Key Insights

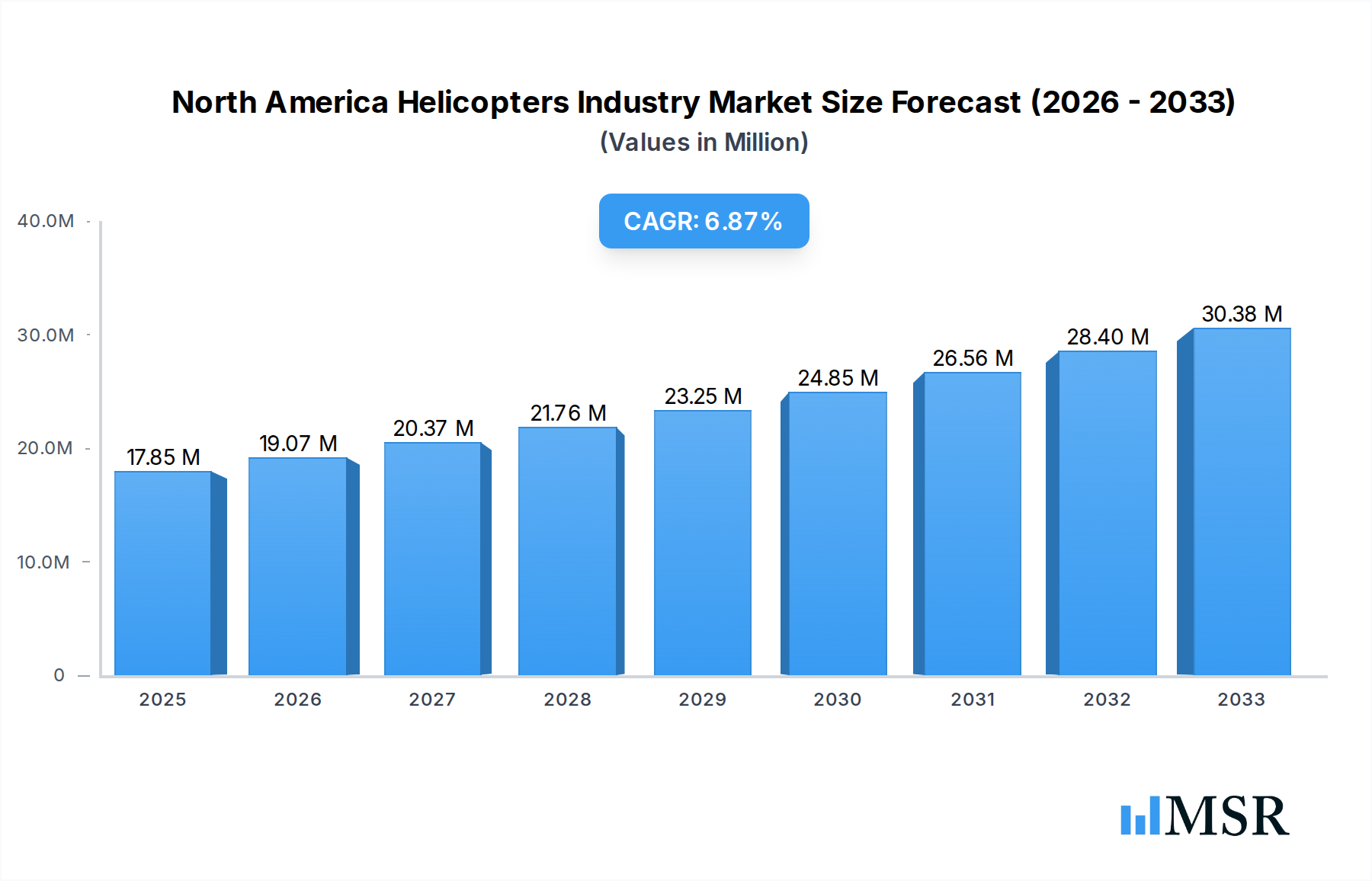

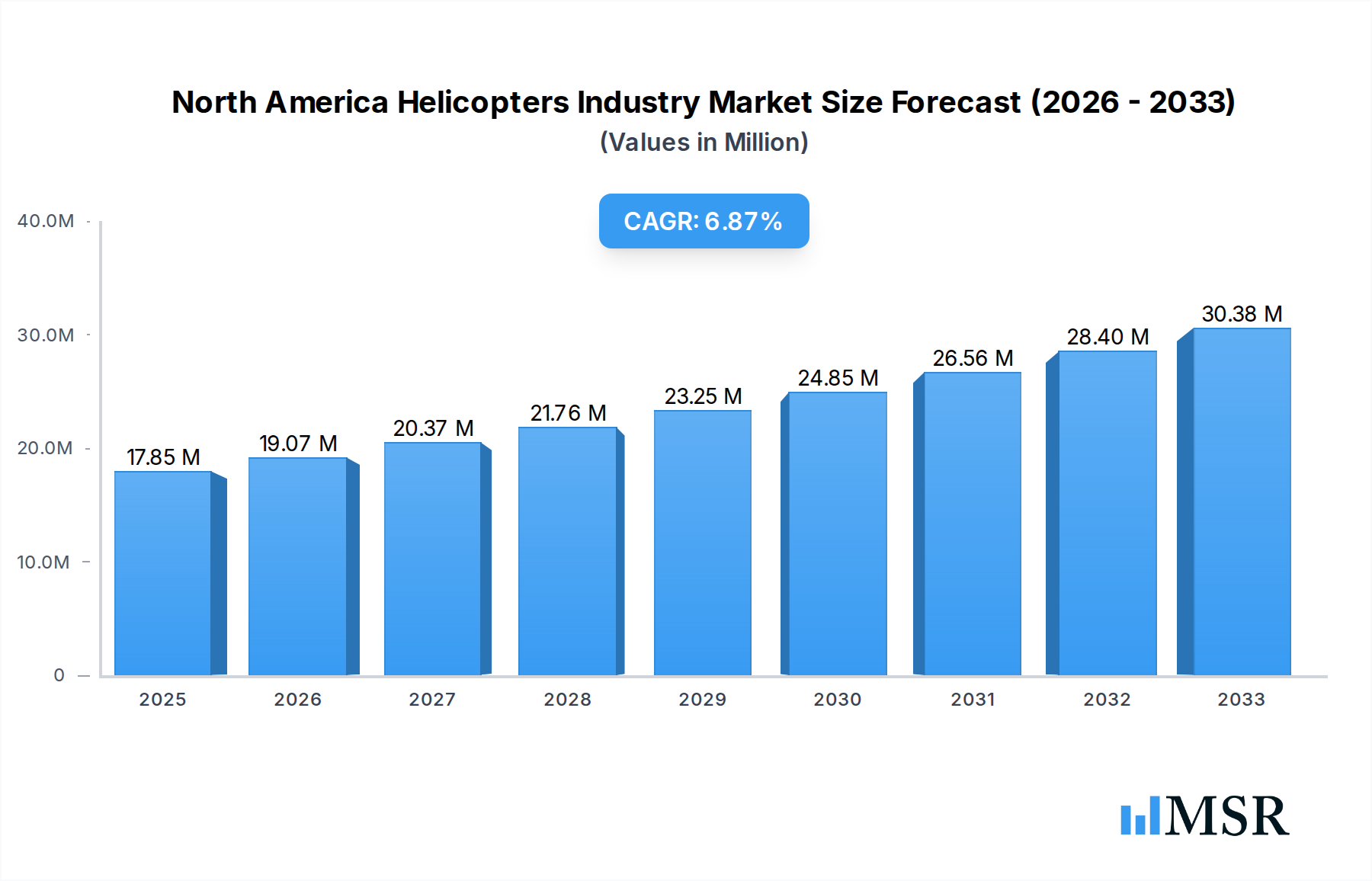

The North America Helicopters Industry is poised for significant expansion, with a current estimated market size of $17.85 million and a projected Compound Annual Growth Rate (CAGR) of 6.72% over the forecast period. This robust growth is fueled by a confluence of factors, including escalating demand for advanced rotorcraft in commercial applications such as emergency medical services (EMS), offshore transport, and corporate travel. The military sector also remains a critical driver, with ongoing modernization programs and defense spending in the United States and Canada necessitating the acquisition of new and upgraded helicopter fleets. Innovations in engine technology, particularly the development of more fuel-efficient and powerful turbine engines, are further contributing to market dynamism. The increasing adoption of sophisticated avionics, enhanced safety features, and the growing interest in electric and hybrid-electric helicopter designs are key trends shaping the industry's trajectory, promising improved performance and reduced environmental impact.

North America Helicopters Industry Market Size (In Million)

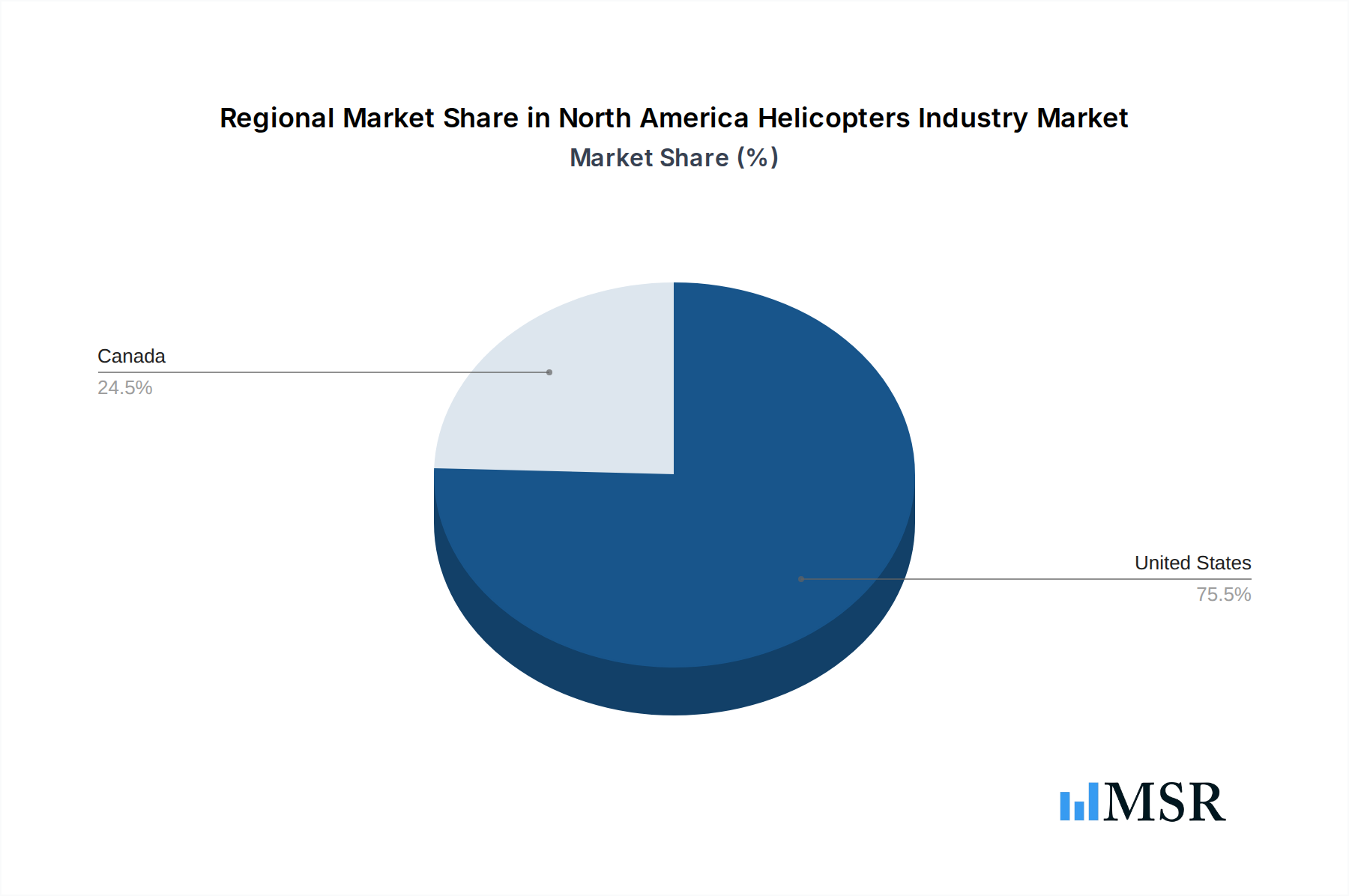

Despite the positive outlook, the market faces certain restraints that could temper its full potential. High acquisition and maintenance costs associated with sophisticated helicopters can be a barrier, especially for smaller commercial operators. Stringent regulatory frameworks governing aviation safety and operations, while essential, can also add complexity and cost to market entry and expansion. Furthermore, economic downturns or shifts in government defense budgets could impact demand. Geographically, the United States dominates the North American helicopter market due to its extensive military presence and a large, diverse commercial aviation sector. Canada, while smaller, presents substantial opportunities in resource extraction and search and rescue operations. Key players like Textron Inc., Lockheed Martin Corporation, Airbus SE, and Leonardo S.p.A. are actively investing in research and development to meet evolving market needs, focusing on areas like advanced propulsion systems and autonomous flight capabilities to maintain their competitive edge.

North America Helicopters Industry Company Market Share

North America Helicopters Industry Market Concentration & Dynamics

The North America helicopters industry is characterized by a moderate to high level of market concentration, with major global players like Textron Inc. (Bell), Lockheed Martin Corporation (Sikorsky), and Airbus SE holding significant market share. These industry giants, alongside The Boeing Company, Leonardo S.p.A., and Kopter Group, dominate innovation ecosystems, driving advancements in rotorcraft technology. Regulatory frameworks, including stringent FAA and Transport Canada certifications, play a crucial role in market entry and product development, fostering a landscape where safety and reliability are paramount. The presence of substitute products, such as fixed-wing aircraft and drones for specific applications, exerts competitive pressure, particularly in certain commercial segments. End-user trends are shifting towards increased demand for advanced avionics, enhanced payload capacity, and greater fuel efficiency, driven by both commercial operators and military modernization programs. Mergers and acquisitions (M&A) activity, while not consistently high, has historically reshaped the competitive landscape, with notable transactions aiming to consolidate market presence and expand product portfolios. For instance, recent years have seen strategic acquisitions focused on emerging technologies and specialized market niches. The overall market concentration is influenced by the substantial R&D investments required for helicopter development and manufacturing, creating high barriers to entry for new companies.

North America Helicopters Industry Industry Insights & Trends

The North America helicopters industry is poised for robust growth, with an estimated market size projected to reach $XX Billion in the base year of 2025, and anticipated to expand at a Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This upward trajectory is significantly fueled by escalating demand from the military sector, driven by ongoing modernization efforts and increasing global security concerns. The United States, a cornerstone of this market, continues to invest heavily in advanced rotorcraft for defense applications, including surveillance, troop transport, and attack missions. Concurrently, the commercial segment is experiencing a resurgence, propelled by growing needs in emergency medical services (EMS), law enforcement, offshore oil and gas exploration, and executive transport. Advancements in engine technology, particularly the adoption of more fuel-efficient and powerful turbine engines, are enhancing helicopter performance and reducing operational costs, thereby broadening their applicability. Furthermore, the integration of sophisticated avionics, autonomous flight capabilities, and advanced safety features is a key trend, addressing the industry’s continuous pursuit of operational excellence and enhanced pilot/passenger safety. The growing emphasis on sustainable aviation solutions is also influencing R&D, with manufacturers exploring hybrid-electric and electric propulsion systems for future rotorcraft. The rise of specialized helicopter applications, such as those supporting infrastructure development and disaster relief operations, further contributes to market expansion. Emerging markets within North America, particularly those requiring rapid transportation and access to remote areas, are also presenting new avenues for growth. The overall industry outlook is highly positive, supported by a strong existing installed base and continuous innovation.

Key Markets & Segments Leading North America Helicopters Industry

The United States unequivocally dominates the North America helicopters industry, accounting for the largest share of market value and volume. This dominance stems from a confluence of factors including a robust defense budget, a highly developed commercial aviation sector, and a significant presence of leading rotorcraft manufacturers. Within the United States, the Military end-user segment is a primary growth engine, consistently driving demand for advanced helicopters. This is directly linked to ongoing defense modernization programs, the need for enhanced surveillance capabilities, and strategic deployment requirements.

Key drivers for the military segment's leadership include:

- Geopolitical Stability & Defense Spending: Sustained government investment in national defense fuels the acquisition of new rotorcraft and upgrades to existing fleets.

- Technological Advancements: The U.S. military's emphasis on next-generation capabilities, such as stealth technology, advanced weaponry, and improved situational awareness, necessitates sophisticated helicopter platforms.

- Global Operations: The operational requirements of U.S. armed forces across various global theaters necessitate versatile and reliable rotary-wing assets for troop transport, combat support, and reconnaissance.

The Turbine engine segment is also a pivotal driver within the North America helicopters industry, particularly within the United States. Turbine engines offer superior power-to-weight ratios, higher performance capabilities, and greater reliability compared to piston engines, making them indispensable for both military and high-demand commercial applications.

Factors contributing to the dominance of the Turbine engine segment include:

- Performance Demands: The stringent performance requirements for military operations, including higher altitudes, greater speeds, and heavier payload capacities, are met by turbine engines.

- Commercial Applications: For offshore operations, EMS, and executive transport, the speed, range, and reliability offered by turbine-powered helicopters are critical.

- Technological Evolution: Continuous innovation in turbine engine design focuses on improved fuel efficiency, reduced emissions, and enhanced durability, further solidifying their market position.

While the Commercial segment is growing, particularly in EMS and law enforcement, the sheer scale of defense procurement and the operational demands of military aviation solidify the United States and the Turbine engine segment as the current leaders in the North America helicopters industry. Canada contributes significantly, with its own military procurement needs and a growing presence in commercial aviation, but the United States' market size and defense expenditure maintain its leading position.

North America Helicopters Industry Product Developments

Product innovation in the North America helicopters industry is witnessing a significant surge. Manufacturers like Textron Inc. (Bell) and Airbus SE are at the forefront, developing next-generation rotorcraft with enhanced capabilities. Key advancements include the integration of advanced avionics, fly-by-wire systems, and sophisticated sensor suites for improved situational awareness and operational efficiency. The pursuit of hybrid-electric and fully electric propulsion systems is a major trend, aiming to reduce operational costs and environmental impact. Furthermore, innovations in rotor blade design and airframe aerodynamics are contributing to increased speed, reduced noise, and improved fuel efficiency. These developments are crucial for meeting the evolving demands of both military and commercial end-users, ensuring a competitive edge in a dynamic market.

Challenges in the North America Helicopters Industry Market

The North America helicopters industry faces several significant challenges that could impede growth. The high cost of research, development, and manufacturing presents a substantial barrier to entry for new players and can limit investment in niche segments. Stringent regulatory compliance, including rigorous safety standards and lengthy certification processes, adds considerable time and expense to bringing new products to market. Supply chain disruptions, particularly for specialized components and raw materials, can lead to production delays and increased costs. Furthermore, the competitive pressure from alternative aviation solutions, such as advanced drones for certain surveillance and delivery tasks, necessitates continuous innovation to maintain market relevance. The long and complex sales cycles, especially within the military sector, also pose a financial and operational challenge for manufacturers.

Forces Driving North America Helicopters Industry Growth

Several powerful forces are propelling the growth of the North America helicopters industry. The unwavering demand from the military sector, driven by national security imperatives and ongoing fleet modernization programs, remains a primary catalyst. In the commercial realm, expanding applications in Emergency Medical Services (EMS), law enforcement, and offshore energy exploration are creating sustained market interest. Technological advancements, including the development of more fuel-efficient turbine engines, advanced avionics, and enhanced safety features, are making helicopters more attractive and versatile. Furthermore, favorable economic conditions in certain sectors and government initiatives supporting infrastructure development in remote areas contribute to increased demand for rotary-wing transportation and support services.

Challenges in the North America Helicopters Industry Market

Long-term growth catalysts for the North America helicopters industry lie in continued innovation and market expansion. The development and adoption of advanced propulsion systems, such as hybrid-electric and fully electric powertrains, will be crucial for meeting future sustainability goals and potentially reducing operational costs. Strategic partnerships and collaborations between manufacturers, technology providers, and end-users can accelerate the development and deployment of new capabilities. Furthermore, exploring new market applications, such as urban air mobility (UAM) and specialized cargo transport, holds significant potential. The ability of the industry to adapt to evolving regulatory landscapes and anticipate future consumer preferences will be key to sustaining its growth trajectory.

Emerging Opportunities in North America Helicopters Industry

Emerging opportunities within the North America helicopters industry are diverse and promising. The burgeoning urban air mobility (UAM) sector presents a significant untapped market for electric vertical takeoff and landing (eVTOL) aircraft, with North America leading development. The increasing need for efficient disaster relief and humanitarian aid operations is creating demand for specialized helicopters equipped for challenging environments. Furthermore, the expansion of offshore wind farm development necessitates robust aerial support, opening avenues for offshore transport and maintenance helicopters. The integration of artificial intelligence (AI) and machine learning (ML) in helicopter operations, for predictive maintenance and enhanced flight planning, also represents a key area for future growth and service provision.

Leading Players in the North America Helicopters Industry Sector

- Textron Inc.

- Lockheed Martin Corporation

- Airbus SE

- Enstrom Helicopter Corp

- MD Helicopters LLC

- Kopter Group

- Robinson Helicopter Company

- Leonardo S.p.A.

- The Boeing Company

Key Milestones in North America Helicopters Industry Industry

- 2019: Introduction of new advanced composite materials in rotor blade manufacturing by leading companies, enhancing durability and performance.

- 2020: Significant increase in military helicopter modernization contracts awarded by the U.S. Department of Defense, focusing on multi-role capabilities.

- 2021: First flight of a new-generation hybrid-electric helicopter prototype, showcasing advancements in sustainable aviation.

- 2022: Acquisition of a key aerospace technology firm by a major helicopter manufacturer to bolster its avionics and AI capabilities.

- 2023: Enhanced focus on autonomous flight systems and pilot assistance technologies in new product developments and upgrades.

- 2024: Growing interest and investment in eVTOL technology for potential future urban air mobility applications.

Strategic Outlook for North America Helicopters Industry Market

The strategic outlook for the North America helicopters industry is exceptionally strong, driven by continuous innovation and expanding market applications. The commitment to developing sustainable rotorcraft solutions, including hybrid-electric and electric propulsion, positions the industry for long-term growth and environmental responsibility. Strategic investments in advanced technologies such as AI, autonomy, and enhanced connectivity will further differentiate offerings and improve operational efficiency for end-users. The increasing demand for specialized missions in defense, emergency services, and emerging sectors like urban air mobility provides ample opportunities for market penetration and revenue growth. Manufacturers that can effectively navigate evolving regulatory landscapes and foster strong partnerships will be best positioned for success in this dynamic and evolving market.

North America Helicopters Industry Segmentation

-

1. Engine

- 1.1. Piston

- 1.2. Turbine

-

2. End-user

- 2.1. Commercial

- 2.2. Military

-

3. Geography

- 3.1. United States

- 3.2. Canada

North America Helicopters Industry Segmentation By Geography

- 1. United States

- 2. Canada

North America Helicopters Industry Regional Market Share

Geographic Coverage of North America Helicopters Industry

North America Helicopters Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.72% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Engine

- 5.1.1. Piston

- 5.1.2. Turbine

- 5.2. Market Analysis, Insights and Forecast - by End-user

- 5.2.1. Commercial

- 5.2.2. Military

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.1. Market Analysis, Insights and Forecast - by Engine

- 6. North America Helicopters Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Engine

- 6.1.1. Piston

- 6.1.2. Turbine

- 6.2. Market Analysis, Insights and Forecast - by End-user

- 6.2.1. Commercial

- 6.2.2. Military

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.1. Market Analysis, Insights and Forecast - by Engine

- 7. United States North America Helicopters Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Engine

- 7.1.1. Piston

- 7.1.2. Turbine

- 7.2. Market Analysis, Insights and Forecast - by End-user

- 7.2.1. Commercial

- 7.2.2. Military

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.1. Market Analysis, Insights and Forecast - by Engine

- 8. Canada North America Helicopters Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Engine

- 8.1.1. Piston

- 8.1.2. Turbine

- 8.2. Market Analysis, Insights and Forecast - by End-user

- 8.2.1. Commercial

- 8.2.2. Military

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.1. Market Analysis, Insights and Forecast - by Engine

- 9. Competitive Analysis

- 9.1. Company Profiles

- 9.1.1 Textron Inc

- 9.1.1.1. Company Overview

- 9.1.1.2. Products

- 9.1.1.3. Company Financials

- 9.1.1.4. SWOT Analysis

- 9.1.2 Lockheed Martin Corporation

- 9.1.2.1. Company Overview

- 9.1.2.2. Products

- 9.1.2.3. Company Financials

- 9.1.2.4. SWOT Analysis

- 9.1.3 Airbus SE

- 9.1.3.1. Company Overview

- 9.1.3.2. Products

- 9.1.3.3. Company Financials

- 9.1.3.4. SWOT Analysis

- 9.1.4 Enstrom Helicopter Corp

- 9.1.4.1. Company Overview

- 9.1.4.2. Products

- 9.1.4.3. Company Financials

- 9.1.4.4. SWOT Analysis

- 9.1.5 MD Helicopters LLC

- 9.1.5.1. Company Overview

- 9.1.5.2. Products

- 9.1.5.3. Company Financials

- 9.1.5.4. SWOT Analysis

- 9.1.6 Kopter Group

- 9.1.6.1. Company Overview

- 9.1.6.2. Products

- 9.1.6.3. Company Financials

- 9.1.6.4. SWOT Analysis

- 9.1.7 Robinson Helicopter Compan

- 9.1.7.1. Company Overview

- 9.1.7.2. Products

- 9.1.7.3. Company Financials

- 9.1.7.4. SWOT Analysis

- 9.1.8 Leonardo S p A

- 9.1.8.1. Company Overview

- 9.1.8.2. Products

- 9.1.8.3. Company Financials

- 9.1.8.4. SWOT Analysis

- 9.1.9 The Boeing Company

- 9.1.9.1. Company Overview

- 9.1.9.2. Products

- 9.1.9.3. Company Financials

- 9.1.9.4. SWOT Analysis

- 9.1.1 Textron Inc

- 9.2. Market Entropy

- 9.2.1 Company's Key Areas Served

- 9.2.2 Recent Developments

- 9.3. Company Market Share Analysis 2025

- 9.3.1 Top 5 Companies Market Share Analysis

- 9.3.2 Top 3 Companies Market Share Analysis

- 9.4. List of Potential Customers

- 10. Research Methodology

List of Figures

- Figure 1: North America Helicopters Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Helicopters Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Helicopters Industry Revenue Million Forecast, by Engine 2020 & 2033

- Table 2: North America Helicopters Industry Revenue Million Forecast, by End-user 2020 & 2033

- Table 3: North America Helicopters Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: North America Helicopters Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: North America Helicopters Industry Revenue Million Forecast, by Engine 2020 & 2033

- Table 6: North America Helicopters Industry Revenue Million Forecast, by End-user 2020 & 2033

- Table 7: North America Helicopters Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: North America Helicopters Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: North America Helicopters Industry Revenue Million Forecast, by Engine 2020 & 2033

- Table 10: North America Helicopters Industry Revenue Million Forecast, by End-user 2020 & 2033

- Table 11: North America Helicopters Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: North America Helicopters Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Helicopters Industry?

The projected CAGR is approximately 6.72%.

2. Which companies are prominent players in the North America Helicopters Industry?

Key companies in the market include Textron Inc, Lockheed Martin Corporation, Airbus SE, Enstrom Helicopter Corp, MD Helicopters LLC, Kopter Group, Robinson Helicopter Compan, Leonardo S p A, The Boeing Company.

3. What are the main segments of the North America Helicopters Industry?

The market segments include Engine, End-user, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.85 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Military End-user Segment to Dominate the Market in Terms of Revenue.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Helicopters Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Helicopters Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Helicopters Industry?

To stay informed about further developments, trends, and reports in the North America Helicopters Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence