Key Insights

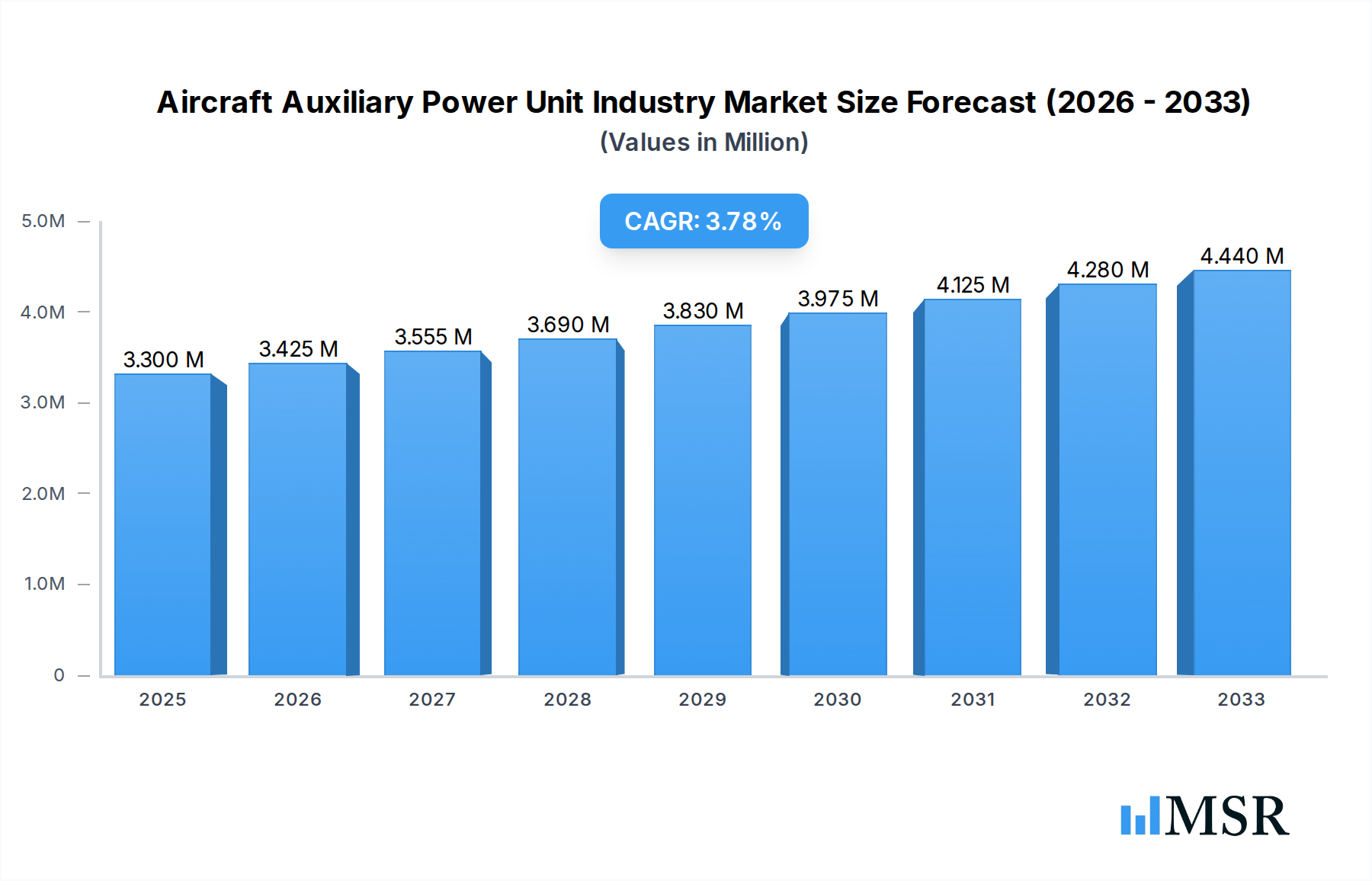

The global Aircraft Auxiliary Power Unit (APU) market is poised for robust growth, projected to reach USD 3.30 Million by 2025, with a Compound Annual Growth Rate (CAGR) of 3.79% from 2019 to 2033. This expansion is primarily fueled by the escalating demand for air travel, leading to increased aircraft production and a growing need for efficient and reliable APU systems. The continuous advancements in APU technology, focusing on improved fuel efficiency, reduced emissions, and enhanced durability, are also significant growth drivers. Furthermore, the increasing adoption of advanced materials and sophisticated control systems is enhancing APU performance and contributing to market expansion. The modernization of existing aircraft fleets with updated APU models to meet stringent regulatory standards and operational demands is another key factor bolstering market growth.

Aircraft Auxiliary Power Unit Industry Market Size (In Million)

The market is segmented by aircraft type into Fixed-Wing and Rotary-Wing. While fixed-wing aircraft represent a larger segment due to their widespread use in commercial aviation, the rotary-wing segment is also experiencing steady growth driven by defense applications and expanding helicopter services. Key players in the market include established aerospace giants and specialized APU manufacturers, all actively engaged in research and development to offer innovative solutions. Despite the positive outlook, the market faces certain restraints, such as the high initial cost of APUs and the stringent certification processes for new technologies. However, the persistent drive for operational efficiency, passenger comfort, and adherence to environmental regulations are expected to drive sustained demand for advanced APU solutions across the globe.

Aircraft Auxiliary Power Unit Industry Company Market Share

Here is an SEO-optimized, engaging report description for the Aircraft Auxiliary Power Unit Industry, ready for immediate use.

Aircraft Auxiliary Power Unit Industry Market Concentration & Dynamics

The Aircraft Auxiliary Power Unit (APU) industry exhibits a moderate to high market concentration, driven by the significant capital investment, advanced technological expertise, and stringent regulatory approvals required for APU manufacturing and servicing. Key players like Honeywell International Inc, Eaton Corporation plc, and Pratt & Whitney (RTX Corporation) hold substantial market shares, influencing innovation and pricing dynamics. The innovation ecosystem is characterized by intense R&D focused on improving fuel efficiency, reducing emissions, and enhancing APU reliability for both fixed-wing and rotary-wing aircraft. Regulatory frameworks, primarily governed by aviation authorities such as the FAA and EASA, impose rigorous safety and performance standards, acting as a significant barrier to entry for new competitors. The threat of substitute products is currently low, as APUs remain a critical and indispensable component for aircraft operations, providing essential power for systems during ground operations, engine start-up, and emergency situations. End-user trends are increasingly leaning towards sustainable aviation, pushing for more electric APUs and hybrid-electric solutions, alongside greater integration with advanced avionics. Mergers and Acquisition (M&A) activities within the sector, though not exceptionally frequent, are strategic, often involving component suppliers integrating capabilities or larger aerospace conglomerates acquiring specialized APU expertise. Recent years have seen a steady flow of M&A deals, with approximately 5-10 significant transactions annually, valued at hundreds of millions of dollars, aimed at consolidating market presence and expanding product portfolios.

Aircraft Auxiliary Power Unit Industry Insights & Trends

The global Aircraft Auxiliary Power Unit (APU) market is projected for robust growth, driven by a confluence of factors shaping the aerospace industry. The market size for APUs is estimated to reach $12.5 Billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of approximately 5.8% throughout the forecast period of 2025–2033. This sustained expansion is primarily fueled by the increasing demand for new aircraft, both commercial and military, as global air travel continues its recovery and expansion post-pandemic. Advancements in APU technology, focusing on enhanced fuel efficiency, reduced emissions, and lighter weight designs, are also key growth drivers. The push towards more sustainable aviation practices is spurring innovation in electric and hybrid-electric APU solutions, creating new market opportunities. Furthermore, the growing fleet of aging aircraft necessitates regular maintenance, repair, and overhaul (MRO) services for existing APUs, contributing significantly to market revenue. The expansion of air cargo operations and the rise of regional and business aviation sectors further bolster the demand for reliable and efficient APU systems. Emerging economies, with their expanding aviation infrastructure and increasing disposable incomes, represent significant growth potential for APU manufacturers and service providers. The integration of advanced digital technologies, such as predictive maintenance and IoT capabilities within APUs, is enhancing their operational efficiency and attractiveness to airlines.

Key Markets & Segments Leading Aircraft Auxiliary Power Unit Industry

The Fixed-Wing aircraft segment is overwhelmingly the dominant force in the Aircraft Auxiliary Power Unit (APU) industry, accounting for an estimated 85% of the global market share. This dominance is attributed to the sheer volume of fixed-wing aircraft operations across commercial aviation, cargo transport, military applications, and business jets. Within the fixed-wing segment, the commercial aviation sector represents the largest consumer of APUs, driven by the continuous demand for new passenger and cargo aircraft.

- Drivers for Fixed-Wing Dominance:

- Global Air Travel Growth: The sustained recovery and projected expansion of international and domestic air travel directly translate into higher demand for new commercial aircraft, each equipped with APUs.

- Fleet Expansion and Replacement: Airlines worldwide are constantly modernizing their fleets, replacing older models with more fuel-efficient and technologically advanced aircraft, thereby boosting APU sales.

- Cargo Aviation Boom: The surge in e-commerce and global trade has led to a significant increase in air cargo operations, necessitating a larger fleet of cargo freighters equipped with APUs.

- Military Procurement: Ongoing global defense spending and modernization programs in various countries drive the demand for military fixed-wing aircraft, which rely heavily on APUs for mission readiness.

- Technological Advancements: Innovations in APU design for fixed-wing aircraft, focusing on weight reduction, increased power output, and improved fuel efficiency, further enhance their appeal.

The Rotary-Wing aircraft segment, while smaller in comparison, is also a significant and growing market for APUs. This segment encompasses helicopters used for passenger transport, emergency medical services (EMS), search and rescue (SAR), military operations, and offshore logistics.

- Drivers for Rotary-Wing Growth:

- Increasing Demand for Specialized Services: The growing need for medical evacuation, disaster relief, and specialized industrial applications fuels the demand for helicopters and their essential APU systems.

- Military Modernization: Many nations are investing in upgrading their helicopter fleets for various defense roles, contributing to APU market growth.

- Emerging Applications: The development of new applications for helicopters, such as urban air mobility (UAM) concepts and advanced surveillance, is expected to drive future demand.

- Technological Improvements: Similar to fixed-wing APUs, advancements in rotary-wing APU technology, including quieter operation and greater power density, are making them more attractive.

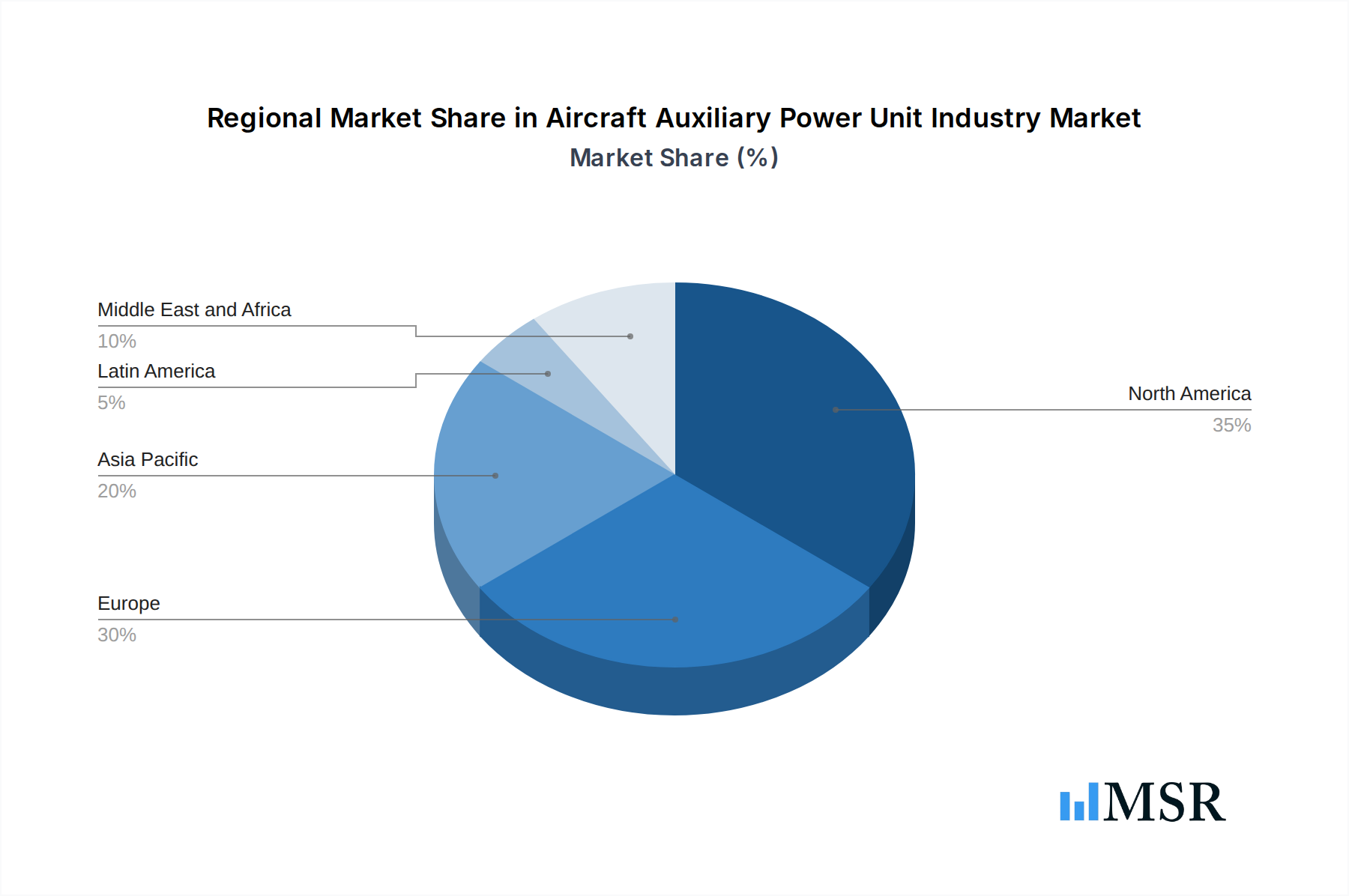

Geographically, North America and Europe currently lead the market, owing to their established aerospace manufacturing bases and significant airline operations. However, the Asia-Pacific region is emerging as a high-growth market, driven by increasing air travel demand, expanding domestic aviation manufacturing, and significant investments in aerospace infrastructure. Countries like China and India are becoming increasingly important.

Aircraft Auxiliary Power Unit Industry Product Developments

The Aircraft Auxiliary Power Unit (APU) industry is experiencing a wave of innovation focused on enhancing efficiency, reducing environmental impact, and improving operational capabilities. Key developments include the advancement of More Electric Aircraft (MEA) architectures, leading to the design of increasingly electric APUs that integrate seamlessly with aircraft power grids. Manufacturers are heavily investing in R&D to develop APUs with lower fuel consumption and reduced emissions, aligning with global sustainability goals. Innovations in digitalization and connectivity are also prominent, enabling predictive maintenance, remote diagnostics, and improved system monitoring. The development of lightweight materials and advanced manufacturing techniques is further contributing to the optimization of APU performance and reliability, offering a competitive edge to early adopters.

Challenges in the Aircraft Auxiliary Power Unit Industry Market

The Aircraft Auxiliary Power Unit (APU) market faces several significant challenges that can impede growth and profitability. Stringent and evolving regulatory requirements from aviation authorities necessitate continuous and costly compliance, impacting development timelines and R&D expenditures. Supply chain disruptions, exacerbated by geopolitical factors and global events, can lead to component shortages and increased manufacturing costs. The high initial cost of APU systems and their sophisticated maintenance requirements also present a barrier for some operators. Furthermore, the intense competition among established players and the threat of rapid technological obsolescence due to ongoing innovation demand constant investment in R&D to maintain a competitive edge.

Forces Driving Aircraft Auxiliary Power Unit Industry Growth

The growth of the Aircraft Auxiliary Power Unit (APU) industry is propelled by a powerful combination of technological advancements, economic factors, and evolving regulatory landscapes. The increasing global demand for air travel, both for passengers and cargo, is a primary driver, necessitating the production of new aircraft equipped with reliable APU systems. Technological innovation, particularly in areas like fuel efficiency, emission reduction, and the development of more electric APUs, is creating new market opportunities and enhancing the appeal of existing technologies. Government initiatives and regulations promoting sustainable aviation and stricter environmental standards are also pushing manufacturers towards greener APU solutions. The growth of the global aerospace MRO market ensures a steady revenue stream from the servicing and maintenance of existing APU fleets.

Challenges in the Aircraft Auxiliary Power Unit Industry Market

Long-term growth catalysts for the Aircraft Auxiliary Power Unit (APU) industry are deeply rooted in continuous innovation and strategic market expansion. The transition towards sustainable aviation fuels and electric propulsion systems presents a significant long-term opportunity, pushing the development of novel APU technologies and hybrid-electric solutions. Increased investment in advanced composite materials and additive manufacturing will further drive efficiency and cost reduction in APU production. Strategic partnerships and collaborations between APU manufacturers, airframe OEMs, and technology providers will be crucial for accelerating the development and adoption of next-generation APUs. Expanding into emerging markets with growing aviation sectors, particularly in Asia and Africa, offers substantial potential for future growth and diversification.

Emerging Opportunities in Aircraft Auxiliary Power Unit Industry

The Aircraft Auxiliary Power Unit (APU) industry is poised to capitalize on several emerging trends and opportunities. The increasing focus on sustainable aviation is creating a demand for APUs that utilize alternative fuels or offer enhanced energy efficiency. The development of More Electric Aircraft (MEA) and the broader electrification trend in aviation present opportunities for innovative electric APU designs and integrated power management systems. The growth of the business and general aviation sector, alongside the burgeoning urban air mobility (UAM) market, offers new avenues for specialized APU solutions. Furthermore, advancements in digital technologies, including AI and IoT, are opening doors for enhanced predictive maintenance, remote diagnostics, and optimized APU performance monitoring.

Leading Players in the Aircraft Auxiliary Power Unit Industry Sector

- Eaton Corporation plc

- PBS Group a.s.

- Honeywell International Inc

- AEGIS Power Systems Inc

- Technodinamika (Rostec)

- Pratt & Whitney (RTX Corporation)

- Safran SA

- Rolls-Royce plc

- Motor Sich JSC

- JSC NPP Aerosila

Key Milestones in Aircraft Auxiliary Power Unit Industry Industry

- 2019: Honeywell launches its 131-9A APU for the Airbus A320neo family, enhancing fuel efficiency.

- 2020: Safran SA receives certification for its Sky Warden™ APU for helicopters, improving performance in challenging environments.

- 2021: Eaton Corporation plc announces advancements in its electric APU technology, signaling a shift towards more electric aircraft.

- 2022: Pratt & Whitney (RTX Corporation) celebrates the delivery of its 25,000th APU, highlighting its sustained market leadership.

- 2023: Rolls-Royce plc invests heavily in R&D for next-generation APUs focusing on hydrogen fuel cell technology for future aircraft.

- 2024 (Q1): PBS Group a.s. announces a strategic partnership with a major European airframe manufacturer for a new helicopter APU program.

- 2024 (Q2): AEGIS Power Systems Inc. receives FAA approval for its advanced APU for a new generation regional jet.

Strategic Outlook for Aircraft Auxiliary Power Unit Industry Market

The strategic outlook for the Aircraft Auxiliary Power Unit (APU) market is characterized by a strong focus on innovation, sustainability, and market expansion. Growth accelerators will be driven by the increasing demand for fuel-efficient and low-emission APUs, particularly for commercial aviation and defense applications. The continued development and integration of electric and hybrid-electric APU technologies will be paramount, aligning with the aerospace industry's decarbonization goals. Strategic partnerships with airframe manufacturers and the expansion into rapidly growing regional markets, such as the Asia-Pacific, will be crucial for capturing future market share. Furthermore, leveraging digital technologies for enhanced APU performance monitoring and predictive maintenance will offer significant value addition and competitive advantages.

Aircraft Auxiliary Power Unit Industry Segmentation

-

1. Aircraft Type

- 1.1. Fixed-Wing

- 1.2. Rotary-Wing

Aircraft Auxiliary Power Unit Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. France

- 2.3. Germany

- 2.4. Russia

- 2.5. Italy

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Mexico

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Egypt

- 5.4. Rest of Middle East and Africa

Aircraft Auxiliary Power Unit Industry Regional Market Share

Geographic Coverage of Aircraft Auxiliary Power Unit Industry

Aircraft Auxiliary Power Unit Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.79% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.1.1. Fixed-Wing

- 5.1.2. Rotary-Wing

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6. Global Aircraft Auxiliary Power Unit Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.1.1. Fixed-Wing

- 6.1.2. Rotary-Wing

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7. North America Aircraft Auxiliary Power Unit Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7.1.1. Fixed-Wing

- 7.1.2. Rotary-Wing

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8. Europe Aircraft Auxiliary Power Unit Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8.1.1. Fixed-Wing

- 8.1.2. Rotary-Wing

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9. Asia Pacific Aircraft Auxiliary Power Unit Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9.1.1. Fixed-Wing

- 9.1.2. Rotary-Wing

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10. Latin America Aircraft Auxiliary Power Unit Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10.1.1. Fixed-Wing

- 10.1.2. Rotary-Wing

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11. Middle East and Africa Aircraft Auxiliary Power Unit Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11.1.1. Fixed-Wing

- 11.1.2. Rotary-Wing

- 11.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Eaton Corporation pl

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 PBS Group a s

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Honeywell International Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 AEGIS Power Systems Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Technodinamika (Rostec)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pratt & Whitney (RTX Corporation)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Safran SA

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Rolls-Royce plc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Motor Sich JSC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 JSC NPP Aerosila

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Eaton Corporation pl

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aircraft Auxiliary Power Unit Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Aircraft Auxiliary Power Unit Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 3: North America Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 4: North America Aircraft Auxiliary Power Unit Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Aircraft Auxiliary Power Unit Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 7: Europe Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 8: Europe Aircraft Auxiliary Power Unit Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Aircraft Auxiliary Power Unit Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 11: Asia Pacific Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 12: Asia Pacific Aircraft Auxiliary Power Unit Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Asia Pacific Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America Aircraft Auxiliary Power Unit Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 15: Latin America Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 16: Latin America Aircraft Auxiliary Power Unit Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Latin America Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Aircraft Auxiliary Power Unit Industry Revenue (Million), by Aircraft Type 2025 & 2033

- Figure 19: Middle East and Africa Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 20: Middle East and Africa Aircraft Auxiliary Power Unit Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Middle East and Africa Aircraft Auxiliary Power Unit Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 2: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 4: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 8: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: France Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Germany Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Russia Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Italy Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Rest of Europe Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 16: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: China Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: India Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Japan Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Australia Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 23: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Brazil Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Mexico Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Rest of Latin America Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Aircraft Type 2020 & 2033

- Table 28: Global Aircraft Auxiliary Power Unit Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 29: United Arab Emirates Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Saudi Arabia Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Egypt Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Rest of Middle East and Africa Aircraft Auxiliary Power Unit Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aircraft Auxiliary Power Unit Industry?

The projected CAGR is approximately 3.79%.

2. Which companies are prominent players in the Aircraft Auxiliary Power Unit Industry?

Key companies in the market include Eaton Corporation pl, PBS Group a s, Honeywell International Inc, AEGIS Power Systems Inc, Technodinamika (Rostec), Pratt & Whitney (RTX Corporation), Safran SA, Rolls-Royce plc, Motor Sich JSC, JSC NPP Aerosila.

3. What are the main segments of the Aircraft Auxiliary Power Unit Industry?

The market segments include Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.30 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Commercial Aviation Segment Holds Highest Shares in the Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aircraft Auxiliary Power Unit Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aircraft Auxiliary Power Unit Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aircraft Auxiliary Power Unit Industry?

To stay informed about further developments, trends, and reports in the Aircraft Auxiliary Power Unit Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence