Key Insights

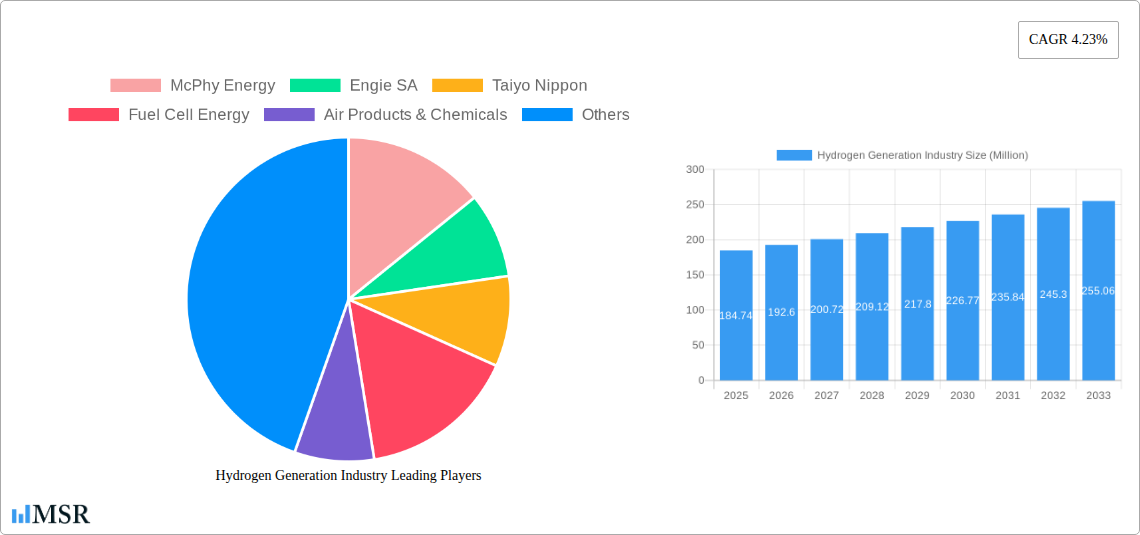

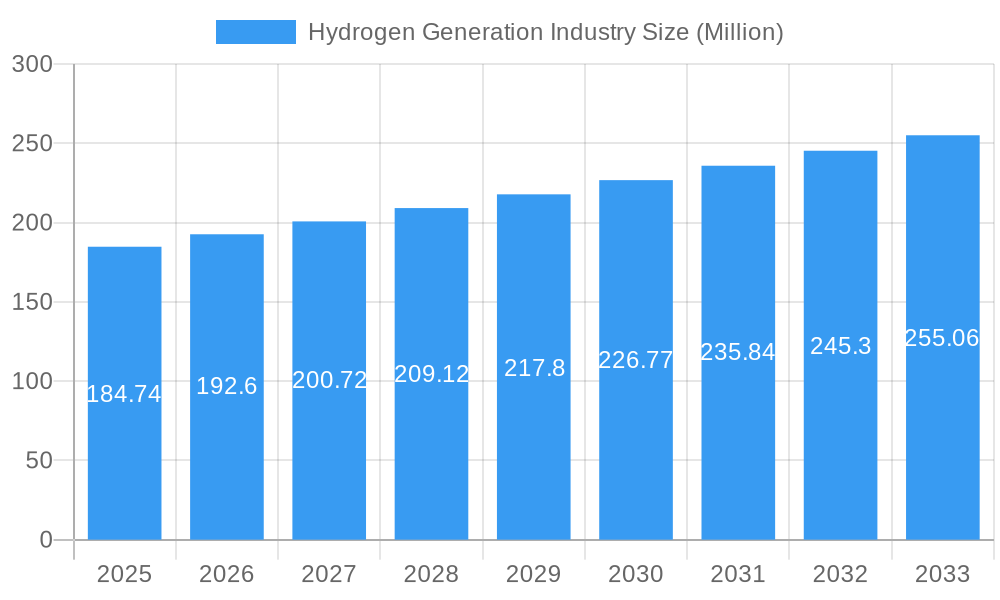

The global hydrogen generation market, valued at $184.74 million in 2025, is poised for substantial growth, exhibiting a Compound Annual Growth Rate (CAGR) of 4.23% from 2025 to 2033. This expansion is driven by the increasing demand for clean energy solutions and the growing adoption of hydrogen fuel cells in various sectors. Key drivers include stringent environmental regulations promoting decarbonization efforts, the escalating need for energy security, and technological advancements that are reducing the cost of hydrogen production, particularly for green hydrogen derived from renewable sources. The transition towards cleaner energy sources is significantly impacting the market, with green hydrogen experiencing faster growth compared to traditional grey hydrogen produced from natural gas. Furthermore, significant investments in research and development are fostering innovation in electrolysis technologies, improving efficiency and lowering production costs. The market is segmented by hydrogen color (blue, green, grey), production technology (steam methane reforming, coal gasification, others), and application (oil refining, chemical processing, iron & steel production, others). Leading companies such as Air Products & Chemicals, Linde plc, and ITM Power plc are actively shaping market dynamics through strategic partnerships, capacity expansions, and technological innovations. Geographical distribution showcases strong growth potential across North America, Europe, and Asia-Pacific, with government support and favorable policies further accelerating market penetration.

Hydrogen Generation Industry Market Size (In Million)

The market's growth trajectory, while promising, faces certain challenges. The high initial investment costs associated with hydrogen production facilities, particularly for green hydrogen, remain a barrier to entry for some players. Furthermore, the development of robust hydrogen infrastructure, including storage and transportation networks, is crucial for widespread market adoption and requires significant investment. Despite these constraints, the long-term prospects for the hydrogen generation market remain exceptionally positive, driven by global decarbonization goals and the increasing competitiveness of green hydrogen as renewable energy sources become more prevalent and cost-effective. The market is anticipated to witness a considerable upswing in the forecast period, driven by technological progress and favorable policy landscapes.

Hydrogen Generation Industry Company Market Share

Hydrogen Generation Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Hydrogen Generation Industry, offering crucial insights for investors, industry stakeholders, and strategic decision-makers. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report meticulously examines market dynamics, key players, technological advancements, and future growth prospects. The global hydrogen generation market is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period.

Hydrogen Generation Industry Market Concentration & Dynamics

The hydrogen generation market is characterized by a dynamic and evolving landscape, with a significant concentration of market share held by established global leaders. Key players such as Air Liquide, Linde plc, Engie SA, and Air Products & Chemicals continue to drive innovation and expansion, leveraging their robust infrastructure, advanced technological capabilities, and extensive international presence. Alongside these giants, a vibrant ecosystem of emerging companies is rapidly gaining traction, particularly in the burgeoning green hydrogen sector. This influx of new entrants is fostering heightened competition, driving significant technological advancements, and diversifying the market's offerings.

- Market Share: The top 5 players are projected to hold approximately 70-75% of the global market share by 2025, reflecting a consolidated yet competitive environment.

- M&A Activity: The past five years have witnessed over 30 strategic mergers and acquisitions, underscoring a strong trend of consolidation. These deals are primarily driven by the imperative to scale production capacity, accelerate technological breakthroughs, and expand geographical footprints to meet growing global demand.

- Innovation Ecosystems: Substantial investments in research and development are propelling innovation across a spectrum of hydrogen production technologies. A particular focus on green hydrogen is yielding significant reductions in production costs and substantial improvements in energy conversion efficiencies, making it increasingly viable.

- Regulatory Frameworks: Government initiatives worldwide, aimed at promoting renewable energy adoption and achieving ambitious carbon reduction targets, are profoundly shaping market dynamics. These policies are actively encouraging substantial investment in green hydrogen projects and are instrumental in defining the regulatory landscape for the industry.

- Substitute Products: While hydrogen remains a premier energy carrier for specific high-demand applications, emerging alternative energy sources and advanced energy storage technologies are presenting growing competition, particularly within the transportation sector.

- End-User Trends: Robust demand from foundational sectors such as oil refining, chemical processing, and iron & steel production continues to be a primary engine of market growth. Furthermore, the increasing adoption of hydrogen in the transportation sector for fuel cell vehicles and in grid-scale energy storage applications signifies a significant expansion of its end-use potential.

Hydrogen Generation Industry Insights & Trends

The hydrogen generation market is experiencing rapid growth, driven primarily by increasing concerns about climate change and the global push for decarbonization. The shift towards renewable energy sources is strongly impacting the industry, leading to a surge in investments in green hydrogen production. This segment is anticipated to experience the fastest growth, propelled by technological advancements, supportive government policies, and growing consumer awareness of environmental sustainability. The market size is estimated at xx Million in 2025, with an anticipated growth to xx Million by 2033. Several technological disruptions are transforming the industry, including advancements in electrolysis technologies, which are making green hydrogen production increasingly cost-competitive. Changing consumer behaviors, particularly a growing preference for sustainable products and services, are further bolstering the market's growth trajectory.

Key Markets & Segments Leading Hydrogen Generation Industry

Dominant Regions & Segments:

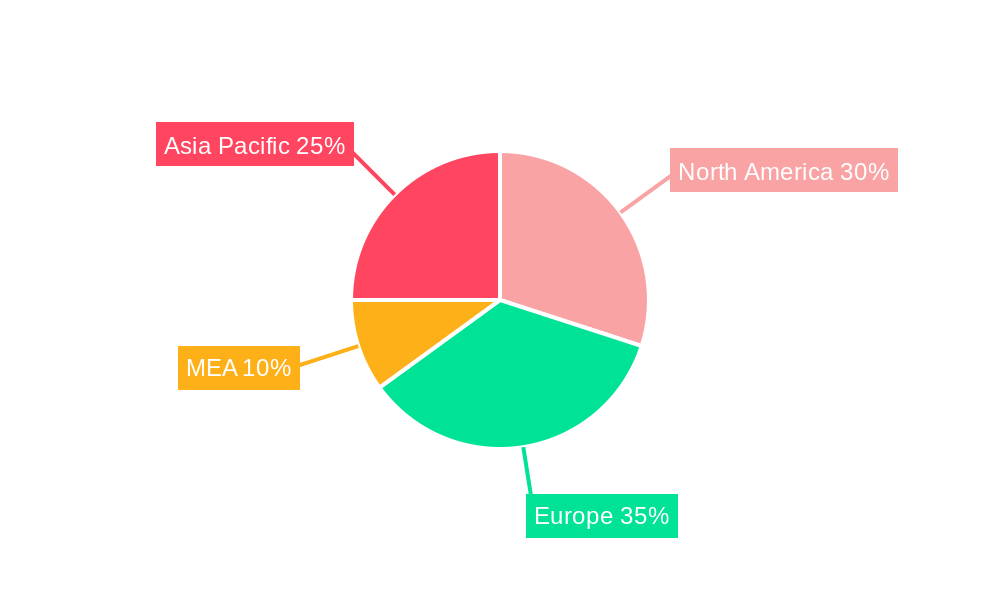

Region: Europe is currently the leading market, followed by North America and Asia-Pacific. Europe's strong commitment to renewable energy, coupled with substantial governmental support, fuels this dominance.

Source: Grey hydrogen currently dominates the market due to its established infrastructure and lower initial costs. However, green hydrogen is witnessing rapid growth due to increasing environmental concerns and supportive government policies. Blue hydrogen occupies a niche market.

Technology: Steam Methane Reforming (SMR) remains the dominant technology, but electrolysis technologies are rapidly gaining traction, particularly alkaline and proton exchange membrane (PEM) electrolysis. Coal gasification is gradually declining due to environmental concerns.

Application: Oil refining, chemical processing, and iron & steel production are the major application segments, but the burgeoning hydrogen fuel cell vehicle sector is emerging as a significant growth driver.

Drivers by Segment:

- Grey Hydrogen: Existing infrastructure and lower production costs.

- Green Hydrogen: Growing environmental awareness and supportive government policies; Technological advancements reducing production costs.

- Blue Hydrogen: Bridging the gap between grey and green hydrogen.

- SMR: Established technology and relatively low capital costs.

- Electrolysis: Increasing efficiency and declining costs; Growing demand for green hydrogen.

- Oil Refining: Existing infrastructure and integration potential.

- Chemical Processing: Use in ammonia production and other chemical processes.

- Iron & Steel Production: Potential for decarbonizing the steel production process.

Hydrogen Generation Industry Product Developments

Recent breakthroughs in electrolysis technology, with a notable emphasis on Proton Exchange Membrane (PEM) electrolysis, are revolutionizing green hydrogen production by significantly reducing costs and enhancing energy efficiency. Concurrently, advancements in material science are leading to the development of more durable and higher-performing electrolyzers. These collective innovations are positioning green hydrogen as a compelling and cost-competitive alternative to traditional grey and blue hydrogen, thereby broadening its scope of application across a wider array of industrial and energy sectors. The parallel progress in developing efficient hydrogen storage and transportation solutions further solidifies hydrogen's role as a practical and economically viable energy carrier.

Challenges in the Hydrogen Generation Industry Market

The hydrogen generation industry confronts a multifaceted array of challenges. The substantial upfront capital investment required for green hydrogen production remains a significant hurdle. The development of extensive and specialized infrastructure, encompassing hydrogen pipelines, liquefaction facilities, and storage solutions, necessitates considerable planning and investment. The complexities associated with the safe and efficient transportation and distribution of hydrogen across vast distances also pose logistical and technical challenges. Furthermore, navigating diverse and sometimes inconsistent regulatory frameworks across different geographical regions can impede market expansion and project development. The inherent intermittency of renewable energy sources, often utilized for green hydrogen production, presents operational challenges in maintaining a consistent and reliable supply. Supply chain vulnerabilities, particularly concerning the sourcing of critical raw materials like rare earth elements essential for certain electrolysis technologies, could potentially constrain market growth. Finally, ongoing competition from established and emerging alternative energy sources and technologies continues to exert pressure on the hydrogen industry's market position and adoption rates.

Forces Driving Hydrogen Generation Industry Growth

The hydrogen generation industry is propelled by several key growth drivers. Firstly, stringent environmental regulations and carbon emission reduction targets are pushing industries to seek cleaner alternatives, with hydrogen emerging as a promising solution. Secondly, significant government subsidies and investments in green hydrogen projects are accelerating technology development and market adoption. Technological advancements are continually reducing the cost and improving the efficiency of hydrogen production, storage, and transportation. The growing demand from the transportation sector, particularly in fuel cell electric vehicles, represents another important growth catalyst. The increasing integration of hydrogen into existing energy infrastructure is also paving the way for wider market penetration.

Long-Term Growth Catalysts in the Hydrogen Generation Industry

Long-term growth in the hydrogen generation industry hinges on continued innovation in production technologies, leading to lower costs and improved efficiency. Strategic partnerships between technology developers, energy companies, and end-users are crucial to accelerate market adoption and infrastructure development. Expansion into new markets, particularly in developing economies with burgeoning energy demands, will unlock significant growth potential. The development of innovative storage and transportation solutions is vital to overcome logistical challenges and ensure the widespread use of hydrogen as an energy carrier.

Emerging Opportunities in Hydrogen Generation Industry

Emerging opportunities within the hydrogen generation industry include the development of novel production methods like high-temperature electrolysis, which promises higher efficiencies. The integration of hydrogen into broader energy systems, including grid-scale energy storage and power-to-gas applications, is creating new market avenues. The rising demand for hydrogen in industrial processes beyond traditional applications presents significant growth potential. Furthermore, exploring the use of hydrogen in hard-to-decarbonize sectors will expand its market reach.

Leading Players in the Hydrogen Generation Industry Sector

- McPhy Energy

- Engie SA

- Taiyo Nippon Sanso Corporation

- Fuel Cell Energy

- Air Products & Chemicals

- Linde plc

- Cummins Inc.

- Messer Group GmbH

- Air Liquide

- ITM Power plc

- Enapter

Key Milestones in Hydrogen Generation Industry Industry

- October 2023: H2B2 inaugurated its SoHyCal green hydrogen plant in Fresno, California, showcasing the deployment of advanced PEM electrolysis technology.

- October 2023: Hygenco Green Energies announced plans for a significant green hydrogen plant in Maharashtra, India, intended to supply Sterlite Technologies Ltd.

- May 2023: RWE and Westfalen Group revealed an ambitious joint venture to establish up to 70 hydrogen refueling stations across Germany by 2030, marking a crucial step in building hydrogen infrastructure.

Strategic Outlook for Hydrogen Generation Industry Market

The future of the hydrogen generation industry is bright, driven by the urgent need for decarbonization and the increasing competitiveness of green hydrogen. Continued technological advancements, coupled with supportive government policies and strategic industry collaborations, will unlock significant market growth. The development of a robust hydrogen infrastructure, including production, storage, and transportation networks, is crucial for realizing the full potential of hydrogen as a clean energy carrier. The industry's ability to successfully address the existing challenges and capitalize on emerging opportunities will determine its long-term success and contribution towards a sustainable energy future.

Hydrogen Generation Industry Segmentation

-

1. Source

- 1.1. Blue hydrogen

- 1.2. Green hydrogen

- 1.3. Grey Hydrogen

-

2. Technology

- 2.1. Steam Methane Reforming (SMR)

- 2.2. Coal Gasification

- 2.3. Other Technologies

-

3. Application

- 3.1. Oil Refining

- 3.2. Chemical Processing

- 3.3. Iron & Steel Production

- 3.4. Other Applications

Hydrogen Generation Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. France

- 2.3. Italy

- 2.4. United Kingdom

- 2.5. Russian Federation

- 2.6. Rest of Europe

- 3. Middle East

-

4. Saudi Arabia

- 4.1. United Arab Emirates

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. Rest of Asia Pacific

-

6. South America

- 6.1. Brazil

- 6.2. Argentina

- 6.3. Rest of South America

Hydrogen Generation Industry Regional Market Share

Geographic Coverage of Hydrogen Generation Industry

Hydrogen Generation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.23% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MSR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Source

- 5.1.1. Blue hydrogen

- 5.1.2. Green hydrogen

- 5.1.3. Grey Hydrogen

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Steam Methane Reforming (SMR)

- 5.2.2. Coal Gasification

- 5.2.3. Other Technologies

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Oil Refining

- 5.3.2. Chemical Processing

- 5.3.3. Iron & Steel Production

- 5.3.4. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Middle East

- 5.4.4. Saudi Arabia

- 5.4.5. Asia Pacific

- 5.4.6. South America

- 5.1. Market Analysis, Insights and Forecast - by Source

- 6. Global Hydrogen Generation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Source

- 6.1.1. Blue hydrogen

- 6.1.2. Green hydrogen

- 6.1.3. Grey Hydrogen

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Steam Methane Reforming (SMR)

- 6.2.2. Coal Gasification

- 6.2.3. Other Technologies

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Oil Refining

- 6.3.2. Chemical Processing

- 6.3.3. Iron & Steel Production

- 6.3.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Source

- 7. North America Hydrogen Generation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Source

- 7.1.1. Blue hydrogen

- 7.1.2. Green hydrogen

- 7.1.3. Grey Hydrogen

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Steam Methane Reforming (SMR)

- 7.2.2. Coal Gasification

- 7.2.3. Other Technologies

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Oil Refining

- 7.3.2. Chemical Processing

- 7.3.3. Iron & Steel Production

- 7.3.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Source

- 8. Europe Hydrogen Generation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Source

- 8.1.1. Blue hydrogen

- 8.1.2. Green hydrogen

- 8.1.3. Grey Hydrogen

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Steam Methane Reforming (SMR)

- 8.2.2. Coal Gasification

- 8.2.3. Other Technologies

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Oil Refining

- 8.3.2. Chemical Processing

- 8.3.3. Iron & Steel Production

- 8.3.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Source

- 9. Middle East Hydrogen Generation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Source

- 9.1.1. Blue hydrogen

- 9.1.2. Green hydrogen

- 9.1.3. Grey Hydrogen

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Steam Methane Reforming (SMR)

- 9.2.2. Coal Gasification

- 9.2.3. Other Technologies

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Oil Refining

- 9.3.2. Chemical Processing

- 9.3.3. Iron & Steel Production

- 9.3.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Source

- 10. Saudi Arabia Hydrogen Generation Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Source

- 10.1.1. Blue hydrogen

- 10.1.2. Green hydrogen

- 10.1.3. Grey Hydrogen

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Steam Methane Reforming (SMR)

- 10.2.2. Coal Gasification

- 10.2.3. Other Technologies

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Oil Refining

- 10.3.2. Chemical Processing

- 10.3.3. Iron & Steel Production

- 10.3.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Source

- 11. Asia Pacific Hydrogen Generation Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Source

- 11.1.1. Blue hydrogen

- 11.1.2. Green hydrogen

- 11.1.3. Grey Hydrogen

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Steam Methane Reforming (SMR)

- 11.2.2. Coal Gasification

- 11.2.3. Other Technologies

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Oil Refining

- 11.3.2. Chemical Processing

- 11.3.3. Iron & Steel Production

- 11.3.4. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Source

- 12. South America Hydrogen Generation Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Source

- 12.1.1. Blue hydrogen

- 12.1.2. Green hydrogen

- 12.1.3. Grey Hydrogen

- 12.2. Market Analysis, Insights and Forecast - by Technology

- 12.2.1. Steam Methane Reforming (SMR)

- 12.2.2. Coal Gasification

- 12.2.3. Other Technologies

- 12.3. Market Analysis, Insights and Forecast - by Application

- 12.3.1. Oil Refining

- 12.3.2. Chemical Processing

- 12.3.3. Iron & Steel Production

- 12.3.4. Other Applications

- 12.1. Market Analysis, Insights and Forecast - by Source

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 McPhy Energy

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Engie SA

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Taiyo Nippon

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Fuel Cell Energy

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Air Products & Chemicals

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Linde plc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Cummins

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Messer Group GmbH

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Air Liquide

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 ITM Power plc

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Enapter

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.1 McPhy Energy

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Hydrogen Generation Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Hydrogen Generation Industry Revenue (Million), by Source 2025 & 2033

- Figure 3: North America Hydrogen Generation Industry Revenue Share (%), by Source 2025 & 2033

- Figure 4: North America Hydrogen Generation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 5: North America Hydrogen Generation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 6: North America Hydrogen Generation Industry Revenue (Million), by Application 2025 & 2033

- Figure 7: North America Hydrogen Generation Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Hydrogen Generation Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Hydrogen Generation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Hydrogen Generation Industry Revenue (Million), by Source 2025 & 2033

- Figure 11: Europe Hydrogen Generation Industry Revenue Share (%), by Source 2025 & 2033

- Figure 12: Europe Hydrogen Generation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 13: Europe Hydrogen Generation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 14: Europe Hydrogen Generation Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Europe Hydrogen Generation Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Hydrogen Generation Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Hydrogen Generation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East Hydrogen Generation Industry Revenue (Million), by Source 2025 & 2033

- Figure 19: Middle East Hydrogen Generation Industry Revenue Share (%), by Source 2025 & 2033

- Figure 20: Middle East Hydrogen Generation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 21: Middle East Hydrogen Generation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Middle East Hydrogen Generation Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Middle East Hydrogen Generation Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Middle East Hydrogen Generation Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East Hydrogen Generation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Saudi Arabia Hydrogen Generation Industry Revenue (Million), by Source 2025 & 2033

- Figure 27: Saudi Arabia Hydrogen Generation Industry Revenue Share (%), by Source 2025 & 2033

- Figure 28: Saudi Arabia Hydrogen Generation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 29: Saudi Arabia Hydrogen Generation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 30: Saudi Arabia Hydrogen Generation Industry Revenue (Million), by Application 2025 & 2033

- Figure 31: Saudi Arabia Hydrogen Generation Industry Revenue Share (%), by Application 2025 & 2033

- Figure 32: Saudi Arabia Hydrogen Generation Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Saudi Arabia Hydrogen Generation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Asia Pacific Hydrogen Generation Industry Revenue (Million), by Source 2025 & 2033

- Figure 35: Asia Pacific Hydrogen Generation Industry Revenue Share (%), by Source 2025 & 2033

- Figure 36: Asia Pacific Hydrogen Generation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 37: Asia Pacific Hydrogen Generation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 38: Asia Pacific Hydrogen Generation Industry Revenue (Million), by Application 2025 & 2033

- Figure 39: Asia Pacific Hydrogen Generation Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Asia Pacific Hydrogen Generation Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Asia Pacific Hydrogen Generation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Hydrogen Generation Industry Revenue (Million), by Source 2025 & 2033

- Figure 43: South America Hydrogen Generation Industry Revenue Share (%), by Source 2025 & 2033

- Figure 44: South America Hydrogen Generation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 45: South America Hydrogen Generation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 46: South America Hydrogen Generation Industry Revenue (Million), by Application 2025 & 2033

- Figure 47: South America Hydrogen Generation Industry Revenue Share (%), by Application 2025 & 2033

- Figure 48: South America Hydrogen Generation Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: South America Hydrogen Generation Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hydrogen Generation Industry Revenue Million Forecast, by Source 2020 & 2033

- Table 2: Global Hydrogen Generation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 3: Global Hydrogen Generation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Hydrogen Generation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Hydrogen Generation Industry Revenue Million Forecast, by Source 2020 & 2033

- Table 6: Global Hydrogen Generation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 7: Global Hydrogen Generation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Hydrogen Generation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Hydrogen Generation Industry Revenue Million Forecast, by Source 2020 & 2033

- Table 13: Global Hydrogen Generation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 14: Global Hydrogen Generation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 15: Global Hydrogen Generation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: United Kingdom Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Russian Federation Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Hydrogen Generation Industry Revenue Million Forecast, by Source 2020 & 2033

- Table 23: Global Hydrogen Generation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 24: Global Hydrogen Generation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 25: Global Hydrogen Generation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global Hydrogen Generation Industry Revenue Million Forecast, by Source 2020 & 2033

- Table 27: Global Hydrogen Generation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 28: Global Hydrogen Generation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 29: Global Hydrogen Generation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: United Arab Emirates Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: South Africa Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Rest of Middle East and Africa Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Global Hydrogen Generation Industry Revenue Million Forecast, by Source 2020 & 2033

- Table 34: Global Hydrogen Generation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 35: Global Hydrogen Generation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 36: Global Hydrogen Generation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: China Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: India Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Japan Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: South Korea Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: Rest of Asia Pacific Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Global Hydrogen Generation Industry Revenue Million Forecast, by Source 2020 & 2033

- Table 43: Global Hydrogen Generation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 44: Global Hydrogen Generation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 45: Global Hydrogen Generation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 46: Brazil Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 47: Argentina Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Rest of South America Hydrogen Generation Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hydrogen Generation Industry?

The projected CAGR is approximately 4.23%.

2. Which companies are prominent players in the Hydrogen Generation Industry?

Key companies in the market include McPhy Energy, Engie SA, Taiyo Nippon, Fuel Cell Energy, Air Products & Chemicals, Linde plc, Cummins, Messer Group GmbH, Air Liquide, ITM Power plc, Enapter.

3. What are the main segments of the Hydrogen Generation Industry?

The market segments include Source, Technology, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 184.74 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Favorable Government Policies4.; Increasing Demand From Refinery and Industrial Sector.

6. What are the notable trends driving market growth?

Oil Refining Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Higher Production Cost.

8. Can you provide examples of recent developments in the market?

October 2023: H2B2, a technology company with a portfolio in Hydrogen production systems, unveiled the green hydrogen plant, which is expected to become operational in North America, the SoHyCal facility located in Fresno, California, United States. The project envisages 100 percent clean hydrogen production using PEM technology.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hydrogen Generation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hydrogen Generation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hydrogen Generation Industry?

To stay informed about further developments, trends, and reports in the Hydrogen Generation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence