Key Insights

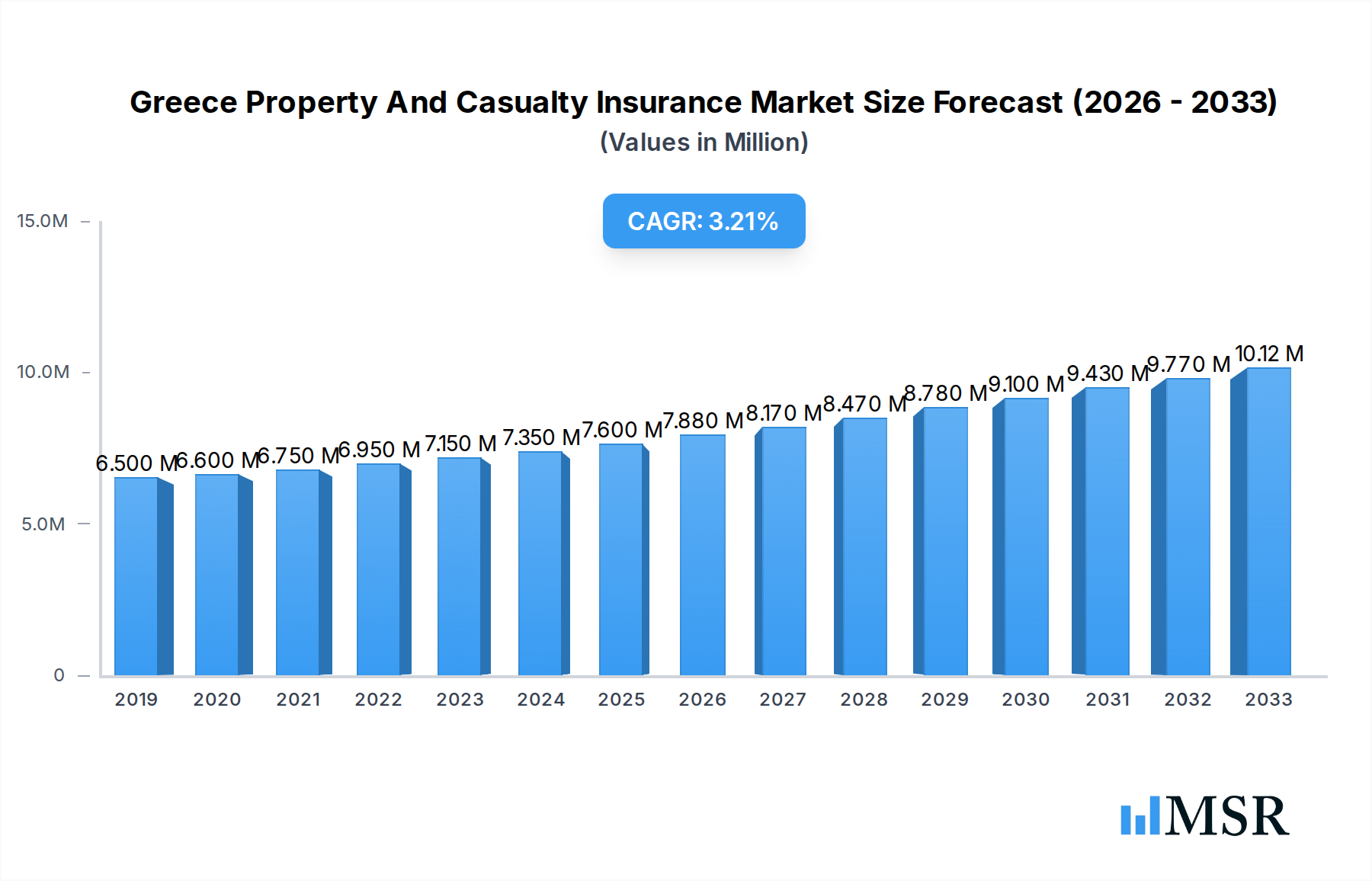

The Greece Property and Casualty (P&C) Insurance Market is poised for steady growth, projected to reach 7.60 million by 2025 and expand at a Compound Annual Growth Rate (CAGR) of 3.67% through to 2033. This expansion is underpinned by a confluence of factors, primarily driven by increasing consumer awareness of insurance as a crucial financial protection tool against unforeseen events. Growing disposable incomes in Greece, especially post-economic recovery, are enabling households and businesses to invest more in comprehensive P&C coverage. Furthermore, the increasing complexity of risks, from natural disasters like floods and wildfires to cyber threats, is compelling individuals and corporations to seek robust insurance solutions. The Motor insurance segment, a traditional backbone of the P&C market, continues to benefit from mandatory vehicle insurance regulations and a large vehicle parc. The Home insurance segment is also witnessing a surge in demand, fueled by a growing emphasis on safeguarding valuable assets and rising property ownership. The distribution landscape is diverse, with direct channels gaining traction due to digital advancements, while agencies and brokers continue to play a significant role in providing tailored advice and specialized coverage.

Greece Property And Casualty Insurance Market Market Size (In Million)

Several trends are shaping the dynamism of the Greek P&C insurance sector. The digitalization of insurance services is a paramount trend, with insurers heavily investing in online platforms, mobile applications, and AI-powered customer service to enhance user experience and streamline claims processing. This digital transformation is crucial for engaging younger demographics and improving operational efficiency. Emerging risks, such as climate change-related events and the growing cyber threat landscape, are prompting insurers to develop innovative products and policies. For instance, specialized coverage for renewable energy infrastructure and cybersecurity insurance are gaining prominence. Insurers are also focusing on personalized pricing models and value-added services to foster customer loyalty and differentiate themselves in a competitive market. However, certain restraints could impact the market’s full potential. Economic volatility, though improving, can still affect premium affordability for some segments of the population. Regulatory changes, while generally aimed at market stability, can introduce compliance challenges and necessitate strategic adjustments for insurance providers. Intense competition among established players and the potential entry of new, digitally-native insurers also put pressure on profit margins, requiring continuous innovation and cost optimization.

Greece Property And Casualty Insurance Market Company Market Share

This in-depth report provides a definitive analysis of the Greece Property And Casualty Insurance Market, offering critical insights into market dynamics, growth drivers, emerging trends, and competitive landscapes. Spanning the Historical Period (2019–2024), Base Year (2025), Estimated Year (2025), and an extensive Forecast Period (2025–2033), this study is an indispensable resource for insurers, reinsurers, brokers, regulators, investors, and industry stakeholders seeking to capitalize on opportunities within the Greek P&C insurance sector. Leveraging a robust methodology, the report dissects market concentration, identifies key growth catalysts, and forecasts future market performance, making it essential for strategic planning and decision-making.

Greece Property And Casualty Insurance Market Market Concentration & Dynamics

The Greece Property And Casualty Insurance Market exhibits a dynamic interplay of established players and evolving market forces, influencing its concentration and competitive intensity. Key players such as Alpha Insurance Company, AXA Greece, Groupama Phoenix, Allianz Greece, Ergo Insurance, HDI-Gerling Greece Insurance, NN Hellas, Piraeus Insurance, Eurobank Insurance, MetLife Greece Insurance Company, Ethniki Hellenic General Insurance Company, Interamerican Greece, and Zurich Insurance are central to the market's structure. While not exhaustive, this list represents a significant portion of market share. The market is characterized by a moderate level of concentration, with a few dominant insurers holding substantial sway, yet a growing number of agile and specialized players contribute to a vibrant ecosystem. Innovation is increasingly driven by digitalization and the adoption of InsurTech solutions, aiming to enhance customer experience and operational efficiency. Regulatory frameworks, particularly those stemming from the European Union, play a crucial role in shaping market practices and consumer protection. The identification of substitute products and the evolving end-user trends, such as a growing demand for tailored coverage and digital-first interaction, are continuously reshaping product development and distribution strategies. Merger and acquisition (M&A) activities, exemplified by the December 2022 integration efforts between European Reliance and Allianz Greece, and the February 2022 acquisition of Ethniki Hellenic General Insurance Company by CVC Capital Partners, signal a trend towards consolidation and strategic partnerships aimed at expanding market reach and operational synergies. The number of significant M&A deals in the historical period is estimated at x indicating strategic maneuvering for competitive advantage.

Greece Property And Casualty Insurance Market Industry Insights & Trends

The Greece Property And Casualty Insurance Market is poised for significant expansion, driven by a confluence of economic recovery, increasing disposable incomes, and a heightened awareness of risk mitigation among consumers and businesses. The market size for property and casualty insurance in Greece is projected to reach approximately €XX Billion by the end of 2025, exhibiting a Compound Annual Growth Rate (CAGR) of around X.XX% during the forecast period. This growth is underpinned by several key factors. Firstly, ongoing infrastructure development and a robust construction sector necessitate comprehensive property insurance solutions. Secondly, motor insurance remains a dominant segment, driven by a relatively large vehicle fleet and evolving regulatory mandates for coverage. Thirdly, a growing trend towards digitalization is transforming the distribution landscape, with a noticeable shift towards direct online sales and the increased utilization of digital platforms by traditional intermediaries. The market is witnessing a surge in demand for specialized insurance products, including cyber insurance and parametric insurance, catering to emerging risks faced by businesses. Furthermore, government initiatives promoting financial literacy and insurance penetration are expected to further bolster market growth. The increasing adoption of advanced analytics and artificial intelligence by insurers is enabling more accurate risk assessment, personalized pricing, and streamlined claims processing, thereby enhancing customer satisfaction and operational efficiency. The economic stability and forecast GDP growth of X% for Greece during the forecast period will further empower consumers and businesses to invest in adequate insurance coverage. The adoption of IoT devices in homes and vehicles is also paving the way for usage-based insurance models and preventative risk management strategies.

Key Markets & Segments Leading Greece Property And Casualty Insurance Market

The Greece Property And Casualty Insurance Market is led by distinct segments and distribution channels, each contributing to the overall market dynamics.

Insurance Type Dominance:

- Motor Insurance: This segment consistently holds the largest market share, driven by the high penetration of vehicles and mandatory insurance requirements. Factors such as increasing vehicle sales, a recovering automotive sector, and the introduction of telematics-based insurance policies contribute to its sustained dominance. The market for motor insurance is estimated to be worth €X Billion in 2025.

- Home Insurance: Experiencing steady growth, home insurance is gaining traction due to increased awareness of property protection against natural disasters, theft, and other perils. Government incentives for energy-efficient renovations and a recovering real estate market also contribute to its expansion. The home insurance market is projected to reach €XXX Million by 2025.

- Other In (Commercial, Liability, etc.): This broad category encompasses commercial property insurance, liability insurance, marine insurance, and other specialized coverages. Growth in this segment is closely tied to the health of the Greek economy, particularly the tourism and shipping industries, as well as the expansion of small and medium-sized enterprises (SMEs). The "Other In" segment is forecast to grow at a CAGR of X.XX%.

Distribution Channel Dominance:

- Agency: Traditional insurance agents and brokers remain a significant distribution channel, especially for complex products and for customers seeking personalized advice. Their role is evolving with digital integration, offering hybrid solutions. The agency channel is estimated to account for XX% of the market.

- Direct: The direct-to-consumer (DTC) channel, encompassing online portals and mobile applications, is experiencing rapid growth. Insurers are investing heavily in user-friendly digital platforms to attract and retain customers seeking convenience and competitive pricing. This channel is expected to capture XX% of the market by 2025.

- Brokers: Independent brokers play a crucial role in serving the commercial and corporate segments, offering specialized expertise and tailored solutions. Their deep market knowledge and ability to negotiate favorable terms are highly valued.

- Other Distribution Channels: This includes partnerships with financial institutions, affinity groups, and aggregators, which are increasingly being leveraged to reach diverse customer segments.

The dominance of these segments is further bolstered by economic factors such as GDP growth of X% in 2025, a stable interest rate environment, and supportive regulatory policies that encourage insurance penetration.

Greece Property And Casualty Insurance Market Product Developments

Product development in the Greece Property And Casualty Insurance Market is increasingly focused on innovation to meet evolving customer needs and address emerging risks. Insurers are actively developing modular and customizable policies, allowing policyholders to tailor coverage to their specific requirements. The integration of InsurTech solutions is leading to the introduction of sophisticated digital tools for policy management, claims processing, and risk assessment. For instance, AI-powered claims automation and fraud detection systems are enhancing efficiency and accuracy. There is a growing emphasis on preventive insurance solutions, leveraging IoT devices and data analytics to identify potential hazards and mitigate risks before they lead to claims. This includes smart home technology integration for property insurance and telematics for motor insurance, offering personalized risk profiles and potential premium reductions. The market is also witnessing the development of parametric insurance products, which trigger payouts based on pre-defined event parameters, such as weather conditions, offering faster and more transparent claims settlements. The relevance of these product innovations lies in their ability to enhance customer experience, improve risk management, and create a competitive edge in a dynamic market.

Challenges in the Greece Property And Casualty Insurance Market Market

The Greece Property And Casualty Insurance Market faces several significant challenges that could impede its growth trajectory. Regulatory hurdles, while essential for consumer protection, can sometimes lead to increased compliance costs and slower product innovation cycles. The dynamic nature of the European regulatory landscape necessitates continuous adaptation and investment in compliance infrastructure. Supply chain issues, particularly in relation to construction materials and vehicle repair, can impact claims costs and settlement times, affecting profitability and customer satisfaction. Furthermore, intense competitive pressures from both established domestic insurers and international players, coupled with the rise of InsurTech startups, demand continuous adaptation and investment in digitalization and customer-centric strategies. The market also contends with a persistent challenge of low insurance penetration in certain segments, requiring concerted efforts in consumer education and product accessibility. Quantifiable impacts include an estimated increase of X% in operational costs due to regulatory compliance and an average delay of X days in claims settlement due to supply chain disruptions in the past year.

Forces Driving Greece Property And Casualty Insurance Market Growth

Several key forces are driving the robust growth of the Greece Property And Casualty Insurance Market. A recovering economy, characterized by projected GDP growth of X% in 2025, is increasing disposable incomes and empowering both individuals and businesses to invest more in insurance coverage. Enhanced awareness of risk management, particularly in the wake of climate change-related events and evolving geopolitical landscapes, is prompting greater demand for comprehensive protection. Technological advancements, including the widespread adoption of InsurTech solutions, are revolutionizing product development, distribution, and claims processing, leading to more efficient and customer-friendly services. Regulatory frameworks, such as those promoting digitalization and consumer protection, are also fostering a more transparent and competitive market environment. Furthermore, government initiatives aimed at supporting key industries like tourism and shipping indirectly boost the demand for relevant insurance products. The increasing digitalization of the Greek economy is creating new avenues for insurance distribution and product innovation, such as embedded insurance within e-commerce platforms.

Challenges in the Greece Property And Casualty Insurance Market Market

While growth is evident, the Greece Property And Casualty Insurance Market must navigate specific long-term challenges to sustain its upward trajectory. Persistent economic uncertainties, though abating, can still lead to fluctuations in consumer spending on non-essential services like insurance. Evolving climate patterns present an ongoing challenge, requiring insurers to adapt their risk models and pricing strategies to account for increasing natural disaster frequency and severity. The digital divide, where certain demographics or regions have limited access to digital channels, poses a challenge for widespread adoption of online insurance solutions. Maintaining profitability in a competitive market while investing in technological advancements and adapting to new regulatory requirements demands careful strategic planning and efficient operational management. The aging population in Greece also presents unique insurance needs that require specialized product development and outreach strategies.

Emerging Opportunities in Greece Property And Casualty Insurance Market

The Greece Property And Casualty Insurance Market is ripe with emerging opportunities poised to shape its future. The burgeoning renewable energy sector presents a significant opportunity for specialized insurance products covering solar farms, wind turbines, and related infrastructure. The increasing adoption of electric vehicles (EVs) is creating demand for tailored motor insurance policies that account for battery life, charging infrastructure, and EV-specific repair requirements. The growth of the Greek tourism industry, a cornerstone of its economy, opens avenues for specialized travel insurance, event cancellation coverage, and hospitality-focused property insurance. The expanding gig economy and freelance workforce necessitate flexible and on-demand insurance solutions for various occupational risks. Furthermore, the continued digitalization of businesses across all sectors creates a growing market for cyber insurance and business interruption coverage, addressing the increasing threat of digital vulnerabilities. The potential for parametric insurance, triggered by specific weather events or other defined parameters, offers a promising avenue for faster claims settlement and enhanced customer experience, particularly in the context of climate change.

Leading Players in the Greece Property And Casualty Insurance Market Sector

The Greece Property And Casualty Insurance Market is characterized by the presence of several prominent players, including:

- Alpha Insurance Company

- AXA Greece

- Groupama Phoenix

- Allianz Greece

- Ergo Insurance

- HDI-Gerling Greece Insurance

- NN Hellas

- Piraeus Insurance

- Eurobank Insurance

- MetLife Greece Insurance Company

- Ethniki Hellenic General Insurance Company

- Interamerican Greece

- Zurich Insurance

Key Milestones in Greece Property And Casualty Insurance Market Industry

- December 2022: European Reliance and Allianz Greece announced the formation of an Executive Committee (ExCom) to oversee their joint expansion journey and facilitate the effective integration of the two companies. This strategic move signals a concerted effort towards market consolidation and enhanced operational synergy, impacting competitive dynamics and potentially leading to new product offerings or service enhancements.

- February 2022: The European Commission unconditionally cleared the acquisition of Ethniki Hellenic General Insurance Company S.A. of Greece by CVC Capital Partners SICAV FIS S.A. of Luxemburg. Ethniki offers life and non-life insurance services, insurance distribution, and reinsurance services in Cyprus, Greece, and Romania. CVC and its subsidiaries manage investment funds and platforms and control many companies, including the Hellenic Healthcare Group, which offers private hospital services in Cyprus and Greece. This acquisition represents a significant consolidation in the Greek insurance market, bringing substantial capital and strategic expertise, potentially leading to enhanced service offerings and expanded market reach for Ethniki.

Strategic Outlook for Greece Property And Casualty Insurance Market Market

The strategic outlook for the Greece Property And Casualty Insurance Market is marked by a strong emphasis on digital transformation, product innovation, and strategic partnerships. Insurers that prioritize customer-centricity, leveraging data analytics and InsurTech to offer personalized and seamless experiences, will be best positioned for success. The growing demand for specialized insurance products, driven by emerging risks such as cyber threats and climate change, presents significant growth avenues. Strategic collaborations with technology providers and other industry players will be crucial for developing innovative solutions and expanding market reach. Furthermore, a focus on enhancing insurance penetration through consumer education and accessible distribution channels will be vital for unlocking the full potential of the Greek market. The market is expected to witness continued consolidation and M&A activity as companies seek to achieve economies of scale and enhance their competitive standing. Investments in cybersecurity and sustainable underwriting practices will also be critical for long-term resilience and profitability.

Greece Property And Casualty Insurance Market Segmentation

-

1. Insurance type

- 1.1. Home

- 1.2. Motor

- 1.3. Other In

-

2. Distribution Channel

- 2.1. Direct

- 2.2. Agency

- 2.3. Brokers

- 2.4. Other Distribution Channels

Greece Property And Casualty Insurance Market Segmentation By Geography

- 1. Greece

Greece Property And Casualty Insurance Market Regional Market Share

Geographic Coverage of Greece Property And Casualty Insurance Market

Greece Property And Casualty Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.67% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 5.1.1. Home

- 5.1.2. Motor

- 5.1.3. Other In

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Brokers

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Greece

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 6. Greece Property And Casualty Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance type

- 6.1.1. Home

- 6.1.2. Motor

- 6.1.3. Other In

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Brokers

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Insurance type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Alpha Insurance Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 AXA Greece

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Groupama Phoenix

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Allianz Greece

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ergo Insurance

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 HDI-Gerling Greece Insurance

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 NN Hellas

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Piraeus Insurance

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Eurobank Insurance

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 MetLife Greece Insurance Company**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Ethniki Hellenic General Insurance Company

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Interamerican Greece

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Zurich Insurance

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Alpha Insurance Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Greece Property And Casualty Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Greece Property And Casualty Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: Greece Property And Casualty Insurance Market Revenue Million Forecast, by Insurance type 2020 & 2033

- Table 2: Greece Property And Casualty Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Greece Property And Casualty Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Greece Property And Casualty Insurance Market Revenue Million Forecast, by Insurance type 2020 & 2033

- Table 5: Greece Property And Casualty Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Greece Property And Casualty Insurance Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Greece Property And Casualty Insurance Market?

The projected CAGR is approximately 3.67%.

2. Which companies are prominent players in the Greece Property And Casualty Insurance Market?

Key companies in the market include Alpha Insurance Company, AXA Greece, Groupama Phoenix, Allianz Greece, Ergo Insurance, HDI-Gerling Greece Insurance, NN Hellas, Piraeus Insurance, Eurobank Insurance, MetLife Greece Insurance Company**List Not Exhaustive, Ethniki Hellenic General Insurance Company, Interamerican Greece, Zurich Insurance.

3. What are the main segments of the Greece Property And Casualty Insurance Market?

The market segments include Insurance type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.60 Million as of 2022.

5. What are some drivers contributing to market growth?

Digitalization is Driving the Market.

6. What are the notable trends driving market growth?

Technological Advancements are Driving the Market.

7. Are there any restraints impacting market growth?

Economic Disparities are Restraining the Market.

8. Can you provide examples of recent developments in the market?

December 2022: European Reliance and Allianz Greece announced the formation of an Executive Committee (ExCom) to oversee their joint expansion journey and facilitate the effective integration of the two companies. The composition of the ExCom members has been carefully chosen with the primary goal of ensuring a seamless integration process..

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Greece Property And Casualty Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Greece Property And Casualty Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Greece Property And Casualty Insurance Market?

To stay informed about further developments, trends, and reports in the Greece Property And Casualty Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence