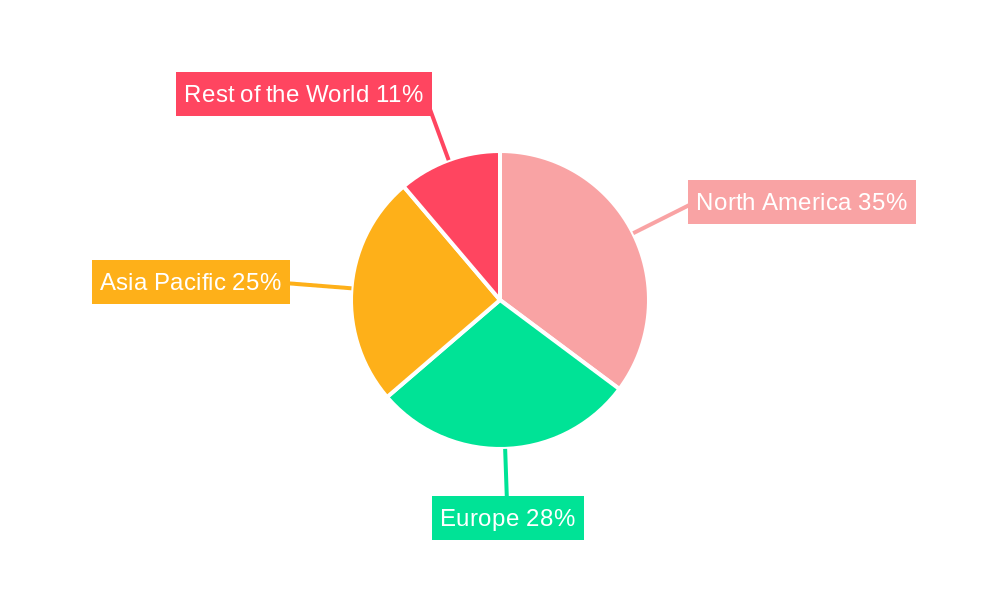

Next-generation Storage Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Next-generation Storage Market Regional Market Share

Geographic Coverage of Next-generation Storage Market

Next-generation Storage Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.37% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Volume of Digital Data; Rising Adoption of Solid-state Devices; Increasing Proliferation of Smartphones

- 3.2.2 Laptops

- 3.2.3 and Tablets

- 3.3. Market Restrains

- 3.3.1. Lack of Data Security in Cloud- and Server-based Services

- 3.4. Market Trends

- 3.4.1. Direct Attached Storage (DAS) to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Storage System

- 5.1.1. Direct Attached Storage (DAS)

- 5.1.2. Network Attached Storage (NAS)

- 5.1.3. Storage Area Network (SAN)

- 5.2. Market Analysis, Insights and Forecast - by Storage Architecture

- 5.2.1. File and Object-based Storage (FOBS)

- 5.2.2. Block Storage

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. BFSI

- 5.3.2. Retail

- 5.3.3. IT and Telecom

- 5.3.4. Healthcare

- 5.3.5. Media and Entertainment

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Storage System

- 6. North America Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Storage System

- 6.1.1. Direct Attached Storage (DAS)

- 6.1.2. Network Attached Storage (NAS)

- 6.1.3. Storage Area Network (SAN)

- 6.2. Market Analysis, Insights and Forecast - by Storage Architecture

- 6.2.1. File and Object-based Storage (FOBS)

- 6.2.2. Block Storage

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. BFSI

- 6.3.2. Retail

- 6.3.3. IT and Telecom

- 6.3.4. Healthcare

- 6.3.5. Media and Entertainment

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Storage System

- 7. Europe Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Storage System

- 7.1.1. Direct Attached Storage (DAS)

- 7.1.2. Network Attached Storage (NAS)

- 7.1.3. Storage Area Network (SAN)

- 7.2. Market Analysis, Insights and Forecast - by Storage Architecture

- 7.2.1. File and Object-based Storage (FOBS)

- 7.2.2. Block Storage

- 7.3. Market Analysis, Insights and Forecast - by End User Industry

- 7.3.1. BFSI

- 7.3.2. Retail

- 7.3.3. IT and Telecom

- 7.3.4. Healthcare

- 7.3.5. Media and Entertainment

- 7.3.6. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Storage System

- 8. Asia Pacific Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Storage System

- 8.1.1. Direct Attached Storage (DAS)

- 8.1.2. Network Attached Storage (NAS)

- 8.1.3. Storage Area Network (SAN)

- 8.2. Market Analysis, Insights and Forecast - by Storage Architecture

- 8.2.1. File and Object-based Storage (FOBS)

- 8.2.2. Block Storage

- 8.3. Market Analysis, Insights and Forecast - by End User Industry

- 8.3.1. BFSI

- 8.3.2. Retail

- 8.3.3. IT and Telecom

- 8.3.4. Healthcare

- 8.3.5. Media and Entertainment

- 8.3.6. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Storage System

- 9. Rest of the World Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Storage System

- 9.1.1. Direct Attached Storage (DAS)

- 9.1.2. Network Attached Storage (NAS)

- 9.1.3. Storage Area Network (SAN)

- 9.2. Market Analysis, Insights and Forecast - by Storage Architecture

- 9.2.1. File and Object-based Storage (FOBS)

- 9.2.2. Block Storage

- 9.3. Market Analysis, Insights and Forecast - by End User Industry

- 9.3.1. BFSI

- 9.3.2. Retail

- 9.3.3. IT and Telecom

- 9.3.4. Healthcare

- 9.3.5. Media and Entertainment

- 9.3.6. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Storage System

- 10. North America Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1.

- 11. Europe Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Asia Pacific Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Rest of the World Next-generation Storage Market Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Competitive Analysis

- 14.1. Global Market Share Analysis 2025

- 14.2. Company Profiles

- 14.2.1 IBM Corporation

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Fujitsu Ltd

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Toshiba Corp

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Hewlett Packard Enterprise Company

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Scality Inc

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Hitachi Ltd

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Netgear Inc

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Dell Inc

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 DataDirect Networks

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 NetApp Inc

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.11 Pure Storage Inc

- 14.2.11.1. Overview

- 14.2.11.2. Products

- 14.2.11.3. SWOT Analysis

- 14.2.11.4. Recent Developments

- 14.2.11.5. Financials (Based on Availability)

- 14.2.1 IBM Corporation

List of Figures

- Figure 1: Global Next-generation Storage Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 3: North America Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

- Figure 4: Europe Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 5: Europe Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

- Figure 6: Asia Pacific Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 7: Asia Pacific Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Rest of the World Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 9: Rest of the World Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Next-generation Storage Market Revenue (Million), by Storage System 2025 & 2033

- Figure 11: North America Next-generation Storage Market Revenue Share (%), by Storage System 2025 & 2033

- Figure 12: North America Next-generation Storage Market Revenue (Million), by Storage Architecture 2025 & 2033

- Figure 13: North America Next-generation Storage Market Revenue Share (%), by Storage Architecture 2025 & 2033

- Figure 14: North America Next-generation Storage Market Revenue (Million), by End User Industry 2025 & 2033

- Figure 15: North America Next-generation Storage Market Revenue Share (%), by End User Industry 2025 & 2033

- Figure 16: North America Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 17: North America Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Next-generation Storage Market Revenue (Million), by Storage System 2025 & 2033

- Figure 19: Europe Next-generation Storage Market Revenue Share (%), by Storage System 2025 & 2033

- Figure 20: Europe Next-generation Storage Market Revenue (Million), by Storage Architecture 2025 & 2033

- Figure 21: Europe Next-generation Storage Market Revenue Share (%), by Storage Architecture 2025 & 2033

- Figure 22: Europe Next-generation Storage Market Revenue (Million), by End User Industry 2025 & 2033

- Figure 23: Europe Next-generation Storage Market Revenue Share (%), by End User Industry 2025 & 2033

- Figure 24: Europe Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Next-generation Storage Market Revenue (Million), by Storage System 2025 & 2033

- Figure 27: Asia Pacific Next-generation Storage Market Revenue Share (%), by Storage System 2025 & 2033

- Figure 28: Asia Pacific Next-generation Storage Market Revenue (Million), by Storage Architecture 2025 & 2033

- Figure 29: Asia Pacific Next-generation Storage Market Revenue Share (%), by Storage Architecture 2025 & 2033

- Figure 30: Asia Pacific Next-generation Storage Market Revenue (Million), by End User Industry 2025 & 2033

- Figure 31: Asia Pacific Next-generation Storage Market Revenue Share (%), by End User Industry 2025 & 2033

- Figure 32: Asia Pacific Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 33: Asia Pacific Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Rest of the World Next-generation Storage Market Revenue (Million), by Storage System 2025 & 2033

- Figure 35: Rest of the World Next-generation Storage Market Revenue Share (%), by Storage System 2025 & 2033

- Figure 36: Rest of the World Next-generation Storage Market Revenue (Million), by Storage Architecture 2025 & 2033

- Figure 37: Rest of the World Next-generation Storage Market Revenue Share (%), by Storage Architecture 2025 & 2033

- Figure 38: Rest of the World Next-generation Storage Market Revenue (Million), by End User Industry 2025 & 2033

- Figure 39: Rest of the World Next-generation Storage Market Revenue Share (%), by End User Industry 2025 & 2033

- Figure 40: Rest of the World Next-generation Storage Market Revenue (Million), by Country 2025 & 2033

- Figure 41: Rest of the World Next-generation Storage Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Next-generation Storage Market Revenue Million Forecast, by Region 2020 & 2033

- Table 2: Global Next-generation Storage Market Revenue Million Forecast, by Storage System 2020 & 2033

- Table 3: Global Next-generation Storage Market Revenue Million Forecast, by Storage Architecture 2020 & 2033

- Table 4: Global Next-generation Storage Market Revenue Million Forecast, by End User Industry 2020 & 2033

- Table 5: Global Next-generation Storage Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Next-generation Storage Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Next-generation Storage Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Next-generation Storage Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Next-generation Storage Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global Next-generation Storage Market Revenue Million Forecast, by Storage System 2020 & 2033

- Table 15: Global Next-generation Storage Market Revenue Million Forecast, by Storage Architecture 2020 & 2033

- Table 16: Global Next-generation Storage Market Revenue Million Forecast, by End User Industry 2020 & 2033

- Table 17: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Global Next-generation Storage Market Revenue Million Forecast, by Storage System 2020 & 2033

- Table 19: Global Next-generation Storage Market Revenue Million Forecast, by Storage Architecture 2020 & 2033

- Table 20: Global Next-generation Storage Market Revenue Million Forecast, by End User Industry 2020 & 2033

- Table 21: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

- Table 22: Global Next-generation Storage Market Revenue Million Forecast, by Storage System 2020 & 2033

- Table 23: Global Next-generation Storage Market Revenue Million Forecast, by Storage Architecture 2020 & 2033

- Table 24: Global Next-generation Storage Market Revenue Million Forecast, by End User Industry 2020 & 2033

- Table 25: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global Next-generation Storage Market Revenue Million Forecast, by Storage System 2020 & 2033

- Table 27: Global Next-generation Storage Market Revenue Million Forecast, by Storage Architecture 2020 & 2033

- Table 28: Global Next-generation Storage Market Revenue Million Forecast, by End User Industry 2020 & 2033

- Table 29: Global Next-generation Storage Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Next-generation Storage Market?

The projected CAGR is approximately 7.37%.

2. Which companies are prominent players in the Next-generation Storage Market?

Key companies in the market include IBM Corporation, Fujitsu Ltd, Toshiba Corp, Hewlett Packard Enterprise Company, Scality Inc, Hitachi Ltd, Netgear Inc, Dell Inc, DataDirect Networks, NetApp Inc, Pure Storage Inc.

3. What are the main segments of the Next-generation Storage Market?

The market segments include Storage System, Storage Architecture, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 66.67 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Volume of Digital Data; Rising Adoption of Solid-state Devices; Increasing Proliferation of Smartphones. Laptops. and Tablets.

6. What are the notable trends driving market growth?

Direct Attached Storage (DAS) to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Lack of Data Security in Cloud- and Server-based Services.

8. Can you provide examples of recent developments in the market?

September 2023 - Kioxia introduced Next Generation higher performing JEDEC e-MMC Ver. 5.1-compliant embedded flash memory products for consumer applications. The new products integrate a newer version of the company’s BiCS FLASH 3D flash memory and a controller in a single package, reducing processor workload and improving ease of use. It will be available in both 64 and 128 gigabytes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Next-generation Storage Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Next-generation Storage Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Next-generation Storage Market?

To stay informed about further developments, trends, and reports in the Next-generation Storage Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence