Key Insights

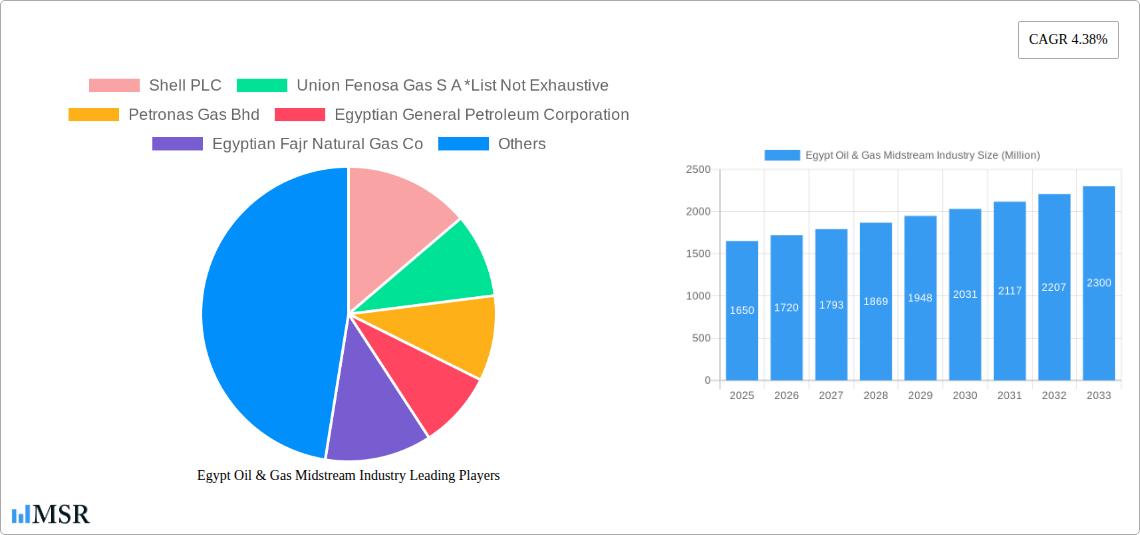

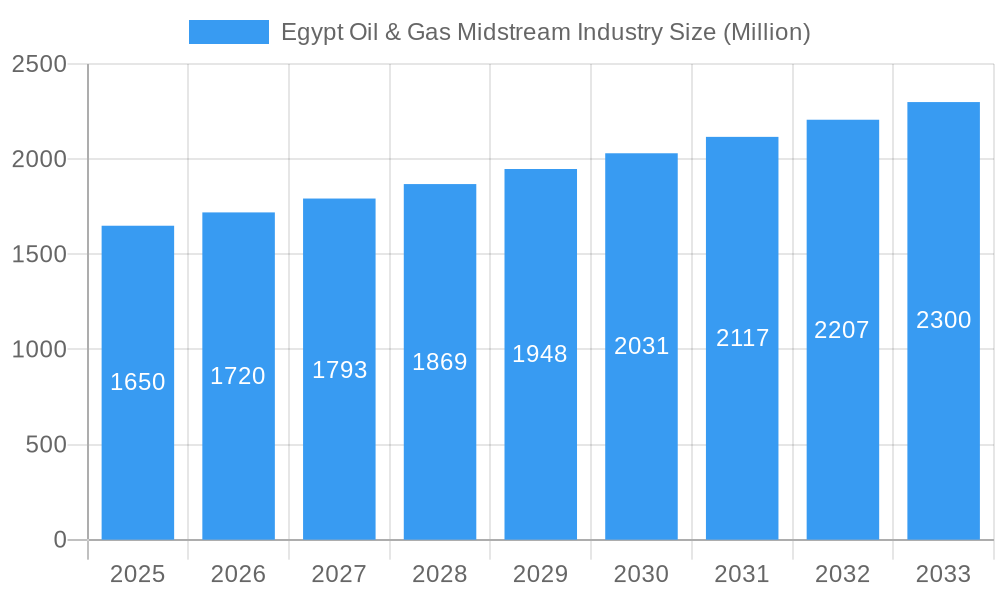

The Egypt Oil & Gas Midstream industry, valued at $1.65 billion in 2025, is projected to experience robust growth, driven by increasing domestic energy demand and strategic investments in infrastructure development. A Compound Annual Growth Rate (CAGR) of 4.38% from 2025 to 2033 indicates a significant expansion of the market, reaching an estimated value of approximately $2.4 billion by 2033. This growth is fueled by several key factors. Firstly, Egypt's ongoing efforts to diversify its energy sources and enhance energy security are attracting considerable foreign investment. Secondly, the development of new LNG terminals and pipelines is bolstering transportation and storage capabilities, improving efficiency and creating new market opportunities. Finally, the government's supportive regulatory environment and focus on attracting private sector participation are further propelling the sector's progress. Key players like Shell, BP, and Eni, alongside local companies, are actively contributing to this expansion.

Egypt Oil & Gas Midstream Industry Market Size (In Billion)

However, challenges remain. Fluctuations in global oil and gas prices can impact investment decisions and profitability. Furthermore, ensuring the sustainable and environmentally responsible development of midstream infrastructure requires careful planning and adherence to strict environmental regulations. The segments contributing most significantly to the market growth are likely LNG terminals, driven by rising LNG import and export activities, followed by transportation and storage, as both are essential for the efficient movement and management of oil and gas resources. The strategic positioning of Egypt as a regional energy hub, coupled with ongoing infrastructure improvements, suggests a positive outlook for the long-term growth of the Egypt Oil & Gas Midstream industry.

Egypt Oil & Gas Midstream Industry Company Market Share

Egypt Oil & Gas Midstream Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Egypt Oil & Gas Midstream Industry, covering market dynamics, key segments, leading players, and future growth prospects. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. This report is essential for industry stakeholders, investors, and strategic decision-makers seeking actionable insights into this dynamic market. The report uses Million as a unit for all values.

Egypt Oil & Gas Midstream Industry Market Concentration & Dynamics

This section assesses the competitive landscape, innovation, regulatory environment, and market trends within the Egyptian oil and gas midstream sector. We analyze market share distribution, M&A activity, and the influence of substitute products on market dynamics.

Market Concentration: The Egyptian midstream sector exhibits a moderate level of concentration, with key players such as Shell PLC, Eni S.p.A, BP plc, and the Egyptian General Petroleum Corporation holding significant market share. Precise market share figures for each company are unavailable (xx%) but are presented in detail within the full report.

Innovation Ecosystem: Innovation is driven by both domestic and international companies focusing on improving efficiency in LNG terminals, pipeline transportation, and storage facilities. Investment in digital technologies and automation is increasing.

Regulatory Framework: The Egyptian government plays a significant role in regulating the midstream sector, impacting infrastructure development, pricing, and environmental considerations. The regulatory landscape is constantly evolving, presenting both opportunities and challenges for market participants.

Substitute Products: The midstream sector faces competition from alternative energy sources, primarily renewable energy, driving a need for efficiency improvements and diversification within the sector.

End-User Trends: The rising energy demand within Egypt, coupled with regional partnerships, is driving significant growth in midstream infrastructure development.

M&A Activity: The number of M&A deals in the Egyptian oil & gas midstream sector over the historical period (2019-2024) averaged approximately xx deals per year. The full report details the specific deals, contributing companies and financial details.

Egypt Oil & Gas Midstream Industry Industry Insights & Trends

This section delves into market size, growth drivers, technological advancements, and evolving consumer behaviour impacting the Egyptian oil & gas midstream market. The market size in 2025 is estimated at USD xx Million, with a Compound Annual Growth Rate (CAGR) projected at xx% from 2025 to 2033. Growth is primarily driven by increased domestic energy consumption, regional collaborations, and investments in infrastructure projects. Technological disruptions, such as the adoption of digital technologies for pipeline monitoring and improved storage solutions, are significantly impacting operational efficiency and cost reduction.

Key Markets & Segments Leading Egypt Oil & Gas Midstream Industry

This section identifies the dominant segments within the Egyptian midstream industry: LNG Terminals, Transportation, and Storage.

LNG Terminals: Overview

- Dominant Region: The Red Sea region is currently the most important for LNG terminals, with the potential for growth in other coastal areas.

- Growth Drivers: Increased LNG imports, strategic partnerships with neighboring countries, and government investments in port infrastructure.

Transportation: Overview

- Dominant Mode: Pipelines remain the dominant mode of transportation, while road and rail transport play secondary roles.

- Growth Drivers: Expansion of existing pipeline networks and the construction of new pipelines to connect new gas fields and processing facilities.

Storage: Overview

- Dominant Location: Existing storage facilities are concentrated near major consumption centers and import terminals. The recent announcement of a new crude oil storage area in El-Tebbin suggests a geographic shift.

- Growth Drivers: Increased domestic production, the need for strategic reserves, and the growth of LNG imports.

Detailed analysis of each segment's dominance and drivers is included in the full report.

Egypt Oil & Gas Midstream Industry Product Developments

Recent product innovations include advanced pipeline monitoring systems, improved LNG regasification technologies, and enhanced storage solutions designed to improve efficiency, reduce environmental impact, and increase capacity. These advancements are enhancing the competitiveness of the Egyptian midstream sector on a global scale.

Challenges in the Egypt Oil & Gas Midstream Industry Market

The Egyptian midstream sector faces challenges including regulatory complexities, the need for continuous infrastructure investment (estimated at USD xx Million annually), and competition from alternative energy sources impacting long-term growth. Supply chain disruptions and geopolitical instability also pose significant risks.

Forces Driving Egypt Oil & Gas Midstream Industry Growth

Key growth drivers include increasing domestic energy demand, regional energy partnerships (such as the agreement with Jordan), government support for infrastructure development, and technological advancements improving efficiency and safety. These factors are crucial for sustainable growth and expansion.

Long-Term Growth Catalysts in the Egypt Oil & Gas Midstream Industry

Long-term growth is projected to be fueled by strategic partnerships, infrastructure investments, and technological innovation. The exploration and development of new gas fields will also contribute substantially to long-term growth.

Emerging Opportunities in Egypt Oil & Gas Midstream Industry

Emerging opportunities include expansion into renewable natural gas (RNG) integration, the development of carbon capture and storage (CCS) technologies, and increased regional cooperation to build new trans-border pipelines. These trends represent considerable potential for future growth.

Leading Players in the Egypt Oil & Gas Midstream Industry Sector

- Shell PLC

- Union Fenosa Gas S.A

- Petronas Gas Bhd

- Egyptian General Petroleum Corporation

- Egyptian Fajr Natural Gas Co

- Eni S.p.A

- Egyptian Natural Gas Holding Company

- BP plc

- Spanish Egyptian Gas Company

Key Milestones in Egypt Oil & Gas Midstream Industry Industry

- June 2023: Egypt and Jordan collaborate on utilizing the FSRU at Aqaba port, boosting LNG handling capacity and regional energy cooperation.

- July 2022: The Egyptian petroleum ministry announces plans for a new crude oil storage area in El-Tebbin, enhancing storage capacity and distribution efficiency.

Strategic Outlook for Egypt Oil & Gas Midstream Industry Market

The Egyptian oil & gas midstream sector is poised for significant growth driven by increasing domestic demand, regional integration, and technological advancements. Strategic partnerships and infrastructure investment will be crucial for capitalizing on the vast growth potential. The market is expected to continue expanding, creating opportunities for both domestic and international players.

Egypt Oil & Gas Midstream Industry Segmentation

-

1. Transportation

-

1.1. Overview

- 1.1.1. Existing Infrastructure

- 1.1.2. Projects in pipeline

- 1.1.3. Upcoming projects

-

1.1. Overview

-

2. Storage

-

2.1. Overview

- 2.1.1. Existing Infrastructure

- 2.1.2. Projects in pipeline

- 2.1.3. Upcoming projects

-

2.1. Overview

-

3. LNG Terminals

-

3.1. Overview

- 3.1.1. Existing Infrastructure

- 3.1.2. Projects in pipeline

- 3.1.3. Upcoming projects

-

3.1. Overview

Egypt Oil & Gas Midstream Industry Segmentation By Geography

- 1. Egypt

Egypt Oil & Gas Midstream Industry Regional Market Share

Geographic Coverage of Egypt Oil & Gas Midstream Industry

Egypt Oil & Gas Midstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Transportation

- 5.1.1. Overview

- 5.1.1.1. Existing Infrastructure

- 5.1.1.2. Projects in pipeline

- 5.1.1.3. Upcoming projects

- 5.1.1. Overview

- 5.2. Market Analysis, Insights and Forecast - by Storage

- 5.2.1. Overview

- 5.2.1.1. Existing Infrastructure

- 5.2.1.2. Projects in pipeline

- 5.2.1.3. Upcoming projects

- 5.2.1. Overview

- 5.3. Market Analysis, Insights and Forecast - by LNG Terminals

- 5.3.1. Overview

- 5.3.1.1. Existing Infrastructure

- 5.3.1.2. Projects in pipeline

- 5.3.1.3. Upcoming projects

- 5.3.1. Overview

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Egypt

- 5.1. Market Analysis, Insights and Forecast - by Transportation

- 6. Egypt Oil & Gas Midstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Transportation

- 6.1.1. Overview

- 6.1.1.1. Existing Infrastructure

- 6.1.1.2. Projects in pipeline

- 6.1.1.3. Upcoming projects

- 6.1.1. Overview

- 6.2. Market Analysis, Insights and Forecast - by Storage

- 6.2.1. Overview

- 6.2.1.1. Existing Infrastructure

- 6.2.1.2. Projects in pipeline

- 6.2.1.3. Upcoming projects

- 6.2.1. Overview

- 6.3. Market Analysis, Insights and Forecast - by LNG Terminals

- 6.3.1. Overview

- 6.3.1.1. Existing Infrastructure

- 6.3.1.2. Projects in pipeline

- 6.3.1.3. Upcoming projects

- 6.3.1. Overview

- 6.1. Market Analysis, Insights and Forecast - by Transportation

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Union Fenosa Gas S A *List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Petronas Gas Bhd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Egyptian General Petroleum Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Egyptian Fajr Natural Gas Co

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Eni S p A

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Egyptian Natural Gas Holding Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 BP p l c

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Spanish Egyptian Gas Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Shell PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Egypt Oil & Gas Midstream Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Egypt Oil & Gas Midstream Industry Share (%) by Company 2025

List of Tables

- Table 1: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Transportation 2020 & 2033

- Table 2: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Storage 2020 & 2033

- Table 3: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by LNG Terminals 2020 & 2033

- Table 4: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Transportation 2020 & 2033

- Table 6: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Storage 2020 & 2033

- Table 7: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by LNG Terminals 2020 & 2033

- Table 8: Egypt Oil & Gas Midstream Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Egypt Oil & Gas Midstream Industry?

The projected CAGR is approximately 4.38%.

2. Which companies are prominent players in the Egypt Oil & Gas Midstream Industry?

Key companies in the market include Shell PLC, Union Fenosa Gas S A *List Not Exhaustive, Petronas Gas Bhd, Egyptian General Petroleum Corporation, Egyptian Fajr Natural Gas Co, Eni S p A, Egyptian Natural Gas Holding Company, BP p l c, Spanish Egyptian Gas Company.

3. What are the main segments of the Egypt Oil & Gas Midstream Industry?

The market segments include Transportation, Storage, LNG Terminals.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.65 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing investment in the Midstream Sector4.; Increasing Production of Oil and Natural Gas.

6. What are the notable trends driving market growth?

Transportation Sector to Witness Growth.

7. Are there any restraints impacting market growth?

4.; Inadequate Infrastructure in the Country.

8. Can you provide examples of recent developments in the market?

In June 2023, Egypt and Jordan entered into a collaboration agreement that allows the North African nation to use the floating storage regasification unit (FSRU) at the Sheikh Sabah port in Aqaba. FSRU terminals are crucial in the liquefied natural gas value chain, forming the interface between LNG carriers and the local gas supply infrastructure. As part of the agreement, the Jordanian side will receive LNG from Egypt and pump back some of the gas through transborder pipelines to the country if needed.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Egypt Oil & Gas Midstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Egypt Oil & Gas Midstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Egypt Oil & Gas Midstream Industry?

To stay informed about further developments, trends, and reports in the Egypt Oil & Gas Midstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence