Key Insights

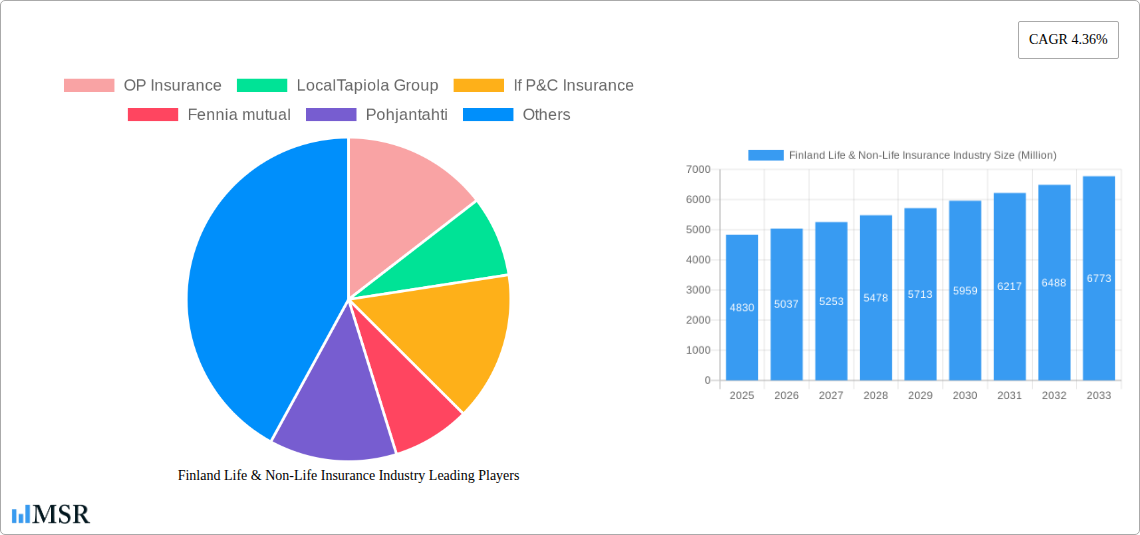

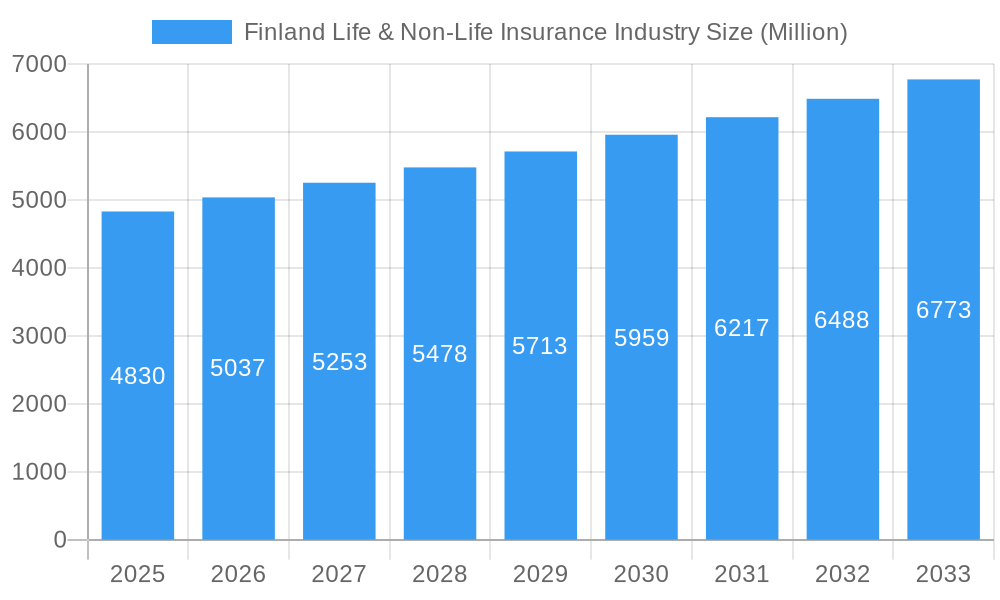

The Finland Life & Non-Life Insurance Industry is poised for steady growth, with a current market size estimated at USD 4.83 billion and a projected Compound Annual Growth Rate (CAGR) of 4.36% for the forecast period of 2025-2033. This growth is driven by an increasing demand for comprehensive financial security solutions among individuals and businesses, coupled with evolving consumer preferences towards digital channels and personalized offerings. The life insurance segment, encompassing both individual and group policies, is expected to remain a significant contributor, driven by factors such as an aging population, rising disposable incomes, and greater awareness of long-term financial planning needs. Simultaneously, the non-life insurance sector, including crucial lines like motor and home insurance, is experiencing a sustained demand influenced by stringent regulations, increasing vehicle ownership, and the growing value of property assets. The industry's expansion is further bolstered by robust economic conditions in Finland and supportive government policies aimed at enhancing financial inclusion and consumer protection.

Finland Life & Non-Life Insurance Industry Market Size (In Billion)

Key trends shaping the Finland insurance landscape include a significant shift towards online distribution channels, enabling greater accessibility and convenience for consumers. Insurers are investing heavily in digital platforms, mobile applications, and artificial intelligence to streamline underwriting, claims processing, and customer service. The agency channel, while still relevant, is adapting to integrate digital tools and provide more value-added advisory services. Furthermore, there's a growing emphasis on personalized insurance products tailored to specific customer needs and risk profiles, moving away from one-size-fits-all solutions. Emerging opportunities lie in parametric insurance and other innovative products addressing emerging risks like climate change and cyber threats. However, the market also faces certain restraints, including intense competition among established players and new entrants, as well as regulatory complexities and evolving compliance requirements that necessitate continuous adaptation by insurance providers. Navigating these challenges while capitalizing on growth opportunities will be critical for sustained success in the Finnish insurance market.

Finland Life & Non-Life Insurance Industry Company Market Share

Dive deep into the dynamic Finland life and non-life insurance industry with this in-depth market research report. Covering the historical period of 2019-2024 and projecting future growth through 2033 (with a base and estimated year of 2025), this analysis offers actionable insights for insurance companies in Finland, Finnish insurance brokers, and investment opportunities in the Finnish insurance sector. Discover market concentration, regulatory shifts, technological advancements, and emerging trends shaping the Finnish insurance market size and CAGR. This report is an essential guide for stakeholders seeking to understand and capitalize on the evolving Finnish insurance landscape, including digital insurance Finland and insurtech Finland.

Finland Life & Non-Life Insurance Industry Market Concentration & Dynamics

The Finland life and non-life insurance industry exhibits a moderately concentrated market structure, with a few dominant players like OP Insurance and LocalTapiola Group holding significant market share. This concentration is influenced by a robust regulatory framework overseen by Finanssivalvonta (FIN-FSA), which emphasizes consumer protection and financial stability, impacting innovation ecosystems. While competition exists, strategic partnerships and M&A activities in the Finnish insurance sector are key to expanding reach and optimizing operations. The market is characterized by a continuous drive for innovation in product development and digital service delivery. Substitute products, such as alternative investment vehicles or self-insurance, pose a moderate threat, necessitating insurers to offer compelling value propositions. End-user trends are increasingly leaning towards personalized, digitally accessible insurance solutions. Recent M&A activities are geared towards consolidating market position and acquiring technological capabilities to enhance customer experience and operational efficiency.

Finland Life & Non-Life Insurance Industry Industry Insights & Trends

The Finland life and non-life insurance industry is projected for steady growth, driven by an aging population demanding enhanced life insurance solutions and a resilient economy fueling demand for non-life insurance products like motor and home insurance. Technological disruptions are at the forefront, with the adoption of artificial intelligence (AI) and machine learning (ML) revolutionizing underwriting, claims processing, and customer service. Insurtech startups are pushing the boundaries of innovation, offering niche products and leveraging big data analytics for personalized risk assessment. Evolving consumer behaviors are marked by a preference for online channels, demand for transparent pricing, and a growing interest in flexible, on-demand insurance policies. The market size is estimated to reach significant figures by 2033, with a Compound Annual Growth Rate (CAGR) reflecting sustained expansion. The increasing digitalization of public services, as exemplified by the Tietoevry partnership with DigiFinland, is creating new avenues for integrated insurance solutions within broader service ecosystems, particularly in health and social care. Furthermore, the modernization of payment capabilities, as seen with Aktia's adoption of Temenos Payments Hub, signals a trend towards seamless and efficient financial transactions within the insurance value chain.

Key Markets & Segments Leading Finland Life & Non-Life Insurance Industry

Life Insurance

- Individual Life Insurance: This segment is driven by increasing financial literacy, a growing emphasis on long-term financial planning, and a desire for income protection among individuals. Economic stability and disposable income levels are significant contributors to its dominance.

- Group Life Insurance: Employer-sponsored group life insurance remains a crucial segment, boosted by corporate welfare programs and the need for employee benefits. The presence of large corporations and a stable employment market are key drivers.

Non-life Insurance

- Motor Insurance: As a mandatory insurance type and with a high vehicle penetration rate in Finland, motor insurance consistently leads the non-life segment. Economic activity and road usage directly impact this segment's growth.

- Home Insurance: Rising property ownership and the prevalence of natural events requiring coverage contribute to the strength of home insurance. Government initiatives promoting homeownership and disaster preparedness play a vital role.

- Other Non-life Insurance: This broad category includes a range of products such as commercial lines, travel insurance, and liability insurance, all of which are experiencing growth due to increased business activity and evolving consumer needs for specialized protection.

Channel of Distribution

- Direct: The increasing adoption of online platforms and insurer-owned digital channels is driving the growth of direct distribution, offering greater convenience and potentially lower costs for consumers.

- Agency: Traditional insurance agents continue to play a vital role, providing personalized advice and building long-term relationships, particularly for complex insurance needs.

- Banks: Bancassurance remains a significant channel, leveraging the trust and established customer base of financial institutions to offer insurance products.

- Online: The rapid shift towards digital interactions makes online channels a rapidly growing and increasingly important distribution method for both life and non-life insurance products.

- Other Channels of Distribution: This includes partnerships, affinity groups, and brokers, which cater to specific market niches and offer specialized insurance solutions.

Finland Life & Non-Life Insurance Industry Product Developments

Finnish insurance providers are actively innovating in product development, driven by technological advancements and evolving consumer needs. The focus is on creating personalized and flexible insurance solutions. This includes the development of parametric insurance products that trigger payouts based on predefined events, reducing claims processing times. Furthermore, the integration of IoT devices in home and motor insurance is enabling usage-based pricing and proactive risk mitigation. Insurtech collaborations are fostering the creation of digital-first products with seamless online onboarding and policy management, providing a competitive edge in the increasingly digital Finnish insurance market.

Challenges in the Finland Life & Non-Life Insurance Industry Market

The Finland life and non-life insurance industry faces several challenges. Intense competition from both established players and agile insurtech startups can lead to price wars and squeezed profit margins. Evolving regulatory landscapes, while aimed at consumer protection, can introduce compliance burdens and implementation costs. Furthermore, the increasing sophistication of cyber threats necessitates continuous investment in cybersecurity measures to protect sensitive customer data and maintain operational resilience. The management of legacy IT systems can also hinder rapid digital transformation and innovation, impacting the ability to respond quickly to market shifts.

Forces Driving Finland Life & Non-Life Insurance Industry Growth

Several key forces are propelling the Finland life and non-life insurance industry forward. Technological advancements, including AI, big data analytics, and blockchain, are enhancing operational efficiency, improving risk assessment, and enabling personalized customer experiences. Favorable demographic trends, such as an aging population, are increasing the demand for life and health insurance products. A stable economic environment, coupled with government support for digital transformation initiatives, also creates a conducive atmosphere for growth. The increasing awareness among consumers about the importance of financial security and risk management further bolsters demand for insurance coverage.

Challenges in the Finland Life & Non-Life Insurance Industry Market

Long-term growth catalysts in the Finland life and non-life insurance industry are rooted in continuous innovation and strategic market expansion. The ongoing digital transformation, including the adoption of AI for underwriting and claims, and the use of telematics for personalized pricing, will continue to drive efficiency and customer engagement. Partnerships between traditional insurers and insurtechs will foster the development of niche products and new distribution channels. Expanding into underserved segments and exploring cross-border opportunities within the EU will also contribute to sustained growth. Furthermore, a proactive approach to sustainability and ESG (Environmental, Social, and Governance) factors will become increasingly important for long-term success and stakeholder value.

Emerging Opportunities in Finland Life & Non-Life Insurance Industry

Emerging opportunities within the Finland life and non-life insurance industry are abundant and diverse. The growing demand for personalized and on-demand insurance products, driven by evolving consumer preferences, presents a significant avenue for growth. The integration of insurance with other digital services, particularly in health tech and smart homes, offers a chance to embed insurance seamlessly into daily life. The increasing focus on cyber insurance and data privacy protection for businesses and individuals creates a substantial market. Furthermore, the development of sustainable and ESG-aligned insurance products is gaining traction, appealing to a growing segment of socially conscious consumers and investors.

Leading Players in the Finland Life & Non-Life Insurance Industry Sector

OP Insurance LocalTapiola Group If P&C Insurance Fennia mutual Pohjantahti Turva Alandia Group Suomen Vahinkovakuutus Nordea Insurance Finland Suomen Keskinainen Laakevahinkovakuutusyhtio POP Insurance Patient Insurance Company Garantia Nordea Insurance

Key Milestones in Finland Life & Non-Life Insurance Industry Industry

- October 2023: DigiFinland enhanced digital public services with a USD 22.72 million Tietoevry partnership, spanning a seven-year contract period for developing and sustaining digital solutions for social and health care, emergency services, and other pivotal public sector services. This collaboration signifies a move towards integrated digital ecosystems, potentially opening new avenues for health and life insurance product delivery and data utilization.

- October 2023: Temenos announced that Finland’s wealth manager bank Aktia selected Temenos to modernize its payments capabilities, adopting Temenos Payments Hub. This adoption supports the introduction of pan-European instant payments and consolidates payment rail processing onto a single platform, indicating a trend towards streamlined and efficient financial operations that can benefit insurance payment processing and customer transactions.

Strategic Outlook for Finland Life & Non-Life Insurance Industry Market

The strategic outlook for the Finland life and non-life insurance industry is one of significant opportunity driven by digital transformation and evolving consumer demands. Key growth accelerators include the continued adoption of AI and data analytics for hyper-personalization of products and services, enhancing both customer satisfaction and risk management. Investments in insurtech will be crucial for developing innovative solutions, such as embedded insurance and micro-insurance, catering to specific needs and market niches. Expanding distribution channels to include more digital-first platforms and strategic partnerships will broaden market reach. Furthermore, a focus on sustainability and ESG principles will not only align with regulatory expectations but also attract environmentally and socially conscious consumers, positioning companies for long-term resilience and competitive advantage.

Finland Life & Non-Life Insurance Industry Segmentation

-

1. Insurance Type

-

1.1. Life Insurance

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non-life Insurance

- 1.2.1. Home

- 1.2.2. Motor

- 1.2.3. Others

-

1.1. Life Insurance

-

2. Channel of Distribution

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Online

- 2.5. Other Channels of Distribution

Finland Life & Non-Life Insurance Industry Segmentation By Geography

- 1. Finland

Finland Life & Non-Life Insurance Industry Regional Market Share

Geographic Coverage of Finland Life & Non-Life Insurance Industry

Finland Life & Non-Life Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.36% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 5.1.1. Life Insurance

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non-life Insurance

- 5.1.2.1. Home

- 5.1.2.2. Motor

- 5.1.2.3. Others

- 5.1.1. Life Insurance

- 5.2. Market Analysis, Insights and Forecast - by Channel of Distribution

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Online

- 5.2.5. Other Channels of Distribution

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Finland

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6. Finland Life & Non-Life Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6.1.1. Life Insurance

- 6.1.1.1. Individual

- 6.1.1.2. Group

- 6.1.2. Non-life Insurance

- 6.1.2.1. Home

- 6.1.2.2. Motor

- 6.1.2.3. Others

- 6.1.1. Life Insurance

- 6.2. Market Analysis, Insights and Forecast - by Channel of Distribution

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Banks

- 6.2.4. Online

- 6.2.5. Other Channels of Distribution

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 OP Insurance

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 LocalTapiola Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 If P&C Insurance

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Fennia mutual

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Pohjantahti

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Turva

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Alandia Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Suomen Vahinkovakuutus

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Nordea Insurance Finland

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Suomen Keskinainen Laakevahinkovakuutusyhtio

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 POP Insurance

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Patient Insurance Company

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Garantia

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Nordea Insurance**List Not Exhaustive

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.1 OP Insurance

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Finland Life & Non-Life Insurance Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Finland Life & Non-Life Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: Finland Life & Non-Life Insurance Industry Revenue Million Forecast, by Insurance Type 2020 & 2033

- Table 2: Finland Life & Non-Life Insurance Industry Volume Billion Forecast, by Insurance Type 2020 & 2033

- Table 3: Finland Life & Non-Life Insurance Industry Revenue Million Forecast, by Channel of Distribution 2020 & 2033

- Table 4: Finland Life & Non-Life Insurance Industry Volume Billion Forecast, by Channel of Distribution 2020 & 2033

- Table 5: Finland Life & Non-Life Insurance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Finland Life & Non-Life Insurance Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 7: Finland Life & Non-Life Insurance Industry Revenue Million Forecast, by Insurance Type 2020 & 2033

- Table 8: Finland Life & Non-Life Insurance Industry Volume Billion Forecast, by Insurance Type 2020 & 2033

- Table 9: Finland Life & Non-Life Insurance Industry Revenue Million Forecast, by Channel of Distribution 2020 & 2033

- Table 10: Finland Life & Non-Life Insurance Industry Volume Billion Forecast, by Channel of Distribution 2020 & 2033

- Table 11: Finland Life & Non-Life Insurance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Finland Life & Non-Life Insurance Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Finland Life & Non-Life Insurance Industry?

The projected CAGR is approximately 4.36%.

2. Which companies are prominent players in the Finland Life & Non-Life Insurance Industry?

Key companies in the market include OP Insurance, LocalTapiola Group, If P&C Insurance, Fennia mutual, Pohjantahti, Turva, Alandia Group, Suomen Vahinkovakuutus, Nordea Insurance Finland, Suomen Keskinainen Laakevahinkovakuutusyhtio, POP Insurance, Patient Insurance Company, Garantia, Nordea Insurance**List Not Exhaustive.

3. What are the main segments of the Finland Life & Non-Life Insurance Industry?

The market segments include Insurance Type, Channel of Distribution.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.83 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth of Insurtech Partnerships.

6. What are the notable trends driving market growth?

Online Channel will witness New growth avenue in Coming Future.

7. Are there any restraints impacting market growth?

Growth of Insurtech Partnerships.

8. Can you provide examples of recent developments in the market?

October 2023: DigiFinland enhanced digital public services with a USD 22.72 million Tietoevry partnership. This collaboration spans a robust seven-year contract period and aspires to develop and sustain digital solutions that will streamline Finland’s social and health care, emergency services, and other pivotal public sector services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Finland Life & Non-Life Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Finland Life & Non-Life Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Finland Life & Non-Life Insurance Industry?

To stay informed about further developments, trends, and reports in the Finland Life & Non-Life Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence